|

市場調查報告書

商品編碼

2062340

低熔點纖維:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Low Melting Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

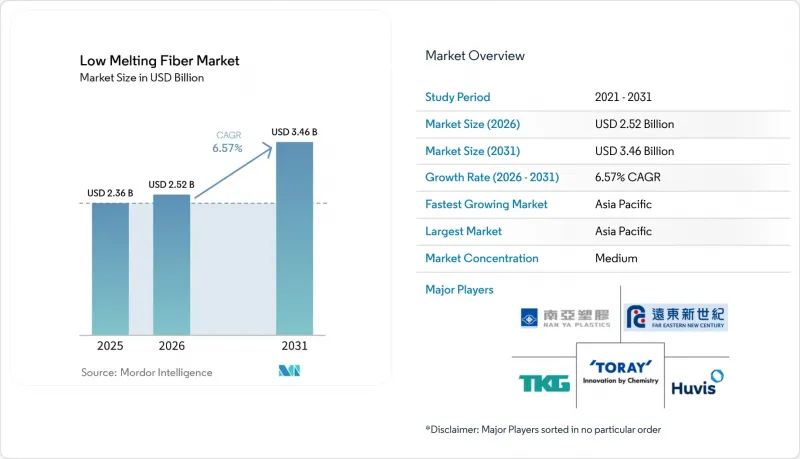

預計低熔點纖維市場將從 2025 年的 23.6 億美元成長到 2026 年的 25.2 億美元,到 2031 年將達到 34.6 億美元,2026 年至 2031 年的複合年成長率為 6.57%。

本報告按熔點(低於和高於 130 度C)、結構類型(芯鞘套、並排式、島式)、終端用戶行業(紡織和不織布、汽車和交通運輸、家具和床上用品等)以及地區(亞太地區、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元計價。

全球低熔點纖維市場趨勢及洞察

對環保型和永續熱黏合纖維的需求日益成長

各大品牌為減少碳排放所做的努力正在加速從原生聚酯纖維轉變為化學回收和植物來源的替代品。 Indorama Ventures 和嘉仁化學回收公司生產的再生PET纖維能夠保持原生級的分子量,從而實現低熔點雙組分擠出,且不影響強度。 Fiberpartner 的「PolyPlant BICO」是一種雙組分纖維,其鞘套為耐熱130°C的PLA,並採用100%生物基熱黏合技術。本產品符合OEKO-TEX® Class 1 Annex 6標準,主要應用於以可堆肥性和皮膚安全性為首要考量的衛生用品領域。歐盟的「循環紡織品戰略」強制要求實施生態設計法規和數位護照,從而提升了對擁有ISCC Plus物料平衡認證供應商的需求。東方申宏憑藉其再生聚酯部門和從瓶到紗的直接紡絲工藝,正在成為可追溯、低碳原料的供應商。該公司生產的特級產品被耐吉和優衣庫等知名品牌所採用。

床墊和床上用品製造地的擴建

為了規避美國301條款關稅,原本銷往中國的床墊訂單如今正轉向越南和泰國的工廠。這一轉變導致該地區對低熔點聚碸纖維(PSF)的需求激增,這種纖維常用於絎縫被套和枕頭芯填充物。作為一項深思熟慮的策略,PVChem於2025年7月與越南聚合物公司(VNPOLY)簽署協議,向該國的聚對苯二甲酸乙二醇酯(POY)生產線供應再生聚對苯二甲酸乙二醇酯(PET)切片。位於宜山省的大規模瓶回收廠計劃於今年稍後投產,這將進一步加強這項措施。這種一體化模式有望顯著降低曾經對進口短纖維的依賴。此外,床墊製造商現在更注重縮短前置作業時間和提高纖維丹尼爾的柔軟性。這一轉變為當地加工商帶來了機遇,使他們能夠透過提供比中國競爭對手更低的運輸成本來獲得競爭優勢。

