|

市場調查報告書

商品編碼

2062393

冷屋頂:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Cool Roof - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

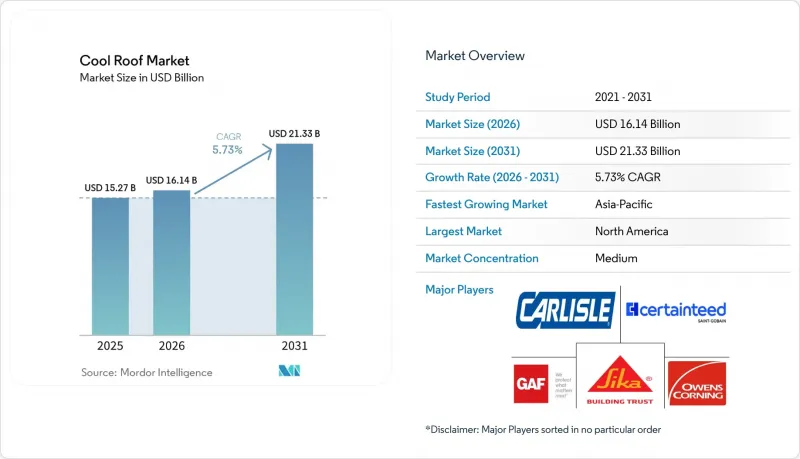

據 Mordor Intelligence 稱,2025 年冷屋頂市場價值 152.7 億美元,預計到 2031 年將達到 213.3 億美元,而 2026 年為 161.4 億美元,預測期(2026-2031 年)複合年成長率為 5.73%。

本報告按屋頂類型(低坡度屋頂、陡坡度屋頂、平屋頂)、材料類型(冷屋頂塗料、單層薄膜等)、塗料化學成分(丙烯酸、彈性體、矽酮等)、應用領域(商業建築、住宅、其他)和地區(亞太地區、北美地區、歐洲、其他地區)進行細分。市場預測以美元計價。

全球冷屋頂市場趨勢與洞察

能源效率法規與零碳排放義務

在各個司法管轄區,最低太陽反射率(SRI)基準值正被直接納入建築規範,取消了先前允許開發商使用額外隔熱材料而非反射屋頂的權衡選擇。一項旨在2030年實現新建築零排放的歐盟指令要求建築師在設計初期就採用冷屋頂。同時,中國的性能標準GB 55015-2021實際上強制要求使用高反射率屋頂材料,以實現約30%的節能目標。印度的《2024年生態住宅標準》(Eco-Niwas Samhita 2024)對屋頂的U值設定了數值上限,並規定緩坡屋頂的初始反射率必須達到0.6,這表明冷屋頂市場正在大力推進監管。在美國,LEED v5 將低坡度屋頂結構的太陽反射率 (SRI) 要求提高至初始值 82 和老化後值 64,迫使製造商修改塗料配方以抵禦污染造成的劣化下降。這些監管變化正在加速規範制定,縮短投資回收期,並刺激材料創新和供應鏈擴張。

城市熱島效應緩解計劃

在城市中,用於建造冷屋頂的公共基礎設施正獲得越來越多的資金支持,以降低夏季尖峰時段的能源需求和環境溫度。例如,亞特蘭大2025年的法令適用於面積超過10,000平方英尺的商業建築,預計到2035年將累積節省3.1億美元的能源費用。海德拉巴的計畫目標是到2028年安裝3億平方公尺的冷屋頂,將室內溫度降低高達攝氏4.5度C,並大幅節省冷氣能源。包括波士頓、蒙特婁和加州的幾個城市在內的其他城市也提供補貼,津貼低收入建築安裝冷屋頂。這些措施正在將需求從私人維修轉向公共採購,從而穩定供應商供應並擴大冷屋頂市場。

與傳統瀝青屋頂相比,初始成本較高

反射塗層的成本為每平方英尺 0.75 美元至 2.50 美元,TPO 薄膜的成本為每平方英尺 3.50 美元至 6.50 美元,而普通瀝青瓦的成本為每平方英尺 1.00 美元至 3 美元。這 50% 至 150% 的價格差異對成本敏感的建築商來說是一大障礙。在冷凍需求較低的溫帶地區,投資回收期可能超過五年,因此冷屋頂只能作為可選升級。拆除和處理現有屋頂的成本為每平方英尺 1 至 2 美元,但使用無需拆除的維修塗層可以將投資回收期縮短至五年以內。由於 PACE 融資允許透過房產稅分攤成本,目前涼爽屋頂的普及主要集中在加州和其他幾個州。在獎勵彌合這一成本差距之前,價格仍將是市場滲透的主要障礙。

