|

市場調查報告書

商品編碼

2062356

導熱填料分散劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Thermally Conductive Filler Dispersants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

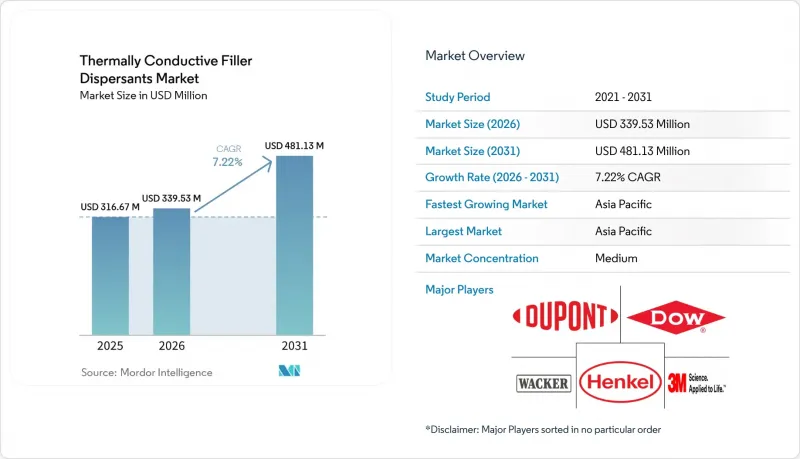

據 Mordor Intelligence 稱,2025 年導熱填料分散劑的市場規模為 3.1667 億美元,預計到 2031 年將達到 4.8113 億美元,而 2026 年為 3.3953 億美元,預測期(2026-2031 年)的複合年成長率為 7.22%。

本報告按填料類型(例如,氮化硼、氧化鋁)、配方(例如,液體分散體)、應用(例如,導熱界面材料 (TIM)、電絕緣化合物)、終端用戶行業(例如,電子行業)和地區(例如,亞太地區、北美地區)進行細分。市場預測以美元計價。

全球導熱填料分散劑市場趨勢及洞察

電動車電池和功率模組的熱通量密度激增

目前,液冷和浸沒式冷卻在300 Wh/kg電池組中普遍應用,電池極耳處的局部熱通量超過50 W/cm²。為了在0.3 mm的間隙內保持5 W/m·K的粘合線熱導率,贏創的ORTEGOL DA 801和杜邦的BETAMATE 2090等產品採用了與聚氨酯兼容的分散劑,這些分散劑能夠適應Z軸方向±0.2 mm的膨脹,從而無需耗能的烘箱固化。深圳飛龍達等中國整合商正與寧德時代合作,共同設計均熱板組件,並將分散劑整合到完整的散熱模組中,以確保足夠的裕量。然而,隨著浸沒式冷卻技術的日益普及,殘留離子雜質含量超過10 ppm仍然是一項挑戰。這些雜質會將介電液的電阻率降低到1 GΩ·cm以下,導致人們轉向使用超純填料。

與半導體節點小型化相關的熱點管理

在3D堆疊式高頻寬記憶體和200W CPU中,每個封裝最多可引入四個導熱介面材料(TIM)介面。除非填料間距保持在50nm以下,否則每層熱阻將增加0.15 K cm²/W。漢高公司的Bergquist TLF 6500 CGel-SF和英飛凌公司的銦合金連接件的指導原則要求使用分散劑,以穩定25µm鍵合線內85vol%的陶瓷填料,並防止在180 度C的回流焊接溫度下發生沉澱。由於封裝技術的這些進步,預計到2026年,高固態膏狀組合藥物的市場規模將增加8,500萬美元。

高黏度體系中聚合物-填料相容性的局限性

當陶瓷含量達到 80 vol% 時,空間位阻穩定作用失效,因為顆粒間的間隙縮小到小於分散劑流體動態半徑的兩倍。十八烷基接枝的梳狀聚矽氧烷的氧化鋁含量可達 87.8 vol%,電導率為 8.181 W/m·K,但其價格比線性 PDMS 高出 40%,限制了其在人工智慧加速器中的應用。可靠性測試揭示了一個相容性問題:含胺基的分散劑會發生遷移,導致 500 次熱循環後電導率下降 18%。相較之下,膦酸酯基改質材料仍能維持 96% 的電導率。

細分市場分析

預計到2025年,氮化硼將佔據導熱填料分散劑市場34.22%的佔有率。這主要歸功於其優異的性能,例如面內導熱係數高達300 W/m·K,體積電阻率低至10¹³ Ω·cm。然而,石墨和石墨烯正以7.33%的複合年成長率持續成長,對氮化硼的地位構成挑戰。這是因為中國在越南的合成石墨產能正以每年400萬平方公尺的速度成長,受惠於當地35%的低人事費用。氧化鋁在對成本敏感、導熱係數目標為3-5 W/m·K的應用中仍然佔據重要地位,而刷狀聚矽氧烷分散劑則在縮小與氮化硼性能差距的同時,將材料成本降低至五分之一。

碳化矽的熱導率高達 120 W/m·K,是引擎室電子設備中常用的機械增強材料。然而,950 度C的氧化製程會使加工成本增加 8-12 美元/公斤。對濕度敏感的氮化鋁仍是一種小眾材料,但透過聚對二甲苯 C 鈍化處理可以顯著改善其性能。即使浸入沸水中,氮化鋁仍能維持 97% 的熱導率,從而滿足航太領域的認證要求。

到2025年,液態分散體將佔據導熱填料分散劑市場46.36%的佔有率,這主要得益於其低於15 Pa·s的黏度,使其能夠噴射塗覆至厚度小於50 µm的黏合層。然而,在資料中心營運商對能夠承受±0.5 mm層厚公差且不會發生泵出(材料洩漏)的材料的需求推動下,膏狀和凝膠狀體系的複合年成長率預計到2031年將達到8.02%。 Bergquist TGF 10000 證明了觸變性和導熱性能可以兼得,在1000次循環後仍能保持10 W/m·K的導熱係數和小於5%的厚度漂移。

粉末狀添加劑可輔助熱塑性化合物製造商,而凝膠狀導熱材料 (TIM) 的邵氏 00 硬度為 60–70,並能適應不規則形狀。即使觸變改質劑的添加量增加 18%,網版印刷仍可節省每單位 0.32 美元的人事費用。固態含量上限仍為 85%(體積比),超過此限制會導致點膠過程中出現流動起始應力問題。瓶刷穩定型易傾倒液體的固含量超過此閾值,但僅限於人工智慧伺服器,因為 700 W 的噴嘴負載使得分散劑的成本達到每公斤 28 美元。

區域分析

預計到2025年,亞太地區將佔全球銷售額的44.45%,並在2031年之前以8.38%的複合年成長率成長,這主要得益於中國人工智慧伺服器的擴張以及韓國特種矽業務的成長。深圳飛龍達報告稱,透過與華為和比亞迪的合作,該公司2024年的銷售額達到50.31億元人民幣(約6.93億美元),預計2025年的利潤成長率將超過110%。中國思泉新材料公司維持97.47%的運轉率,並正在越南擴建400萬平方公尺的合成石墨薄膜生產線,以利用當地35%的低人事費用優勢。在韓國,蔚山和益山在瓦克化學和DENKA COMPANY LIMITED電子的投資推動下,被定位為氮化硼和矽導熱界面材料的創新中心。

在北美,杜邦位於密西根州的電池技術中心符合《通膨控制法案》的採購規定;漢高在其布蘭登工廠投資3,000萬美元進行擴建,預計到2027年,Bergquist的產量將提高40%,從而增強對使用700W GPU的超大規模資料中心的供應。加拿大的需求與強制推廣電動公車密切相關,而墨西哥則向二級汽車供應商提供成本最佳化的氧化鋁導熱介面材料(TIM)。

在歐洲,嚴格的REACH法規推動了向低VOC水性分散體的轉變,儘管不斷上漲的能源成本給利潤率帶來了壓力。陶氏化學正在考慮減少在英國和德國的矽氧烷產量,但其位於亞伯達的Path2Zero裂解裝置計畫(旨在2029年整合乙烯原料)正按計畫推進。同時,原始設備製造商(OEM)的脫碳努力正在加速可回收熱塑性導熱界面材料(TIM)的採用,為生物基化學品創造了新的機會。

南美、中東和非洲的總合仍然很低。雖然巴西靈活燃料混合動力汽車的成長和沙烏地阿美石化業務的發展刺激了對小眾TIM的需求,但當地填料產量有限阻礙了其快速普及。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電動車電池和功率模組的熱通量密度激增

- 與半導體製程小型化相關的熱點管理

- 過渡到低VOC、無鹵分散劑,優先考慮安全性。

- 原始設備製造商的脫碳目標正在推動可回收分散劑化學品的使用。

- 透過混合 BN + 石墨烯填料網路減少分散劑用量。

- 市場限制因素

- 高黏度體系中聚合物-填料相容性的局限性

- 逐步淘汰 PFAS 導致特殊溶劑短缺。

- 在混煉過程中,高長寬比填料會受到剪切損傷。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按填料類型

- 氮化硼(BN)

- 氧化鋁(Al2O3)

- 氮化鋁(AlN)

- 碳化矽(SiC)

- 石墨和石墨烯

- 陶瓷微球和玻璃珠

- 其他填料(炭黑、混合填料)

- 配方

- 液體分散劑

- 粉狀添加劑

- 膏狀和凝膠狀產品

- 透過使用

- 導熱界面材料(TIMs)

- 電絕緣化合物

- 導熱油脂和黏合劑

- 縫隙填充劑和灌封膠

- 封裝材料和底部填充物

- 其他用途

- 按最終用戶行業分類

- 電子設備

- 汽車和運輸業

- 建築/施工

- 發電

- 產業

- 航太

- 其他終端用戶產業(例如醫療保健)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Arkema

- ATLANTA

- Avient Corporation

- Cabot Corporation

- Dow

- DuPont

- Evonik Industries AG

- Henkel AG & Co. KGaA

- Momentive

- Resonac Holdings Corporation

- SANYO CHEMICAL, LTD.

- Shin-Etsu Chemical Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- Wacker Chemie AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the thermally conductive filler dispersants market size was valued at USD 316.67 million in 2025 and is estimated to grow from USD 339.53 million in 2026 to reach USD 481.13 million by 2031, at a CAGR of 7.22% during the forecast period (2026-2031).

This report is Segmented by Filler Type (Boron Nitride, Aluminum Oxide, and More), Formulation (Liquid Dispersions, and More), Application (Thermal Interface Materials (TIMs), Electrically-Insulating Compounds, and More), End-User Industry (Electronics, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Thermally Conductive Filler Dispersants Market Trends and Insights

Surge in EV Battery and Power-Module Heat-Flux Density

Liquid and immersion cooling are now dominant in 300 Wh/kg battery packs, where local heat fluxes exceed 50 W/cm2 at cell tabs. To maintain 5 W/m*K bond lines within 0.3 mm gaps, products like Evonik's ORTEGOL DA 801 and DuPont's BETAMATE 2090 utilize polyurethane-compatible dispersants that accommodate +-0.2 mm z-axis expansion while eliminating the need for energy-intensive oven curing. Chinese integrators, such as Shenzhen Feirongda, collaborate with CATL to co-design vapor-chamber assemblies, embedding dispersants within complete thermal modules to capture margins. However, as immersion cooling becomes more widespread, residual ionic impurities above 10 ppm remain a challenge, as they reduce dielectric-fluid resistivity below 1 GΩ*cm, prompting a shift toward ultrapure filler grades.

Semiconductor Node-Shrink Driven Hotspot Management

3D-stacked high-bandwidth memory and 200 W CPUs introduce up to four TIM interfaces per package, increasing thermal resistance by 0.15 K cm2/W per layer unless sub-50 nm filler spacing is maintained. Henkel's Bergquist TLF 6500 CGel-SF and Infineon's indium-alloy attach guidelines require dispersants that stabilize 85 vol% ceramic loadings within 25 µm bond lines while preventing sedimentation at 180 °C reflow temperatures. These advancements in packaging are expected to create an incremental addressable market of USD 85 million for high-solids paste formulations by 2026.

Polymer-Filler Compatibility Limits in High-Viscosity Systems

At ceramic loadings of 80 vol%, steric stabilization fails as inter-particle gaps shrink below twice the dispersant's hydrodynamic radius. Bottlebrush polysiloxanes with octadecyl grafts achieve 87.8 vol% alumina and 8.181 W/m*K but are 40% more expensive than linear PDMS, limiting their application to AI accelerators. Compatibility issues arise during reliability tests, where amine-terminated dispersants migrate, reducing conductivity by 18% after 500 thermal cycles. In contrast, phosphonate variants retain 96% conductivity.

Other drivers and restraints analyzed in the detailed report include:

- Safety-Driven Shift to Low-VOC, Halogen-Free Dispersants

- OEM Decarbonization Targets Favor Recyclable Chemistries

- PFAS Phase-Out Tightening Specialty-Solvent Availability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Boron nitride secured 34.22% of the thermally conductive filler dispersants market share in 2025, attributed to its 300 W/m*K through-plane conductivity and 1013 Ω*cm resistivity. However, graphite and graphene, expanding at a 7.33% CAGR through 2031, are challenging this position as Chinese synthetic-graphite capacity increases by 4 million m2 annually in Vietnam, benefiting from 35% lower labor costs. Aluminum oxide remains critical for cost-sensitive applications targeting 3-5 W/m*K, with bottlebrush polysiloxane dispersants reducing the performance gap to BN at one-fifth of the material cost.

Silicon carbide, with its 120 W/m*K conductivity, is the preferred choice for mechanical reinforcement in under-hood electronics, although its 950 °C oxidation step adds USD 8-12 per kg in processing costs. Moisture-sensitive aluminum nitride remains a niche material but benefits from Parylene-C passivation, which retains 97% conductivity after boiling-water immersion, enabling aerospace qualification pipelines.

Liquid dispersions held 46.36% of the thermally conductive filler dispersants market in 2025, supported by viscosities below 15 Pa*s that allow jetting into sub-50 µm bond lines. However, paste and gel systems are growing at an 8.02% CAGR through 2031, driven by data-center operators' need for materials that can withstand +-0.5 mm stack tolerances without pump-out. Bergquist TGF 10000 demonstrates that thixotropy can coexist with thermal performance, maintaining 10 W/m*K and less than 5% thickness drift over 1,000 cycles.

Powder additives support thermoplastic compounders, while gel TIMs offer Shore 00 hardness of 60-70, conforming to irregular geometries. Screen printing reduces labor costs by USD 0.32 per unit, even after accounting for the 18% dose premium of thixotropic modifiers. The solids content ceiling remains at 85 vol%; exceeding this limit results in yield stress issues during dispensing. Bottlebrush-stabilized pourable liquids surpass this threshold but are limited to AI servers, where USD 28 per kg dispersant costs are justified by 700 W chip loads.

Geography Analysis

Asia-Pacific generated 44.45% of 2025 revenue and is set to grow at an 8.38% CAGR through 2031 on the back of China's AI-server build-outs and South Korea's specialty silicone expansions. Shenzhen Feirongda reported RMB 5.031 billion (USD 693 million) 2024 revenue and greater than 110% 2025 profit growth from partnering with Huawei and BYD. China's Siquan New Materials, running 97.47% utilization, is adding 4 million m2 synthetic-graphite film capacity in Vietnam to leverage 35% cheaper labor. South Korea, buoyed by Wacker and Denka investments, positions Ulsan and Iksan as hubs for BN and silicone TIM innovation.

In North America, DuPont's Battery Technology Center in Michigan aligns with Inflation Reduction Act sourcing rules, while Henkel's USD 30 million Brandon expansion will raise Bergquist output 40% by 2027 to serve hyperscale data centers using 700 W GPUs. Canada's demand is tied to electric-bus mandates, whereas Mexico supplies cost-optimized alumina TIMs to Tier 2 automotive plants.

Europe is anchored by strict REACH rules, pushing suppliers toward low-VOC water-based dispersions even as high energy costs squeeze margins. Dow is evaluating UK and German siloxane cutbacks but keeps its Alberta Path2Zero cracker on schedule for 2029 ethylene feedstock integration. Meanwhile, OEM decarbonization pledges accelerate recyclable thermoplastic TIM adoption, giving an opening to bio-based chemistries.

South America and Middle-East and Africa collectively hold lower shares. Brazil's flex-fuel hybrids and Saudi Aramco's petrochemical growth spur niche TIM demand, but limited local filler production continues to hinder rapid uptake.

- 3M

- Arkema

- ATLANTA

- Avient Corporation

- Cabot Corporation

- Dow

- DuPont

- Evonik Industries AG

- Henkel AG & Co. KGaA

- Momentive

- Resonac Holdings Corporation

- SANYO CHEMICAL, LTD.

- Shin-Etsu Chemical Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in EV battery and power-module heat-flux density

- 4.2.2 Semiconductor node-shrink driven hotspot management

- 4.2.3 Safety-driven shift to low-VOC, halogen-free dispersants

- 4.2.4 OEM decarbonisation targets favour recyclable dispersant chemistries

- 4.2.5 Hybrid BN + graphene filler networks lowering dispersant loadings

- 4.3 Market Restraints

- 4.3.1 Polymer/filler compatibility limits in high-viscosity systems

- 4.3.2 PFAS phase-out tightening specialty-solvent availability

- 4.3.3 Shear-induced damage to high-aspect-ratio fillers during compounding

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Filler Type

- 5.1.1 Boron Nitride (BN)

- 5.1.2 Aluminum Oxide (Al2O3)

- 5.1.3 Aluminum Nitride (AlN)

- 5.1.4 Silicon Carbide (SiC)

- 5.1.5 Graphite and Graphene

- 5.1.6 Ceramic Microspheres and Glass Beads

- 5.1.7 Other Filler Types (Carbon Black, Hybrid)

- 5.2 By Formulation

- 5.2.1 Liquid Dispersions

- 5.2.2 Powder Additives

- 5.2.3 Paste/Gel Systems

- 5.3 By Application

- 5.3.1 Thermal Interface Materials (TIMs)

- 5.3.2 Electrically-Insulating Compounds

- 5.3.3 Thermal Greases and Adhesives

- 5.3.4 Gap Fillers and Potting Compounds

- 5.3.5 Encapsulation and Underfills

- 5.3.6 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Electronics

- 5.4.2 Automotive and Transportation

- 5.4.3 Building and Construction

- 5.4.4 Power Generation

- 5.4.5 Industrial

- 5.4.6 Aerospace

- 5.4.7 Other End-user Industries (Medical, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 ATLANTA

- 6.4.4 Avient Corporation

- 6.4.5 Cabot Corporation

- 6.4.6 Dow

- 6.4.7 DuPont

- 6.4.8 Evonik Industries AG

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Momentive

- 6.4.11 Resonac Holdings Corporation

- 6.4.12 SANYO CHEMICAL, LTD.

- 6.4.13 Shin-Etsu Chemical Co., Ltd.

- 6.4.14 Sumitomo Chemical Co., Ltd.

- 6.4.15 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

2026年全球奈米碳管(CNT)導電添加劑市場報告

2026年全球奈米碳管(CNT)導電添加劑市場報告 導熱填料分散劑市場規模、佔有率及成長分析:依填料類型、原料、應用、終端用戶產業及地區分類-2026-2033年產業預測

導熱填料分散劑市場規模、佔有率及成長分析:依填料類型、原料、應用、終端用戶產業及地區分類-2026-2033年產業預測 塑膠填料市場:全球市場預測(按填料類型、形態、聚合物類型、最終用途產業和應用分類)—2026-2032年

塑膠填料市場:全球市場預測(按填料類型、形態、聚合物類型、最終用途產業和應用分類)—2026-2032年 全球導電填料市場規模、佔有率、趨勢和成長分析報告(2026-2034)混凝土填料市場:按產品類型、應用和最終用途產業分類-2026-2032年全球市場預測

全球導電填料市場規模、佔有率、趨勢和成長分析報告(2026-2034)混凝土填料市場:按產品類型、應用和最終用途產業分類-2026-2032年全球市場預測 航太填料複合材料市場規模、佔有率和成長分析:按填料類型、配方類型、應用領域、最終用戶和地區分類-2026-2033年產業預測

航太填料複合材料市場規模、佔有率和成長分析:按填料類型、配方類型、應用領域、最終用戶和地區分類-2026-2033年產業預測 導熱奈米材料市場分析與預測(至2035年):類型、應用、產品類型、材料類型、技術、最終用戶、形態、組件、功能、工藝2026-2034年全球導熱填料和分散劑市場規模、佔有率、趨勢和成長分析報告

導熱奈米材料市場分析與預測(至2035年):類型、應用、產品類型、材料類型、技術、最終用戶、形態、組件、功能、工藝2026-2034年全球導熱填料和分散劑市場規模、佔有率、趨勢和成長分析報告 奈米填料市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、物理形態、應用、地區和競爭格局分類,2021-2031年)氮化硼填料市場按形態、粒徑、等級、應用和分銷管道分類-2026-2032年全球預測

奈米填料市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、物理形態、應用、地區和競爭格局分類,2021-2031年)氮化硼填料市場按形態、粒徑、等級、應用和分銷管道分類-2026-2032年全球預測