生產成本高昂,且PTA和MEG原料價格波動較大

2026年3月,印度PTA和MEG的價格先是飆漲後回落。這種價格波動迫使長絲生產商提高價格。中東供應路線的延誤以及中國生產商優先滿足國內需求,導致MEG現貨市場供應緊張。在商品化領域,一旦聚酯價格溢價超過一定閾值,買家就會轉向聚丙烯,價格傳導效應也會隨之減弱。儘管中國的半解聚計畫有望帶來顯著的節能效果,但其高昂的資本投入限制了這些計畫的即時實施。

細分市場分析

到2025年,131-160°C溫度範圍的纖維將成為市場主導,佔總需求的46.02%。其主要優勢在於壓延過程中良好的流動性以及在亞太地區倉庫中優異的抗冷凝性能(避免粘連)。熔點低於130°C的超低熔點纖維預計在2026年至2031年的預測期內將以6.72%的複合年成長率成長。它們日益普及的原因在於其在PLA基纖維中發揮關鍵作用,確保衛生棉和可堆肥信封的無縫黏合。相較之下,熔點高於160°C的高熔點纖維主要用於熔噴濾材和某些引擎室零件。然而,它們正逐漸被陶瓷纖維蠶食市場佔有率,尤其是在電池相關應用領域。低熔點纖維市場,特別是中熔點纖維市場,預計將顯著成長。隨著歐盟顆粒損耗法規於2025年12月生效,各大工廠目前正在部署除塵系統。這項轉變將使擁有現場防塵解決方案的綜合性企業受益。遠東新世紀正進行策略性投資,致力於提升低熔點下材料的彈性恢復性能,以提高運動服和壓力襪的利潤率。

一個新的趨勢是人們越來越重視回收。循環設計規格現在包括熔化溫度,從而簡化未來的分類流程。在歐洲,眼光獨到的大型買家願意為帶有「護照」(品質保證證書)的中價位纖維產品支付溢價,而不是購買來自檢驗供應商的產品。

區域分析

2025年,亞太地區在低熔點纖維市場佔據主導地位,市佔率高達51.37%。預計該地區在2026年至2031年的預測期內將維持6.77%的強勁複合年成長率。中國憑藉東方盛宏的大規模長絲生產線處於領先地位。自2026年第四季起,越南宜山rPET綜合體將透過向VNPOLY的POY擠出機供應再生切片來加強當地的供應鏈。儘管印度在2026年3月因原物料價格波動而出現價格上漲,但全年需求依然強勁,吸引新的參與企業進入低熔點纖維市場。

尤其是在北美,韓國進口聚苯乙烯泡沫塑膠(PSF)需繳納反傾銷稅。因此,買家正將目光轉向美國本土生產或墨西哥的加工商。 Indorama Ventures位於莫克斯維爾的生產線不僅縮短了衛生用品原始設備製造商(OEM)的交貨時間,也鞏固了其在汽車內裝領域的地位。

在歐洲,各方正致力於遵守顆粒損耗法規,並引入強制披露熔點資訊的數位護照,2025年12月的最後期限即將到來。德國和義大利均已表示願意為化學回收生產並經ISCC認證的低熔點產品支付溢價。雖然南美洲、中東和非洲的市場佔有率相對較小,但巴西衛生棉市場的擴張以及沙烏地阿拉伯的大規模基礎設施投資正在推動對地毯背襯和暖通空調隔熱材料的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對環保型和永續熱黏合纖維的需求日益成長

- 床墊及寢俱生產設施擴建

- 汽車隔音隔熱應用領域的成長

- 功能性運動服向無溶劑熱熔層壓製程的過渡

- 3D列印纖維預成型體在輕質複合材料的應用。

- 人們對用於電動車電池散熱墊的可生物分解LMF級材料的興趣日益濃厚。

- 市場限制因素

- 生產成本高昂,且PTA和MEG原料價格波動較大

- 與傳統黏合劑(黏合劑粉末、PP纖維)的激烈競爭

- 關於合成不織布中微塑膠釋放的法規(歐盟提案)

- 美國對來自韓國和台灣的低熔點聚苯乙烯泡沫塑膠徵收反傾銷稅

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按熔點

- 低於 130 度C

- 131~160°C

- 160 度C或更高

- 依結構類型

- 核心鞘套

- 並排

- 海島結構

- 最終用戶

- 紡織品和不織布

- 汽車和運輸業

- 家具和床上用品

- 建築材料

- 用於衛生和醫療用途的一次性產品

- 3D列印和複合材料

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Amerex Hubei Decon Polyester Co., Ltd.

