|

市場調查報告書

商品編碼

2062390

再生鉛:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Recycled Lead - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

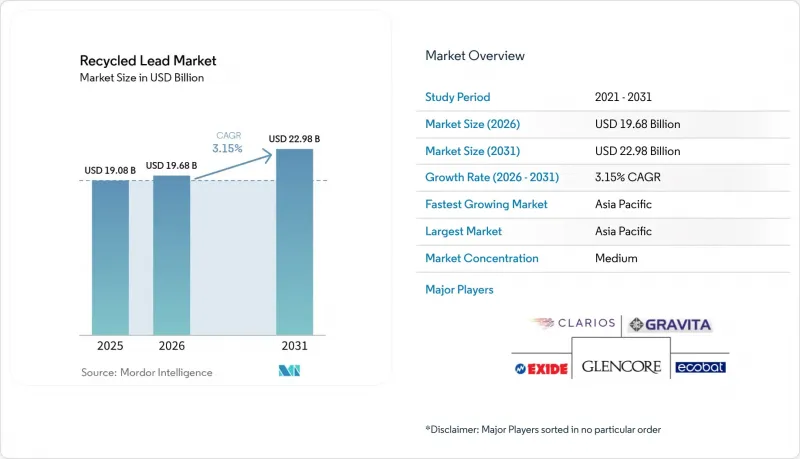

根據 Mordor Intelligence 預測,再生鉛市場規模預計將在 2025 年達到 190.8 億美元,2026 年達到 196.8 億美元,到 2031 年達到 229.8 億美元,2026 年至 2031 年的複合年成長率為 3.15%。

本報告按原料類型(例如,廢棄舊鉛酸電池、廢鉛)、回收方法(例如,熱回收、濕回收)、形態(例如,再生鉛錠、再生鉛合金)、終端用戶行業(例如,汽車 - SLI、能源儲存系統)和地區(例如,亞太地區、北美地區)進行細分。市場預測以美元計價。

全球再生鉛市場趨勢及洞察

對永續和循環經濟實踐的需求日益成長

循環經濟相關法規正在改變汽車製造商和工業電池採購商的籌資策略。歐盟強制要求製造商在2025年達到75%的回收率,2027年達到90%的鉛回收率,促使目的地設備製造商(OEM)與經認證的回收商簽訂長期供應合約。在美國,國家空氣污染控制法案(NESHAP)對二次冶煉廠的監管正在改善都市區設施周圍的空氣質量,儘管合規成本也在增加。大型企業正在採用洗滌器和靜電除塵設備等先進技術,而這些技術對於小規模企業來說難以實施,這正在推動再生鉛市場的重組。電池製造商將再生鉛定位為應對原生礦供應中斷的安全網,尤其是在印尼和澳洲於2024年限制鉛礦石出口之後。因此,再生鉛市場在更廣泛的電池價值鏈中變得越來越具有戰略意義。

鉛酸電池在汽車和固定式儲能系統中的應用日益廣泛。

預計到2024年,全球汽車產量將超過8,500萬輛,而每輛內燃機汽車都需要一顆SLI電池,因此對再生鉛的基本需求依然強勁。即使是電動車也使用12伏特輔助電池組來支援安全系統,這進一步凸顯了再生鉛的重要性。印度和非洲的通訊塔數量已超過60萬座,它們依靠閥控式鉛酸蓄電池(VRLA電池)來應對不穩定的電網狀況,擴大了廢鉛的供應。資料中心營運商報告稱,2025年備用電池的出貨量將成長15%,凸顯了固定式儲能市場的成長。回收商受益於從VRLA廢料中提取的高純度氧化鉛,這帶來了5%至8%的價格溢價,從而提高了再生鉛市場的利潤率。

非官方回收點的環境與健康風險

在印度和奈及利亞等國,一些未經監管的回收設施工人的血鉛含量經常超過 40 微克/分升,遠高於世界衛生組織 (WHO) 規定的 5 微克/分升的標準。這些設施排放的廢水污染了灌溉渠,引發了社區的擔憂,有時甚至導致工廠關閉。儘管《巴塞爾公約》強制要求使用封閉式熔爐和穩定爐渣,但執法力度仍然不足,導致價格競爭加劇,合規經營者的利潤率下降。電池製造商正在加強供應鏈審核,以降低聲譽風險。將非正規設施升級到 ISO 14001 標準的成本在每個設施 50 萬至 100 萬美元之間,這是一筆許多經營者無法承擔的巨額費用,導致流入合法再生鉛市場的廢料暫時減少。

