|

市場調查報告書

商品編碼

2062416

電子指南針:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)E-Compass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

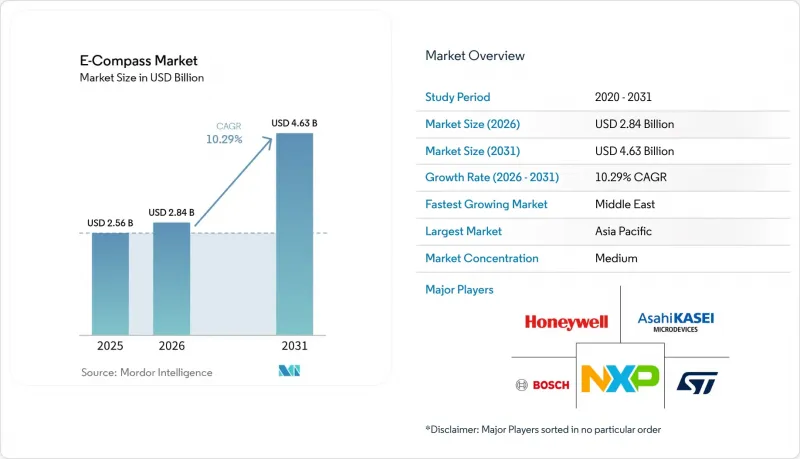

根據 Mordor Intelligence 預測,電子指南針市場規模預計將在 2025 年達到 25.6 億美元,2026 年達到 28.4 億美元,到 2031 年達到 46.3 億美元,2026 年至 2031 年的複合年成長率為 10.29%。

本報告按技術(霍爾效應、異向性、巨磁阻、隧道磁阻、磁通門等)、軸向(1-2軸、3軸、6軸和9軸感測器融合)、應用(家用電子電器等)、外形規格(分立式指南針模組、整合感測器組合、SoC整合電子指南針等)和地區進行細分。市場預測以美元(USD)為單位。

全球電子指南針市場趨勢與洞察

配備導航感應器的智慧型手機的普及

到2025年,智慧型手機用戶數量將達到69億,幾乎所有中階和旗艦機型都將整合一個9軸感測器中心,該中心整合了磁力計、加速計和陀螺儀數據,用於擴增實境(AR)疊加和室內導航。此整合組合模組可將組件成本降低25%,並實現小於1毫米的封裝高度,適用於折疊式顯示器。目前,在GNSS不可用時,地鐵和購物中心的行人定位主要依賴基於磁力計的方向資訊。旭化成將於2025年10月發布的AK09974C晶片實現了極致的微型化,在晶圓級1.2×1.2毫米封裝中達到了0.15µT的解析度。由於只有不到40%的使用者會進行手動8字形校準,因此廠商正在開發基於從數百萬條運動軌跡中收集的機器學習模型的自動校準功能。

ADAS在乘用車和商用車中的廣泛應用

到2025年,45%的新乘用車將配備高級駕駛輔助系統(ADAS),所有達到L2級或更高級別的平台都將至少整合一個6軸或9軸慣性測量單元(IMU),以滿足ISO 26262的功能安全要求。這些IMU內建的磁力計可補償長途高速公路行駛過程中陀螺儀的漂移,從而防止累積方向誤差。 TDK的「PositionSense」系統已於2024年獲得AEC-Q100 1級認證,目前正向歐洲和日本的OEM廠商供貨,並正在為2027年的車型上市做準備。車隊營運商正在部署配備指南針的車載資訊系統盒,透過最佳化路線降低3-5%的油耗,從而抵消15-25美元的額外感測器成本。從 2024 年起,歐盟將強制實施緊急煞車和車道維持系統,但這將繼續增加事故率。

易受磁干擾和校準漂移的影響

周圍的鐵質物體和電流環路會造成超過 500µT 的磁干擾,遠超地球磁場(25–65µT),導致智慧型手機、機器人和無人機的定向誤差超過 30 度。都市區高層建築、地鐵軌道和工廠馬達進一步加劇了這種干擾。只有 60% 的終端使用者會進行手動校準,而殘餘偏移會降低室內導航的精確度。雖然汽車系統透過將 GNSS 與車輪速度編碼器融合來減輕漂移,但固定式服務機器人卻不得不依賴查找表和定期更新的磁異常圖。 2025 年 12 月,旭化成與 Aizip 合作,利用群眾外包方式取得磁場圖,將校準週期從數天縮短至數小時。

