|

市場調查報告書

商品編碼

2062351

滑動表面油:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Slideway Oil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

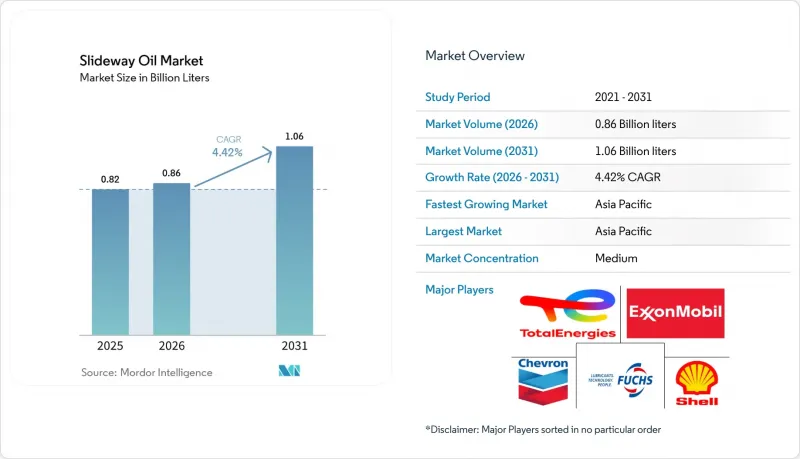

2025 年滑動表面油的市場規模估計為 8.2 億公升,預計到 2031 年將從 2026 年的 8.6 億升成長到 10.6 億公升,預測期(2026-2031 年)的複合年成長率為 4.42%。

本報告按基礎油(礦物油、合成油、生物基油)、應用領域(CNC工具工具機、水平滑台、垂直滑台等)、終端用戶產業(重型機械及金屬加工、汽車及零件等)及地區(亞太地區、北美地區、歐洲地區等)進行細分。市場預測以公升為單位。

全球滑動表面潤滑劑市場趨勢及洞察

精密加工的擴展與CNC技術的普及

預計到2024年,中國將出貨70萬台工具機,這將為未來的潤滑油需求樹立標桿,因為新型五軸加工中心需要低遷移性表面油。發那FANUC)在重慶投資12億美元的擴建計劃以及通快(Trumpf)在康涅狄格州的智慧工廠,都凸顯了北美類似的成長趨勢,反映了全球對配備封閉回路型潤滑系統且兼容自動托盤交換器的高精度機床的需求。越南和印尼緊湊型數控車床的日益普及進一步推動了其部署量和更換需求,促使供應商採用可將換油週期延長30%至40%的合成酯混合油。

新興國家金屬加工生產加速發展

印度價值1000億盧比的工具機生產以及墨西哥360億美元的近岸外包投資,正在推動對滑動表面潤滑油的需求,這種潤滑油即使在高溫高濕環境下也能保證可靠的油膜形成。同時,中國價值30.8兆元的機械產業仍依賴抗乳化配方來防止共用油箱數控工具機單元中的油箱污染。除了產品銷售外,提供油液分析服務的供應商正在獲得多年維護契約,從而擺脫現貨價格競爭的影響。

基礎油價格波動與原油價格相關

2025年第四季,美國潤滑油生產者物價指數跌至2021年以來的最低點。然而,隨後中東地區意外停產導致供應緊張,現貨價格上漲,給未進行避險交易的調配商的利潤率帶來壓力。布蘭特原油價格10%的波動將導致基礎油成本6%至8%的波動。為此,中石化決定投資興建一座年產能3萬噸的茂金屬聚環氧乙烷(PAO)裝置,以降低其高級產品供應對原油價格的依賴。

細分市場分析

截至2025年,礦物油將佔滑動表面油市場佔有率的55.89%,而合成聚環氧乙烷(PAO)和酯類混合物則用於高溫應用。生物基基礎油預計到2031年將以5.16%的複合年成長率成長,超過所有其他基礎油類別。殼牌PANOLIN和道達爾能源BIOHYDRAN等產品表明,經認證的生物分解油在其生命週期內可減少高達84%的二氧化碳排放,同時保持極壓性能。

然而,原料成本上漲以及符合 ISO VG 320 以上標準的 HEES 認證流體供不應求,阻礙了其在大型垂直滑道中的應用。環氧化大豆油和妥爾油酯產量的增加,預計在 2029 年前縮小與 II 類礦物油的價格差距。

區域分析

預計到2025年,亞太地區將佔據導軌潤滑劑市場47.57%的佔有率,並在2031年之前以5.23%的複合年成長率成長,這主要得益於中國70萬台工具機的產量以及印度不斷壯大的出口導向型機械加工叢集。北美受惠於美國2,390億美元的製造業建設投資,由於美國環保署修訂了風險管理計劃,生物基產品的應用也日益普及。歐洲雖然工具機訂單情況不一,但在監管方面處於領先地位,並正努力成為不含PFAS的創新中心。中東和非洲地區雖然規模較小,但正透過與Quaker Horton Petrolube等夥伴關係,日益關注客製化解決方案,該公司針對高溫環境客製化潤滑油配方。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 精密加工的擴展與CNC技術的普及

- 新興國家金屬加工生產加速發展

- 對工業4.0自動化工具車間的投資

- 老舊滑軌床的維修和維護需求激增。

- 更嚴格的 VOC排放法規正在推動生物基潤滑劑在滑道上的應用。

- 利用工業物聯網實現“智慧潤滑”,根據狀態對燃料供應的需求。

- 市場限制因素

- 基礎油價格波動與原油價格相關

- 與水溶性金屬加工液的化學不相容性

- 嚴格的處置法規和 REACH/EPA 合規成本

- 採用乾式/自潤滑聚合物進行直線運動

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 基礎油

- 礦物油基

- 合成油基

- 生物基

- 透過使用

- CNC工具工具機

- 水平滑道

- 垂直滑道

- 研磨機

- 車床

- 其他用途(例如,無塵室工具)

- 按最終用戶行業分類

- 金屬加工、重型設備、機械加工

- 汽車及汽車零件

- 航太/國防

- 船舶和鐵路

- 其他產業(電子、能源和電力)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Blaser Swisslube AG

- BP plc

- Chem Arrow Corporation

- Chevron Corporation

- ENEOS Corporation

- Exxon Mobil Corporation

- FUCHS

- Kluber Lubrication SE

- LUKOIL

- MotulTech(Motul SA)

- Petro-Canada Lubricants Inc.

- PETRONAS Lubricants International

- PT Idemitsu Lube Techno Indonesia

- Quaker Houghton

- Shell plc

- Sinopec Lubricants Co.

- TotalEnergies

- Valvoline Global Operations

- Yushiro Chemical Industry Co.

第7章 市場機會與未來展望

According to Mordor Intelligence, the slideway oil market size was valued at 0.82 Billion liters in 2025 and is estimated to grow from 0.86 Billion liters in 2026 to reach 1.06 Billion liters by 2031, at a CAGR of 4.42% during the forecast period (2026-2031).

This report is Segmented by Base Oil (Mineral Oil-Based, Synthetic Oil-Based, and Bio-Based), Application (CNC Machines, Horizontal Slideways, Vertical Slideways, and More), End-User Industry (Metalworking Heavy Equipment and Machining, Automotive and Auto Components, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Liters).

Global Slideway Oil Market Trends and Insights

Expanding Precision Machining and CNC Penetration

China shipped 700,000 machine-tool units in 2024, setting a benchmark for future lubricant volumes as each new five-axis center requires low-migration slideway oil. FANUC's USD 1.2 billion Chongqing expansion and TRUMPF's Connecticut smart factory highlight similar growth trends in North America, reflecting the global demand for high-accuracy beds with closed-loop lubrication systems compatible with automated pallet changers. The increasing adoption of compact CNC lathes in Vietnam and Indonesia is further expanding the installed base, boosting replacement consumption, and encouraging suppliers to introduce synthetic-ester blends that extend drain intervals by 30-40%.