細分市場分析

預計到2025年,低坡屋頂將佔總銷售額的44.87%,凸顯其在倉庫、購物中心和公共設施等建築冷屋頂市場的重要性。這類屋頂利用大面積連續面積來提高冷卻效率,並允許安裝安定器太陽能板而無需穿透防水卷材。 2025年採用的更為嚴格的中車三區氣候耐候性評估標準優先考慮具有持久反射率的防水卷材,這將推動對優質PVC和TPO產品的需求,從而促進冷屋頂市場的擴張。由於反射性瀝青瓦的成本溢價高達30-50%,且住宅通常更注重美觀而非節能,因此陡坡屋頂的安裝成長速度較為緩慢。然而,GAF推出的太陽能瓦片表明,如果成本進一步降低,這種捆綁式增值提案有望擴大住宅用戶的使用範圍。

物流業者使用TPO膜維修複合屋頂是推動二次成長的主要因素,預計到2031年,平屋頂市場的複合年成長率將達到6.28%。 30年綜合保固和能源之星認證提升了其經濟吸引力,並幫助資產管理公司滿足獲得綠色債券的要求。此外,屋頂施工人員正在利用閉合迴路回收計畫來降低掩埋成本,並展現其對環境的承諾,這進一步凸顯了冷屋頂與傳統膜材的差異化優勢。

冷屋頂塗料可直接塗覆於現有基材之上,避免了拆除成本,並在注重成本的維修項目中拓展了冷屋頂市場,預計到2025年將佔銷售額的30.02%。同時,單層膜材是成長最快的細分市場,到2031年複合年成長率將達到6.42%。這是因為新建物流中心和資料中心的開發商更青睞其20年的保固期和焊接接縫。丙烯酸彈性體雖然成本績效,但容易積聚污垢。另一方面,矽酮和聚氨酯-丙烯酸混合材料由於其老化後優異的反射率而日益普及。瀝青瓦的成長較為緩慢,而金屬屋頂因其抗風壓掀起的能力,在颶風多發地區越來越受歡迎。新興的奈米陶瓷面漆具有防污效果,但在標準化測試驗證其長期性能之前,仍屬於小眾產品。

區域分析

受加州嚴格的建築規範、亞特蘭大的強制實施以及LEED認證的廣泛應用等因素推動,北美預計將在2025年以35.50%的市佔率引領市場。聯邦稅收優惠和州政府津貼正在抵消初期成本,並持續推動冷屋頂市場規模的擴張。雖然由於冷度日數較少,加拿大和墨西哥的成長速度較慢,但多倫多和蒙特雷對城市熱島現象的研究正在推動市政試驗計畫。

預計亞太地區將達到最高成長率,到2031年複合年成長率將達到6.88%。印度特倫甘納邦的政策(目標是到2028年安裝300平方公里的隔熱屋頂)以及「Eco-Niwas」標準(該標準對屋頂的U值設定了限制)推動了該地區的快速發展,這兩項政策都在促使公共和私人企業競標採用反射性屋頂方案。中國的能源標準「GB 55015-2021」將冷屋頂指定為新建住宅的合規標準,而日本的CASBEE評估系統則在推廣高密度商業建築中採用隔熱屋頂。

在歐洲,受修訂後的建築能源性能指令的推動,矽酸鹽水泥的應用正在穩步成長。德國和法國正在將歐盟義務納入其國家標準,其中包括矽酸鹽水泥的最低標準;而北歐國家則由於擔心冬季熱量損失而保持謹慎態度。在南歐,為了緩解夏季極端高溫,矽酸鹽水泥的應用正在增加;米蘭和馬德里等城市的高污染水平也推動了對耐污矽酸鹽水泥塗料的需求。

