|

市場調查報告書

商品編碼

2062352

金屬惰性:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Metal Deactivator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

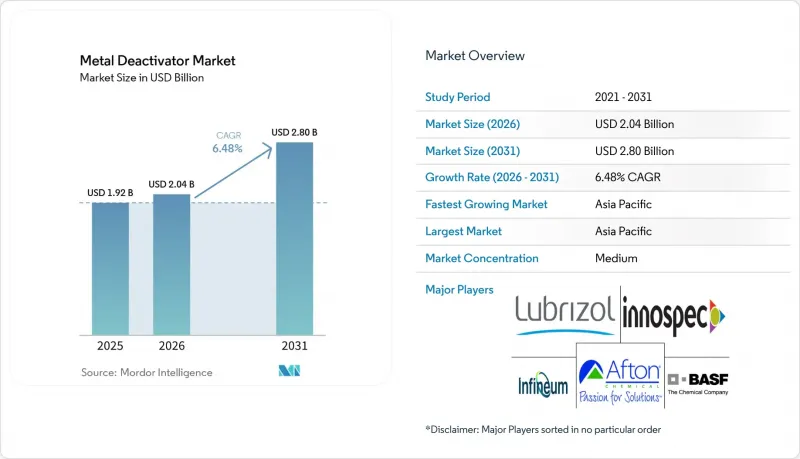

據 Mordor Intelligence 稱,金屬惰性的市場規模預計將從 2025 年的 19.2 億美元成長到 2026 年的 20.4 億美元,到 2031 年達到 28 億美元,2026 年至 2031 年的複合年成長率為 6.48%。

本報告按類型(燃料添加劑、潤滑油添加劑等)、化學性質(含氮螯合劑、含硫化合物等)、應用(汽油、柴油等)、終端用戶產業(汽車和運輸、石油、天然氣和煉油等)以及地區(亞太地區、北美地區、歐洲地區等)進行細分。市場預測以美元計價。

全球金屬惰性市場趨勢及洞察

燃料和潤滑油長期穩定性的需求日益成長

隨著乘用車和工業用油換油週期的延長,化合物製造商需要將金屬惰性與高性能抗氧化劑混合,以防止銅催化劑氧化,以避免油泥和漆膜的形成。合成酯和聚α烯烴比礦物油基油更容易發生過渡金屬劣化,因此惰性對於滿足ACEA C5和API SP標準至關重要,這些標準認證的換油週期為10,000英里或更長。全球潤滑油添加劑市場預計到2025年將達到224億美元,這推動了對包含金屬惰性的多功能添加劑組合的結構性需求,以控制氧化和腐蝕。生質柴油混合物在原料加工過程中會保留銅。實驗室測試表明,濃度為300-500 ppm的水楊醛螯合劑可以抑制過氧化物的形成並延長保存期限。受歐盟生態標籤標準的推動,生物基和精煉基礎油的成長正在促進與極性酯相容的氮螯合劑的使用。在VDS-5 等 OEM 認證中,金屬催化劑的氧化作用會被明確評估,而惰性與下一代石油認證流程密切相關。

流體系統非鐵金屬的使用量增加

海軍艦艇中的銅鎳熱交換器、電動車中的鋁製散熱器以及液壓迴路中的黃銅接頭都會使流體暴露於催化作用表面。如果不進行鈍化處理,這些表面會加速劣化。根據美國海軍的數據,航空母艦上JP-5燃油的銅污染水平高達1000 ppb,每年使引擎大修成本增加10億美元。在電壓高於400V的電動車的快速充電冷卻迴路中,銅會發生電化學滲入絕緣冷卻液中,導致導電性波動,如果不進行螯合處理,則有短路的風險。同行評審的研究證實,過渡金屬在250 度C以上會催化噴射機燃料的氧化,研究表明,添加微量的N,N'-二水楊醛亞胺-1,2-丙二胺可減少80%的沉積物質量。在符合IEC 60296標準的變壓器油中,苯並三唑衍生物用於保護銅繞組免受硫化物形成的影響,硫化物會降低介電強度。隨著銅在可再生能源齒輪箱和太陽能熱儲存系統中的應用日益廣泛,金屬惰性的市場正從汽車和航空航太領域擴展到其他產業。