Accelerating Metal-Working Output in Emerging Economies

India's INR 100 billion machine-tool production and Mexico's USD 36 billion in nearshoring inflows are driving demand for slideway oils that ensure reliable film formation in humid, high-temperature environments. At the same time, China's CNY 30.8 trillion machinery industry continues to rely on demulsifying formulations that prevent sump contamination in shared-fluid CNC cells. Suppliers offering oil-analysis services alongside product sales are securing multi-year maintenance contracts, insulating themselves from spot-price competition.

Crude-Linked Volatility in Base-Oil Prices

In the fourth quarter of 2025, the U.S. Producer Price Index for lubricants reached its lowest level since 2021. However, unplanned outages in the Middle-East subsequently tightened supply and drove up spot prices, squeezing margins for formulators without hedging programs. A 10% fluctuation in Brent crude prices translates to a 6-8% shift in base-oil costs, prompting Sinopec to invest in a 30,000 tpa metallocene PAO plant to reduce reliance on crude benchmarks for premium supply.

Other drivers and restraints analyzed in the detailed report include:

- Industry 4.0 Investments in Automated Tool Rooms

- Tightening VOC-Emission Rules Favoring Bio-Based Slideway Fluids

- Chemical Incompatibility with Water-Miscible Metalworking Fluids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mineral oil-based represented 55.89% of the slideway oil market share in 2025, with synthetic PAO and ester blends serving high-temperature applications. The bio-based segment is anticipated to grow at a CAGR of 5.16% through 2031, surpassing all other base oil categories. Products such as Shell PANOLIN and TotalEnergies BIOHYDRAN illustrate that certified biodegradable oils can maintain extreme-pressure performance while reducing CO2 life-cycle emissions by up to 84%.

Nevertheless, high feedstock costs and the limited availability of HEES-certified fluids above ISO VG 320 hinder adoption in heavy-duty vertical slideways. Expanding the production of epoxidized-soybean and tall-oil esters could help bridge the price gap with Group II mineral oils by 2029.

Geography Analysis

Asia-Pacific accounted for 47.57% of the slideway oil market share in 2025 and is projected to grow at a CAGR of 5.23% through 2031, supported by China's machine-tool production of 700,000 units and India's growing export machining clusters. North America benefits from USD 239 billion in U.S. manufacturing construction, with EPA Risk Management Plan revisions encouraging the adoption of bio-based products. Europe, while facing mixed machine-tool order volumes, leads in regulatory advancements, positioning it as a hub for PFAS-free innovations. The Middle-East and Africa, though starting from a smaller base, are attracting tailored solutions through partnerships like Quaker Houghton-Petrolube, which localizes blending for high-temperature environments.

- Blaser Swisslube AG

- BP p.l.c.

- Chem Arrow Corporation

- Chevron Corporation

- ENEOS Corporation

- Exxon Mobil Corporation

- FUCHS

- Kluber Lubrication SE

- LUKOIL

- MotulTech (Motul SA)

- Petro-Canada Lubricants Inc.

- PETRONAS Lubricants International

- PT Idemitsu Lube Techno Indonesia

- Quaker Houghton

- Shell plc

- Sinopec Lubricants Co.

- TotalEnergies

- Valvoline Global Operations

- Yushiro Chemical Industry Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding precision machining and CNC penetration

- 4.2.2 Accelerating metal-working output in emerging economies

- 4.2.3 Industry 4.0 investments in automated tool rooms

- 4.2.4 Surge in retrofit/maintenance of ageing slideway beds

- 4.2.5 Tightening VOC-emission rules favouring bio-based slideway fluids

- 4.2.6 IIoT-enabled "smart-lubrication" demand for condition-based dosing

- 4.3 Market Restraints

- 4.3.1 Crude-linked volatility in base-oil prices

- 4.3.2 Chemical incompatibility with water-miscible metal-working fluids

- 4.3.3 Stringent disposal and REACH/EPA compliance costs

- 4.3.4 Adoption of dry/self-lubricating linear-motion polymers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Base Oil

- 5.1.1 Mineral oil-based

- 5.1.2 Synthetic oil-based

- 5.1.3 Bio-based

- 5.2 By Application

- 5.2.1 CNC Machines

- 5.2.2 Horizontal Slideways

- 5.2.3 Vertical Slideways

- 5.2.4 Grinders

- 5.2.5 Lathes

- 5.2.6 Other Applications (clean-room tools, etc.)

- 5.3 By End-user Industry

- 5.3.1 Metalworking, Heavy Equipment and Machining

- 5.3.2 Automotive and Auto Components

- 5.3.3 Aerospace and Defense

- 5.3.4 Marine and Rail

- 5.3.5 Other Industries (Electronics, Energy and Power)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Blaser Swisslube AG

- 6.4.2 BP p.l.c.

- 6.4.3 Chem Arrow Corporation

- 6.4.4 Chevron Corporation

- 6.4.5 ENEOS Corporation

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 FUCHS

- 6.4.8 Kluber Lubrication SE

- 6.4.9 LUKOIL

- 6.4.10 MotulTech (Motul SA)

- 6.4.11 Petro-Canada Lubricants Inc.

- 6.4.12 PETRONAS Lubricants International

- 6.4.13 PT Idemitsu Lube Techno Indonesia

- 6.4.14 Quaker Houghton

- 6.4.15 Shell plc

- 6.4.16 Sinopec Lubricants Co.

- 6.4.17 TotalEnergies

- 6.4.18 Valvoline Global Operations

- 6.4.19 Yushiro Chemical Industry Co.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

全球工業潤滑油市場:依基礎油、產品類型、最終用途產業及地區分類-預測至2031年

全球工業潤滑油市場:依基礎油、產品類型、最終用途產業及地區分類-預測至2031年 工業潤滑油市場:2026-2030年全球市場依產品類型、基礎油、最終用戶及通路分類的預測

工業潤滑油市場:2026-2030年全球市場依產品類型、基礎油、最終用戶及通路分類的預測 工業潤滑油市場規模、佔有率、趨勢和預測:按產品類型、基礎油、最終用途行業和地區分類,2026-2034年

工業潤滑油市場規模、佔有率、趨勢和預測:按產品類型、基礎油、最終用途行業和地區分類,2026-2034年 工業潤滑脂市場:依基礎油類型、增稠劑類型、最終用途產業及地區分類

工業潤滑脂市場:依基礎油類型、增稠劑類型、最終用途產業及地區分類 工業潤滑油市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年

工業潤滑油市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年 工業潤滑油市場規模、佔有率和成長分析(按基礎油類型、產品類型、應用、最終用戶產業和地區分類)-2026-2033年產業預測

工業潤滑油市場規模、佔有率和成長分析(按基礎油類型、產品類型、應用、最終用戶產業和地區分類)-2026-2033年產業預測 工業潤滑油市場:依類型(液壓油、金屬加工油、齒輪油、壓縮機油、潤滑脂)及產業(建築與礦業、金屬生產、水泥與化工、發電、石油與天然氣)劃分-全球預測至2036年

工業潤滑油市場:依類型(液壓油、金屬加工油、齒輪油、壓縮機油、潤滑脂)及產業(建築與礦業、金屬生產、水泥與化工、發電、石油與天然氣)劃分-全球預測至2036年 工業潤滑劑市場分析及預測(至2035年):類型、產品類型、應用、技術、最終用戶、功能、形態、材質類型、設備

工業潤滑劑市場分析及預測(至2035年):類型、產品類型、應用、技術、最終用戶、功能、形態、材質類型、設備 工業潤滑油市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測,2026-2033年滑道油市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年)

工業潤滑油市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測,2026-2033年滑道油市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年)