中東和非洲地區正從小規模的基數開始快速成長。在沙烏地阿拉伯,取消補貼後的價格體系改革創造了強勁的經濟獎勵。同時,阿拉伯聯合大公國的「Estidama」認證強制要求阿布達比和杜拜的大型專案使用反射性屋頂材料。南非的成長較為緩慢,主要受豪登省以外地區空調需求低迷的限制,但約翰尼斯堡和開普敦的綠色建築計劃為其發展提供了支持。巴西在南美洲反射性屋頂材料的應用方面處於領先地位,該國於2024年發布了NBR 17162標準,該標準使測試標準與ASTM標準接軌,並增強了國內生產能力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 能源效率法規與零碳排放義務

- 城市熱島效應緩解計劃

- 炎熱氣候地區電費上漲

- 綠建築認證獎勵

- 維修資料中心冷卻設備以降低熱量

- 市場限制因素

- 初始成本高:與傳統瀝青屋頂相比

- 大氣中的煙塵和污染物導致反射率降低。

- 潮濕多雲地區效能下降

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按屋頂類型

- 低坡屋頂

- 陡峭的屋頂

- 平屋頂

- 材料類型

- 冷屋頂塗料

- 單層薄膜(TPO、PVC、EPDM)

- 瀝青瓦

- 金屬屋頂

- 瓷磚和石板

- 層壓屋頂(BUR)

- 改性瀝青

- 其他材料類型(綠色屋頂、木瓦)

- 塗料化學

- 丙烯酸纖維

- 彈性體

- 矽酮

- 聚氨酯

- 其他塗層技術(鋁、陶瓷、奈米)

- 施工階段

- 新建工程

- 維修和屋頂更換

- 透過使用

- 商業建築

- 住宅大樓

- 工業設施

- 政府和公共基礎設施

- 醫療和教育設施

- 其他用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Akzo Nobel NV

- Asian Paints Ltd.

- Carlisle Companies Inc.

- CertainTeed, LLC

- Dow

- Elevate

- GACO

- GAF Materials LLC

- Huntsman International LLC

- IKO Industries Ltd.

- Johns Manville

- NanoTech Materials

- Nippon Paint Holdings Co., Ltd.

- Owens Corning

- PPG Industries, Inc.

- Saint-Gobain

- Sika AG

- SOPREMA Group

- TAMKO Building Products LLC

- Valspar

第7章 市場機會與未來展望

According to Mordor Intelligence, the cool roof market size was valued at USD 15.27 billion in 2025 and is estimated to grow from USD 16.14 billion in 2026 to reach USD 21.33 billion by 2031, at a CAGR of 5.73% during the forecast period (2026-2031).

This report is Segmented by Roof Type (Low-Slope Roofs, Steep-Slope Roofs, and Flat Roofs), Material Type (Cool Roof Coatings, Single-Ply Membranes, and More), Coating Chemistry (Acrylic, Elastomeric, Silicone, and More), Application (Commercial Buildings, Residential Buildings, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Cool Roof Market Trends and Insights

Energy-Efficiency Regulations and Zero-Carbon Mandates

Jurisdictions are incorporating minimum SRI thresholds directly into building codes, removing trade-off options that previously allowed developers to use additional insulation instead of reflective roofs. Europe's directive for zero-emission new buildings by 2030 requires architects to integrate cool roofs early in the design process, while China's GB 55015-2021 performance standards effectively mandate high-albedo roofing to achieve its approximately 30% energy-reduction target. India's Eco-Niwas Samhita 2024 introduces numeric caps on roof U-values and requires an initial reflectance of 0.6 for shallow slopes, signaling a strong regulatory push for the cool roof market. In the United States, LEED v5 increases SRI requirements to 82 (initial) and 64 (aged) for low-slope assemblies, driving manufacturers to reformulate coatings to withstand pollution-related degradation. These regulatory changes are expediting specification decisions, reducing payback periods, and fostering material innovation and supply chain scaling.

Urban Heat-Island Mitigation Programs

Cities are increasingly funding cool roofs as public infrastructure to reduce peak energy demand and lower ambient summer temperatures. For example, Atlanta's 2025 ordinance applies to commercial buildings over 10,000 ft2 and projects USD 310 million in cumulative energy savings by 2035. Hyderabad's program aims to cover 300 million m2 by 2028, achieving indoor temperature reductions of up to 4.5 °C and significant cooling energy savings. Other cities, such as Boston, Montreal, and various locations in California, offer grants to subsidize cool roof adoption for low-income buildings. These initiatives shift demand from private retrofits to public procurement, stabilizing supplier volumes and expanding the market footprint for cool roofs.