- Beaulieu Fibres International

- Far Eastern New Century Corporation

- FiberPartner ApS

- Hickory Springs Manufacturing

- IFG International Fibres Group

- Indorama Ventures Public Company Limited

- Kolon Industries, Inc.

- NAN YA PLASTICS CORPORATION

- Shaoxing Global Chemical Fiber Co., Ltd.

- Sichuan Huvis

- Sinopec Yizheng Chemical Fibre Co., Ltd.

- Suzhou Makeit Technology Co., Ltd.

- Taekwang Industrial Co., Ltd.

- TEIJIN FRONTIER(USA), INC.

- Toray Advanced Materials Korea

- VNPOLYFIBER

- XiangLu Tenglong Group

- Yangzhou Tinfulong Group Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the low melting fiber market size is expected to grow from USD 2.36 billion in 2025 to USD 2.52 billion in 2026 and is forecast to reach USD 3.46 billion by 2031 at 6.57% CAGR over 2026-2031.

This report is Segmented by Melting Point (<=130°C, and More), Structure Type (Core-Sheath, Side-By-Side, and Islands-In-Sea), End-User Industry (Textiles and Nonwovens, Automotive and Transportation, Furniture and Bedding, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Low Melting Fiber Market Trends and Insights

Rising Demand for Eco-Friendly and Sustainable Thermal-Bond Fibers

Brand commitments to carbon reduction have accelerated the shift from virgin polyester to both chemically recycled and plant-based alternatives. Indorama Ventures and Jiaren Chemical Recycling have been producing textile-recycled PET that maintains virgin-grade molecular weight, allowing for a low-melt bicomponent extrusion without compromising strength. Fiberpartner's PolyPlant BICO, a bicomponent fiber with a 130 °C sheath made from PLA, boasts 100% bio-based thermal bonding. It meets the OEKO-TEX Class 1 Annex 6 standard and is aimed at hygiene products, where compostability and skin safety are paramount. The EU's Circular Textiles Strategy mandates ecodesign regulations and digital passports, pushing demand toward suppliers with the ISCC Plus mass-balance certification. Oriental Shenghong, with its recycled-polyester unit and a direct-spinning method from bottle to yarn, has emerged as a traceable, low-carbon feedstock provider. Its specialty grades cater to renowned brands such as Nike and Uniqlo.

Expansion of Mattress and Bedding Manufacturing Footprints

In a bid to evade U.S. Section 301 tariffs, mattress orders that once headed to China are now finding their way to factories in Vietnam and Thailand. This pivot has spurred a surge in demand for low-melt PSF in the region, a material frequently utilized in quilted covers and as filling for pillows. In a calculated maneuver, PVChem inked a pact in July 2025 with VNPOLY, directing recycled PET chips into the country's POY production lines. This effort is further strengthened by an upcoming bottle-recycling facility in Nghi Son, boasting a significant capacity, set to commence operations later this year. This integrated approach significantly reduces Vietnam's long-standing reliance on imported staple fiber, a dependency that was once pronounced. Additionally, mattress OEMs are now prioritizing shorter lead times and flexible denier counts. This evolution has created opportunities for local converters, enabling them to compete successfully by providing shipping costs that are lower than those of their Chinese rivals.

High Production Costs and PTA/MEG Feedstock Volatility

In March 2026, the prices of PTA and MEG in India surged before declining. This fluctuation compelled filament makers to increase their prices. A tightening in spot MEG availability emerged as Middle-East supply lines faced delays, while Chinese producers prioritized domestic demands. In commoditized segments, buyers shift to polypropylene when polyester premiums exceed a specific threshold, reducing the pass-through effect. Although Chinese semi-depolymerization projects promise significant energy savings, their high capital requirements limit immediate implementation.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Automotive Acoustic and Thermal-Insulation Applications

- Shift Toward Solvent-Free Hot-Melt Lamination in Functional Sportswear

- Intense Competition from Conventional Binders and U.S. Duties

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, the market saw the 131-160 °C band dominate, capturing 46.02% of the demand. Its appeal was largely due to its smooth flow during calendering and its resilience in Asia-Pacific warehouses, where it avoided sticking. Ultra-low-melt grades, set at or below 130 °C, are projected to expand at a 6.72% CAGR during the forecast period of 2026-2031. Their rising popularity is attributed to their pivotal role in PLA-based fibers, ensuring seamless bonding for hygiene pads and compostable mailers. In contrast, high-melt grades, surpassing 160 °C, are primarily used in melt-blown filter media and select under-hood components. However, they are losing market share to ceramic fibers, particularly in battery-adjacent applications. The market for low-melting fibers, especially in the mid-range band, is poised for significant growth. With the European Union's pellet-loss regulations taking effect in December 2025, major plants are now adopting dust capture systems. This transition favors integrated players with on-site containment solutions. In a calculated move, Far Eastern New Century is channeling investments into boosting elastic recovery at low-melt points, targeting the lucrative margins in sportswear and compression hosiery.

Emerging trends underscore a heightened focus on recycling; circular-design invoices now highlight melt temperatures, streamlining future separations. In Europe, discerning core buyers are willing to pay a premium for mid-range fiber lots accompanied by a "passport" - a quality assurance - over those from unverified sources.

Geography Analysis

In 2025, the Asia-Pacific region dominated the Low Melting Fiber market, capturing a substantial 51.37% share. Projections indicate the region will sustain a robust 6.77% CAGR through the forecast period of 2026-2031. China, anchored at the forefront, boasts significant filament lines at Oriental Shenghong. Starting in Q4 2026, Vietnam's Nghi Son rPET complex will bolster local supply loops by providing recycled chips to VNPOLY POY extruders. Even with feedstock price fluctuations in March 2026 leading to price hikes in India, the annual demand remains strong, attracting new players to the low-melt market.

North America finds itself contending with antidumping levies, specifically duties on imports of Korean PSF. Consequently, buyers are pivoting towards domestic U.S. production and converters in Mexico. Indorama Ventures' Mocksville line not only streamlines transit times for hygiene OEMs but also secures a position in the automotive interior sector.

Europe is preparing for a December 2025 deadline, focusing on pellet-loss compliance and the rollout of digital passports that require melt-point disclosures. Both Germany and Italy are showing a willingness to pay a premium for ISCC-certified, chemically recycled low-melt products. While South America and the Middle-East and Africa play relatively minor roles, Brazil's expanding footprint in hygiene pads and Saudi Arabia's significant infrastructure investments are driving demand for carpet backings and HVAC insulation.

- Amerex Hubei Decon Polyester Co., Ltd.

- Beaulieu Fibres International

- Far Eastern New Century Corporation

- FiberPartner ApS

- Hickory Springs Manufacturing

- IFG International Fibres Group

- Indorama Ventures Public Company Limited

- Kolon Industries, Inc.

- NAN YA PLASTICS CORPORATION

- Shaoxing Global Chemical Fiber Co., Ltd.

- Sichuan Huvis

- Sinopec Yizheng Chemical Fibre Co., Ltd.

- Suzhou Makeit Technology Co., Ltd.

- Taekwang Industrial Co., Ltd.

- TEIJIN FRONTIER (U.S.A.), INC.

- Toray Advanced Materials Korea

- VNPOLYFIBER

- XiangLu Tenglong Group

- Yangzhou Tinfulong Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for eco-friendly and sustainable thermal-bond fibers

- 4.2.2 Expansion of mattress and bedding manufacturing footprints

- 4.2.3 Growth in automotive acoustic and thermal-insulation applications

- 4.2.4 Shift toward solvent-free hot-melt lamination in functional sportswear

- 4.2.5 Emergence of 3-D printed fiber preforms for lightweight composites

- 4.2.6 Surging interest in biodegradable LMF grades for EV-battery thermal pads

- 4.3 Market Restraints

- 4.3.1 High production costs and PTA/MEG feed-stock volatility

- 4.3.2 Intense competition from conventional binders (adhesive powders, PP fibers)

- 4.3.3 Micro-plastic shedding restrictions on synthetic non-wovens (EU proposal)

- 4.3.4 US anti-dumping duties on Korean and Taiwanese low-melt PSF

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Melting Point

- 5.1.1 <= 130 °C

- 5.1.2 131 - 160 °C

- 5.1.3 Greater than 160 °C

- 5.2 By Structure Type

- 5.2.1 Core-Sheath

- 5.2.2 Side-by-Side

- 5.2.3 Islands-in-Sea

- 5.3 By End-user Industry

- 5.3.1 Textiles and Nonwovens

- 5.3.2 Automotive and Transportation

- 5.3.3 Furniture and Bedding

- 5.3.4 Construction and Building Materials

- 5.3.5 Hygiene and Medical Disposables

- 5.3.6 3-D Printing and Composites

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)}

- 6.4.1 Amerex Hubei Decon Polyester Co., Ltd.

- 6.4.2 Beaulieu Fibres International

- 6.4.3 Far Eastern New Century Corporation

- 6.4.4 FiberPartner ApS

- 6.4.5 Hickory Springs Manufacturing

- 6.4.6 IFG International Fibres Group

- 6.4.7 Indorama Ventures Public Company Limited

- 6.4.8 Kolon Industries, Inc.

- 6.4.9 NAN YA PLASTICS CORPORATION

- 6.4.10 Shaoxing Global Chemical Fiber Co., Ltd.

- 6.4.11 Sichuan Huvis

- 6.4.12 Sinopec Yizheng Chemical Fibre Co., Ltd.

- 6.4.13 Suzhou Makeit Technology Co., Ltd.

- 6.4.14 Taekwang Industrial Co., Ltd.

- 6.4.15 TEIJIN FRONTIER (U.S.A.), INC.

- 6.4.16 Toray Advanced Materials Korea

- 6.4.17 VNPOLYFIBER

- 6.4.18 XiangLu Tenglong Group

- 6.4.19 Yangzhou Tinfulong Group Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

膠纖維市場規模、佔有率和成長分析:按類型、原料、形態、功能、應用、分銷管道、最終用途和地區分類-2026-2033年產業預測

膠纖維市場規模、佔有率和成長分析:按類型、原料、形態、功能、應用、分銷管道、最終用途和地區分類-2026-2033年產業預測 2026年全球阻燃芳綸黏膠混紡纖維市場報告(防護纖維用)

2026年全球阻燃芳綸黏膠混紡纖維市場報告(防護纖維用) 纖維到纖維回收技術市場預測至2034年-全球技術、纖維類型、原料、製程階段、輸出形式、應用、經營模式、最終用戶與地區分析

纖維到纖維回收技術市場預測至2034年-全球技術、纖維類型、原料、製程階段、輸出形式、應用、經營模式、最終用戶與地區分析 軍用克維拉市場規模、佔有率和成長分析:按產品類型、功能、最終用途產業、材料整合、銷售管道和地區分類-2026-2033年產業預測2026年全球益生元纖維市場報告益生元纖維市場預測至2034年:按類型、來源、形態、性質、功能、應用、最終用戶、分銷管道和地區分類的全球分析

軍用克維拉市場規模、佔有率和成長分析:按產品類型、功能、最終用途產業、材料整合、銷售管道和地區分類-2026-2033年產業預測2026年全球益生元纖維市場報告益生元纖維市場預測至2034年:按類型、來源、形態、性質、功能、應用、最終用戶、分銷管道和地區分類的全球分析 農業纖維產品市場:依產品類型、形態、最終用途及通路分類-2026-2032年全球預測高鍺摻雜光纖市場:按應用、光纖類型、最終用戶、分銷管道和技術分類的全球預測(2026-2032年)2026年全球低熔點纖維市場報告

農業纖維產品市場:依產品類型、形態、最終用途及通路分類-2026-2032年全球預測高鍺摻雜光纖市場:按應用、光纖類型、最終用戶、分銷管道和技術分類的全球預測(2026-2032年)2026年全球低熔點纖維市場報告 益生元纖維市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)

益生元纖維市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)