細分市場分析

到2025年,廢棄鉛酸電池(ULAB)將佔再生鉛市場佔有率的73.89%,凸顯了廢棄舊SLI和VRLA電池在保障原料供應方面發揮的關鍵作用。工業廢棄物和污泥是成長最快的來源,預計到2031年將以3.58%的年複合成長率(CAGR)成長,這主要得益於電子設備和金屬模塑殘渣處置法規的日益嚴格。拓展污泥和工廠廢料業務有助於加工商穩定收入,抵禦ULAB流入量的波動,這項策略已被許多大型企業採用。

工業廢棄物需要進行硫酸鹽中和、碳酸鹽去除等處理,但其高純度氧化物含量對注重產品一致性的電池糊劑製造商極具吸引力。 Aqua Metals 的「AquaRefining」系統可在室溫下運作,專為 ULAB 設計,無需高爐,可將新工廠的資本投資成本降低約 30%。採用混合原料策略的加工商可獲得更大的柔軟性,有助於再生鉛市場的長期穩定發展。

至2025年,年處理能力為5萬至10萬噸的高爐將達到顯著的規模經濟效益,熱冶煉將佔再生鉛總產量的63.02%。由於濕式冶煉具有能耗降低40%至50%以及消除二氧化硫排放等優勢,預計到2031年,濕式冶煉的年複合成長率將達到3.64%。

歐盟的碳邊境調節機制(CBAM)將於2026年生效,屆時將對高碳金屬徵收進口關稅,鼓勵企業維修熔爐,加裝脫硫裝置,並投資興建低溫反應器。 ACE Green Recycling公司為非洲和印度等地區小規模企業設計的模組化電化學裝置,售價低於100萬美元,預計將加速技術應用。預計市場將出現技術兩極化:大型工廠將繼續採用火法工藝提純排放,而新參與企業則更有可能採用符合ESG融資標準的濕式冶煉工藝,從而增加再生鉛市場的競爭多樣性。

區域分析

預計亞太地區將在2025年佔據再生鉛市場45.33%的佔有率,並保持3.97%的複合年成長率直至2031年。中國在2024年收緊了排放法規,迫使非正規冶煉廠進行整合,並扶持那些能夠獲得脫硫裝置和即時監測資金的持證運營商。印度的電動三輪車生態系統為Gravita India等回收商提供了穩定的VRLA廢料供應,而東南亞國協則為新建濕式冶煉設施提供稅收優惠。日本和韓國的目標是到2050年實現碳中和,並正在推廣低碳反應器先導工廠,以支援整個再生鉛市場的區域技術應用。

在北美,鉛回收效率已超過99%,限制了其進一步的量化成長。美國鉛銅法規2024年的修訂案強制要求工廠維修,雖然增加了固定成本,但改善了區域空氣品質。加拿大和墨西哥正在整合跨境廢料流動,以提高運轉率;一些美國公司正在轉向使用優質氧化鉛生產固定式電池,以滿足資料中心ESG採購法規的要求。因此,再生鉛市場正在成熟的回收基礎設施與不斷變化的產品組合機會之間尋求平衡。

歐洲的需求受歐盟電池法規的影響,該法規將回收成分標準納入產品核可流程。在德國、法國和義大利,有垂直整合的叢集,將回收和冶煉集中在同一地點,透過密集確保經濟效益。由於俄羅斯的出口限制,需求已轉向國內和北非的回收商,從而實現了供應來源的多元化。

預計到2025年,南美洲和中東/非洲的市場佔有率總和仍將保持在較低水準。巴西擁有4000萬輛汽車,是廢棄鉛酸電池(ULAB)的主要來源,儘管在主要都會區以外仍然存在一些非正式的廢品回收站。阿拉伯聯合大公國和沙烏地阿拉伯資料中心的擴張刺激了閥控式鉛酸電池(VRLA)的進口,這些電池將在本世紀下半葉被報廢。這將為再生鉛市場帶來區域成長動力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對永續實踐和循環經濟的需求日益成長

- 鉛酸電池在汽車和固定式儲能系統中的應用日益廣泛。

- 嚴格的環境、健康與安全法規要求對鉛進行回收。

- 一級線索相對於二級線索的成本優勢

- 新興微出行市場對VRLA電池的需求不斷成長

- 市場限制因素

- 非正規回收點的環境和健康風險。

- 鉛價波動給冶煉廠的利潤率帶來了壓力。

- 電池壽命延長導致廢料供應減少

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依原料類型

- 廢棄鉛酸蓄電池(ULABs)

- 鉛廢料(電纜、屋頂材料、合金)

- 工業廢棄物和污泥

- 其他來源

- 透過回收方法

- 熱冶金法

- 濕式冶煉工藝

- 電化學

- 其他回收方法

- 按形式

- 回收鉛錠

- 回收鉛合金

- 二次氧化鉛

- 其他形式

- 按最終用戶行業分類

- 汽車 - SLI(啟動、照明、點火)

- 能源儲存系統

- 通訊和資料中心

- 工業設備

- 建築和基礎設施

- 家用電子產品

- 國防部/海軍陸戰隊

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- ACE Green Recycling, Inc.

- Aqua Metals, Inc.

- Battery Solutions Inc.

- Campine nv

- Clarios

- East Penn Manufacturing Company

- ECOBAT

- ENERSYS

- EXIDE INDUSTRIES LTD.

- Fenix Battery Recycling

- Glencore

- Gravita India Ltd.

- JAIN RESOURCE RECYCLING LTD.

- KC Recycling

- METALICO

- Pilot Industries Limited

- Pondy Oxides and Chemicals Limited

- Recylex SA

- Terrapure BR Ltd.

- The Doe Run Company

- Wirtz Manufacturing

第7章 市場機會與未來展望

According to Mordor Intelligence, the recycled lead market size is projected to be USD 19.08 billion in 2025, USD 19.68 billion in 2026, and reach USD 22.98 billion by 2031, growing at a CAGR of 3.15% from 2026 to 2031.

This report is Segmented by Source Type (Used Lead-Acid Batteries, Lead Scrap, and More), Recycling Method (Pyrometallurgical, Hydrometallurgical, and More), Form (Recycled Lead Ingots, Recycled Lead Alloys, and More), End-User Industry (Automotive - SLI, Energy Storage Systems, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Recycled Lead Market Trends and Insights

Growing Demand for Sustainable and Circular-Economy Practices

Circular-economy regulations are transforming procurement strategies among automakers and industrial battery buyers. The European Union mandates manufacturers to achieve 75% collection efficiency by 2025 and 90% lead recovery by 2027, encouraging original equipment manufacturers to establish long-term supply agreements with certified recyclers. In the United States, NESHAP limits for secondary smelters increase compliance costs but improve air quality near urban facilities. Large integrated firms are adopting advanced technologies like scrubbers and electrostatic precipitators, which smaller operators cannot afford, driving consolidation in the recycled lead market. Battery manufacturers view recycled lead as a safeguard against disruptions in primary-mine supply, particularly after Indonesia and Australia restricted lead-ore exports in 2024. As a result, the recycled lead market is gaining strategic importance within the broader battery value chain.

Rising Use of Lead-Acid Batteries in Automotive and Stationary Storage

Global vehicle production surpassed 85 million units in 2024, with each internal-combustion vehicle requiring an SLI battery, maintaining baseline demand for the recycled lead market. Even battery-electric vehicles use 12-volt auxiliary packs for safety systems, ensuring the continued relevance of recycled lead. Telecom towers in India and Africa now exceed 600,000 units and rely on VRLA batteries to address unreliable grid conditions, expanding the scrap stream. Data-center operators reported a 15% increase in reserve-power battery shipments in 2025, highlighting the growth of stationary storage. Recyclers benefit from VRLA scrap, which provides high-purity lead oxide with a 5%-8% price premium, boosting margins within the recycled lead market.

Environmental and Health Risks in Informal Recycling Clusters

Workers in unregulated recycling facilities in countries like India and Nigeria often record blood-lead levels exceeding 40 µg/dL, far above the World Health Organization guideline of 5 µg/dL. Effluent from these facilities contaminates irrigation channels, raising community concerns and occasionally leading to plant closures. While the Basel Convention prescribes enclosed furnaces and slag stabilization, enforcement gaps persist, enabling price undercutting that reduces margins for compliant operators. Battery manufacturers are increasingly auditing supply chains to avoid reputational risks. Upgrading informal facilities to ISO 14001 standards would cost USD 0.5-1 million per site, a financial burden many operators cannot bear, temporarily reducing scrap flows into the formal recycled lead market.

