|

市場調查報告書

商品編碼

2062341

異戊二烯橡膠乳膠:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)Isoprene Rubber Latex - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

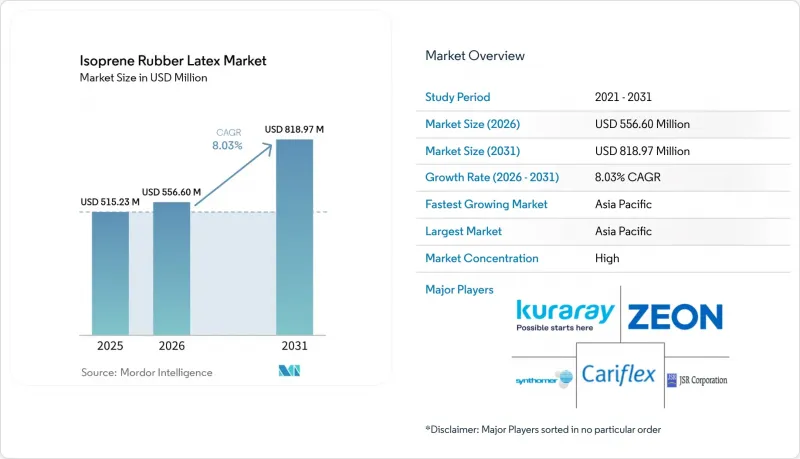

2025 年異戊二烯橡膠乳膠市場價值為 5.1523 億美元,預計到 2031 年將達到 8.1897 億美元,而 2026 年為 5.566 億美元,預測期(2026-2031 年)複合年成長率為 8.03%。

本報告按等級(醫用、工業、食品、高氨)、形態(高固態和低固態/預硫化)、應用(醫用手套、導管、保險套、黏合劑、紡織品、其他)、最終用戶(醫療保健、個人護理、工業、消費品、其他)和地區(亞太、歐洲、北美、其他)進行細分。市場預測以美元計價。

全球異戊二烯橡膠乳膠市場趨勢與洞察

無粉醫用手套的需求量激增。

2017年,美國禁止使用含粉實驗室手套,特別是以玉米粉為載體的產品,因為玉米澱粉已知會傳播乳膠過敏原。這項監管變化迫使醫院轉向使用低過敏性合成替代品。預計到2026年至2031年,馬來西亞將成為外科手套的主要出口國,從而推動對異戊二烯乳膠的需求。中國製造商英科醫療(Intco Medical)透過擴大產能和最佳化人事費用,進一步加劇了市場競爭。蛋白質含量低於50微克/克的低蛋白異戊二烯乳膠因其能夠減輕I型超敏反應而備受青睞,在醫院採購中佔據主導地位。受此趨勢影響,強制使用無粉手套的規定正在擴展到工業領域和餐飲服務業,進一步提升了異戊二烯橡膠乳膠的市場潛力。

出於對過敏問題的考慮,尋找天然橡膠乳膠的替代品

天然乳膠過敏影響相當一部分醫護人員,職業安全與健康機構已將其列為職場危害。歐洲藥典3.2.9禁止在藥品初級包裝中使用天然橡膠乳膠,使得合成異戊二烯瓶蓋備受關注。雖然有報告指出瓜尤爾橡膠和生物基異戊二烯引起的過敏較少,但仍需進行大規模的檢驗。北美和歐洲的醫院正在使用丁腈橡膠或合成異戊二烯手套,丁腈橡膠手套的銷售持續成長。合成異戊二烯手套由於其順式-1,4-聚異戊二烯骨架與天然橡膠相同,因此具有與天然橡膠相似的彈性。此外,由於不含作物來源的蛋白質,確保了批次間的一致性,適用於II/III類醫療設備。

天然橡膠(NRL)生產成本高

在2026年至2031年的預測期內,合成異戊二烯乳膠的價格預計將優於天然乳膠的價格。這是因為聚合物級單體的交易價格高於粗製C4/C5原料的價格。儘管天然橡膠價格保持穩定,但異戊二烯單體市場仍在穩步成長。對價格敏感的行業,例如家用手套和工業浸漬產品,仍然依賴天然乳膠。相較之下,醫療和食品級應用的價格更高,這得益於其低致敏性。