細分市場分析

到2025年,霍爾效應感測器和TMR感測器的銷售額將佔總銷售額的42.19%。這主要歸功於其亞納特斯拉級的靈敏度和熱穩定性,符合AEC-Q100和IEC 61508標準,適用於動力傳動系統、航空電子設備和工廠自動化等領域。隨著汽車製造商和工業系統整合商在長生命週期平台上採用這種架構,TMR模組的電子指南針市場預計將以穩定的中等個位數成長率成長。霍爾效應感測器由於單價低於0.40美元,在成本受限的行動電話市場中保持著一定的市場佔有率,但其10µT的噪音基底限制了其精度,使其僅能達到約5度,這限制了其在高階產品中的應用。磁通門指南針可為潛水艇和飛機提供亞1度的精度,但其50-200mW的功耗使其仍處於小眾市場。

採用氮空位鑽石或光激發鹼性蒸氣電池的量子指南針預計到2031年將以10.99%的複合年成長率成長,成為電子指南針市場中成長最快的產品。這主要歸功於它們在國防和潛艇等對方位角漂移極其敏感的環境中,具有極強的抗磁干擾能力。 2024年的實驗室記錄顯示,其精度可達0.1度,目前原型產品正在自動駕駛車輛中進行測試。 Q-Nav等供應商正在將鑽石感測器與FPGA控制器整合,以過濾微波驅動噪聲,從而將機殼尺寸縮小至45立方厘米。儘管功耗是傳統電子羅盤的5到10倍,但世界各國政府仍在資助試點部署,因為他們預計在無人潛水器和太空平台中,精度將比電池壽命更為重要。同時,晶片級光激發蒸氣電池的研發預計在2030年前將量子模組的尺寸縮小至數立方公分。

即使到了2025年,三軸指南針的出貨量仍佔61.18%。這主要得益於智慧型手機和無人機的成本控制以及成熟的傳統軟體堆疊。同時,單軸和雙軸電子指南針的市佔率下降至12%,因為開發人員傾向於避免機械對準的限制。整合加速計和陀螺儀的六軸和九軸封裝預計將在2026年至2031年間成長10.57%。這主要得益於汽車行業的一級供應商轉向採用單系統級封裝(SiP)單元,這種封裝可將基板面積減少40%,並支援緊耦合卡爾曼濾波器。

在汽車領域,雙9軸配置提供冗餘,即使一個感測器故障,也能確保車輛自動回正,符合ISO 26262合規性要求。在穿戴式裝置中,9軸中心用於手勢辨識和跌倒偵測,磁力計資料在區分旋轉和平移時可將分類精度提高15%。 PNI Sensors基於RM3100的NaviGuider整合了連續硬鐵和軟鐵自動校準功能,主要面向無法浮出水面進行日常手動操作的水上滑翔機。隨著下游韌體統一感測器融合庫,製造商正從獨立指南針轉向整合中心,這些整合中心能夠以200 Hz的頻率將四元數向量直接輸出到應用處理器,從而縮短開發時間。

區域分析

預計到2025年,亞太地區將佔據全球市場規模的48.79%,主要驅動力來自中國、日本和韓國,這三國將供應全球整體約70%的霍爾效應和自適應磁阻(AMR)晶片。儘管亞太地區企業在電子指南針市場佔有較大佔有率,但由於汽車業的認證週期超過24個月,以及原始設備製造商(OEM)對零缺陷供貨的要求,其利潤率正面臨壓力。中國透過國內行動電話和電動車組裝消化了亞太地區35%的出貨量,但對高等級磁通門和量子感測器的出口限制制約了其在國防領域的應用,促使像Bewis Sensing這樣的國內企業填補這一市場空白。

日本和韓國專注於汽車級三極管磁阻 (TMR) 和整合式慣性測量單元 (IMU) 模組的生產,並與歐洲和北美原始設備製造商 (OEM) 簽訂了長期協議,確保供應量直至 2028 年。印度正在崛起為重要的電子製造地,並獲得了 2024 年至 2025 年 12 億美元的電子製造業扶持計畫的支持,正逐步確立其在消費和工業市場低成本替代方案的地位。亞太地區的電子指南針市場規模預計將穩定成長,但成長速度將低於歐洲和北美。

中東地區呈現最快成長勢頭,預計2031年複合年成長率將達到19.84%。這主要得益於沙烏地阿拉伯「2030願景」推動了當地感測器生產,以及國防項目採購不受《國際武器貿易條例》(ITAR)約束的導航系統。泰萊公司(Teledyne)位於達曼的工廠將於2025年運作,克羅內公司(Krone)也將於2026年簽署本地生產合作備忘錄,這些都將進一步推動區域供應鏈的發展。北美和歐洲合計佔2025年銷售額的32%,主要得益於航太、國防和工業機器人領域的強勁需求,這些領域需要抗輻射且具有傾斜補償功能的指南針。南美洲的市佔率不足5%,但巴西和阿根廷精密農業的進步正在推動GNSS輔助指南針陣列的應用,從而實現公分級行間導航。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

- 市場促進因素

- 配備導航感應器的智慧型手機的普及

- ADAS在乘用車和商用車中的廣泛應用

- 透過MEMS製程實現小型化和成本降低

- 穿戴式裝置和 XR 裝置的普及推動了對超薄指南針的需求。

- 需要傾斜校正姿態的自主海上無人機

- 配備電子指南針陣列的精密農業機器人,用於行間引導。

- 市場限制因素

- 易受磁干擾和校準漂移的影響

- 消費性電子產品原物料價格面臨壓力

- 磁通閘和量子指南針設計中的高功耗

- 高靈敏度磁通門模組的出口限制

第5章 市場規模與成長預測

- 透過技術

- 霍爾效應

- 異向性、巨型、隧道磁阻

- 磁通門

- 磁感應型

- 量子

- 按軸向

- 1-2軸

- 3軸

- 6軸和9軸感測器融合

- 透過使用

- 家用電子產品

- 車

- 航太/國防

- 工業與機器人

- 海洋和海底

- 醫療保健和穿戴式設備

- 按外形規格

- 離散指南針模組

- 整合感測器組合

- 片上整合式電子指南針

- 開發板和客製化ASIC

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- STMicroelectronics NV

- Honeywell International Inc.

- Robert Bosch GmbH(Bosch Sensortec GmbH)

- Asahi Kasei Microdevices Corporation

- NXP Semiconductors NV

- TDK Corporation(Invensense Inc.)

- MEMSIC Semiconductor(Shanghai)Co., Ltd.

- PNI Sensor Corporation

- Analog Devices, Inc.

- Alps Alpine Co., Ltd.

- Infineon Technologies AG

- TE Connectivity Ltd.

- Shanghai Bewis Sensing Technology LLC

- Ericco International Limited

- Jewell Instruments, LLC

- Melexis NV

- MagnaChip Semiconductor Corp.

- Renesas Electronics Corporation

- Lake Shore Cryotronics, Inc.

- VectorNav Technologies, LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the e-Compass market size is projected to be USD 2.56 billion in 2025, USD 2.84 billion in 2026, and reach USD 4.63 billion by 2031, growing at a CAGR of 10.29% from 2026 to 2031.

This report is Segmented by Technology (Hall-Effect, Anisotropic, Giant, Tunnel Magneto-Resistive, Fluxgate, and More), Axis Orientation (1-2-Axis, 3-Axis, and 6- and 9-Axis Sensor-Fusion), Application (Consumer Electronics, and More), Form Factor (Discrete Compass Modules, Integrated Sensor-Combo, SoC-Embedded E-Compass, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global E-Compass Market Trends and Insights

Proliferation of Smartphones Integrating Navigation Sensors

Smartphone subscriptions stood at 6.9 billion in 2025, and virtually every mid-tier or flagship handset embeds a 9-axis sensor hub that blends magnetometer, accelerometer, and gyroscope data for augmented-reality overlays and indoor navigation. Integrated combo modules trimmed bill-of-material cost by 25% and enabled sub-1 millimeter package heights suitable for foldable displays. Pedestrian dead-reckoning in subways and malls now depends on magnetometer-driven heading when GNSS is unavailable. Asahi Kasei's AK09974C, released in October 2025, achieves 0.15 µT resolution in a wafer-level 1.2 X 1.2 mm package, showcasing aggressive miniaturization. Because fewer than 40% of users perform manual figure-eight calibration, vendors are building auto-calibration based on machine-learning models harvested from millions of motion traces.

Rising Adoption of ADAS in Passenger and Commercial Vehicles

Advanced Driver Assistance Systems (ADAS) were shipped in 45% of new passenger vehicles in 2025, and each Level 2+ platform includes at least one 6-axis or 9-axis inertial measurement unit to meet ISO 26262 functional-safety requirements. Magnetometers within these IMUs correct gyroscope drift during prolonged highway driving, preventing cumulative heading error. TDK's PositionSense, qualified to AEC-Q100 Grade 1 in 2024, now ships to European and Japanese OEMs, prepping 2027 model launches. Fleet operators add compass-equipped telematics boxes that shave 3-5% fuel through optimized routing, offsetting the USD 15-25 incremental sensor cost. Mandatory emergency braking and lane-keeping systems introduced in the European Union from 2024 onward continue to elevate accident rates.

Susceptibility to Magnetic Interference and Calibration Drift

Local ferrous objects and current loops create magnetic disturbances exceeding 500 µT, orders above Earth's 25-65 µT field, causing heading errors beyond 30 degrees in phones, robots, and drones. Urban skyscrapers, subway rails, and factory motors exacerbate distortion. Only 60% of end users complete manual calibration, leaving a residual offset that degrades indoor navigation. Automotive systems mitigate drift by fusing GNSS and wheel-speed encoders, but stationary service robots must rely on lookup tables or periodically updated magnetic-anomaly maps. Asahi Kasei partnered with Aizip in December 2025 to crowd-source magnetic-field maps that shorten calibration cycles from days to hours.

Other drivers and restraints analyzed in the detailed report include:

- Miniaturization and Cost Reduction Through MEMS Processes

- Expansion of Wearable and XR Devices Demanding Ultrathin Compasses

- Commodity Pricing Pressure in Consumer-Grade Devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hall-effect, TMR sensors commanded 42.19% of 2025 revenue, anchored by sub-nanotesla sensitivity and thermal stability that meet AEC-Q100 and IEC 61508 norms for powertrain, avionics, and factory automation. The E-Compass market for TMR modules is set to grow at a steady, high-single-digit pace as carmakers and industrial integrators choose the architecture for long-life-cycle platforms. Hall-effect alternatives keep share in cost-constrained phones because their unit cost stays below USD 0.40, but their 10 µT noise floor caps accuracy at around 5 degrees, a ceiling that limits premium adoption. Fluxgate compasses deliver sub-degree precision for submarines and aircraft, but consume 50-200 mW, so they remain niche.

Quantum compasses using nitrogen-vacancy diamond or optically pumped alkali vapor cells are poised to grow at a 10.99% CAGR through 2031, the fastest in the E-Compass market, because they resist magnetic interference in defense and subsea environments where heading drift is unacceptable. A 2024 laboratory record showed 0.1-degree accuracy, and prototypes are undergoing trials on autonomous vehicles. Vendors such as Q-Nav are packaging diamond sensors with FPGA controllers that filter microwave drive noise, slimming form factors to 45 cm3. Governments fund pilot deployments despite 5-10X higher power draw, betting that unmanned underwater or space platforms will prioritize accuracy over battery life. Parallel R&D in chip-scale optically pumped vapor cells could shrink quantum modules to several cubic centimeters by 2030.

Three-axis compasses still accounted for 61.18% of shipments in 2025 because they meet the cost ceilings for smartphones and drones and have well-understood legacy software stacks. E-Compass market share for single-axis and dual-axis units slipped to 12% as developers reject mechanical alignment constraints. Six-axis and nine-axis packages that integrate accelerometers and gyroscopes are forecast to rise 10.57% over 2026-2031, helped by automotive Tier-1 moves to single-system-in-package units that save 40% of board area and enable tightly coupled Kalman filters.

In the automotive domain, dual 9-axis setups provide redundancy to meet ISO 26262 compliance requirements, ensuring limp-home steering even if one sensor fails. Wearables exploit 9-axis hubs to recognize gestures and detect falls, as magnetometer data improves classifier accuracy by 15% when distinguishing rotation from translation. PNI Sensor's RM3100-based NaviGuider bundles continuous hard-iron and soft-iron autocalibration, aimed at ocean gliders that cannot surface for manual routines. As downstream firmware unifies sensor-fusion libraries, manufacturers are transitioning from discrete compasses to integrated hubs that deliver quaternion vectors at 200 Hz directly to application processors, reducing development time.

Geography Analysis

Asia-Pacific accounted for 48.79% of the 2025 value, driven by China, Japan, and South Korea, which supply roughly 70% of the global Hall-effect and AMR dies. Despite the large E-Compass market share, regional players face margin compression because automotive qualification cycles stretch past 24 months and OEMs demand zero-defect supply. China absorbs 35% of local shipments through domestic phone and EV assembly, yet export restrictions on high-grade fluxgate and quantum sensors limit defense uptake, spurring indigenous firms like Bewis Sensing to fill the gap.

Japan and South Korea specialize in automotive-grade TMR and integrated IMU modules under long-term contracts with European and North American OEMs that guarantee volume until 2028. India is emerging as a leading electronics manufacturing hub, supported by electronics manufacturing incentives totaling USD 1.2 billion during 2024-2025, positioning the country as a low-cost alternative for consumer and industrial markets. The E-Compass market size in Asia-Pacific is expected to expand steadily but at slower margins than in Western regions.

