|

市場調查報告書

商品編碼

2062377

K-12教師技術培訓:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)K-12 Technology Training For Teachers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

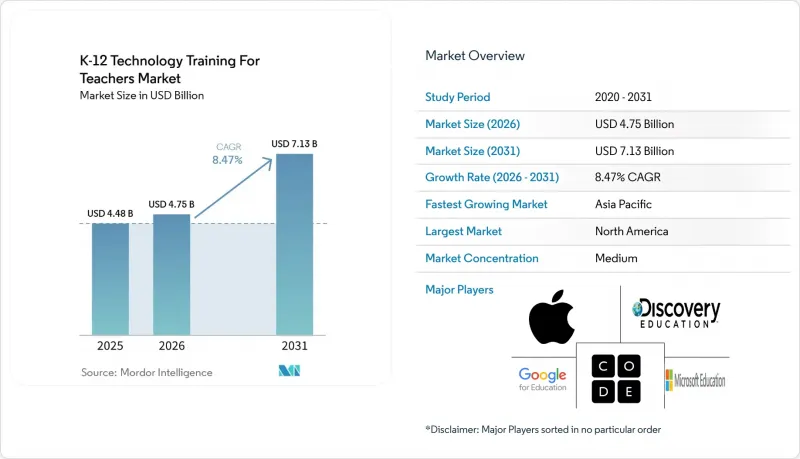

根據 Mordor Intelligence 預測,K-12 教師技能培訓的市場規模預計將從 2025 年的 44.8 億美元和 2026 年的 47.5 億美元成長到 2031 年的 71.3 億美元,2026 年至 2031 年的複合年成長率為 8.47%。

本報告按培訓形式(線上自學、講師主導的虛擬培訓等)、交付模式(訂閱式專業發展平台、計量收費課程等)、技術領域(基礎數位素養、STEM 等)、最終用戶群(小學教師、中學教師等)和地區進行細分。市場預測以美元計價。

全球K-12教師技術培訓市場趨勢與洞察

混合型光電探測器在全球的應用正在加速。

混合式專業發展模式將即時小組課程與非同步微課程結合,旨在滿足學區提高課程完成率和課堂實際應用能力的需求,同時避免增加教師的業餘時間負擔。洛杉磯聯合學區 (LAUSD) 的微證書系統清晰地分類了面授時間、線上模組和實踐作業,從而提高了完成率、教師獲得加分資格並提升了教師參與度。學區團隊指出,即時互動模式(用於模型演示和問答)、靈活的學習進度安排(以適應繁忙的日程)以及嵌入式(用於在課堂應用前澄清誤解),都符合 2026 年的實際需求。 PowerSchool University 的開放實驗室和嵌入式的微培訓(伴隨產品更新)透過解決教師現有工具中時間緊迫的工作流程變更問題,完善了混合式學習路徑。這些措施降低了與學習管理系統 (LMS) 和內容更新相關的流失率,並促進了 K-12 教師技術培訓市場新功能的持續應用。由於混合教學模式與合約課程和認證學分相符,因此正逐漸成為希望大規模提高技術素養的學區的首選。

對用於課堂教學的人工智慧產生數據的需求

學區正努力彌合學生對人工智慧的熟悉程度與教師使用人工智慧工具的熟練程度之間的差距,方法是在其專業發展課程目錄中優先考慮人工智慧素養和負責任使用框架。 2026年4月,Google推出了Gemini認證教育者考試,提供六個月的免費試用期,將經過檢驗的人工智慧認證定位為全球K-12教育工作者能力的可擴展衡量標準。微軟的Elevate for Educators計畫於2026年啟動,提供免費認證、人工智慧社群以及將課程推出和評估與安全實踐相結合的Microsoft 365 Copilot教學應用程式。 Discovery Education整合生態系統整合了IBM SkillsBuild專業發展課程和AI TeacherTools,使教育工作者能夠根據課堂資源和學生資料獲得情境化建議。政策也是一個重要的促進因素;中國於2026年4月公佈的「AI+教育」計畫要求到2030年將人工智慧能力納入教師資格考試,這將擴大整個教育系統對以人工智慧為重點的專業發展(PD)的需求。這些趨勢將提高2026年K-12教師技術培訓市場對人工智慧素養和安全實踐的最低標準。