細分市場分析

2025年,符合FDA 21 CFR 880手套標準及USP 381封口標準的醫用級乳膠佔總銷售額的41.94%。受避孕套製造商推動,食品級異戊二烯橡膠乳膠市場預計將在2026年至2031年間以8.52%的複合年成長率成長,這些製造商的目標是生產符合FDA 21 CFR 177.2600標準的配方。工業乳膠用於黏合劑和密封劑,其中液態聚異戊二烯乳膠可用作增粘劑。高氨乳膠因其較長的保存期限而備受關注,但其是否符合歐盟VOC法規正受到嚴格審查,儘管行業正在顯著轉向使用低氨穩定劑。蛋白質濃度低於50 µg/g的超低蛋白乳膠專為III級外科手套和專用醫療設備而設計。

醫用乳膠價格依然堅挺,這得益於基於 ISO 13485 標準的可追溯性以及醫院對天然乳膠過敏原更為嚴格的規定。食品級乳膠廣泛用於安撫奶嘴、奶瓶奶嘴和低過敏性保險套,推動了需求的穩定成長。工業領域也呈現成長態勢,尤其是在電動車製造商為了減輕車重而從傳統機械緊固件轉向彈性體黏合劑的情況下。

至2025年,固態含量超過50%的高固態乳膠將佔銷售額的63.91%。高固態含量不僅有助於降低運輸成本,還有助於提高機械穩定性。同時,低固態預硫化乳膠在異戊二烯橡膠領域的市佔率在2026年至2031年間將以8.63%的複合年成長率成長。這一成長主要歸功於輻射硫化和過氧化物硫化工藝,這些工藝生產的乳膠拉伸強度已超過ASTM D3577外科手套標準。此外,室溫預硫化技術的進步使得生產薄壁導管膜成為可能,無需使用後硫化爐。

儘管高固態產品仍佔據主導地位,但對無硫預硫化產品的需求正在成長。其吸引力在於降低了亞硝胺風險並縮短了生產週期。亞太地區(馬來西亞和泰國)的手套製造地也在不斷發展,引入了結合輻射交聯和過氧化物硫化的混合生產模式。在物流方面,供應鏈參與者,特別是那些能夠在2-8°C的嚴格低溫運輸條件下運輸穩定低固態乳膠的企業,將在2026年至2031年的預測期內,在獲取專業醫療訂單方面擁有戰略優勢。

區域分析

亞太地區在2025年佔全球銷售額的53.37%,預計將進一步鞏固其市場主導地位,在2026年至2031年的預測期內,複合年成長率將達到8.99%。馬來西亞在外科手套出口方面發揮了重要作用。除手套出口外,中國也正在擴大合成橡膠產能。為因應影響中國產手套的關稅變化,泰國和越南也在擴大生產。 2026年2月,阿朗新科在常州推出了一家氫化丁腈橡膠(HNBR)生產廠,而ZEON位於米澤的工廠計劃在2034年實現生物異戊二烯的商業化。此外,印度和印尼中產階級的崛起正在推動醫療保健支出的成長,凸顯了該地區的成長潛力。

預計北美和歐洲將在2025年佔據相當大的銷售佔有率。美國食品藥物管理局(FDA)將於2026年推出的品管系統法規(QMSR),以及各州對鄰苯二甲酸酯使用的禁令,正在推動導管和塞子產業的改革,從而促進合成異戊二烯的應用。同時,歐洲蒸汽裂解裝置的運作限制了當地的原料供應,迫使該地區依賴進口,導致乳膠價格飆升。在北美,疫苗塞子的需求依然強勁,這主要得益於mRNA製劑填充和包裝生產線的擴張。

即使將南美、中東和非洲這三個地區的銷售額加總,它們在2025年的總銷售額中所佔佔有率仍然很小。預硫化乳膠需要在2°C至8°C的溫度下儲存,但由於低溫運輸不足,其分銷面臨挑戰。阿朗新歐計劃在2027年前完成其位於特里溫福的工廠擴建,以加強在拉丁美洲的本地供應。同時,中東雖然擁有豐富的石化原料,但下游乳膠產能有限,為手套和導管產業的投資者創造了極具吸引力的合資機會。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 無粉醫用手套的需求量激增。

- 由於過敏問題,天然橡膠乳膠(NRL)是一種替代品。

- 微創導管和球囊療法的擴展

- 有關不含DEHP的醫療設備的法規對IRL導管球囊有利。

- mRNA疫苗管瓶在實際應用上需要極高的潔淨度。

- 用於微流體晶片的彈性體層需要超高純度IRL

- 市場限制因素

- 高生產成本與NRL相比

- 異戊二烯單體原料價格波動

- 蒸汽裂解裝置的運作限制了聚合物用異戊二烯的供應。

- 新興市場低溫運輸物流面臨的限制因素

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按年級

- 醫用級

- 工業級

- 食品級

- 高氨氣紅外光譜

- 按形式

- 個人護理和衛生用品

- 低固態含量/預硫化乳膠

- 透過使用

- 醫用手套

- 導管和球囊裝置

- 保險套

- 黏合劑和密封劑

- 彈性紗線和纖維

- 其他用途(塗層、嬰兒用品)

- 按最終用戶行業分類

- 醫療保健

- 個人護理和衛生用品

- 工業製造

- 消費品

- 其他行業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- ARLANXEO

- Cariflex

- Daelim Co., Ltd.

- Eni SpA

- Exxon Mobil Corporation

- Fushun Yikesi New Materials Co., Ltd.

- JSR Corporation

- Kent Elastomers Products, Inc.

- Kraton Corporation

- Kumho Petrochemical

- Kuraray Co., Ltd.

- LG Chem

- Lion Elastomers

- PetroChina Yanshan Petrochemical

- PJSC SIBUR Holding

- Shandong Yuhuang Chemical Co., Ltd.

- Sumitomo Rubber Industries

- Synthomer plc

- Top Glove Corporation Bhd

- Zeon Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the isoprene rubber latex market size was valued at USD 515.23 million in 2025 and is estimated to grow from USD 556.60 million in 2026 to reach USD 818.97 million by 2031, at a CAGR of 8.03% during the forecast period (2026-2031).

This report is Segmented by Grade (Medical, Industrial, Food, and High-Ammonia), Form (High-Solids and Low-Solids/Prevulcanized), Application (Medical Gloves, Catheters, Condoms, Adhesives, Textiles, and Others), End-User (Healthcare, Personal Care, Industrial, Consumer Goods, and Others), and Geography (Asia-Pacific, Europe, North America, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Isoprene Rubber Latex Market Trends and Insights

Surging Demand for Powder-Free Medical Gloves

In 2017, the U.S. imposed a ban on powdered examination gloves, specifically targeting cornstarch carriers known to disseminate latex allergens. This regulatory shift prompted hospitals to pivot towards hypoallergenic synthetic alternatives. By the forecast period 2026-2031, Malaysia has emerged as a key exporter of surgical gloves, bolstering the demand for isoprene latex. Chinese manufacturer Intco Medical has increased its production capacity and streamlined labor costs, heightening the competitive landscape. Low-protein isoprene grades, containing less than 50 micrograms per gram, are now favored for their ability to reduce type I hypersensitivity, securing a premium position in hospital purchases. Reflecting this trend, mandates for powder-free gloves have expanded to encompass industrial and food-service sectors, amplifying the market potential for isoprene rubber latex.

Substitution of Natural Rubber Latex Amid Allergy Concerns

Natural-latex allergies affect a significant portion of healthcare workers, prompting occupational safety organizations to classify them as a workplace hazard. The European Pharmacopeia 3.2.9 has banned natural rubber latex in pharmaceutical primary packaging, shifting the focus to synthetic isoprene closures. Although guayule rubber and bio-based isoprene report fewer allergy incidents, they still await large-scale validation. Hospitals across North America and Europe have adopted nitrile or synthetic isoprene gloves, with nitrile glove revenues continuing to grow. Due to their identical cis-1,4 polyisoprene backbones, synthetic grades replicate the elasticity of natural rubber. Furthermore, being free from crop-derived proteins, they ensure consistent batches suitable for Class II/III devices.

High Production Cost Versus NRL

By the forecast period 2026-2031, synthetic isoprene latex prices outpace those of natural latex, fueled by the premium trading of polymer-grade monomers over crude C4/C5 streams. While natural rubber prices remain stable, the isoprene monomer market continues to grow steadily. Price-sensitive sectors, including household gloves and industrial dipped goods, still rely on natural latex. In contrast, medical and food-grade segments, benefiting from their hypoallergenic compliance, command premium prices.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Minimally Invasive Catheter and Balloon Procedures

- DEHP-Free Device Regulation Favors IRL Catheter Balloons

- Volatile Isoprene-Monomer Feedstock Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, medical-grade latex, adhering to FDA 21 CFR 880 standards for gloves and USP 381 standards for closures, commanded 41.94% of the revenue. The market for food-grade isoprene rubber latex, driven by condom manufacturers targeting FDA 21 CFR 177.2600 compliant formulations, is set to expand at a CAGR of 8.52% from 2026 to 2031. Industrial-grade latex finds its application in adhesives and sealants, with liquid polyisoprene grades acting as tackifiers. While high-ammonia grades, known for enhancing shelf life, face scrutiny for EU VOC compliance, there is a noticeable industry shift towards low-ammonia stabilizers. Ultra-low-protein latex, with concentrations below 50 µg/g, is tailored for Class III surgical gloves and specialized medical devices.

Pricing for medical-grade latex remains strong, supported by ISO 13485 traceability and tightening hospital regulations on natural-latex allergens. Food-grade latex is commonly used in pacifiers, baby-bottle nipples, and hypoallergenic condoms, which drives a consistent volume increase. The industrial-grade segment is witnessing growth, especially as electric-vehicle manufacturers lean towards elastomeric bonding, moving away from traditional mechanical fasteners for weight reduction.

In 2025, high-solids latex, boasting over 50% solids content, commanded 63.91% of the revenue. This high-solids content not only reduced freight costs but also enhanced mechanical stability. Meanwhile, the market share of low-solids prevulcanized latex in the isoprene rubber sector is growing at 8.63% CAGR, from 2026 to 2031. This growth is attributed to radiation-peroxide vulcanization, which has achieved tensile strengths exceeding the ASTM D3577 standard, a benchmark for surgical gloves. Additionally, advancements in room-temperature pre-vulcanization have enabled the production of thin-wall catheter films, eliminating the need for post-cure ovens.

Although high-solids variants continue to dominate, sulfur-free prevulcanized grades are gaining traction. Their appeal lies in a reduced nitrosamine risk and faster production cycles. Glove manufacturing hubs in the Asia-Pacific (Malaysia and Thailand) region are also evolving. They have started integrating hybrid manufacturing models, combining radiation crosslinking with peroxide curing. On the logistics front, players in the supply chain, particularly those proficient in shipping stabilized low-solids latex under stringent cold-chain conditions of 2 to 8 °C, are strategically positioned to capture specialized medical orders during the forecast period of 2026-2031.

Geography Analysis

Asia-Pacific, which accounted for 53.37% of the revenue in 2025, is set to reinforce its lead with a projected 8.99% CAGR during the forecast period of 2026-2031. Malaysia has played a significant role in exporting surgical gloves. China, in addition to exporting gloves, is expanding its synthetic-rubber capacity. Both Thailand and Vietnam are increasing production in response to tariff changes affecting Chinese gloves. In February 2026, ARLANXEO launched an HNBR unit in Changzhou, while Zeon's Yonezawa facility is targeting bio-isoprene commercialization by 2034. Additionally, a rising middle class in India and Indonesia is driving increased healthcare spending, highlighting the region's growth potential.

North America and Europe are set to capture a substantial share of 2025's sales. The FDA's QMSR, introduced in 2026, along with state-level bans on phthalates, is driving reforms in catheters and stoppers, leading to increased adoption of synthetic isoprene. At the same time, European steam-cracker shutdowns are limiting local feedstock availability, pushing the region towards imports and driving up latex prices. In North America, the demand for vaccine stoppers remains strong, particularly with the expansion of mRNA fill-finish lines.

South America, the Middle-East, and Africa together make up a smaller portion of the 2025 revenue. The distribution of pre-vulcanized latex, which requires storage between 2°C and 8°C, faces challenges due to cold-chain deficiencies. ARLANXEO aims to complete its Triunfo expansion by 2027 to bolster local supply in Latin America. Meanwhile, the Middle-East's abundant petrochemical feedstock contrasts with its limited downstream latex production capacity, presenting attractive joint-venture opportunities for investors in gloves and catheters.

- ARLANXEO

- Cariflex

- Daelim Co., Ltd.

- Eni S.p.A

- Exxon Mobil Corporation

- Fushun Yikesi New Materials Co., Ltd.

- JSR Corporation

- Kent Elastomers Products, Inc.

- Kraton Corporation

- Kumho Petrochemical

- Kuraray Co., Ltd.

- LG Chem

- Lion Elastomers

- PetroChina Yanshan Petrochemical

- PJSC SIBUR Holding

- Shandong Yuhuang Chemical Co., Ltd.

- Sumitomo Rubber Industries

- Synthomer plc

- Top Glove Corporation Bhd

- Zeon Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for powder-free medical gloves

- 4.2.2 Substitution of natural rubber latex (NRL) amid allergy concerns

- 4.2.3 Growth in minimally-invasive catheter and balloon procedures

- 4.2.4 DEHP-free device regulation favouring IRL catheter balloons

- 4.2.5 Ultra-clean IRL required for mRNA-vaccine vial stoppers

- 4.2.6 Microfluidic-chip elastomer layers needing ultra-pure IRL

- 4.3 Market Restraints

- 4.3.1 High production cost versus NRL

- 4.3.2 Volatile isoprene-monomer feedstock pricing

- 4.3.3 Steam-cracker outages limiting polymer-grade isoprene

- 4.3.4 Cold-chain logistics limitations in emerging markets

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Grade

- 5.1.1 Medical Grade

- 5.1.2 Industrial Grade

- 5.1.3 Food Grade

- 5.1.4 High-Ammonia IRL

- 5.2 By Form

- 5.2.1 Personal Care and Hygiene

- 5.2.2 Low-Solids/Prevulcanized Latex

- 5.3 By Application

- 5.3.1 Medical Gloves

- 5.3.2 Catheters and Balloon Devices

- 5.3.3 Condoms

- 5.3.4 Adhesives and Sealants

- 5.3.5 Elastic Threads and Textiles

- 5.3.6 Other Applications (Coatings, Baby Products)

- 5.4 By End-user Industry

- 5.4.1 Healthcare and Medical

- 5.4.2 Personal Care and Hygiene

- 5.4.3 Industrial Manufacturing

- 5.4.4 Consumer Goods

- 5.4.5 Other Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 North America

- 5.5.3.1 United States

- 5.5.3.2 Canada

- 5.5.3.3 Mexico

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 ARLANXEO

- 6.4.2 Cariflex

- 6.4.3 Daelim Co., Ltd.

- 6.4.4 Eni S.p.A

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 Fushun Yikesi New Materials Co., Ltd.

- 6.4.7 JSR Corporation

- 6.4.8 Kent Elastomers Products, Inc.

- 6.4.9 Kraton Corporation

- 6.4.10 Kumho Petrochemical

- 6.4.11 Kuraray Co., Ltd.

- 6.4.12 LG Chem

- 6.4.13 Lion Elastomers

- 6.4.14 PetroChina Yanshan Petrochemical

- 6.4.15 PJSC SIBUR Holding

- 6.4.16 Shandong Yuhuang Chemical Co., Ltd.

- 6.4.17 Sumitomo Rubber Industries

- 6.4.18 Synthomer plc

- 6.4.19 Top Glove Corporation Bhd

- 6.4.20 Zeon Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Bio-based Isoprene Latex