|

市場調查報告書

商品編碼

2062349

碳鋼板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Flat Carbon Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

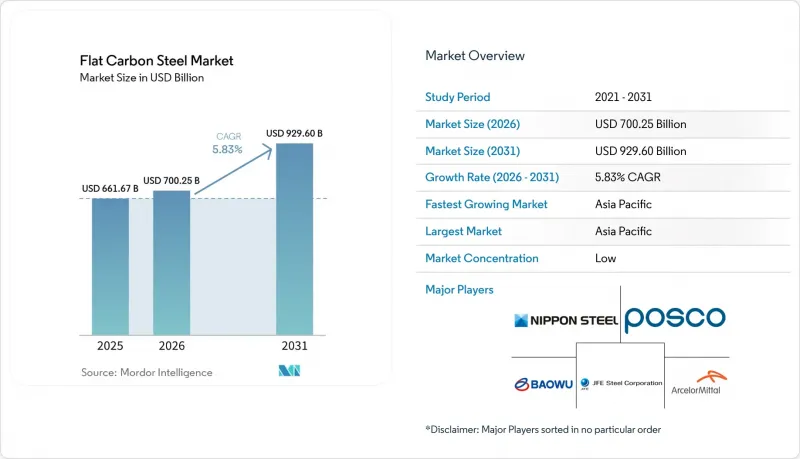

預計到 2025 年,碳鋼板市場規模將達到 6,616.7 億美元,到 2026 年將達到 7,002.5 億美元,到 2031 年將達到 9,296 億美元,2026 年至 2031 年的複合年成長率為 5.83%。

本報告按產品類型(熱軋鋼卷、冷軋鋼卷等)、厚度(超薄(小於0.8毫米))、製造方法(轉爐軋製等)、最終用途(消費電子等)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以美元計價。

全球碳鋼板市場趨勢及洞察

汽車和造船業需求增加

汽車電氣化使每輛車的鋼材用量保持在約1200公斤(其中電工鋼板最多可達100公斤),儘管產量持平,但對冷軋捲板的需求仍然強勁。在亞洲造船廠,液化天然氣(LNG)裝運船隻的訂單積壓已達三年之久,對高韌性鋼板和高級塗層的需求支撐了造船用鋼的價格。 2024年,印度白色家電新增6,500萬台,導致鍍鋅捲板出貨量增加,但由於鋼板厚度變薄,每台家電的鋼材用量下降。在中國,香港國際船舶安全環保回收公約實施後,對提高廢鋼品質的重視推高了為汽車沖壓件提供原料的電弧爐(EAF)製造商的成本。韓國的「2040 年超大差距願景」計畫正在推動對液化二氧化碳 (CO2)裝運船隻和雙燃料船舶用先進鋼板的需求。

全球基礎設施和消費性電子產品的擴張

2026年1月,美國建築開工量達到年化1.24兆美元,其中約200億美元來自三個大型企劃,將對鋼板市場產生影響。印度價值11.1億美元(1,182萬美元)的基礎建設項目預計到2034會計年度將產生2.52億噸鋼鐵產品。東協在區域全面經濟夥伴關係協定(RCEP)框架下實施的3.1兆美元發展計劃,正在促進區域內鋼捲分銷,同時降低對中國進口的依賴。 2025年,暖通空調(HVAC)設備的出貨量下降20%至770萬台,對機櫃和風管用鋼板的出貨量產生了負面影響。在中東,諸如NEOM和「2030願景」等項目正在推動重型鋼板和結構樑的消費,需求量將穩定在約5000萬噸。

鐵礦石和煉焦煤價格波動

預計到2026年,美國冶金煤出口量將增加至5,340萬短噸,將影響全球焦炭供應並推高高爐煉鋼成本。巴西礦業營運中斷和澳洲港口延誤導致鐵礦石價格顯著的月度波動,影響了鋼鐵廠的營運資金。中東地區的航運中斷推高了煉焦煤現貨價格,進一步擴大了高爐煉鋼和電弧爐煉鋼成本之間的差距。此外,高爐煉鋼企業面臨不斷上漲的碳排放稅,而電弧爐煉鋼企業則面臨廢鋼價格上漲,廢鋼價格已達到每毛噸422.50美元。柴油和電力價格上漲也增加了運輸和熔煉成本,降低了碳鋼板產業的利潤率。