The Middle East shows the fastest trajectory, slated for a 19.84% CAGR through 2031, as Saudi Vision 2030 drives local sensor production and defense programs procure ITAR-free navigation systems. Teledyne's 2025 launch of its Dammam plant and KROHNE's 2026 localization MoU underscore thee riseof regional supply chains. North America and Europe together accounted for 32% of 2025 revenue, driven by the aerospace, defense, and industrial robotics sectors, which demand radiation-hardened, tilt-compensated compasses. South America remained below 5%, but precision agriculture in Brazil and Argentina is prompting the adoption of GNSS-aided compass arrays for centimeter-level row guidance.

- STMicroelectronics N.V.

- Honeywell International Inc.

- Robert Bosch GmbH (Bosch Sensortec GmbH)

- Asahi Kasei Microdevices Corporation

- NXP Semiconductors N.V.

- TDK Corporation (Invensense Inc.)

- MEMSIC Semiconductor (Shanghai) Co., Ltd.

- PNI Sensor Corporation

- Analog Devices, Inc.

- Alps Alpine Co., Ltd.

- Infineon Technologies AG

- TE Connectivity Ltd.

- Shanghai Bewis Sensing Technology LLC

- Ericco International Limited

- Jewell Instruments, LLC

- Melexis N.V.

- MagnaChip Semiconductor Corp.

- Renesas Electronics Corporation

- Lake Shore Cryotronics, Inc.

- VectorNav Technologies, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Supply-Chain Analysis

- 4.3 Regulatory Landscape

- 4.4 Technological Outlook

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Market Drivers

- 4.7.1 Proliferation of Smartphones Integrating Navigation Sensors

- 4.7.2 Rising Adoption of ADAS in Passenger and Commercial Vehicles

- 4.7.3 Miniaturization and Cost Reduction Through MEMS Processes

- 4.7.4 Expansion of Wearable and XR Devices Demanding Ultrathin Compasses

- 4.7.5 Autonomous Maritime Drones Needing Tilt-Compensated Heading

- 4.7.6 Precision-Ag-Robots Deploying Row-Guidance E-Compass Arrays

- 4.8 Market Restraints

- 4.8.1 Susceptibility to Magnetic Interference and Calibration Drift

- 4.8.2 Commodity Pricing Pressure in Consumer-Grade Devices

- 4.8.3 High Power Consumption in Fluxgate and Quantum Compass Designs

- 4.8.4 Export-Control Limits on High-Sensitivity Fluxgate Modules

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Hall-Effect

- 5.1.2 Anisotropic, Giant, Tunnel Magneto-Resistive

- 5.1.3 Fluxgate

- 5.1.4 Magneto-Inductive

- 5.1.5 Quantum

- 5.2 By Axis Orientation

- 5.2.1 1-2-Axis

- 5.2.2 3-Axis

- 5.2.3 6- and 9-Axis Sensor-Fusion

- 5.3 By Application

- 5.3.1 Consumer Electronics

- 5.3.2 Automotive

- 5.3.3 Aerospace and Defense

- 5.3.4 Industrial and Robotics

- 5.3.5 Marine and Sub-Sea

- 5.3.6 Healthcare and Wearables

- 5.4 By Form Factor

- 5.4.1 Discrete Compass Modules

- 5.4.2 Integrated Sensor-Combo

- 5.4.3 SoC-Embedded E-Compass

- 5.4.4 Dev-Boards and Custom ASICs

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 STMicroelectronics N.V.

- 6.4.2 Honeywell International Inc.

- 6.4.3 Robert Bosch GmbH (Bosch Sensortec GmbH)

- 6.4.4 Asahi Kasei Microdevices Corporation

- 6.4.5 NXP Semiconductors N.V.

- 6.4.6 TDK Corporation (Invensense Inc.)

- 6.4.7 MEMSIC Semiconductor (Shanghai) Co., Ltd.

- 6.4.8 PNI Sensor Corporation

- 6.4.9 Analog Devices, Inc.

- 6.4.10 Alps Alpine Co., Ltd.

- 6.4.11 Infineon Technologies AG

- 6.4.12 TE Connectivity Ltd.

- 6.4.13 Shanghai Bewis Sensing Technology LLC

- 6.4.14 Ericco International Limited

- 6.4.15 Jewell Instruments, LLC

- 6.4.16 Melexis N.V.

- 6.4.17 MagnaChip Semiconductor Corp.

- 6.4.18 Renesas Electronics Corporation

- 6.4.19 Lake Shore Cryotronics, Inc.

- 6.4.20 VectorNav Technologies, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment