|

市場調查報告書

商品編碼

2062344

雙層玻璃窗:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)Insulating Glass Window - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

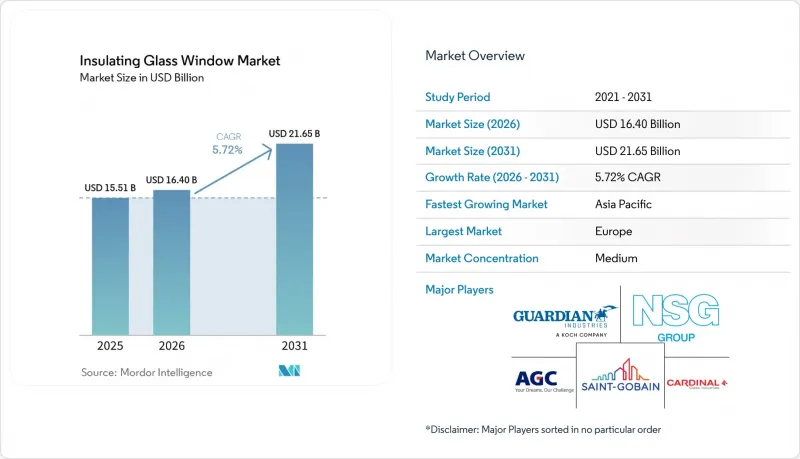

據 Mordor Intelligence 稱,2025 年雙層玻璃窗市值為 155.1 億美元,預計到 2031 年將達到 216.5 億美元,而 2026 年為 164 億美元,預測期(2026-2031 年)的複合年成長率為 5.72%。

本報告按玻璃規格(例如,雙層玻璃)、窗框材質(例如,uPVC)、應用領域(例如,住宅、商業建築)和地區(亞太地區、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元計價。

全球雙層玻璃窗市場趨勢及洞察

主要經濟區強制建築能源效率標準

加州的「Title 24-2025」和紐約市2025年能源法規將窗戶的U值限制在溫暖氣候下為0.30,寒冷氣候下為0.25,這實際上禁止了新建建築使用單層玻璃。歐盟2024年對《建築能源性能指令》(EPBD)的修訂規定,到2027年,所有新建建築都必須達到近零能耗標準。在德國、法國和北歐國家,三層玻璃的採用率已超過60%。在中國,2025年住宅建築標準要求暖氣區域的U值低於1.5 W/m²K。只有使用帶有暖邊隔條的雙層玻璃才能達到這一標準,這加速了三層玻璃的普及。這些法規的協調統一已將大多數氣候區的投資回收期縮短至五年以內,隔熱玻璃也正從一種升級選項轉變為一種標準配置。這些政策結合起來,預計將使雙層玻璃窗市場的預期複合年成長率提高 1.2 個百分點。

LEED 和 BREEAM 認證課程的綠色標籤高級認證

根據 LEED v5 認證計劃,經過第三方驗證,檢驗其環境產品聲明 (EPD) 和回收成分的玻璃系統將獲得最高 4 個「材料透明度」積分。這鼓勵使用每平方公尺二氧化碳當量低於 100 公斤 (kg CO2e/m2) 的隔熱玻璃。英國建築研究院環境評估方法 (BREEAM) 國際版 2024 要求對建築立面的整個生命週期進行碳排放評估,並推薦使用採用森林管理委員會 (FSC) 認證木材的三層中空玻璃和木框,以實現淨負碳排放。在倫敦、紐約和新加坡等城市,獲得認證的房產到 2025 年可獲得 8% 至 12% 的價格溢價,如果其 U 值低於 0.8 W/m2K,開發商每平方公尺可額外獲得 150 至 200 美元的收入。這些溢價正在推動高層綜合用途開發項目中對真空隔熱玻璃 (VIG) 和三層玻璃的需求,因為高租金證明了投資的合理性。預計在預測期的前兩年,這一趨勢將為隔熱玻璃窗市場成長貢獻約 0.8 個百分點。

與單層玻璃相比,初始成本較高

在印尼、菲律賓和撒哈拉以南非洲等地區,雙層玻璃窗的價格比單層玻璃窗高出60%至80%。在這些地區,較低的電價和超過10年的投資回收期限制了雙層玻璃窗在低價住宅中的普及。在巴西,「我的房子,我的生活」(Minha Casa Minha Vida)計畫不包括雙層玻璃窗,其使用僅限於中等收入住宅和商業建築。在沙烏地阿拉伯,開發商採用混合策略,僅在陽光照射的立面上使用雙層玻璃窗,在實現約一半節能效果的同時,還能降低30%的成本。

細分市場分析

預計到2025年,雙層玻璃窗將佔總銷售量的61.89%。在溫帶氣候地區,雙層玻璃窗是維修工程中廣泛採用的選擇。然而,隨著政策制定者收緊U值標準,其市佔率正逐漸下降。在北歐和加拿大,為了滿足被動式房屋標準(要求窗戶總U值達到0.7-0.9平方公尺/平方米·開爾文),三層玻璃窗越來越受歡迎。此外,包括四層玻璃窗和真空中空玻璃(VIG)在內的「其他」細分市場正以6.57%的複合年成長率成長。真空中空玻璃的成本有所下降,目前在商業訂單中比三層玻璃窗便宜不到20%,使其成為歷史建築和超薄幕牆的理想選擇。

製造商正在實施針對特定玻璃類型的分級氣體填充解決方案。具體而言,雙層玻璃窗使用氬氣,三層玻璃窗使用氪氣,而電壓隔熱玻璃 (VIG) 則採用真空腔,並針對厚度和重量限制進行了最佳化。厚度達 50-60 毫米、重量達每平方公尺40 公斤 (kg/m²) 的四層玻璃窗在斯堪地那維亞地區仍屬於小眾產品。儘管需求有限,但德國復興信貸銀行 (KfW) 的「40 Plus」計畫(旨在獎勵建造淨零能耗住宅)為其提供了支持。成本趨勢的變化表明市場正在走向兩極分化:一方面是面向大眾市場的維修項目,另一方面是超低能耗新建住宅,兩者分別對應著雙層玻璃窗市場中不同的玻璃類別。

區域分析

預計到2025年,歐洲將佔全球銷售額的37.21%,這主要得益於「近零能耗」法規的推動,這些法規使得新建住宅中三層玻璃窗的採用率超過60%。維修需求也十分顯著,英國和德國正興起一股用超薄三層玻璃窗替換20世紀70年代老舊窗戶的趨勢,這種新窗戶無需對窗框進行任何改造。更換窗戶可減少45%的熱量損失,並符合政府獎勵。聖戈班投資140億歐元(約163.9億美元)用於改造其在法國的生產爐並擴大在埃及的產能,從而為歐洲和北非市場提供充足的供應。雖然由於氣候溫暖,南歐的普及速度相對較慢,但在馬德里和米蘭等城市,高性能玻璃仍被用於獲得BREEAM(英國建築研究院環境評估方法)認證的辦公大樓,以確保更高的租金溢價。

亞太地區預計將以6.77%的複合年成長率成長,這主要得益於中國的維修補貼、印度120萬套住房的城市發展計劃以及越南高層公寓的蓬勃發展(福耀新工廠的投產更是推動了這一成長)。在中國的一線城市,低輻射(Low-E)塗層的三層玻璃窗已成為標配,而三線城市則更傾向於暖邊雙層玻璃窗。日本和韓國的寒冷地區為三層玻璃窗提供補貼,首爾的公寓開發商也在銷售材料中強調窗戶的U值。在東協市場,窗戶邊緣密封條在炎熱潮濕氣候下的耐久性仍然是一個挑戰,但雙層密封和乾燥劑間隔條技術正在被廣泛應用,以延長其使用壽命。

在北美,「Title 24-2025」和紐約州2025年標準加強了建築規範,將單層玻璃從可接受的規格中剔除,並加速了商業地產的升級改造。 Vitro的VacuMax工廠和福耀在伊利諾伊州的擴建增強了國內供應,減少了對亞洲進口的依賴,並減輕了關稅的影響。在墨西哥,雙層玻璃常用於晝夜溫差較大的邊境城市,而三層玻璃則更受墨西哥城高層建築的青睞,這些建築已獲得LEED(能源與環境設計先鋒獎)認證。在南美洲,玻璃的應用主要集中在巴西和阿根廷,高昂的資金籌措成本限制了其發展,儘管政府住宅計畫提供了一些支持。在中東,玻璃規格主要針對NEOM和紅海開發等大型項目,需要使用船用級密封劑和低輻射鍍膜,以承受高達50 度C的極端溫度。在撒哈拉以南非洲,成本仍然是一個重要因素,在都市區辦公大樓中,主要使用雙層玻璃窗,以平衡成本和性能。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 主要經濟區強制性建築節能標準

- LEED 和 BREEAM 認證課程的綠色標籤高級認證

- 開發中國家的都市住宅熱潮

- 淨零碳排放法規正在加速三層和四層玻璃窗的過渡。

- 真空絕熱玻璃(VIG)的大規模生產

- 超薄三層玻璃,無需更換框架即可維修。

- 市場限制因素

- 與單層玻璃相比,初始成本較高。

- 高溫高濕區域邊緣密封失效導致性能下降

- 堿灰和鋁墊片的價格波動

- 自動化IG和VIG生產線技術純熟勞工短缺

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按玻璃類型

- 雙層玻璃窗

- 三層玻璃

- 其他類型(四層玻璃、真空雙層玻璃)

- 窗框材質

- uPVC

- 鋁

- 樹

- 複合材料

- 其他材質(玻璃纖維、鋼材)

- 透過使用

- 住宅

- 商業建築

- 工業設施

- 公共機構及公共基礎設施

- 其他用途(零售、混合用途)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- AeroShield

- AGC Inc.

- ALUK

- CARDINAL GLASS INDUSTRIES, INC

- Central Glass Co.

- CSG HOLDING CO., LTD.

- Fuyao Glass Industry Group

- Glaston Corporation

- Guardian Industries

- Hartung Glass

- Internorm

- Morley Glass & Glazing Ltd.

- NSG Group/Pilkington

- PRESS GLASS Holding SA

- Saint-Gobain

- sedak GmbH & Co. KG

- Sisecam Group

- Viracon

- Vitro Architectural Glass

- Xinyi Glass Holdings Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the insulating glass window market size was valued at USD 15.51 billion in 2025 and is estimated to grow from USD 16.40 billion in 2026 to reach USD 21.65 billion by 2031, at a CAGR of 5.72% during the forecast period (2026-2031).

This report is Segmented by Glazing Type (Double Glazing and More), Window Frame Material (uPVC and More), Application (Residential, Commercial Buildings, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Insulating Glass Window Market Trends and Insights

Mandatory Building-Energy Codes in Major Economies

California's Title 24-2025 and the 2025 New York City Energy Conservation Code now limit whole-window U-values to 0.30 in warm zones and 0.25 in colder zones, effectively removing single glazing from new construction. The European Union's 2024 Energy Performance of Buildings Directive (EPBD) revision mandates near-zero-energy standards for all new buildings by 2027, increasing triple-glazing adoption to over 60% in Germany, France, and Nordic countries. In China, the 2025 residential code requires U-values of 1.5 W/m2K or lower in heating zones, a threshold achievable by double glazing only with warm-edge spacers, accelerating the adoption of triple-glazed units. These converging regulations reduce payback periods to under five years in most climates, transitioning insulating glass from an upgrade to a standard specification. Collectively, these policies are projected to add 1.2 percentage points to the forecasted compound annual growth rate (CAGR) of the insulating glass window market.

Green-Label Premiums from LEED and BREEAM Certified Projects

Leadership in Energy and Environmental Design (LEED) v5 awards up to four material transparency points for glazing systems with third-party environmental product declarations and recycled-content verification, encouraging the use of insulating glass with embodied-carbon footprints below 100 kilograms of carbon dioxide equivalent per square meter (kg CO2e/m2). Building Research Establishment Environmental Assessment Method (BREEAM) International 2024 requires whole-life carbon assessments for facades, favoring timber-framed triple glazing that achieves net-negative embodied carbon when Forest Stewardship Council (FSC)-certified timber is used. Certified properties in cities like London, New York, and Singapore commanded 8-12% price premiums in 2025, translating to additional developer revenue of USD 150-200/m2 when U-values below 0.8 W/m2K are documented. These premiums drive demand for vacuum-insulated glass (VIG) and triple-glazed units in high-rise mixed-use developments, where higher rents justify the investment. This trend is expected to contribute approximately 0.8 percentage points to the insulating glass window market growth over the initial two forecast years.

Higher Upfront Cost Versus Single Glazing

Insulating glass has a price premium of 60-80% compared to single glazing in regions such as Indonesia, the Philippines, and sub-Saharan Africa. In these areas, low power tariffs and a payback period exceeding a decade limit its use in entry-level housing. In Brazil, the Minha Casa Minha Vida (My House My Life) program excludes insulating glass, restricting its adoption to mid-income housing and commercial buildings. In Saudi Arabia, developers adopt a mixed approach, using insulating glass only on solar-exposed facades to achieve approximately half the energy savings at 30% lower costs.

Other drivers and restraints analyzed in the detailed report include:

- Urban Housing Booms in Developing Countries

- Net-Zero-Carbon Mandates Accelerating Triple and Quad Glazing

- Edge-Seal Failures Causing Performance Loss in Hot-Humid Zones

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The insulating glass window market size for double glazing accounts for 61.89% of total revenue in 2025. Double glazing is a widely used option for retrofits in temperate climates. However, its market share is gradually declining as policymakers implement stricter U-value limits. Triple glazing is gaining adoption in northern Europe and Canada, where whole-window U-values of 0.7-0.9 watts per square meter kelvin (W/m2K) meet passive-house standards. Additionally, the "other types" segment, which includes quadruple and vacuum insulating glass (VIG), is expanding at a compound annual growth rate (CAGR) of 6.57%. The decreasing costs of VIG, now within 20% of triple glazing for commercial orders, make it a viable choice for heritage sites and slender curtain walls.

Manufacturers are introducing tiered gas-fill solutions tailored to specific glazing types: argon for double glazing, krypton for triple glazing, and vacuum chambers for VIG, optimized to address thickness and weight constraints. Quadruple glazing remains a niche product in Scandinavia due to its 50-60 millimeter thickness and 40 kilograms per square meter (kg/m2) weight. Despite limited demand, it is supported by KfW 40 Plus incentives for net-zero homes. The evolving cost dynamics suggest a bifurcation in the market, with mass-market retrofits on one side and ultra-low-energy new builds on the other, each served by distinct glazing categories within the insulating glass window market.

Geography Analysis

Europe accounted for 37.21% of the projected 2025 revenue, driven by near-zero-energy mandates that have increased triple-glazing penetration to over 60% in new housing. Retrofit demand is also significant, with ultra-thin triple-glazed units replacing 1970s-era windows in the United Kingdom and Germany without requiring frame modifications. This reduces heat loss by 45% and qualifies for government incentives. Saint-Gobain's EUR 14 billion (USD 16.39 billion) investment to convert furnaces in France and expand capacity in Egypt supports supply for both European and North African markets. Southern Europe shows slower adoption due to milder climates, but Building Research Establishment Environmental Assessment Method (BREEAM)-certified offices in cities like Madrid and Milan continue to specify high-performance glazing to secure rental premiums.

The Asia-Pacific region is expected to grow at a 6.77% compound annual growth rate (CAGR), supported by China's retrofit subsidies, India's 1.2 million-unit metro development pipeline, and Vietnam's high-rise condominium boom, which is bolstered by Fuyao's new manufacturing plant. In tier-1 Chinese cities, triple-glazed units with Low-Emissivity (Low-E) coatings are standard, while tier-3 cities opt for warm-edge double glazing. Japan and South Korea provide subsidies for triple glazing in colder regions, with Seoul's condominium developers highlighting window U-values in sales materials. Association of Southeast Asian Nations (ASEAN) markets face challenges with edge-seal durability in hot and humid climates, but are adopting dual-seal and desiccant spacer technologies to improve service life.

North America has tightened building codes with Title 24-2025 and New York's 2025 standards, which eliminate single glazing from permissible specifications and drive upgrades in commercial real estate. Domestic supply is bolstered by Vitro's VacuMax plant and Fuyao's Illinois expansion, reducing reliance on Asian imports and mitigating tariff impacts. In Mexico, double glazing is commonly installed in border cities with significant diurnal temperature variations, while Leadership in Energy and Environmental Design (LEED)-certified towers in Mexico City prefer triple-glazed units. South America's adoption is concentrated in Brazil and Argentina, where high financing costs limit growth, though governmental housing programs provide some support. The Middle East focuses on glazing specifications for large-scale projects like NEOM and the Red Sea developments, which require marine-grade seals and Low-E coatings to withstand extreme temperatures of up to 50°C. In Sub-Saharan Africa, cost considerations remain a key factor, with urban office towers primarily using double glazing to balance cost and performance.

- AeroShield

- AGC Inc.

- ALUK

- CARDINAL GLASS INDUSTRIES, INC

- Central Glass Co.

- CSG HOLDING CO., LTD.

- Fuyao Glass Industry Group

- Glaston Corporation

- Guardian Industries

- Hartung Glass

- Internorm

- Morley Glass & Glazing Ltd.

- NSG Group/Pilkington

- PRESS GLASS Holding SA

- Saint-Gobain

- sedak GmbH & Co. KG

- Sisecam Group

- Viracon

- Vitro Architectural Glass

- Xinyi Glass Holdings Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory building-energy codes in major economies

- 4.2.2 Green-label premiums from LEED and BREEAM certified projects

- 4.2.3 Urban housing booms in developing countries

- 4.2.4 Net-zero-carbon mandates accelerating triple and quad glazing

- 4.2.5 Mass-production scale-up of vacuum insulated glass (VIG)

- 4.2.6 Ultra-thin glass triples enabling retrofits without frame changes

- 4.3 Market Restraints

- 4.3.1 Higher upfront cost versus single glazing

- 4.3.2 Edge-seal failures causing performance loss in hot-humid zones

- 4.3.3 Volatile soda-ash and aluminium-spacer prices

- 4.3.4 Skilled-labour shortages for automated IG and VIG lines

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Glazing Type

- 5.1.1 Double Glazing

- 5.1.2 Triple Glazing

- 5.1.3 Other Types (Quadruple, Vacuum IG)

- 5.2 By Window Frame Material

- 5.2.1 uPVC

- 5.2.2 Aluminium

- 5.2.3 Wood

- 5.2.4 Composite

- 5.2.5 Other Materials (Fibreglass, Steel)

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial Buildings

- 5.3.3 Industrial Facilities

- 5.3.4 Institutional and Public Infrastructure

- 5.3.5 Other Applications (Retail, Mixed-Use)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Nordic Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 AeroShield

- 6.4.2 AGC Inc.

- 6.4.3 ALUK

- 6.4.4 CARDINAL GLASS INDUSTRIES, INC

- 6.4.5 Central Glass Co.

- 6.4.6 CSG HOLDING CO., LTD.

- 6.4.7 Fuyao Glass Industry Group

- 6.4.8 Glaston Corporation

- 6.4.9 Guardian Industries

- 6.4.10 Hartung Glass

- 6.4.11 Internorm

- 6.4.12 Morley Glass & Glazing Ltd.

- 6.4.13 NSG Group/Pilkington

- 6.4.14 PRESS GLASS Holding SA

- 6.4.15 Saint-Gobain

- 6.4.16 sedak GmbH & Co. KG

- 6.4.17 Sisecam Group

- 6.4.18 Viracon

- 6.4.19 Vitro Architectural Glass

- 6.4.20 Xinyi Glass Holdings Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

雙層玻璃窗市場-2026-2032年全球市場預測

雙層玻璃窗市場-2026-2032年全球市場預測 隔熱玻璃窗市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、玻璃類型、間隔條類型、地區和競爭對手分類,2021-2031年

隔熱玻璃窗市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、玻璃類型、間隔條類型、地區和競爭對手分類,2021-2031年 2026年全球雙層玻璃窗市場報告玻璃絕緣子市場:2026-2032年全球市場預測(依產品類型、電壓等級、應用、終端用戶產業及通路分類)中空玻璃市場:依產品類型、玻璃類型、技術、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測按電壓等級、每串絕緣子數量、配銷通路和最終用途分類的盤式懸式玻璃絕緣子市場-全球預測,2026-2032年

2026年全球雙層玻璃窗市場報告玻璃絕緣子市場:2026-2032年全球市場預測(依產品類型、電壓等級、應用、終端用戶產業及通路分類)中空玻璃市場:依產品類型、玻璃類型、技術、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測按電壓等級、每串絕緣子數量、配銷通路和最終用途分類的盤式懸式玻璃絕緣子市場-全球預測,2026-2032年 全球真空絕熱玻璃市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球真空絕熱玻璃市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026-2030年全球隔熱玻璃窗市場全球中空玻璃市場:市場規模、份額、成長率、產業分析、按類型、應用和地區劃分的分析以及未來預測(2026-2034)

2026-2030年全球隔熱玻璃窗市場全球中空玻璃市場:市場規模、份額、成長率、產業分析、按類型、應用和地區劃分的分析以及未來預測(2026-2034) 隔熱玻璃窗市場規模、佔有率和趨勢分析報告:按產品類型、最終用途、地區和細分市場預測(2025-2033 年)

隔熱玻璃窗市場規模、佔有率和趨勢分析報告:按產品類型、最終用途、地區和細分市場預測(2025-2033 年)