細分市場分析

預計到2031年,鍍鋅鋼板和鋼捲的年均成長率將達到6.47%。 2025年,熱軋鋼捲佔碳鋼板市場的32.89%,這主要得益於結構型材、船用鋼板和汽車面板的需求。隨著亞洲造船業的復甦和印度家電行業的成長,鍍鋅產品的市場規模預計將進一步擴大。冷軋鋼捲是汽車沖壓件的重要材料,但由於越來越多更薄的替代品出現,其市場面臨替代挑戰。電鍍鋅鋼板在汽車外露面板領域保持著雖小但穩定的市場佔有率。其他塗層碳鋼板產品則受益於食品包裝和太陽能屋頂的日益普及。

隨著客戶對塗層重量認證的要求日益提高,擁有內部鍍鋅和連續退火生產線的鋼廠具有競爭優勢。中國強大的鋼板產能使得造船廠能夠提出更高的標準,這對新參與企業構成了挑戰。安賽樂米塔爾投資5億歐元(約5.855億美元)在法國建造一條電工鋼板生產線,旨在為電動車(EV)馬達提供材料,並實現矽鋼產品線的多元化發展。由於液化天然氣(LNG)儲存和低溫性能的要求,高等級造船鋼板價格居高不下。消費性電子產品製造商願意為更嚴格的厚度公差支付溢價,而配備數位雙胞胎技術的鋼廠能夠可靠地生產出符合這些要求的鋼板。

厚度小於2毫米的薄金屬捲材預計將成長6.62%,這主要得益於冷藏庫和洗衣機等設備對0.4-0.6毫米厚面板的廣泛應用,這些面板在保證剛性的前提下,能夠滿足市場需求。中等厚度的鋼板用途廣泛,可用於製造梁、汽車底盤和海上單樁等,預計到2025年,其在扁平碳鋼市場中的佔有率將達到41.92%。該市場受益於數位化榜樣,將厚度偏差降低到0.5%以下,使家電製造商(OEM)能夠在國內採購特定寬度規格的鋼板。厚度小於0.8毫米的超薄鋼帶則廣泛應用於包裝和電動車層壓板等領域。

厚度超過10毫米的厚鋼板是風力渦輪機塔筒和造船業的必需材料,但產能仍然有限,這使得獲得認證的鋼廠擁有定價權。美國公共產業項目推動了對中等厚度鋼板的需求,而多用戶住宅支撐了對薄鋼龍骨的需求。中國產能過剩導致中等厚度鋼板的利潤率承壓,但品質的提升正在擴大出口機會。數據顯示,亞洲家用電器單件鋼量正在下降,但產量增加抵消了材料成本的節省,導致鋼鐵需求持續成長。

區域分析

到2025年,亞太地區將佔全球碳鋼板市場佔有率的44.37%,預計到2031年將以6.72%的年均成長率成長。這一成長得益於印度11.1億盧比(約1182萬美元)的基礎設施項目以及東南亞國協製造業的擴張,這些因素共同支撐了對鋼捲的需求。儘管由於「1.5:1」的產能削減政策,中國的粗鋼產量已降至9.6081億噸,但中國仍是成本最低的供應國,有助於維持區域價格穩定。印度的人均鋼鐵消費量為93公斤,遠低於219公斤的全球平均水平,這顯示印度碳鋼板市場仍有巨大的成長空間。同時,在政府主導的創新基金的支持下,日本和韓國正致力於開發造船用鋼板和汽車用電工鋼板等高附加價值產品。

在北美,脫碳和製造業回流是重點領域。日本鋼鐵住友金屬公司以149億美元收購美國鋼鐵公司,其中包括一項110億美元的額外資本計劃,旨在對軋延廠進行現代化改造,並提高直接還原鐵(DRI)的產能。到2026年1月,北美地區的建築開工量將達到每年1.24兆美元,但這種成長依賴零星的大型企劃。 122條款關稅已將運轉率提高到79.1%,但這會增加下游加工商的成本。加拿大和墨西哥已從汽車組裝業務的近岸外包中受益,但仍容易受到美國政策變化的影響。

歐洲正努力應對碳排放法規和飆升的能源成本。安賽樂米塔爾的敦克爾克電弧爐和馬爾迪克的電工鋼板生產線象徵以廢鋼為原料轉型為低碳鋼生產。受離岸風力發電計畫(需要高達2,500萬噸鋼板)的推動,預計到2026年,歐盟和英國的鋼鐵需求將恢復3.2%。德國和法國正在推動電網升級,並投資電動車價值鏈。同時,由於制裁,獨立國協(獨立國協)的鋼鐵供應正轉向亞洲。南美洲的成長依賴巴西的鐵礦石出口和當地的建設活動。在中東,鋼鐵自給自足的趨勢日益明顯,阿拉伯聯合大公國鋼鐵阿爾坎公司已將產能擴大至550萬噸。沿岸地區的鋼鐵廠正利用碳邊境調節措施(CBAM)的優惠政策,準備向歐洲出口綠色優質鋼板。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 汽車和造船業需求增加

- 全球基礎設施和家用電器的發展

- 在建築業中,這是一種性價比高、強度高的等級。

- 離岸風力發電塔架的建造(採用厚板)

- OEM的第三階段目標引領「綠色扁鋼」的發展

- 利用數位雙胞胎實現產量最佳化(減少廢品)

- 市場限制因素

- 鐵礦石和焦結煤價格波動

- 嚴格的碳排放法規

- 全球產能持續過剩

- 電爐脫碳所需的高品質廢料短缺

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 熱軋鋼卷

- 冷軋捲

- 鍍鋅鋼板和鋼捲

- 電鍍鋅鋼板

- 其他塗層/處理碳鋼板

- 按厚度

- 超薄(小於0.8毫米)

- 薄片(小於2毫米)

- 中型規格(2-10毫米)

- 厚板(超過 10 毫米)

- 透過製造路線

- 鹼性氧氣轉爐(BOF)

- 電弧爐(EAF)

- 氫-DRI+EAF

- 按最終用途

- 建築和基礎設施

- 汽車和運輸業

- 家用電器

- 機械和工業設備

- 可再生能源和電力設施

- 造船/海洋

- 其他用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- AM/NS India

- ARCELORMITTAL

- BlueScope Steel Limited.

- China BaoWu Steel Group Corp. Ltd.

- Cleveland-Cliffs Inc.

- Gerdau S/A

- Hyundai Steel

- JFE Steel Corporation

- JSW

- LIBERTY Steel Group

- NIPPON STEEL CORPORATION

- Nucor Corporation

- POSCO

- SAIL

- Severstal

- SSAB AB

- Tata Steel

- Thyssenkrupp Steel Europe

- United States Steel Corporation

- voestalpine Stahl GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the flat carbon steel market size is projected to be USD 661.67 billion in 2025, USD 700.25 billion in 2026, and reach USD 929.60 billion by 2031, growing at a CAGR of 5.83% from 2026 to 2031.

This report is Segmented by Product Type (Hot Rolled Coil, Cold Rolled Coil, and More), Thickness (Ultra-Thin (Less Than 0. 8 Mm) and More), Production Route (Basic Oxygen Furnace (BOF) and More), End-Use Application (Home Appliances and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Flat Carbon Steel Market Trends and Insights

Rising Demand in Automotive and Shipbuilding

Automotive electrification maintains steel content at approximately 1,200 kilograms per vehicle, including up to 100 kilograms of electrical steel, sustaining cold-rolled coil demand despite a plateau in unit production. Asian shipyards face three-year backlogs for liquefied natural gas (LNG) carriers, requiring high-toughness plate grades and premium coatings, which support pricing for shipbuilding steel. In 2024, India added 65 million white goods, increasing galvanized coil volumes, though thinner gauges reduced per-unit steel usage. China's focus on improving scrap quality following the Hong Kong International Convention for the Safe and Environmentally Sound Recycling of Ships is raising feed costs for electric arc furnace (EAF) mills supplying automotive stampers. South Korea's Hyper-Gap Vision 2040 program is driving demand for advanced plate in liquefied carbon dioxide (CO2) carriers and dual-fuel ships.

Global Infrastructure and Appliance Build-Out

U.S. construction starts reached an annualized USD 1.24 trillion in January 2026, with nearly USD 20 billion attributed to just three megaprojects, introducing volatility to the flat carbon steel market. India's INR 1,110 million (USD 11.82 million) infrastructure pipeline supports a projected 252 million tons of finished steel demand by fiscal year (FY) 2034. The Association of Southeast Asian Nations (ASEAN)'s USD 3.1 trillion development program is boosting regional coil flows under the Regional Comprehensive Economic Partnership (RCEP) while reducing reliance on Chinese imports. Heating, ventilation, and air conditioning (HVAC) shipments declined by 20% in 2025 to 7.7 million units, negatively impacting sheet volumes for cabinets and ducts. In the Middle East, demand remains steady at approximately 50 million tons, driven by projects like NEOM and Vision 2030, which drive heavy plate and structural beam consumption.

Volatile Iron-Ore and Coking-Coal Prices

U.S. metallurgical coal exports are projected to rise to 53.4 million short tons by 2026, affecting global coke supplies and increasing furnace costs. Disruptions in Brazilian mining operations and port delays in Australia have caused significant monthly fluctuations in iron-ore prices, impacting mill working capital. Spot coking coal prices increased following shipping disruptions in the Middle East, further widening the cost difference between blast furnace (BF) and electric arc furnace (EAF) production routes. Additionally, blast furnace producers are facing increasing carbon fees, while EAF mills are dealing with scrap price increases, with busheling reaching USD 422.50 per gross ton. Higher diesel and power tariffs have also increased freight and melting costs, reducing profit margins across the Flat carbon steel industry.

Other drivers and restraints analyzed in the detailed report include:

- Offshore Wind Tower Build-Out

- OEM Scope-3 Goals Driving Green Flat Steel

- Persistent Global Over-Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Galvanized sheet and coil are projected to grow at a rate of 6.47% by 2031. Hot rolled coil accounted for 32.89% of the flat carbon steel market share in 2025, supported by demand for structural beams, ship plates, and automotive panels. The market size for galvanized products is expected to expand alongside Asia's shipbuilding recovery and India's growing appliance industry. Cold-rolled coil, while essential for automotive stampings, faces substitution challenges due to gauge-thinning alternatives. Electro-galvanized sheet maintains a small but steady niche in automotive exposed panels. Other coated flat steel products benefit from growth in food packaging and solar-roof initiatives.

Mills with in-house galvanizing and continuous annealing lines have a competitive advantage as customers prioritize certified coating weights. China's sufficient plate capacity enables shipyards to demand higher standards, creating challenges for new market entrants. ArcelorMittal has invested EUR 500 million (USD 585.5 million) in a French electrical-steel line to supply electric vehicle (EV) motors and diversify into silicon grades. Premium ship plates command higher prices due to requirements for liquefied natural gas (LNG) containment and cryogenic properties. Appliance manufacturers pay a premium for tighter thickness tolerances, which digital-twin mills can reliably produce.

Light-gauge coil under 2 millimeters (mm) is expected to grow at 6.62%, driven by the adoption of 0.4-0.6 mm panels in refrigerators and washing machines without compromising rigidity. Medium-gauge steel held a 41.92% share of the flat carbon steel market in 2025, owing to its versatility in beams, automotive chassis, and offshore monopiles. The market benefits from digital roll models that reduce gauge spreads to below 0.5%, enabling appliance original equipment manufacturers (OEMs) to source niche widths domestically. Ultra-thin strips below 0.8 mm support applications in packaging and EV laminations.

Heavy plates over 10 mm are essential for wind towers and shipbuilding but remain capacity-constrained, giving pricing power to qualified mills. U.S. utility projects are driving medium-gauge demand, while multifamily housing supports light-gauge steel for studs. Although Chinese overcapacity pressures mid-gauge margins, quality improvements are opening export opportunities. Data indicates that appliances produced in Asia require fewer kilograms of steel per unit, but rising production volumes offset material reductions, sustaining tonnage growth.

Geography Analysis

Asia-Pacific accounted for 44.37% of the flat carbon steel market in 2025 and is projected to grow at a rate of 6.72% through 2031. This growth is supported by India's INR 1,110 million (USD 11.82 million) infrastructure pipeline and the expansion of manufacturing in ASEAN countries, which sustains demand for steel coils. China's 1.5:1 capacity-swap rule reduced crude steel output to 960.81 million tonnes, yet the country remains the lowest-cost supplier, stabilizing regional prices. India's per-capita steel consumption stands at 93 kg, significantly below the global average of 219 kg, indicating substantial growth potential for the flat carbon steel market. Meanwhile, Japan and South Korea are focusing on high-value products such as ship plates and automotive electrical steel, supported by government-backed innovation funds.

North America emphasizes decarbonization and reshoring efforts. Nippon Steel's USD 14.9 billion acquisition of U.S. Steel includes an additional USD 11 billion capital plan aimed at modernizing hot-strip mills and increasing DRI capacity. Construction starts reached an annualized USD 1.24 trillion in January 2026, though growth depends on sporadic megaprojects. Section 122 tariffs have increased utilization rates to 79.1%, but they also raise costs for downstream fabricators. Canada and Mexico benefit from near-shoring vehicle assembly operations but remain vulnerable to shifts in U.S. policies.

Europe is navigating carbon regulations and high energy costs. ArcelorMittal's Dunkirk EAF and Mardyck electrical steel line highlight the transition to scrap-based, low-carbon steel production. Steel demand in the EU and UK is expected to recover by 3.2% in 2026, driven by offshore wind projects requiring up to 25 million tonnes of steel plate. Germany and France are investing in grid upgrades and electric vehicle value chains. Meanwhile, CIS steel supply is being redirected to Asia due to sanctions. South America's growth is tied to Brazilian iron ore exports and local construction activities. In the Middle East, efforts to achieve self-sufficiency are evident, with Emirates Steel Arkan increasing capacity to 5.5 million tonnes. Gulf mills are positioning themselves to export green-premium steel plates to Europe, benefiting from CBAM relief measures.

- AM/NS India

- ARCELORMITTAL

- BlueScope Steel Limited.

- China BaoWu Steel Group Corp. Ltd.

- Cleveland-Cliffs Inc.

- Gerdau S/A

- Hyundai Steel

- JFE Steel Corporation

- JSW

- LIBERTY Steel Group

- NIPPON STEEL CORPORATION

- Nucor Corporation

- POSCO

- SAIL

- Severstal

- SSAB AB

- Tata Steel

- Thyssenkrupp Steel Europe

- United States Steel Corporation

- voestalpine Stahl GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand in automotive and shipbuilding

- 4.2.2 Global infrastructure and appliance build-out

- 4.2.3 Cost-efficient high-strength grades in construction

- 4.2.4 Offshore-wind tower build-out (heavy-gauge plate)

- 4.2.5 OEM Scope-3 goals driving 'green flat steel'

- 4.2.6 Digital-twin yield optimisation (scrap-cut)

- 4.3 Market Restraints

- 4.3.1 Volatile iron-ore and coking-coal prices

- 4.3.2 Stringent carbon-emission regulations

- 4.3.3 Persistent global over-capacity

- 4.3.4 Scarce prime scrap for EAF decarbonisation

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Hot Rolled Coil

- 5.1.2 Cold Rolled Coil

- 5.1.3 Galvanized Sheet/Coil

- 5.1.4 Electro-Galvanized Sheet

- 5.1.5 Other Coated or Treated Flat Steel

- 5.2 By Thickness

- 5.2.1 Ultra-Thin (Less than 0.8 mm)

- 5.2.2 Light-Gauge (Less than 2 mm)

- 5.2.3 Medium-Gauge (2-10 mm)

- 5.2.4 Heavy-Gauge (Greater than 10 mm)

- 5.3 By Production Route

- 5.3.1 Basic Oxygen Furnace (BOF)

- 5.3.2 Electric Arc Furnace (EAF)

- 5.3.3 Hydrogen-DRI + EAF

- 5.4 By End-Use Application

- 5.4.1 Construction and Infrastructure

- 5.4.2 Automotive and Transportation

- 5.4.3 Home Appliances

- 5.4.4 Machinery and Industrial Equipment

- 5.4.5 Renewable Energy and Power Equipment

- 5.4.6 Shipbuilding and Marine

- 5.4.7 Other Applications

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Nordic Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 AM/NS India

- 6.4.2 ARCELORMITTAL

- 6.4.3 BlueScope Steel Limited.

- 6.4.4 China BaoWu Steel Group Corp. Ltd.

- 6.4.5 Cleveland-Cliffs Inc.

- 6.4.6 Gerdau S/A

- 6.4.7 Hyundai Steel

- 6.4.8 JFE Steel Corporation

- 6.4.9 JSW

- 6.4.10 LIBERTY Steel Group

- 6.4.11 NIPPON STEEL CORPORATION

- 6.4.12 Nucor Corporation

- 6.4.13 POSCO

- 6.4.14 SAIL

- 6.4.15 Severstal

- 6.4.16 SSAB AB

- 6.4.17 Tata Steel

- 6.4.18 Thyssenkrupp Steel Europe

- 6.4.19 United States Steel Corporation

- 6.4.20 voestalpine Stahl GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

鋼樑市場:依產品類型、製造類型、材料類型、最終用戶和地區分類

鋼樑市場:依產品類型、製造類型、材料類型、最終用戶和地區分類 扁平碳鋼市場:2026-2032年全球市場預測(依產品形式、產品類型、厚度、鋼種、應用及分銷通路分類)

扁平碳鋼市場:2026-2032年全球市場預測(依產品形式、產品類型、厚度、鋼種、應用及分銷通路分類) 全球碳鋼管市場規模、佔有率、趨勢和成長分析報告(2026-2034年)碳鋼市場:按類型、產品類型、製造流程和最終用途產業分類-2026-2032年全球市場預測碳鋼市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測

全球碳鋼管市場規模、佔有率、趨勢和成長分析報告(2026-2034年)碳鋼市場:按類型、產品類型、製造流程和最終用途產業分類-2026-2032年全球市場預測碳鋼市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測 碳鋼市場規模、佔有率及成長分析(依碳鋼類型、產品類型、應用、形式、最終用途及地區分類)-2026-2033年產業預測

碳鋼市場規模、佔有率及成長分析(依碳鋼類型、產品類型、應用、形式、最終用途及地區分類)-2026-2033年產業預測 碳鋼市場分析及預測(至2035年):依類型、產品、應用、形式、材料類型、製程、最終用戶、技術及安裝類型分類全球碳鋼(SC)市場規模、佔有率、趨勢和成長分析報告:2026-2034年冷鍛線材市場依產品種類、材料、直徑範圍、最終用途產業及通路分類,全球預測(2026-2032年)碳鋼分散支架市場按產品類型、材料等級、表面處理、銷售管道和最終用途產業分類,全球預測(2026-2032年)

碳鋼市場分析及預測(至2035年):依類型、產品、應用、形式、材料類型、製程、最終用戶、技術及安裝類型分類全球碳鋼(SC)市場規模、佔有率、趨勢和成長分析報告:2026-2034年冷鍛線材市場依產品種類、材料、直徑範圍、最終用途產業及通路分類,全球預測(2026-2032年)碳鋼分散支架市場按產品類型、材料等級、表面處理、銷售管道和最終用途產業分類,全球預測(2026-2032年)