Other drivers and restraints analyzed in the detailed report include:

- Stringent EHS Regulations That Mandate Lead Recovery

- Cost Advantage of Secondary versus Primary Lead

- Lead-Price Volatility Squeezing Smelter Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Used lead-acid batteries (ULABs) contributed 73.89% of the recycled lead market share in 2025, highlighting the critical role of end-of-life SLI and VRLA units in ensuring feedstock availability. Industrial waste and sludge is the fastest-growing source type, with a CAGR of 3.58% projected through 2031, driven by stricter regulations on the disposal of electronics and metal-forming residues. Expanding into sludge and factory scrap helps processors stabilize revenues against fluctuations in ULAB inflows, a strategy already being utilized by larger firms.

Industrial waste requires processes like sulfate neutralization and carbonate removal, but its high-purity oxide content is appealing to battery paste manufacturers prioritizing consistency. Aqua Metals' AquaRefining system, which operates at room temperature, is designed for ULABs and eliminates the need for blast furnaces, reducing capital costs by approximately 30% for greenfield plants. Processors adopting blended feedstock strategies gain flexibility, supporting the long-term stability of the recycled lead market.

The pyrometallurgical method accounted for 63.02% of recycled lead output in 2025, as blast furnaces with capacities ranging from 50,000 to 100,000 tons per year achieve significant economies of scale. The hydrometallurgical method is expected to grow at a CAGR of 3.64% through 2031, benefiting from 40%-50% lower energy consumption and the elimination of sulfur-dioxide emissions.

The European Union's Carbon Border Adjustment Mechanism, effective from 2026, will impose import fees on carbon-intensive metals, encouraging companies to retrofit furnaces with scrubbers or invest in low-temperature reactors. ACE Green Recycling's modular electrochemical units, priced under USD 1 million, are designed for small operators in regions like Africa and India, potentially accelerating technology adoption. A bifurcation in technology is anticipated: high-volume plants will continue refining pyrometallurgical emissions, while new entrants are likely to adopt hydrometallurgical methods that align with ESG financing criteria, enhancing competitive diversity in the recycled lead market.

Geography Analysis

Asia-Pacific led the recycled lead market with 45.33% share in 2025 and is anticipated to grow at a 3.97% CAGR to 2031. China tightened emission controls in 2024, pushing informal smelters toward consolidation and favoring licensed operators capable of funding scrubbers and real-time monitoring. India's e-rickshaw ecosystem supplies predictable VRLA scrap to recyclers such as Gravita India, while ASEAN economies offer fiscal perks for new hydrometallurgical capacity. Japan and South Korea target carbon neutrality by 2050, stimulating pilot plants that test low-carbon reactors and supporting regional technology diffusion across the recycled lead market.

In North America, collection efficiency already exceeds 99%, capping incremental volume growth. The U.S. Lead and Copper Rule revisions in 2024 forced facility retrofits that raise fixed costs but improve community air quality. Canada and Mexico integrate cross-border scrap flows to buff smelter utilization, and several U.S. players are shifting into premium oxide for stationary storage that meets data-center ESG procurement rules. The recycled lead market thus balances mature collection infrastructure with evolving product-mix opportunities.

Europe's demand is shaped by the EU Battery Regulation that embeds recycled-content thresholds into product approval pathways. Germany, France, and Italy host vertically integrated clusters where ECOBAT and Campine co-locate collection and smelting, securing economies of density. Russia's export restrictions shift demand to domestic and North African recyclers, diversifying supply.

South America, and Middle-East and Africa combined for a lower share in 2025. Brazil's 40 million-vehicle fleet supplies significant ULAB volumes, yet informal yards persist outside major metros. Data-center expansion in the United Arab Emirates and Saudi Arabia stimulates VRLA imports that will transition into scrap later this decade, adding a regional growth vector to the recycled lead market.

- ACE Green Recycling, Inc.

- Aqua Metals, Inc.

- Battery Solutions Inc.

- Campine nv

- Clarios

- East Penn Manufacturing Company

- ECOBAT

- ENERSYS

- EXIDE INDUSTRIES LTD.

- Fenix Battery Recycling

- Glencore

- Gravita India Ltd.

- JAIN RESOURCE RECYCLING LTD.

- KC Recycling

- METALICO

- Pilot Industries Limited

- Pondy Oxides and Chemicals Limited

- Recylex SA

- Terrapure BR Ltd.

- The Doe Run Company

- Wirtz Manufacturing

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for sustainable and circular-economy practices

- 4.2.2 Rising use of lead-acid batteries in automotive and stationary storage

- 4.2.3 Stringent EHS regulations mandating lead recovery

- 4.2.4 Cost advantage of secondary vs. primary lead

- 4.2.5 Ramp-up of VRLA battery demand in emerging micro-mobility markets

- 4.3 Market Restraints

- 4.3.1 Environmental and health risks in informal recycling clusters

- 4.3.2 Lead-price volatility squeezing smelter margins

- 4.3.3 Shrinking scrap availability due to longer battery life

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Source Type

- 5.1.1 Used Lead-Acid Batteries (ULABs)

- 5.1.2 Lead Scrap (cables, roofing, alloys)

- 5.1.3 Industrial Waste and Sludge

- 5.1.4 Other Source Types

- 5.2 By Recycling Method

- 5.2.1 Pyrometallurgical

- 5.2.2 Hydrometallurgical

- 5.2.3 Electrochemical

- 5.2.4 Other Recycling Methods

- 5.3 By Form

- 5.3.1 Recycled Lead Ingots

- 5.3.2 Recycled Lead Alloys

- 5.3.3 Secondary Lead Oxide

- 5.3.4 Other Forms

- 5.4 By End-user Industry

- 5.4.1 Automotive - SLI (Starting, Lighting, and Ignition)

- 5.4.2 Energy Storage Systems

- 5.4.3 Telecom and Data Centers

- 5.4.4 Industrial Equipment

- 5.4.5 Construction and Infrastructure

- 5.4.6 Consumer Electronics

- 5.4.7 Defense and Marine

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 ACE Green Recycling, Inc.

- 6.4.2 Aqua Metals, Inc.

- 6.4.3 Battery Solutions Inc.

- 6.4.4 Campine nv

- 6.4.5 Clarios

- 6.4.6 East Penn Manufacturing Company

- 6.4.7 ECOBAT

- 6.4.8 ENERSYS

- 6.4.9 EXIDE INDUSTRIES LTD.

- 6.4.10 Fenix Battery Recycling

- 6.4.11 Glencore

- 6.4.12 Gravita India Ltd.

- 6.4.13 JAIN RESOURCE RECYCLING LTD.

- 6.4.14 KC Recycling

- 6.4.15 METALICO

- 6.4.16 Pilot Industries Limited

- 6.4.17 Pondy Oxides and Chemicals Limited

- 6.4.18 Recylex SA

- 6.4.19 Terrapure BR Ltd.

- 6.4.20 The Doe Run Company

- 6.4.21 Wirtz Manufacturing

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

金屬回收市場規模、佔有率、趨勢和預測:按金屬類型、類別、最終用途行業和地區分類,2026-2034年

金屬回收市場規模、佔有率、趨勢和預測:按金屬類型、類別、最終用途行業和地區分類,2026-2034年 金屬回收市場規模、佔有率和成長分析:按所用設備、廢料類型、金屬類型、最終用途產業和地區分類-2026-2033年產業預測

金屬回收市場規模、佔有率和成長分析:按所用設備、廢料類型、金屬類型、最終用途產業和地區分類-2026-2033年產業預測 金屬回收市場:2026-2032年全球市場預測(依金屬類型、最終用途產業、產品形態及回收來源分類)

金屬回收市場:2026-2032年全球市場預測(依金屬類型、最終用途產業、產品形態及回收來源分類) 全球金屬回收市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球金屬回收市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球非鐵金屬回收市場報告

2026年全球非鐵金屬回收市場報告 廢金屬回收市場分析及預測(至2035年):類型、產品類型、服務、技術、應用、形式、材質類型、製程、最終用戶、設備

廢金屬回收市場分析及預測(至2035年):類型、產品類型、服務、技術、應用、形式、材質類型、製程、最終用戶、設備 再生廢金屬市場規模、佔有率和成長分析(按來源、材質、應用、最終用戶和地區分類)—產業預測(2026-2033 年)日本金屬回收市場規模、佔有率、趨勢和預測:按金屬、產業和地區分類,2026-2034年2026年全球再生金屬市場報告2026年全球再生鉛市場報告

再生廢金屬市場規模、佔有率和成長分析(按來源、材質、應用、最終用戶和地區分類)—產業預測(2026-2033 年)日本金屬回收市場規模、佔有率、趨勢和預測:按金屬、產業和地區分類,2026-2034年2026年全球再生金屬市場報告2026年全球再生鉛市場報告