對添加劑化學品實施嚴格的環境法規

2025年,歐洲化學品管理局(ECHA)將苯並三唑列入其持久、生物、技術和污染物(PBT)觀察名單,啟動了對其內分泌干擾效應的研究,並暗示未來可能製定濃度限制。同年,REACH法規附件XVII的修訂限制了16種CMR物質,其中包括二苯基(2,4,6-三甲基苯甲醯基)氧化膦,縮小了含磷惰性的選擇範圍。 ECHA擬議的批准清單包括三聚氰胺和氧化膦化合物,其日落期短至36個月,這要求迅速調整配方。歐盟監管藍圖強調了輪胎抗氧化劑6PPD因其水生毒性而受到關注,這反映出監管機構傾向於透過廣泛的禁令來統一控制添加劑。與測試和標籤相關的合規成本不斷上升,這對小規模混合商構成了障礙,導致擁有專門法規合規團隊的全球添加劑製造商佔據了市場主導地位。

細分市場分析

截至2025年,燃油添加劑將佔金屬惰性劑市場規模的46.71%,預計到2031年將以6.84%的複合年成長率保持其主導地位。這一主導地位歸因於諸多因素,例如對超低硫柴油燃料的需求、噴射機燃料的熱穩定性限制以及將金屬鈍化技術納入沉積物抑製配方的TOP TIER+汽油標準。潤滑油添加劑受益於合成油的日益普及和氫燃料引擎的出現,這些都需要有效的銅腐蝕抑制措施。聚合物穩定劑雖然是一個細分領域,但對於電線電纜絕緣至關重要,可以有效防止銅接觸件的劣化。其他小規模的細分市場包括金屬加工液。在該領域,水基冷卻液需要對銅和鋁進行保護,以滿足原始設備製造商(OEM)的腐蝕標準。

為了滿足 TOP TIER+ Revision G 和 MIL-PRF-25017 等認證要求,原始設備製造商 (OEM) 越來越重視多功能化學製劑,這類製劑結合了金屬惰性、清潔劑和抗氧化劑。例如,BASF的「Keropur」汽油系列和 Afton 的「HiTEC 65522」就整合了氮螯合劑和沈積物抑制劑,用於解決 GDI 引擎的噴油器積碳和隨機預燃問題。噴射機燃料中添加劑的監管限制,例如初始濃度 2.0 mg/L 和累積5.7 mg/L,正在推動高親和性氮螯合劑的創新,這些螯合劑在較低的添加劑下即可發揮作用,從而持續推動金屬惰性行業的進步。

預計到2025年,氮基螯合劑將佔據金屬惰性市場35.27%的佔有率,並在2031年之前以7.22%的複合年成長率成長。例如,N,N'-二水楊醛-1,2-丙二胺等化合物在2-5 ppm的低濃度下即可滿足ASTM D1655-22a噴射機燃料標準,而苯並三唑衍生物則在變壓器油鈍化領域佔據主導地位。與生物酯和環保潤滑油(EAL)的兼容性支撐了市場需求,尤其是在歐盟港口實施OSPAR指南後,這一趨勢更為顯著。硫基化合物在需要極壓性能的重柴油應用中仍然十分重要,但由於基於歐7和印度第六階段排放標準的更嚴格的硫排放法規,其長期發展潛力受到限制。磷基添加劑由於歐盟基於CMR分類對某些膦氧化物的法規而面臨重大挑戰。

結合苯並三唑和硼基分散劑的混合體系研究正在取得進展,該體系兼具金屬鈍化和抗氧化雙重功效,同時也能降低水生毒性。一項2026年的研究重點關注了氮摻雜奈米氧化鈰,其自由基清除能力提高了40倍,顯示其在氧化控制方面的潛力可能超過未來對螯合劑的需求。由於汽車製造商在電動車動力系統中更傾向於使用酯類潤滑油,預計氮基金屬惰性的市場將進一步擴大。

區域分析

預計到2025年,亞太地區將佔全球銷售額的44.67%,並維持7.22%的複合年成長率,直至2031年。中國9.36億噸的年煉油產能,加上東南亞國協航空旅行需求的兩位數成長,正在推動該地區金屬惰性市場的快速擴張。印度的「第六階段排放標準」(Bharat Stage VI)柴油硫量限制(10 ppm)禁止使用天然抗氧化劑,迫使煉油商在儲存和分銷過程中採用金屬惰性技術。在韓國,密集的快速充電網路內電動車冷卻迴路中的銅浸出問題日益突出,加速了對含螯合劑的絕緣冷卻劑的需求。基於「印度製造」和中國本土化計畫的在地化添加劑生產正在改變供應鏈結構,為區域製造商創造利潤空間,而全球巨頭則努力維持其OEM認證。

北美市場受益於美國環保署 (EPA) 嚴格的 Tier 3 汽油標準,該標準提高了加工速度,以及美國國防部對 JP-5 燃料中銅污染問題的關注。隨著航空母艦透過管道維修和添加劑過濾來降低維護成本,航空燃料中金屬惰性的市場佔有率正在上升。電動車 (EV) 製造商要求在電池導熱液中使用銅鈍化劑以防止導電性波動,這進一步推動了需求成長。儘管合規成本是意料之中,但由於法律規範成熟以及加拿大為符合歐盟 7 標準而提出的短期提案,合規成本仍然很高。

歐洲正面臨最嚴格的監管壓力。 REACH法規對苯並三唑的審查以及附件十七中新增的CMR物質降低了配方靈活性,用戶正轉向其他含氮化學品。德國和法國的變壓器充填計畫穩定了對苯並三唑的需求,但PBT(持久性、生物、技術和化學品)認定的可能性威脅著其長期銷售量。荷蘭將苯並三唑的淡水環境基準值(EQS)設定為97 µg/L,這可能會為廢水排放許可鋪平道路,從而鼓勵使用封閉回路型系統和替代物質。總體而言,儘管合規門檻不斷提高,但由於先進的汽車和航太應用,歐洲的需求仍然保持穩定。

其他地區則提供具有戰略意義的獨特市場。在中東,杜拜、杜哈和利雅德等噴射機燃料處理量的成長推動了高溫儲存環境下對鈍化劑的需求。在南美洲,強制性生物柴油的使用以及海上平台採用金屬惰性鑽井液也促進了鈍化劑市場的發展。雖然非洲的鈍化劑市場普及速度仍然緩慢,但需求仍然存在,尤其是在南非,對礦用油壓設備和老舊變壓器的需求尤其旺盛。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 燃料和潤滑油長期穩定性的需求日益成長

- 流體系統非鐵金屬的使用量增加

- 加強對氧化穩定性的監管

- 航空和船舶燃料的廣泛應用

- 快速充電電動車冷卻迴路中銅浸出量激增

- 高壓變壓器更新

- 市場限制因素

- 對添加劑化學成分的嚴格環境法規

- 原物料價格波動

- 奈米氧化鈰基抗氧化劑作為替代品

- 向固態電池的轉變將抑制對介電液體的需求。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 燃油添加劑

- 潤滑劑添加劑

- 聚合物穩定劑

- 其他(塗料、金屬加工液)

- 化學物質

- 含氮螯合劑

- 硫化合物

- 磷化合物

- 胺衍生物

- 其他金屬鈍化劑

- 透過使用

- 汽油

- 柴油引擎

- 噴射機燃料

- 渦輪機和壓縮機油

- 變壓器和絕緣油

- 聚合物和塑膠穩定劑

- 其他用途(冷卻劑、潤滑脂、塗料)

- 按最終用戶行業分類

- 汽車和運輸業

- 石油、天然氣和煉油

- 工業設備及製造

- 航太/國防

- 能源公用事業

- 海上

- 其他終端用戶產業(電子、塑膠、電力)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- ADEKA CORPORATION

- Afton Chemical

- BASF

- Bodo Moller Chemie GmbH

- Chevron Oronite Company LLC.

- Clariant

- Croda International Plc

- Dorf Ketal Chemicals

- DOVER CHEMICAL CORPORATION

- Evonik Industries AG

- Infineum International Limited

- Innospec

- King Industries, Inc.

- LANXESS

- Lubrizol

- Mayzo, Inc.

- Nouryon

- RT Vanderbilt Holding Company, Inc.

- SI Group, Inc.

- SONGWON

- Valvoline Global Operations

- Yasho Industries Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the metal deactivator market size is expected to increase from USD 1.92 billion in 2025 to USD 2.04 billion in 2026 and reach USD 2.80 billion by 2031, growing at a CAGR of 6.48% over 2026-2031.

This report is Segmented by Type (Fuel Additives, Lubricant Additives, and More), Chemistry (Nitrogen-Based Chelating Agents, Sulfur-Based Compounds, and More), Application (Gasoline, Diesel, and More), End-User Industry (Automotive and Transportation, Oil and Gas and Refining, and More) and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Metal Deactivator Market Trends and Insights

Growing Demand for Long-term Fuel and Lubricant Stability

Extended drain intervals in passenger-car and industrial oils require formulators to blend metal deactivators with high-performance antioxidants to prevent copper-catalyzed oxidation, which leads to sludge and varnish formation. Synthetic esters and polyalphaolefins are more vulnerable to transition-metal degradation than mineral bases, making passivation essential for meeting ACEA C5 and API SP standards that certify drain intervals of 10,000 miles or more. The global lubricant additives market, valued at USD 22.4 billion in 2025, supports structural demand for multifunctional packages incorporating metal deactivators to manage oxidation and corrosion. Biodiesel blends retain copper from feedstock processing; laboratory tests show that 300-500 ppm of salicylidene chelators suppress peroxide growth and extend storage life. The growth of bio-based and re-refined base oils, driven by EU Ecolabel criteria, supports the use of nitrogen chelators compatible with polar esters. OEM approvals such as Volvo VDS-5 explicitly assess metal-catalyzed oxidation, linking deactivators to the qualification process for next-generation oils.

Increase in Non-ferrous Metal Usage in Fluid Systems

Copper-nickel heat exchangers in naval vessels, aluminum radiators in electric vehicles, and brass fittings in hydraulic circuits expose fluids to catalytic surfaces that accelerate degradation unless passivated. U.S. Navy data shows copper contamination levels as high as 1,000 ppb in JP-5 fuel aboard aircraft carriers, increasing engine overhaul costs to USD 1 billion annually. Fast-charging EV cooling loops operating above 400 V experience galvanic leaching of copper into dielectric coolants, risking conductivity drift and short circuits without chelation. Peer-reviewed studies confirm that transition metals catalyze jet-fuel oxidation above 250°C, with N, N'-disalicylidene-1,2-propanediamine reducing deposit mass by 80% at trace treatment levels. Transformer oils meeting IEC 60296 standards use benzotriazole derivatives to protect copper windings from sulfide formation, which can erode dielectric strength. The increasing use of copper in renewable-energy gearboxes and solar-thermal storage systems is expanding the metal deactivator market beyond automotive and aviation applications.

Stringent Environmental Limits on Additive Chemistries

The European Chemicals Agency added benzotriazole to its PBT watchlist in 2025, initiating endocrine-disruption studies and signaling potential future concentration limits. REACH Annex XVII amendments in the same year restricted 16 CMR substances, including diphenyl(2,4,6-trimethylbenzoyl)phosphine oxide, reducing formulation options for phosphorus-based deactivators. ECHA's draft Authorization List includes melamine and phosphine-oxide compounds with sunset periods as short as 36 months, necessitating rapid reformulations. The EU Restrictions Roadmap flagged tire antioxidant 6PPD for aquatic toxicity, reflecting regulators' inclination to group additives under broad bans. Rising compliance costs for testing and labeling discourage smaller blenders, consolidating market power among global additive manufacturers with dedicated regulatory teams.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Oxidation-stability Regulations

- Rising Adoption of Aviation and Marine Fuels

- Volatile Raw-material Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fuel additives accounted for 46.71% of the metal deactivator market size in 2025 and are expected to maintain their dominance with a 6.84% CAGR through 2031. This dominance is attributed to factors such as ultra-low-sulfur diesel requirements, jet-fuel thermal stability limits, and the TOP TIER+ gasoline protocol, which incorporates metal passivation into deposit-control formulations. Lubricant additives benefit from the growing adoption of synthetic oils and the launch of hydrogen engines, which require effective copper inhibition. Polymer stabilizers, though niche, are essential for wire-and-cable insulation to address copper-contact degradation. Other smaller segments include metalworking fluids, where water-borne coolants require copper and aluminum protection to meet OEM corrosion standards.

OEMs are increasingly prioritizing multifunctional chemical packages that combine metal deactivators with detergents and antioxidants to meet certifications such as TOP TIER+ Revision G or MIL-PRF-25017. Examples include BASF's Keropur gasoline series and Afton's HiTEC 65522, which integrate nitrogen chelators with deposit inhibitors to address injector fouling and stochastic pre-ignition in GDI engines. Regulatory dosage limits, such as 2.0 mg/L initial and 5.7 mg/L cumulative in jet fuel, are driving innovation toward high-affinity nitrogen chelators that deliver efficacy at lower treat rates, sustaining advancements in the metal deactivator industry.

Nitrogen-based chelating agents held 35.27% of the metal deactivator market share in 2025 and are projected to grow at a 7.22% CAGR through 2031. Compounds like N, N'-disalicylidene-1,2-propanediamine meet ASTM D1655-22a jet-fuel standards at low concentrations of 2-5 ppm, while benzotriazole derivatives dominate transformer-oil passivation. Their compatibility with bio-esters and Environmentally Acceptable Lubricants supports demand, particularly as EU ports enforce OSPAR guidelines. Sulfur-based compounds remain relevant in heavy-duty diesel applications requiring extreme-pressure performance, but their long-term potential is limited by tightening sulfur regulations under Euro 7 and Bharat Stage VI standards. Phosphorus-based agents face significant challenges due to EU restrictions on certain phosphine oxides under CMR classifications.

Research is advancing hybrid systems that combine benzotriazole with borated dispersants, offering dual benefits of metal passivation and antioxidancy while reducing aquatoxicity. Studies from 2026 highlight nitrogen-doped nano-cerium oxide, which provides a 40-fold increase in radical-scavenging capacity, suggesting a potential future pathway where oxidation control surpasses chelation needs. The market for nitrogen-based metal deactivators is expected to expand further, supported by OEM preferences for ester-based fluids in EV drivetrains.

Geography Analysis

Asia-Pacific accounted for 44.67% of 2025 revenue and is forecast to maintain the fastest 7.22% CAGR through 2031. China's 936-million-ton-per-annum refining capacity, coupled with ASEAN's double-digit aviation growth, keeps the metal deactivator market size in the region expanding briskly. India's Bharat Stage VI diesel sulfur cap at 10 ppm strips natural antioxidants, pushing refiners to adopt metal passivation in storage and distribution. South Korea's dense fast-charging network faces copper leaching in EV cooling loops, accelerating demand for dielectric coolants with chelators. Local additive production under Make-in-India and Chinese localization programs shifts supply dynamics, giving regional formulators margin room while global majors protect OEM approvals.

North America is anchored by stringent EPA Tier 3 gasoline standards that elevate treat rates and by the Department of Defense's focus on copper contamination in JP-5 fuels. The metal deactivator market share in aviation fuels climbs as carrier groups retrofit piping and implement additive filtration to cut maintenance costs. Electric-vehicle OEMs specify copper passivation in battery thermal fluids to avert conductivity drift, adding incremental demand. Mature regulatory pathways and near-term Euro-7-type proposals in Canada create predictable but elevated compliance costs.

Europe faces the tightest regulatory squeeze. REACH scrutiny of benzotriazole and new Annex XVII CMR listings lower formulation latitude, nudging users toward alternative nitrogen chemistries. Transformer retro-fill projects in Germany and France maintain steady benzotriazole pull, but potential PBT designation threatens long-run volumes. The Netherlands' freshwater EQS of 97 µg/L for benzotriazole foreshadows wastewater-discharge permits that may spur closed-loop systems or substance substitution. Overall, European demand steadies on advanced automotive and aerospace applications even as compliance barriers rise.

Other regions contribute niche but strategic value. The Middle-East scales jet-fuel throughput in Dubai, Doha, and Riyadh, elevating passivator demand in hot-storage conditions. South America benefits from biodiesel mandates and offshore platforms employing metal-deactivator-treated drilling fluids. Africa's uptake remains moderate, centered on South African mining hydraulics and aging transformer fleets.

- ADEKA CORPORATION

- Afton Chemical

- BASF

- Bodo Moller Chemie GmbH

- Chevron Oronite Company LLC.

- Clariant

- Croda International Plc

- Dorf Ketal Chemicals

- DOVER CHEMICAL CORPORATION

- Evonik Industries AG

- Infineum International Limited

- Innospec

- King Industries, Inc.

- LANXESS

- Lubrizol

- Mayzo, Inc.

- Nouryon

- R.T. Vanderbilt Holding Company, Inc.

- SI Group, Inc.

- SONGWON

- Valvoline Global Operations

- Yasho Industries Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for long-term fuel and lubricant stability

- 4.2.2 Increase in non-ferrous metal usage in fluid systems

- 4.2.3 Stricter oxidation-stability regulations

- 4.2.4 Rising adoption of aviation and marine fuels

- 4.2.5 Surge in copper-leaching in fast-charging EV cooling loops

- 4.2.6 High-voltage transformer retro-fill programs

- 4.3 Market Restraints

- 4.3.1 Stringent environmental limits on additive chemistries

- 4.3.2 Volatile raw-material prices

- 4.3.3 Nano-cerium oxide antioxidants as substitutes

- 4.3.4 Shift to solid-state batteries curbing dielectric-fluid demand

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Fuel Additives

- 5.1.2 Lubricant Additives

- 5.1.3 Polymer Stabilizers

- 5.1.4 Other Types (Coatings, Metalworking Fluids)

- 5.2 By Chemistry

- 5.2.1 Nitrogen-based Chelating Agents

- 5.2.2 Sulfur-based Compounds

- 5.2.3 Phosphorus-based Compounds

- 5.2.4 Amine Derivatives

- 5.2.5 Other Metal Passivating Agents

- 5.3 By Application

- 5.3.1 Gasoline

- 5.3.2 Diesel

- 5.3.3 Jet Fuel

- 5.3.4 Turbine and Compressor Oils

- 5.3.5 Transformer and Insulating Oils

- 5.3.6 Polymer and Plastic Stabilizers

- 5.3.7 Other Applications (Coolants, Greases, Coatings)

- 5.4 By End-user Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Oil and Gas and Refining

- 5.4.3 Industrial Equipment and Manufacturing

- 5.4.4 Aerospace and Defense

- 5.4.5 Energy and Utilities

- 5.4.6 Marine

- 5.4.7 Other End-user Industries (Electronics, Plastics, Power)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 ADEKA CORPORATION

- 6.4.2 Afton Chemical

- 6.4.3 BASF

- 6.4.4 Bodo Moller Chemie GmbH

- 6.4.5 Chevron Oronite Company LLC.

- 6.4.6 Clariant

- 6.4.7 Croda International Plc

- 6.4.8 Dorf Ketal Chemicals

- 6.4.9 DOVER CHEMICAL CORPORATION

- 6.4.10 Evonik Industries AG

- 6.4.11 Infineum International Limited

- 6.4.12 Innospec

- 6.4.13 King Industries, Inc.

- 6.4.14 LANXESS

- 6.4.15 Lubrizol

- 6.4.16 Mayzo, Inc.

- 6.4.17 Nouryon

- 6.4.18 R.T. Vanderbilt Holding Company, Inc.

- 6.4.19 SI Group, Inc.

- 6.4.20 SONGWON

- 6.4.21 Valvoline Global Operations

- 6.4.22 Yasho Industries Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

金屬合金市場:按合金類型、形狀、製造流程和應用分類-全球預測,2026-2032年

金屬合金市場:按合金類型、形狀、製造流程和應用分類-全球預測,2026-2032年 金屬合金市場規模、佔有率和成長分析:按產品類型、合金元素、製造流程、功能、最終用途產業、分銷管道和地區分類-2026-2033年產業預測

金屬合金市場規模、佔有率和成長分析:按產品類型、合金元素、製造流程、功能、最終用途產業、分銷管道和地區分類-2026-2033年產業預測 砷金屬市場-全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、區域和競爭格局(2021-2031年)

砷金屬市場-全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、區域和競爭格局(2021-2031年) 全球金屬氧化物市場規模、佔有率、趨勢和成長分析報告(2026-2034年)戰略金屬市場:依金屬類型、產品形式及最終用途產業分類-2026-2032年全球市場預測

全球金屬氧化物市場規模、佔有率、趨勢和成長分析報告(2026-2034年)戰略金屬市場:依金屬類型、產品形式及最終用途產業分類-2026-2032年全球市場預測 金屬及金屬加工產品市場:依產品類型、金屬類型、最終用途產業及地區分類(2026-2034 年)黃金市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察與預測(2026-2034 年)

金屬及金屬加工產品市場:依產品類型、金屬類型、最終用途產業及地區分類(2026-2034 年)黃金市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察與預測(2026-2034 年) 2026年全球橡膠塗層金屬市場報告醫用金屬市場:2026-2032年全球市場預測(按產品類型、形態、製造流程、應用和最終用戶分類)金屬市場:按金屬類型、形狀、製造流程和應用分類的全球市場預測,2026-2032年

2026年全球橡膠塗層金屬市場報告醫用金屬市場:2026-2032年全球市場預測(按產品類型、形態、製造流程、應用和最終用戶分類)金屬市場:按金屬類型、形狀、製造流程和應用分類的全球市場預測,2026-2032年