Higher Upfront Cost vs Conventional Asphalt Roofs

Reflective coatings cost between USD 0.75-2.50/ft2, and TPO membranes range from USD 3.50-6.50/ft2, compared to USD 1.00-3.00/ft2 for basic asphalt shingles. This 50-150% premium deters cost-sensitive builders. In temperate regions with lower cooling demands, payback periods can exceed five years, limiting cool roofs to discretionary upgrades. Tear-off disposal adds an additional USD 1-2/ft2, although retrofit coatings that avoid removal can reduce payback to under five years. While PACE financing spreads costs through property taxes, adoption remains concentrated in California and a few other states. Until incentives bridge this cost gap, price remains a significant barrier to wider market penetration.

Other drivers and restraints analyzed in the detailed report include:

- Rising Electricity Tariffs in Hot Climates

- Green-Building Certification Incentives

- Reflectivity Loss from Airborne Soot and Pollution

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Low-slope roofs accounted for 44.87% of 2025 revenue, emphasizing their importance in the cool roof market share for warehouses, malls, and institutional buildings. These roofs utilize large contiguous areas to enhance cooling efficiency and support ballasted solar arrays without membrane penetrations. CRRC's stricter three-climate aged-rating protocol, adopted in 2025, now prioritizes membranes with longer-lasting reflectance, increasing demand for premium PVC and TPO options that sustain cool roof market size gains. Steep-slope installations have slower growth as reflective asphalt shingles carry a 30-50% cost premium, and homeowners often prioritize aesthetics over energy savings. However, GAF's solar shingle launch suggests a bundled value proposition that could increase residential adoption if costs decrease further.

Secondary growth is driven by logistics operators retrofitting built-up roofs with TPO membranes, contributing to a 6.28% CAGR for flat roofs through 2031. Integrated 30-year warranties and ENERGY STAR certifications enhance financial appeal, enabling asset managers to qualify for green bonds. Roofers also utilize closed-loop take-back programs to reduce landfill fees and promote environmental credentials, further differentiating cool roofs from conventional membranes.

Cool roof coatings retained 30.02% revenue in 2025 due to their ability to overlay existing substrates, avoiding tear-off costs and expanding the cool roof market size across cost-sensitive retrofits. Single-ply membranes, however, are the fastest-growing segment, with a 6.42% CAGR through 2031, as builders of new logistics and data hubs prefer their 20-year warranties and weld-sealed seams. Acrylic elastomers remain cost-effective but are prone to dirt accumulation, while silicones and polyurethane-acrylic hybrids are increasingly specified for their superior aged reflectance. Asphalt shingles show modest growth, while metal roofs gain traction in hurricane-prone regions for their uplift resilience. Emerging nano-ceramic top-coats offer anti-soiling benefits but remain niche until standardized testing validates their long-term performance.

Geography Analysis

North America led 2025 demand with 35.50% share, driven by California's stringent building codes, Atlanta's city mandates, and widespread LEED adoption. Federal tax incentives and state grants offset upfront costs, sustaining the leading cool roof market size momentum. Canada and Mexico exhibit slower growth due to fewer cooling-degree days, though urban heat-island studies in Toronto and Monterrey are encouraging municipal pilot programs.

Asia-Pacific exhibits the fastest 6.88% CAGR through 2031. India's regional acceleration is supported by Telangana's policy targeting 300 km2 of installations by 2028 and Eco-Niwas caps on roof U-values, steering both public and private tenders toward reflective options. China's GB 55015-2021 energy code establishes cool roofs as the standard compliance path for new dwellings, while Japan's CASBEE assessments promote adoption in high-occupancy commercial towers.

Europe grows steadily on the back of the recast Energy Performance of Buildings Directive. Germany and France have translated EU mandates into national codes that incorporate SRI minimums, while Nordic countries remain cautious due to winter heat-loss concerns. Southern Europe is seeing increased adoption to mitigate extreme summer temperatures, though high pollution levels in cities like Milan and Madrid drive demand for dirt-resistant silicone coatings.

Middle-East and Africa expands from a smaller base. Saudi Arabia's post-subsidy tariff reforms create strong economic incentives, while the UAE's Estidama certification mandates reflective roofing for major projects in Abu Dhabi and Dubai. South Africa's growth is modest, limited by lower cooling needs outside Gauteng, but supported by green-building initiatives in Johannesburg and Cape Town. Brazil anchors South America's uptake following the 2024 publication of NBR 17162, which aligns testing standards with ASTM and boosts local production capacity.

- Akzo Nobel N.V.

- Asian Paints Ltd.

- Carlisle Companies Inc.

- CertainTeed, LLC

- Dow

- Elevate

- GACO

- GAF Materials LLC

- Huntsman International LLC

- IKO Industries Ltd.

- Johns Manville

- NanoTech Materials

- Nippon Paint Holdings Co., Ltd.

- Owens Corning

- PPG Industries, Inc.

- Saint-Gobain

- Sika AG

- SOPREMA Group

- TAMKO Building Products LLC

- Valspar

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Energy-efficiency Regulations and Zero-carbon Mandates

- 4.2.2 Urban Heat-Island Mitigation Programs

- 4.2.3 Rising Electricity Tariffs in Hot Climates

- 4.2.4 Green-Building Certification Incentives

- 4.2.5 Data-Centre Cooling Retrofits for Heat Reduction

- 4.3 Market Restraints

- 4.3.1 Higher Upfront Cost vs Conventional Asphalt Roofs

- 4.3.2 Reflectivity Loss from Airborne Soot and Pollution

- 4.3.3 Performance Degradation in Humid/Cloudy Zones

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Roof Type

- 5.1.1 Low-Slope Roofs

- 5.1.2 Steep-Slope Roofs

- 5.1.3 Flat Roofs

- 5.2 By Material Type

- 5.2.1 Cool Roof Coatings

- 5.2.2 Single-Ply Membranes (TPO, PVC, EPDM)

- 5.2.3 Asphalt Shingles

- 5.2.4 Metal Roofs

- 5.2.5 Tiles and Slates

- 5.2.6 Built-Up Roofs (BUR)

- 5.2.7 Modified Bitumen

- 5.2.8 Other Material Types (Green Roofs, Wood Shingles)

- 5.3 By Coating Chemistry

- 5.3.1 Acrylic

- 5.3.2 Elastomeric

- 5.3.3 Silicone

- 5.3.4 Polyurethane

- 5.3.5 Other Coating Chemistries (Aluminum, Ceramic, Nano)

- 5.4 By Build Phase

- 5.4.1 New Construction

- 5.4.2 Retrofit/Reroofing

- 5.5 By Application

- 5.5.1 Commercial Buildings

- 5.5.2 Residential Buildings

- 5.5.3 Industrial Facilities

- 5.5.4 Government and Public Infrastructure

- 5.5.5 Healthcare and Educational Campuses

- 5.5.6 Other Applications

- 5.6 By Geography

- 5.6.1 Asia-Pacific

- 5.6.1.1 China

- 5.6.1.2 India

- 5.6.1.3 Japan

- 5.6.1.4 South Korea

- 5.6.1.5 ASEAN Countries

- 5.6.1.6 Rest of Asia-Pacific

- 5.6.2 North America

- 5.6.2.1 United States

- 5.6.2.2 Canada

- 5.6.2.3 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 NORDIC Countries

- 5.6.3.8 Rest of Europe

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle-East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle-East and Africa

- 5.6.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Asian Paints Ltd.

- 6.4.3 Carlisle Companies Inc.

- 6.4.4 CertainTeed, LLC

- 6.4.5 Dow

- 6.4.6 Elevate

- 6.4.7 GACO

- 6.4.8 GAF Materials LLC

- 6.4.9 Huntsman International LLC

- 6.4.10 IKO Industries Ltd.

- 6.4.11 Johns Manville

- 6.4.12 NanoTech Materials

- 6.4.13 Nippon Paint Holdings Co., Ltd.

- 6.4.14 Owens Corning

- 6.4.15 PPG Industries, Inc.

- 6.4.16 Saint-Gobain

- 6.4.17 Sika AG

- 6.4.18 SOPREMA Group

- 6.4.19 TAMKO Building Products LLC

- 6.4.20 Valspar

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment