|

市場調查報告書

商品編碼

2062387

白蟻防治:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Termite Control - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

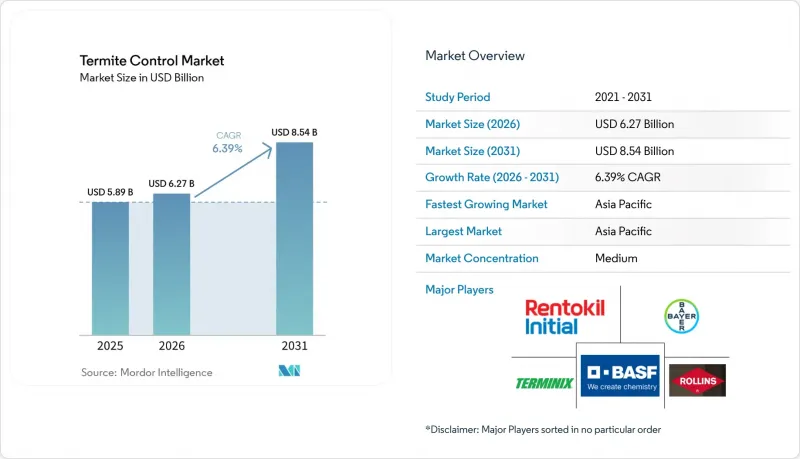

根據 Mordor Intelligence 預測,白蟻防治市場規模將從 2025 年的 58.9 億美元成長到 2026 年的 62.7 億美元,到 2031 年將達到 85.4 億美元,2026 年至 2031 年的複合年成長率為 6.39%。

本報告按防治方法(化學防治、物理/機械防治、生物防治等)、白蟻種類(地下白蟻、乾木白蟻等)、應用領域(住宅、商業/工業等)和地區(亞太地區、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元計價。

全球白蟻防治市場趨勢及洞察

修復結構性損傷的成本增加

在美國,白蟻造成的年度維修費用已達到相當可觀的水平。這一數字還不包括間接損失,例如房產價值下降和保險費上漲。在潮濕地區,維護不善的老舊住宅存量更容易遭受白蟻侵害。因此,貸款機構正在收緊房屋檢查標準,保險公司也為有效的保險提供保費折扣。地方政府現在已將多年期白蟻防治合約納入橋樑、電線杆和公共建築的維護預算。這種轉變將曾經的自由支配支出轉變為計畫性資本支出。因此,全球白蟻防治市場正在擴張,更高的白蟻檢測率、不斷上漲的維修成本以及預防措施已成為資金籌措的必要條件。擅長量化避免維修成本的服務供應商正在與公共和私人業主簽訂長期合約。

新興市場建築業蓬勃發展,但同時也容易遭受白蟻侵害。

印度的國家基礎設施規劃和中國的「一帶一路」計劃正在熱帶和亞熱帶地區投入大量資源用於交通走廊和住宅計畫。在越南、印尼和泰國,新的建築規範強制要求使用土壤基白蟻防治劑或安裝實體屏障,適用於預計使用超過20年的建築物。開發商現在將白蟻防治視為與能源效率同等重要的品質指標。這種轉變正促使全球白蟻防治供應商實現供應鏈和認證專案的在地化。不銹鋼網和碎石屏障的供應商需求不斷成長。這些非化學解決方案非常適合綠色建築認證,而綠色建築認證在高階城市專案中廣泛應用。預計占地面積的擴大和這些規範的日益普及將推動亞太地區全球白蟻防治市場的持續成長。氣候變遷也促使白蟻棲息地向極地地區擴張。

對傳統白蟻防治劑制定了嚴格的環境法規

近年來,加州已禁止在住宅使用Bifenthrin和Chlorpyrifos。同時,歐盟也因擔心Fipronil的水生毒性而對其展開重新評估。幾乎在同一時間,澳洲監管機構也逐步淘汰了多種有機磷殺蟲劑的使用。因此,服務公司目前面臨許多挑戰,包括重新培訓員工、投資精密輸液設備,以及說服注重預算的住宅選擇更高價格的化學處理和物理防治方法。生產商正爭相重新配製產品,但重新貼標和進行現場效果測試既費時又昂貴。這將擠壓短期利潤,並減緩全球白蟻防治市場的成長,直到服務提供者調整價格,客戶也逐漸適應新的殺蟲劑為止。

細分市場分析

預計到2025年,化學防治將佔銷售額的54.67%,反映了其在施工前土壤屏障和周邊噴灑修復領域數十年來的主導地位。隨著監管機構限制有機磷和擬除蟲菊酯類殺蟲劑的使用,該細分市場的佔有率正在逐漸下降,物業管理人員正轉向毒性較低的替代方案。預計2026年至2031年,誘餌系統的複合年成長率將達到6.92%。在全球白蟻防治市場,幾丁質合成抑制劑(例如Sentricon和Trelona ATBS)能夠相對快速地根除白蟻群落。這些方法也符合室內空氣品質和綠色建築標準,因此適用於醫院、學校和LEED(能源與環境設計先鋒獎)認證專案。同時,在建築規範強制要求使用非化學解決方案的地區,不銹鋼網、聚合物薄膜和分級石材等物理屏障正日益普及。然而,由於安裝成本高昂,這些方法僅限於高價值建築。

配備震動感測器的智慧誘餌站可即時傳輸餵食數據。這項創新技術不僅最大限度地減少了技術人員的出行,還有助於提高合約續約率。BASF的Thermidor HE是化學防治方法的顯著變革。此配方在不影響防治效果的前提下顯著降低了活性成分的用量,使其更容易符合嚴格的殘留標準。雖然綠菌等生物防治方法由於田間持久性存在差異仍處於測試階段,但綜合蟲害防治方案已將衛生、濕度控制和針對性局部處理納入其中,以減少對化學品的依賴。隨著業主逐漸認知到生命週期成本計算的價值,市場需求正從傳統的土壤大面積噴灑轉向預測性防治方案,從而推動全球白蟻防治市場產品系列的轉型。

區域分析

亞太地區預計在2025年將佔全球銷售額的44.93%,並預計在2026年至2031年間以7.14%的複合年成長率成長。熱帶濕潤氣候、季風帶來的高濕度以及快速的都市化進程,共同鞏固了亞太地區在全球白蟻防治市場的主導地位。中國的建築規範強制要求在施工前進行土壤處理,而印度的馬哈拉斯特拉邦和卡納塔克邦等邦則要求中低層經濟適用住宅安裝實體防蟲屏障。在越南和印度尼西亞,開發商已將年度監測成本納入管理費,從而為服務公司提供了穩定的收入來源。在可預見的未來,亞太地區的建築項目數量沒有放緩的跡象,因此該地區在全球市場的主導地位仍然穩固。

北美市場規模位居第二,美國退伍軍人事務部計劃在不久的將來擴大強制檢查的縣域範圍。這項擴大使得許多原本可選的白蟻防治措施成為獲得房屋抵押貸款的強制性要求。冬季氣溫升高導致地下白蟻遷移至中西部和加拿大南部,而這些地區的建築規範歷來忽略白蟻防治措施。為了應對這些新的風險區域,保險公司現在要求提供保險證明,從而推動了對具備遠端錄影功能的智慧監控解決方案的需求成長。此外,加拿大各省正在考慮修訂其建築規範,這可能會在未來幾年催生新的市場需求。

在歐洲,網紋白蟻的活動正在增加,主要集中在地中海沿岸國家,且成長緩慢。歐盟植物檢疫條例要求建築商在特定緯度以南的新建築中採取白蟻防治措施。在西班牙和義大利,由於化學土壤處理會造成環境問題,人口密集的歷史中心地帶正在對歷史建築的石砌部分加裝不銹鋼防護罩。同時,為了因應白蟻風險向北蔓延的趨勢,德國和法國的建築管理部門已開始進行白蟻危害風險測繪調查。

在南美洲,巴西扮演主導角色,其人工林使用預防性白蟻防治劑來保護木材和灌溉系統。在阿根廷的都市區,社會住宅計畫的競標文件中已明確規定使用硼酸鹽進行預處理。雖然中東和非洲的推廣速度較為緩慢,但海灣合作理事會(GCC)的大型企劃,從沙烏地阿拉伯的「2030願景」住宅計畫到卡達的物流園區,都已強制要求安裝白蟻屏障,以符合國際保險公司的標準。儘管日本市場已趨於成熟,但其人均支出仍然很高。這主要歸功於日本嚴格的建築標準,該標準要求定期檢查和更新已進行蟲害處理的區域。這些區域趨勢清楚地展現了全球白蟻防治市場多樣化的成長軌跡。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 修復結構性損壞的成本增加(主流觀點)

- 新興市場建築業蓬勃發展,但白蟻危害嚴重(主流觀點)

- 保險公司對抵押房產進行強制白蟻檢查(主流做法)

- 氣候變遷導致白蟻棲息地向極地地區擴張(一個被忽視的現象)

- 智慧/物聯網白蟻監測平台的快速普及(一個研究不足的領域)

- 工程木高層建築工程的興起需要採取預防性防護措施(一個被忽視的趨勢)

- 市場限制因素

- 對傳統白蟻防治劑(主流)實施嚴格的環境法規

- 住宅健康和室內空氣品質問題(主流)

- 對化學活性物質的遺傳和行為耐受性加速發展(一個常被忽略的因素)

- 在價格敏感地區,智慧誘餌和監測合約的初始成本較高(表中未顯示)。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 控制方法

- 化學防治

- 物理和機械屏障

- 生物防治

- 餵料系統

- 綜合蟲害管理(IPM)

- 類型

- 地下白蟻

- 乾木白蟻

- 潮濕木材中的白蟻

- 其他類型的白蟻

- 透過使用

- 住宅

- 商業和工業用途

- 農地

- 公共基礎設施

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)和排名分析

- 公司簡介

- Anticimex

- Arrow Exterminators

- BASF

- Bayer AG

- Corteva Agriscience

- Dow

- Ecolab Inc.

- Ensystex

- FMC Corporation

- Rentokil Initial plc

- Rentokil North America, Inc.

- Rollins, Inc.

- SEMCO co.Ltd.

- Sumitomo Chemical Co., Ltd.

- Syngenta

- UPL

- Woodstream Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the termite control market size is expected to grow from USD 5.89 billion in 2025 to USD 6.27 billion in 2026 and is forecast to reach USD 8.54 billion by 2031 at 6.39% CAGR over 2026-2031.

This report is Segmented by Control Method (Chemical Control, Physical and Mechanical Barriers, Biological Control, and More), Species (Subterranean Termites, Drywood Termites, and More), Application (Residential, Commercial and Industrial, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Termite Control Market Trends and Insights

Growing Structural-Damage Remediation Costs

In the United States, annual repair bills due to termite damage have reached significant levels. This figure does not account for the indirect losses, such as property devaluation and increased insurance premiums. In humid regions, an aging housing stock with postponed maintenance heightens vulnerability to termite damage. As a result, lenders are tightening their inspection criteria, and insurers are offering premium discounts for active warranties. Municipal agencies are now incorporating multi-year termite contracts into their budgets for bridge, pole, and public-building maintenance. This shift turns what was once discretionary spending into planned capital outlays. Consequently, detection rates have risen, remediation spending has increased, and the global termite control market has expanded, with preventive treatments now seen as a financing necessity. Service providers adept at quantifying avoided repair costs are securing long-term contracts with both public and private owners.

Construction Boom in Termite-Prone Emerging Markets

India's National Infrastructure Pipeline and China's Belt and Road Initiative are investing significant resources into transport corridors and housing projects in tropical and subtropical regions. In Vietnam, Indonesia, and Thailand, new building codes mandate pre-construction soil termiticides or physical barriers for structures intended to last over two decades. Developers now view termite protection as a quality metric, on par with energy efficiency. This shift is prompting global termite control vendors to localize their supply chains and certification programs. Suppliers of stainless-steel mesh and graded-stone barriers are experiencing increased demand. These non-chemical solutions resonate with green-building labels, which are prevalent in premium urban projects. Looking ahead, the combination of expanding floor space and rising specification rates is set to drive the continued growth of the global termite control market in the Asia-Pacific region.Climate-Change Driven Pole-Ward Termite Range Expansion

Stringent Environmental Bans on Legacy Termiticides

In recent years, California prohibited the residential use of bifenthrin and chlorpyrifos. Meanwhile, the European Union initiated a review of fipronil due to concerns over its aquatic toxicity. Around the same period, regulatory authorities in Australia canceled the use of several organophosphates. As a result, service firms are now faced with the challenge of retraining their crews, investing in precision-injection rigs, and convincing budget-conscious homeowners to opt for more expensive chemical treatments or physical barriers. While manufacturers are hastening the reformulation of their products, they find that amending labels and validating in the field require significant capital and time investments. This has led to a compression in near-term profits, slowing the growth of the global termite control market until operators adjust their service prices and customers become accustomed to the new range of chemicals.

Other drivers and restraints analyzed in the detailed report include:

- Climate-Change Driven Pole-Ward Termite Range Expansion

- Rapid Adoption of Smart/IoT Termite Monitoring Platforms

- Accelerating Genetic and Behavioral Resistance to Chemical Actives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chemical Control held 54.67% of 2025 revenue, reflecting decades-long dominance in pre-construction soil barriers and corrective perimeter drenches. The segment's share edges downward as regulators restrict organophosphates and pyrethroids, nudging property managers toward lower-toxicity alternatives. Bait systems are expanding at a projected 6.92% CAGR between 2026 and 2031. In the global termite control market, Sentricon and Trelona ATBS, utilizing chitin-synthesis inhibitors, can collapse colonies within a relatively short period. These methods also meet indoor-air and green-building standards, making them suitable for hospitals, schools, and Leadership in Energy and Environmental Design-certified projects. Meanwhile, physical barriers like stainless-steel mesh, polymer films, and graded stone are gaining popularity in regions with building codes that mandate chemical-free solutions. However, their installation costs confine them to high-value structures.

Smart bait stations, now equipped with vibration sensors, relay real-time feeding data. This innovation not only minimizes technician callouts but also enhances subscription renewals. A notable shift in chemical approach is evident with BASF's Termidor HE: this formulation reduces active-ingredient loading significantly without compromising efficacy, making it easier to adhere to stringent residue limits. While biological controls like Metarhizium anisopliae are still in the pilot phase due to inconsistent field persistence, integrated pest-management programs are already incorporating sanitation, moisture management, and targeted spot treatments to reduce chemical dependency. As property owners recognize the value of life-cycle cost calculations, there's a noticeable shift in demand towards predictive programs over traditional blanket soil drenches, leading to a transformation in product portfolios within the global termite control market.

Geography Analysis

Asia-Pacific anchored 44.93% of 2025 revenue and is projected to grow at 7.14% CAGR between 2026 and 2031. As tropical humidity, monsoon moisture, and rapid urbanization converge, Asia-Pacific solidifies its dominance in the global termite control market. Chinese construction standards mandate pre-construction soil treatments, while states like Maharashtra and Karnataka in India now require physical barriers for mid-rise affordable housing. In Vietnam and Indonesia, developers incorporate annual monitoring into strata fees, creating a steady revenue stream for service firms. With construction pipelines showing no signs of slowing down in the foreseeable future, the region's lead in the global market remains unchallenged.

North America, with the United States Department of Veterans Affairs expanding mandatory inspection counties in the near future, ranks second in market value. This expansion has turned many previously discretionary treatments into essential mortgage closing requirements. Warmer winters have enabled subterranean termites to migrate into the Midwest and southern Canada, regions where building codes have traditionally overlooked termite barriers. In response to emerging risk zones, insurance carriers are now mandating proof of coverage, spurring a rise in smart monitoring solutions equipped with remote documentation features. Furthermore, Canadian provinces are contemplating code amendments, potentially introducing a new layer of demand in the coming years.

Europe witnesses moderate growth, predominantly in Mediterranean nations where Reticulitermes activity is on the rise. European Union phytosanitary regulations mandate builders to integrate termite protection in new constructions south of a specific latitude. In Spain and Italy, heritage masonry is being retrofitted with stainless-steel shields, as chemical soil treatments face environmental challenges in densely populated historic centers. Meanwhile, the northern spread of termite risks has led German and French building authorities to initiate hazard mapping studies.

In South America, Brazil takes the lead, with plantations using preventive termiticides to protect timber and irrigation systems. Argentine urban centers are now specifying borate pre-treatments in tender documents for social housing blocks. While the Middle-East and Africa have been slow to adopt, megaprojects in the Gulf Cooperation Council, from Saudi Vision housing initiatives to Qatari logistics parks, are now mandating termite barriers to meet international insurer standards. Japan, despite its maturity in the market, continues to command a premium per-capita spend. This is largely due to stringent Japanese construction standards, which necessitate periodic inspections and the renewal of chemical zones. These regional dynamics collectively underscore the diverse growth trajectory of the global termite control market.

- Anticimex

- Arrow Exterminators

- BASF

- Bayer AG

- Corteva Agriscience

- Dow

- Ecolab Inc.

- Ensystex

- FMC Corporation

- Rentokil Initial plc

- Rentokil North America, Inc.

- Rollins, Inc.

- SEMCO co.Ltd.

- Sumitomo Chemical Co., Ltd.

- Syngenta

- UPL

- Woodstream Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing structural-damage remediation costs (mainstream)

- 4.2.2 Construction boom in termite-prone emerging markets (mainstream)

- 4.2.3 Insurance-mandated termite inspections for mortgaged assets (mainstream)

- 4.2.4 Climate-change driven pole-ward termite range expansion (under-the-radar)

- 4.2.5 Rapid adoption of smart/IoT termite monitoring platforms (under-the-radar)

- 4.2.6 Rise of engineered-timber high-rise projects requiring preventive barriers (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 Stringent environmental bans on legacy termiticides (mainstream)

- 4.3.2 Health and indoor-air-quality concerns among homeowners (mainstream)

- 4.3.3 Accelerating genetic and behavioural resistance to chemical actives (under-the-radar)

- 4.3.4 High up-front cost of smart bait and monitoring contracts in price-sensitive regions (under-the-radar)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Control Method

- 5.1.1 Chemical Control

- 5.1.2 Physical and Mechanical Barriers

- 5.1.3 Biological Control

- 5.1.4 Bait Systems

- 5.1.5 Integrated Pest Management (IPM)

- 5.2 By Species

- 5.2.1 Subterranean Termites

- 5.2.2 Drywood Termites

- 5.2.3 Dampwood Termites

- 5.2.4 Other Termite Types

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial and Industrial

- 5.3.3 Agricultural Lands

- 5.3.4 Public Infrastructure

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Nordic Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/(%)Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 Anticimex

- 6.4.2 Arrow Exterminators

- 6.4.3 BASF

- 6.4.4 Bayer AG

- 6.4.5 Corteva Agriscience

- 6.4.6 Dow

- 6.4.7 Ecolab Inc.

- 6.4.8 Ensystex

- 6.4.9 FMC Corporation

- 6.4.10 Rentokil Initial plc

- 6.4.11 Rentokil North America, Inc.

- 6.4.12 Rollins, Inc.

- 6.4.13 SEMCO co.Ltd.

- 6.4.14 Sumitomo Chemical Co., Ltd.

- 6.4.15 Syngenta

- 6.4.16 UPL

- 6.4.17 Woodstream Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Expansion of smart termite monitoring systems