ESSER計畫結束後,PD預算將會減少。

2025年付款期限的延長限制擾亂了許多學區的多年期專業發展(PD)計劃,導致強制性資金的去向不明朗,並暫停了對培訓機構的付款。 2026年,擁有完善證據體系的學區將能夠透過將專業發展完成情況與學生成績和檢驗的資格證書掛鉤,更有效地爭取預算續約。雖然第二類A項撥款仍然是基礎性的,但管理者現在優先考慮提案能夠提供清晰途徑獲得校際認可的證書和薪資成長的方案。培訓機構正在透過實施證據檔案和合規模組來應對這一變化,使學區即使在預算縮減的情況下也能維持培訓名額。這一趨勢有利於K-12教師技能培訓市場中那些能夠證明有效性並允許跨雇主重複使用資格證書的解決方案。這種轉變導致一次性研討會減少,而更加重視具有檢驗評估和透明參與者名單的多期系列培訓。

細分市場分析

2025年,線上自主學習和虛擬學習模式將佔據37.38%的市場佔有率,但隨著教師尋求更靈活的學習進度和即時小組互動,混合式學習預計將以14.36%的複合年成長率成長至2031年。 K-12教師技能培訓市場正轉向結契約步和非同步實踐的混合模式,這有助於教師更好地適應工作時間,並減少因長時間晚間課程造成的職業倦怠。學區透過要求提交作品集和課堂實踐成績來獲得學分和獎勵,從而提高課程完成率,進而促進教師對新技能的更深入掌握。整合到學習管理系統(LMS)入口網站中的平台更新微培訓可在使用時提供及時支持,並增強日常應用。在儀表板中顯示有針對性的專業發展(PD)提案的內容生態系統,有助於教育工作者將培訓與學生的實際需求聯繫起來。隨著培訓機構將混合式設計與基於學區認證評估的資格證書相結合,K-12教師技能培訓市場正從中受益。

當「電腦科學原理」和「電腦科學應用」等課程中的混合式課程包含基於實證的回饋和課堂實踐指導時,課程完成率和留存率都會提高。隨著學區將結合即時互動和非同步練習的小組模式標準化,預計K-12教師技能培訓市場中混合式教學模式的規模將會擴大。雖然在出行受限的情況下,即時虛擬研討會不失為一個選擇,但由於時區和覆蓋範圍的限制,大規模學區的參與度仍然有限。培訓機構正在添加簡短的複習內容,使教師能夠在更新後無需重複學習整個模組即可重新學習工作流程,從而支持2026年的持續變革週期。與認證和學區薪酬系統的銜接能夠提高教師完成包含基於實證的作業和實踐任務的混合式課程的積極性。預計這種模式將在K-12教師技能培訓市場中超越傳統的自主學習模式。

到2025年,教育機構的全區合約和計畫將佔39.87%。這主要歸功於平台提供者將教師培訓(PD)整合到多年續約週期的學生資訊系統(SIS)和學習管理系統(LMS)合約中。隨著教育工作者對可跨校通用的認證和基於實證的資格要求日益成長,基於認證和訂閱的平台預計將以15.44%的複合年成長率成長。 K-12教師技術培訓市場也反映了這一趨勢,學區在維持大規模生態系統合約的同時,還會增加訂閱課程以滿足合約續約期間的新能力要求。 2026年,Google推出了為期六個月的Gemini教育者認證免費試用,旨在大規模推廣人工智慧素養,不受語言或背景的限制。微軟的「Elevate for Educators」計畫提供免費認證和人工智慧社區,學區可以在其學校網路中部署這些資源,從而實現同儕互助和教學的連續性。這些變化提高了資格證書的可移植性,並減少了整個 K-12 教師技能培訓市場對一次性研討會的依賴。

預計到2025年,在K-12教師技能培訓市場中,全區合約仍將佔據最大佔有率,但由於訂閱和認證模式與薪資結構和合約續約的關聯性更加明確,其發展速度正在加快。協會和非營利組織正在推廣基於能力的評估,透過評估課堂表現而非課時來衡量能力,這種評估方式正獲得獨立教育工作者和尋求專業認證的中學教師的支持。州津貼的計畫會根據其覆蓋範圍和學員組成影響完成率。這些都是各學區在選擇優先認證夥伴時會考慮的因素。學員名冊同步和完成記錄互通性正在推動這些模式的普及,因為它們可以減輕行政負擔並簡化專業發展協調員的審查工作。隨著認證標準的日益明確,訂閱和認證計畫學員群體正逐漸成為K-12教師技能培訓市場中與全區合約相輔相成的常態。

區域分析

2025年,北美地區佔了K-12教師技能培訓市場37.35%的佔有率。這主要歸功於各學區將專業發展(PD)與多年生態系統合約結合,並妥善管理ESSER改革後的過渡期,這影響了對供應商的付款和合約續約。州級電腦科學(CS)認證政策的訂定,增加了對結構化培訓的需求,這些培訓能夠記錄教師能力並滿足中學和高中的人員配置計劃。 OneRoster和Ed-Fi等互通性標準持續影響認證的可移植性和名冊管理實踐,簡化了學區的稽核和合規流程。供應商贊助的活動和開放實驗室式的舉措加速了新功能的普及,教師可以從工程師那裡獲得關於日常使用特定工具的實際操作指導。 2024年主要平台所有權的變更,進一步強化了捆綁式專業發展在2026年提高大規模學區教師留存率的角色。

在亞太地區,隨著各國政府將人工智慧素養和與教師資格相符的培訓列為優先事項,預計到2031年,市場將以13.38%的複合年成長率成長。亞太地區K-12教師技術培訓市場預計將持續成長,因為各國教育部門將資格資訊整合到國家平台,並建立同儕社群以促進科技的持續應用。中國的「人工智慧+教育」計畫要求在2030年將人工智慧能力納入教師資格考試,這為長期的專業發展需求奠定了基礎。透過「學習影響日本」等區域交流項目,支持互通性和證據追蹤的標準、計劃和專業發展設計實踐正在推廣。東南亞教育部長舉措)主導的計劃和國家計畫繼續強調可應用於不同學校系統的混合式教學模式和能力框架。

在歐洲,隨著成員國採用 DigCompEdu 並推廣混合式專業發展(PD)模式(將即時小組學習與基於國家平台的非同步模組相結合),DigCompEdu 的應用持續穩步成長。設備和顯示生態系統正在表彰那些持續進行專業發展活動並建立教師社區的優秀學校,這些學校促進者了永續使用和課堂創新。在拉丁美洲,透過公私合營和區域合作夥伴,中學和初中階段的研討會正在進行,以推動電腦科學(CS)和人工智慧(AI)的教師培訓。在中東和非洲,與認證計畫和平台的合作正在促進正式的專業發展社群的建立,但預算和通訊基礎設施正在影響區域進展的速度和規模。這些區域趨勢共同支撐著 K-12 教師技術培訓市場在 2026 年的多元化成長前景。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 混合型光電探測器在全球的應用正在加速。

- 教師使用人工智慧生成課程的培訓需求。

- 強制推行電腦科學(CS)課程將促進教師的專業發展。

- LMS的快速升級需要重新訓練。

- 基於微證書的獎勵能夠促進技能發展。

- 互通性和工作計畫制定標準需要培訓。

- 市場限制因素

- 自 ESSER 專案結束後,PD 預算有所減少。

- 教師職業倦怠限制了他們專業發展的時間。

- 認證體系的碎片化正在減緩資格認證的普及速度。

- 由於採購和隱私審查,試點項目已被推遲。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按培訓類型

- 線上自學

- 講師主導的虛擬

- 混合

- 現場研討會

- 透過串流媒體模式

- 基於訂閱的PD平台

- 計量型課程

- 全區合約

- 認證項目

- 按技術領域

- 基本數位素養

- STEM/程式設計與機器人

- LMS使用情況

- 新興科技(擴增實境/虛擬實境、人工智慧)

- 網路安全和資料隱私

- 最終用戶

- 國小教師

- 國中教師

- 高中教師

- 特殊教育教師

- 按地區

- 北美洲

- 加拿大

- 美國

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟

- 北歐的

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介[]

- Google for Education

- Microsoft Education

- Apple Education

- Discovery Education

- BetterLesson

- Instructure(Canvas/Impact)

- PowerSchool(Schoology Learning)

- ISTE+ASCD(ISTE Certification)

- Common Sense Education(PD)

- Code.org(Teacher Professional Learning)

- LEGO Education(Professional Development)

- Edmentum(Professional Services)

- HMH(Professional Learning)

- Savvas Learning Company(Professional Learning)

- Amplify(Professional Development)

- Nearpod(PD/Camp Engage)

- Seesaw(Training & PD)

- Promethean(Learn Promethean)

- SMART Technologies(Learn SMART)

- GoGuardian(Training/University)

- Teq(OTIS for Educators)

- D2L Brightspace(K-12 Professional Learning)

- Blackboard/Anthology(Professional Development)

第7章 市場機會與未來展望

According to Mordor Intelligence, the k-12 technology training for teachers market size is projected to expand from USD 4.48 billion in 2025 and USD 4.75 billion in 2026 to USD 7.13 billion by 2031, registering a CAGR of 8.47% between 2026 to 2031.

This report is Segmented by Training Modality (Online Self-Paced, Instructor-Led Virtual, and More), Delivery Mode (Subscription-Based PD Platforms, Pay-As-You-Go Courses, and More), Technology Focus (Basic Digital Literacy, STEM, and More), End-User Level (Elementary School Teachers, Middle School Teachers, and More), and Geography. The Market Forecasts are Provided in Value (USD).

Global K-12 Technology Training For Teachers Market Trends and Insights

Hybrid PD Adoption Accelerates Globally

Blended professional development that merges live cohort sessions with asynchronous micro-lessons is scaling as districts seek better completion and classroom transfer without increasing after-hours demands. LAUSD's micro-credentialing structure uses a clear split between face-to-face time, online modules, and applied homework, leading to high completion and salary point eligibility, which reinforces teacher participation. District teams cite real-time interaction for modeling and Q&A, flexible pacing for busy schedules, and embedded check-ins that surface misconceptions before classroom use, which fit practical needs in 2026. PowerSchool University's open labs and embedded micro-trainings around product updates complement hybrid pathways by addressing time-sensitive workflow changes within the tools teachers already use. These practices reduce churn during LMS or content updates and encourage sustained use of new features inside the K-12 technology training for teachers market. As hybrid formats align with contract time and recognized credits, they become a default choice for districts upgrading technology fluency at scale.

Generative AI Classroom PD Demand

Districts are moving to close the proficiency gap between student familiarity with AI and teacher use of AI-aligned tools by prioritizing AI literacy and responsible-use frameworks in PD catalogs. Google introduced the Gemini Certified Educator exam in April 2026, offering a six-month free window, positioning verified AI credentials as a scalable signal of competency for K-12 educators worldwide. Microsoft's Elevate for Educators program created no-cost credentials, AI communities, and a Teach in Microsoft 365 Copilot app that aligns lesson planning and assessments with safe practice in 2026. Discovery Education's connected ecosystem integrates IBM SkillsBuild PD and AI TeacherTools, so educators receive contextual nudges tied to classroom resources and student data. Policy is also a catalyst, with China's April 2026 AI Plus Education plan embedding AI competencies into teacher qualification exams by 2030, which expands AI-focused PD demand system-wide. These developments raise the floor for AI literacy and safe practice in the K-12 technology training for teachers market in 2026.

Post-ESSER PD Budgets Compress

Late-liquidation limits in 2025 created uncertainty for obligated funds and paused payments to providers, which disrupted multi-year PD planning in many districts. Districts with strong evidence systems can better defend renewals by linking PD completions to student outcomes and verified credentials in 2026. Title II-A funding remains a baseline, but administrators now prioritize offers with clear pathways to endorsements and salary credits that are recognized across schools. Providers have adapted with evidence portfolios and compliance-ready modules that help districts retain training lines within slimmer budgets. This favors solutions that demonstrate impact and credential portability across employers in the K-12 technology training for teachers market. The shift reduces one-off workshops and elevates multi-session sequences with verified assessments and transparent rostering.

Other drivers and restraints analyzed in the detailed report include:

- CS Mandates Expand Teacher PD

- Rapid LMS Upgrades Require Retraining

- Teacher Burnout Limits PD Time

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Online self-paced and virtual formats held 37.38% share in 2025, while blended learning is projected to grow at 14.36% CAGR through 2031 as teachers seek live cohort interaction with flexible pacing. The K-12 technology training for teachers market is shifting toward hybrid pathways that pair synchronous modeling with asynchronous practice, aligning with contract time and reducing burnout from extended evening sessions. Districts improve completion when portfolios and classroom application are required for credit and compensation, which encourages deeper transfer of new skills. Embedded micro-training on platform updates within LMS portals provides timely support at points of use, which strengthens day-to-day adoption. Content ecosystems that surface targeted PD nudges inside dashboards are helping educators link training to real student needs. The K-12 technology training for teachers market benefits when providers align a hybrid design to assessment-backed credentials recognized by districts.

Completion and persistence are stronger when blended courses include feedback on evidence and coaching on classroom implementation for curricula such as CS Principles and CSA. The K-12 technology training for teachers market size for blended modality is projected to grow as districts standardize cohort models with live touchpoints and asynchronous practice. Live virtual workshops remain an option when travel is limited, yet time zones and coverage still constrain participation in large districts. Providers add bite-sized refreshers so teachers can relearn workflows after updates without repeating full modules, which supports continuous change cycles in 2026. Alignment to recognized credentials and district salary lanes increases teacher motivation to complete blended pathways that include evidence and applied tasks. This modality is positioned to outpace legacy self-paced models inside the K-12 technology training for teachers market.

District-wide contracts and institutional programs accounted for 39.87% in 2025, as platform providers embedded PD into SIS and LMS agreements that renew on multi-year cycles. Certification-based and subscription platforms are forecast to grow at 15.44% CAGR as educators seek stackable recognition and evidence-based credentials that travel between schools. The K-12 technology training for teachers market reflects this mix as districts maintain large ecosystem agreements while adding subscription cohorts to address emerging competencies between contract refreshes. Google introduced a six-month free window for Gemini educator certification in 2026 to seed AI literacy at scale across languages and contexts. Microsoft's Elevate for Educators adds no-cost credentials and AI communities that districts can deploy within school-based networks to support peers and maintain continuity. These shifts increase credential portability and reduce reliance on one-off workshops across the K-12 technology training for teachers market.

Despite district-wide contracts accounting for the largest share of the K-12 technology training for teachers market in 2025, subscription and certification models now expand faster due to clear crosswalks into salary lanes and renewals. Associations and nonprofits scale competency-based assessment by validating classroom evidence rather than seat time, which appeals to self-directed educators and secondary teachers pursuing endorsements. State stipend programs influence completion rates based on coverage levels and cohort structure, factors that districts consider when choosing delivery partners for high-priority endorsements. Interoperability for roster sync and completion records is an adoption driver, since it lowers administrative overhead and simplifies audits for PD coordinators. As recognition clarity improves, subscription and certification cohorts become a regular complement to district-wide agreements inside the K-12 technology training for teachers market.

Geography Analysis

North America accounted for 37.35% of the K-12 technology training for teachers market share in 2025 as districts aligned PD with multi-year ecosystem contracts and managed post-ESSER transitions that affected provider payments and renewals. State-level CS endorsement policies strengthened demand for structured cohorts that document competencies and satisfy staffing plans across middle and high school. Interoperability standards such as OneRoster and Ed-Fi continued to shape credential portability and rostering practices, simplifying district audits and compliance. Vendor events and open-lab formats accelerated the adoption of new features as teachers received hands-on guidance from engineers on the exact tools they use every day. Ownership changes at major platforms in 2024 reinforced the role of bundled PD as a retention lever across large districts in 2026.

Asia-Pacific is projected to expand at a 13.38% CAGR through 2031 as national programs prioritize AI literacy and credential-aligned training for teachers. The K-12 technology training for teachers market in Asia-Pacific is set to grow as ministries embed credentials into national platforms and build peer communities that sustain adoption. China's AI Plus Education plan mandates AI competencies in teacher qualification exams by 2030, which anchors long-term PD demand. Regional exchanges such as Learning Impact Japan spread standards, work, and PD design practices that support interoperability and evidence tracking. SEAMEO-led initiatives and national projects continue to emphasize blended formats and competency frameworks that scale across diverse school systems.

Europe maintains steady adoption as member states align with DigCompEdu and expand hybrid PD that combines live cohorts and asynchronous modules anchored to national platforms. Device and display ecosystems recognize exemplary schools where ongoing PD and teacher communities drive sustained use and classroom innovation. Latin America advances CS and AI teacher training through public-private programs and regional partners that deliver facilitated workshops in secondary and middle grades. In the Middle East and Africa, recognition programs and platform partnerships encourage formal PD communities, while budgets and connectivity shape local pacing and scale. These regional patterns collectively support a diverse growth outlook for the K-12 technology training for teachers market in 2026.

- Google for Education

- Microsoft Education

- Apple Education

- Discovery Education

- BetterLesson

- Instructure (Canvas / Impact)

- PowerSchool (Schoology Learning)

- ISTE + ASCD (ISTE Certification)

- Common Sense Education (PD)

- Code.org (Teacher Professional Learning)

- LEGO Education (Professional Development)

- Edmentum (Professional Services)

- HMH (Professional Learning)

- Savvas Learning Company (Professional Learning)

- Amplify (Professional Development)

- Nearpod (PD / Camp Engage)

- Seesaw (Training & PD)

- Promethean (Learn Promethean)

- SMART Technologies (Learn SMART)

- GoGuardian (Training / University)

- Teq (OTIS for Educators)

- D2L Brightspace (K-12 Professional Learning)

- Blackboard / Anthology (Professional Development)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hybrid PD adoption accelerates globally

- 4.2.2 Generative AI classroom PD demand

- 4.2.3 CS mandates expand teacher PD

- 4.2.4 Rapid LMS upgrades require retraining

- 4.2.5 Micro-credential incentives spur upskilling

- 4.2.6 Interoperability, rostering standards demand training

- 4.3 Market Restraints

- 4.3.1 Post-ESSER PD budgets compress

- 4.3.2 Teacher burnout limits PD time

- 4.3.3 Fragmented credential recognition slows uptake

- 4.3.4 Procurement, privacy reviews delay pilots

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Threat of Substitutes

5 Market Size & Growth Forecasts

- 5.1 By Training Modality

- 5.1.1 Online Self-paced

- 5.1.2 Instructor-led Virtual

- 5.1.3 Blended

- 5.1.4 On-site Workshops

- 5.2 By Delivery Mode

- 5.2.1 Subscription-based PD Platforms

- 5.2.2 Pay-as-you-go Courses

- 5.2.3 District-wide Contracts

- 5.2.4 Certification Programs

- 5.3 By Technology Focus

- 5.3.1 Basic Digital Literacy

- 5.3.2 STEM / Coding & Robotics

- 5.3.3 LMS Utilisation

- 5.3.4 Emerging Tech (AR/VR, AI)

- 5.3.5 Cyber-security & Data Privacy

- 5.4 By End-User Level

- 5.4.1 Elementary School Teachers

- 5.4.2 Middle School Teachers

- 5.4.3 High School Teachers

- 5.4.4 Special Education Teachers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 Canada

- 5.5.1.2 United States

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX

- 5.5.3.7 NORDICS

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South-East Asia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East & Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East & Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles [(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)]

- 6.4.1 Google for Education

- 6.4.2 Microsoft Education

- 6.4.3 Apple Education

- 6.4.4 Discovery Education

- 6.4.5 BetterLesson

- 6.4.6 Instructure (Canvas / Impact)

- 6.4.7 PowerSchool (Schoology Learning)

- 6.4.8 ISTE + ASCD (ISTE Certification)

- 6.4.9 Common Sense Education (PD)

- 6.4.10 Code.org (Teacher Professional Learning)

- 6.4.11 LEGO Education (Professional Development)

- 6.4.12 Edmentum (Professional Services)

- 6.4.13 HMH (Professional Learning)

- 6.4.14 Savvas Learning Company (Professional Learning)

- 6.4.15 Amplify (Professional Development)

- 6.4.16 Nearpod (PD / Camp Engage)

- 6.4.17 Seesaw (Training & PD)

- 6.4.18 Promethean (Learn Promethean)

- 6.4.19 SMART Technologies (Learn SMART)

- 6.4.20 GoGuardian (Training / University)

- 6.4.21 Teq (OTIS for Educators)

- 6.4.22 D2L Brightspace (K-12 Professional Learning)

- 6.4.23 Blackboard / Anthology (Professional Development)

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment