|

市場調查報告書

商品編碼

2062382

輕質骨材混凝土:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Lightweight Aggregate Concrete - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

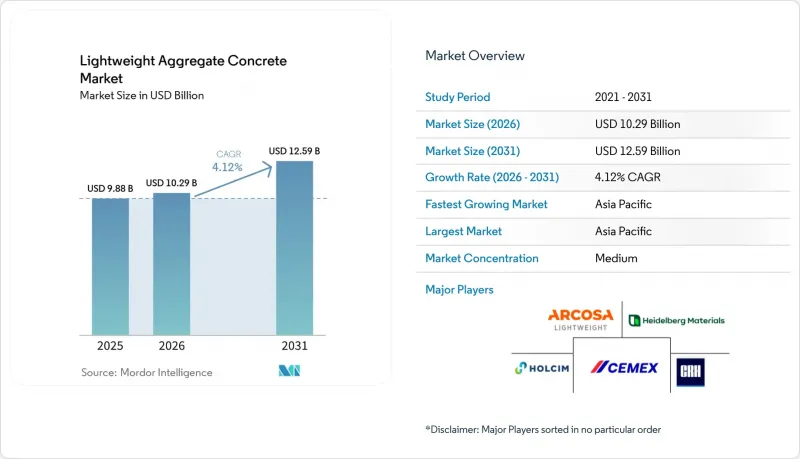

根據 Mordor Intelligence 預測,輕質骨材混凝土市場規模將從 2025 年的 98.8 億美元成長到 2026 年的 102.9 億美元,到 2031 年將達到 125.9 億美元,2026 年至 2031 年的複合年成長率為 4.12%。

本報告按骨材類型(膨脹粘土、膨脹板岩等)、應用領域(結構混凝土、砌塊和板材製造等)、終端用戶行業(住宅、商業、工業等)以及地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以美元計價。

全球輕質骨材混凝土市場趨勢及洞察

對輕質高強度建築材料的需求日益成長

專案工程師指定使用輕質骨材混凝土,以實現超越傳統重量混凝土混合料跨深比的性能。這將使建造100公尺預力橋樑梁體時,撓度不會超過限制。經迴轉窯處理的頁岩骨材在密度約1,920公斤/立方公尺(kg/m³)時,抗壓強度可達每平方英吋6000磅(psi),顯示即使質量減少,強度也不會降低。一項於2025年進行的研究重點介紹了輕質超高強度混凝土混合料,其抗壓強度可達102-123兆帕(MPa),同時自重可降低高達20%。在日本和加州等地震多發地區,降低自重可直接降低基礎的剪力,進而降低基礎施工成本。 Holcim 的 ECOPact 平台結合了輕質骨材和水泥基增強材料,達到了 LC60 等級,同時在製造過程中減少了 30-50% 的二氧化碳 (CO2)排放,這表明實現結構性能和脫碳目標都是可能的。

在高層建築和預製結構中得到更廣泛的應用

由於人手不足,開發商正轉向模組化和預製構件施工方法,泵送運輸和輕質板材有助於縮短起重機作業週期。例如,在哈勒-諾伊施塔特2025年的陽台維修工程中,使用了Liapor LC30/33D1.8泵送混凝土至18層,在幾週內完成了220塊樓板的澆築,並實現了無離析的垂直運輸。香港的一項案例研究表明,使用輕量材料可使非結構樓板的碳排放量減少10.1%,而採用預製構件施工方法則可獲得更大的效益。在印度,供應商正在推廣輕質混凝土混合料,這種混合料還可作為熱帶地區高層建築的被動冷卻層。此外,使用焊接金屬網格和玻璃纖維的自填充樓板製造商報告稱,與未加固的樓板相比,基於輕質膨脹粘土骨材(LECA)的樓板的承載能力提高了45%。

與傳統混凝土相比,成本更高

由於迴轉窯每噸需要1.5-2.0吉焦耳(GJ)的能源,輕質混凝土混合料的成本會增加15-25%。這遠高於碎石每噸0.5吉焦耳的能耗。雖然燒結飛灰技術可以降低燃料消耗,但承包工程的成本仍比破碎設備高出30-40%。對於利潤率僅為個位數的開發商而言,將這些額外成本轉嫁給住宅是一項挑戰,導致輕質混凝土在高檔住宅項目中應用有限。價值工程研究表明,考慮到地基成本、起重機運作時間和更短的工期,專案總成本可以降低5-10%,但由於採購慣例各自為政,這些全生命週期效益往往被忽略。

細分市場分析

截至2025年,膨脹粘土將佔輕質骨材混凝土市場34.44%的佔有率,主要得益於歐洲和亞太地區成熟的迴轉窯基礎設施。珍珠岩是成長最快的骨材,預計到2031年將維持4.58%的年成長率。由於其強度等級超過40兆帕(MPa),珍珠岩的市場規模預計將穩定成長,尤其適用於橋樑建設和維修工程。珍珠岩的成長率預計將比整體骨材類別高出16個基點,這主要歸功於其0.08瓦/米·開爾文(W/mK)的低導熱係數,使其適用於3D列印和超高保溫找平層。

在美國,膨脹頁岩和板岩因其密度超過1600公斤/立方公尺(kg/m³)、抗壓強度超過6000磅/平方英吋(psi)而被廣泛應用於結構工程,例如加州的沙斯塔拱橋計畫就證明了這一點。浮石主要用於裝飾和景觀美化,其產地集中在美國西部和愛琴海地區。由於成本和耐久性方面的限制,蛭石和新興的生物骨材市佔率不足5%。在中國,一旦JC/T 2772-2024標準允許將預分選儲層淤泥顆粒用於LC25級以下的非結構應用,預計將使供應來源更加多元化。

區域分析

預計到2025年,亞太地區將佔全球輕骨材混凝土銷售額的47.89%,並預計到2031年將以6.11%的年均成長率成長。這一增速比全球輕骨材混凝土市場的平均成長速度快近50%。在中國,強制要求在輕骨材中使用再生材料的JC/T 2772-2024標準催生了一條新的供應鏈,有效減少了建築廢棄物掩埋的負擔。此外,位於本溪的一棟26層樓高樓的自重降低了21%至25%,從而降低了地震期間的基礎剪力。在印度,預製構件生產商正在使用品牌輕骨材混凝土,以縮短工程工期高達50%,這些混凝土在熱帶氣候下還能起到被動冷卻的作用。在日本,輕質超高強度混凝土的採用主要得益於其抗震性能的提升,這種混凝土的強度可達 100 兆帕 (MPa),密度低於 2,100 公斤/立方米 (kg/m3)。

北美市場的成長主要得益於Arcosa的窯爐網路、策略性併購以及橋樑管理局的先導計畫。在以4.5億美元出售骨材業務和以6000萬美元收購佛羅裡達州的骨料業務後,Arcosa已將資金重新配置到高利潤的基礎設施產品領域。 Titan America的AI驅動配方設計平台最佳化了性能和碳足跡預測,將估算週期從數週縮短至數小時。佛羅裡達州對用於颶風易發地區的輕質屋頂填充材的監管批准表明,該地區對此類填料的接受度正在不斷提高。

在歐洲,減少碳排放和修復歷史建築是重中之重。例如,伍珀塔爾的卡貝爾斯特拉文橋和施特勞賓的橋樑拓寬工程等項目,在保留現有橋墩的同時,實現了100噸的減重。挪威的「BetongVIND」舉措和「Horizon-Europe MADE4WIND」聯盟正致力於將輕質混凝土打造為深海風發電工程的關鍵組成部分,目標是在連續重力基礎的生產過程中減少80%的二氧化碳排放。在英國,LECA的第三方檢驗環境產品聲明(EPD)幫助建築物獲得BREEAM(英國建築研究院環境評估方法)認證,同時符合2030年的碳減量目標。

在南美洲,Votorantim Cimentos公司一項價值50億雷亞爾(約合9.7億美元)的擴建計劃正在為此做出貢獻,該計劃將馬托格羅索州的產能擴大至120萬噸,並使該地區90%的電網在2026年3月前實現可再生能源供電。在中東和非洲,該技術的部署尚處於早期階段,目前主要應用於沙烏地阿拉伯的高層建築核心區域和液化天然氣(LNG)接收站。在這些場所,輕型設計最大限度地減少了對碼頭加固的需求。然而,對進口的依賴和高昂的運輸成本是全部區域廣泛採用該技術的主要障礙。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對輕質高強度建材的需求日益成長

- 在高層建築和預製結構中的應用日益廣泛

- 透過減少靜載荷實現經濟高效的設計。

- 更嚴格的節能和隔熱標準

- 3D列印混凝土的新應用

- 市場限制因素

- 高成本混凝土與一般混凝土的比較

- 優質輕質骨材短缺

- 水分引起的機械性質變化

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依骨材類型

- 發泡黏土

- 發泡頁岩

- 發泡石板

- 珍珠岩

- 浮石

- 其他骨材)

- 透過使用

- 結構混凝土

- 預製構件

- 砌塊和麵板生產

- 橋面和基礎設施

- 隔熱找平層和屋頂填充材

- 其他

- 按最終用戶行業分類

- 住宅

- 商業的

- 產業

- 基礎設施

- 能源和公共產業(離岸風電、液化天然氣)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Arcosa Lightweight

- Argex SA

- Boral Limited

- Buildex

- Cemex SAB DE CV

- Charah Solutions Inc.

- CRH

- H+H International

- Heidelberg Materials AG

- Holcim

- Laterlite SpA

- Leca International

- Liapor Group

- PORAVER

- Pumice Products International

- Saint-Gobain

- Titan America

- Votorantim Cimentos

- Vulcan Materials Company

第7章 市場機會與未來展望

According to Mordor Intelligence, the lightweight aggregate concrete market size is expected to grow from USD 9.88 billion in 2025 to USD 10.29 billion in 2026 and is forecast to reach USD 12.59 billion by 2031 at 4.12% CAGR over 2026-2031.

This report is Segmented by Type of Aggregate (Expanded Clay, Expanded Slate, and More), Application (Structural Concrete, Block and Panel Production, and More), End-User Industry (Residential, Commercial, Industrial, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Lightweight Aggregate Concrete Market Trends and Insights

Growing Demand for Lightweight and High-Strength Construction Materials

Project engineers are specifying lightweight aggregate concrete to achieve span-to-depth ratios that exceed the capabilities of normal-weight mixes. This enables the construction of 100-meter prestressed bridge girders without surpassing deflection limits. Rotary-kiln shale aggregates have demonstrated compressive strengths of 6,000 pounds per square inch (psi) at densities around 1,920 kilograms per cubic meter (kg/m3), showing that reducing mass does not compromise strength. Research conducted in 2025 highlighted lightweight ultra-high-strength formulations achieving compressive strengths of 102-123 megapascals (MPa) while reducing self-weight by up to 20%. In seismic regions such as Japan and California, lower dead loads directly reduce base shear, leading to cost savings in foundation construction. Holcim's ECOPact platform combines lightweight aggregates with supplementary cementitious materials to achieve LC60 classes while reducing embodied carbon dioxide (CO2) by 30-50%, demonstrating that structural performance and decarbonization objectives can align.

Increasing Use in High-Rise and Precast Structures

Labor shortages are driving developers toward modular and precast construction methods, where pumpability and lighter panels help reduce crane cycle times. For instance, a 2025 balcony retrofit project in Halle-Neustadt utilized Liapor LC30/33D1.8, successfully pumping concrete to the 18th floor and completing 220 slabs within weeks, showcasing vertical conveyance without segregation. Case studies in Hong Kong revealed a 10.1% reduction in embodied carbon for non-structural floors after substituting lightweight materials, with even greater benefits when prefabrication is adopted. In India, suppliers are promoting lightweight mixes that also function as passive cooling masses in tropical high-rise buildings. Additionally, fabricators using welded-wire mesh and glass fibers in lightweight expanded clay aggregate (LECA)-based self-consolidating slabs report a 45% increase in load-carrying capacity compared to unreinforced alternatives.

Higher Cost Versus Conventional Concrete

Lightweight concrete mixes incur a 15-25% cost premium due to the rotary-kiln energy requirements of 1.5-2.0 gigajoules (GJ) per ton, significantly higher than the 0.5 GJ per ton for crushed stone. While sintered fly-ash technology reduces fuel consumption, turnkey plants remain 30-40% more expensive than crushing units. Developers with single-digit profit margins face challenges in transferring these additional costs to homebuyers, limiting the use of lightweight concrete to high-end construction projects. Value-engineering studies indicate 5-10% total project savings when accounting for foundation costs, crane time, and schedule compression, but these life-cycle benefits are often overlooked due to siloed procurement practices.

Other drivers and restraints analyzed in the detailed report include:

- Reduction in Dead Load Enabling Cost-Efficient Designs

- Stricter Energy-Efficiency and Insulation Codes

- Scarcity of Premium Lightweight Aggregates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Expanded clay accounted for 34.44% of the lightweight aggregate concrete market in 2025, supported by established rotary-kiln infrastructure in Europe and Asia-Pacific. Perlite is the fastest-growing aggregate, with a projected growth rate of 4.58% through 2031. The market size associated with this segment is expected to grow steadily, driven by its suitability for bridge builders and retrofitting agencies due to its strength classes exceeding 40 megapascals (MPa). Perlite is anticipated to grow 16 basis points faster than the overall aggregate category, benefiting from its low thermal conductivity of 0.08 watts per meter-kelvin (W/mK), which is particularly suitable for 3D printing and ultra-insulating screeds.

In the United States, expanded shale and slate are widely used in structural applications requiring densities above 1,600 kilograms per cubic meter (kg/m3) and compressive strengths exceeding 6,000 pounds per square inch (psi), as demonstrated by projects like California's Shasta Arch Bridge. Pumice is primarily used in decorative and landscaping applications, with sourcing concentrated in the western United States and the Aegean region. Vermiculite and emerging bio-aggregates together account for less than 5% of the market volume due to cost and durability constraints. In China, pre-screened reservoir-silt pellets are expected to diversify supply once JC/T 2772-2024 standards enable non-structural applications up to LC25.

Geography Analysis

Asia-Pacific accounted for 47.89% of the projected 2025 revenue and is expected to grow at a rate of 6.11% through 2031, nearly 50% higher than the global lightweight aggregate concrete market growth rate. In China, the JC/T 2772-2024 mandate for recycled content in lightweight aggregates has introduced new supply chains, diverting demolition waste from landfills. Additionally, 26-story towers in Benxi demonstrated a 21-25% reduction in self-weight, leading to smaller seismic base shear forces. In India, precast operators have reduced project timelines by up to 50% using branded lightweight mixes, which also serve as passive cooling mass in tropical climates. Japan's adoption is driven by seismic performance improvements, with lightweight ultrahigh-strength concrete achieving 100 megapascals (MPa) strength at densities below 2,100 kilograms per cubic meter (kg/m3).

North America's market growth is supported by Arcosa's kiln network, strategic mergers and acquisitions, and Bridge Authority pilot projects. Following a USD 450 million barge divestiture and a USD 60 million aggregate acquisition in Florida, Arcosa has redirected capital toward higher-margin infrastructure-grade products. Titan America's artificial intelligence (AI)-enabled mix design platform optimizes performance and carbon footprint predictions, reducing quotation cycles from weeks to hours. Florida's regulatory endorsement of lightweight roof fills for hurricane-prone areas highlights growing regional acceptance.

Europe emphasizes carbon reduction and heritage rehabilitation. Projects such as the KabelstraBen-Brucke in Wuppertal and the bridge widening in Straubing achieved 100-ton weight savings, preserving existing structural piers. Norway's BetongVIND initiative and the Horizon-Europe MADE4WIND consortia are positioning lightweight concrete as a critical component for deep-water wind projects, targeting an 80% reduction in carbon dioxide (CO2) emissions for serial gravity-foundation production. In the United Kingdom, LECA's third-party-verified Environmental Product Declarations (EPDs) support buildings in securing Building Research Establishment Environmental Assessment Method (BREEAM) credits while aligning with 2030 carbon reduction goals.

South America benefits from Votorantim Cimentos' BRL 5 billion (USD 0.97 billion) expansion, which will increase Mato Grosso's production capacity to 1.2 million tons and achieve a 90% renewable energy grid mix by March 2026. The Middle East and Africa are in the early stages of adoption, with applications concentrated in Saudi Arabia's high-rise cores and liquefied natural gas (LNG) terminals, where weight reductions help minimize quay wall reinforcement. However, reliance on imports and high freight costs remain significant barriers to broader regional uptake.

- Arcosa Lightweight

- Argex SA

- Boral Limited

- Buildex

- Cemex S.A.B DE C.V.

- Charah Solutions Inc.

- CRH

- H+H International

- Heidelberg Materials AG

- Holcim

- Laterlite SpA

- Leca International

- Liapor Group

- PORAVER

- Pumice Products International

- Saint-Gobain

- Titan America

- Votorantim Cimentos

- Vulcan Materials Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Lightweight and High-Strength Construction Materials

- 4.2.2 Increasing Use in High-Rise and Precast Structures

- 4.2.3 Reduction in Dead Load Enabling Cost-Efficient Designs

- 4.2.4 Stricter Energy-Efficiency and Insulation Codes

- 4.2.5 Emerging 3D-Printed Concrete Applications

- 4.3 Market Restraints

- 4.3.1 Higher Cost Versus Conventional Concrete

- 4.3.2 Scarcity of Premium Lightweight Aggregates

- 4.3.3 Moisture-Induced Variability in Mechanical Properties

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type of Aggregate

- 5.1.1 Expanded Clay

- 5.1.2 Expanded Shale

- 5.1.3 Expanded Slate

- 5.1.4 Perlite

- 5.1.5 Pumice

- 5.1.6 Others (Vermiculite, Bio-aggregates)

- 5.2 By Application

- 5.2.1 Structural Concrete

- 5.2.2 Precast/Prefabricated Elements

- 5.2.3 Block and Panel Production

- 5.2.4 Bridge Decks and Infrastructure

- 5.2.5 Insulating Screeds and Roof Fills

- 5.2.6 Others

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Infrastructure

- 5.3.5 Energy and Utilities (Off-shore wind, LNG)

- 5.4 By Geography

- 5.4.1 Asia-pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Australia and New Zealand

- 5.4.1.6 ASEAN Countries

- 5.4.1.7 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Arcosa Lightweight

- 6.4.2 Argex SA

- 6.4.3 Boral Limited

- 6.4.4 Buildex

- 6.4.5 Cemex S.A.B DE C.V.

- 6.4.6 Charah Solutions Inc.

- 6.4.7 CRH

- 6.4.8 H+H International

- 6.4.9 Heidelberg Materials AG

- 6.4.10 Holcim

- 6.4.11 Laterlite SpA

- 6.4.12 Leca International

- 6.4.13 Liapor Group

- 6.4.14 PORAVER

- 6.4.15 Pumice Products International

- 6.4.16 Saint-Gobain

- 6.4.17 Titan America

- 6.4.18 Votorantim Cimentos

- 6.4.19 Vulcan Materials Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Modular and prefabricated construction adoption

全球輕質骨材混凝土市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球輕質骨材混凝土市場規模、佔有率、趨勢和成長分析報告(2026-2034) 輕質骨材混凝土市場規模、佔有率和成長分析(按骨材類型、應用、終端用戶產業和地區分類)-2026-2033年產業預測

輕質骨材混凝土市場規模、佔有率和成長分析(按骨材類型、應用、終端用戶產業和地區分類)-2026-2033年產業預測 輕質骨材混凝土市場規模、佔有率和趨勢分析報告:按應用、混凝土類型、地區和細分市場預測(2025-2033 年)

輕質骨材混凝土市場規模、佔有率和趨勢分析報告:按應用、混凝土類型、地區和細分市場預測(2025-2033 年) 輕骨材混凝土市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區和競爭細分,2020-2030 年)

輕骨材混凝土市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區和競爭細分,2020-2030 年) 全球輕骨材混凝土市場全球輕骨材混凝土市場規模(依產品類型、應用、地區和預測)

全球輕骨材混凝土市場全球輕骨材混凝土市場規模(依產品類型、應用、地區和預測) 輕骨材混凝土市場報告:2031 年趨勢、預測與競爭分析

輕骨材混凝土市場報告:2031 年趨勢、預測與競爭分析