|

市場調查報告書

商品編碼

2062339

被動式防火塗料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Passive Fire Protection Coating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

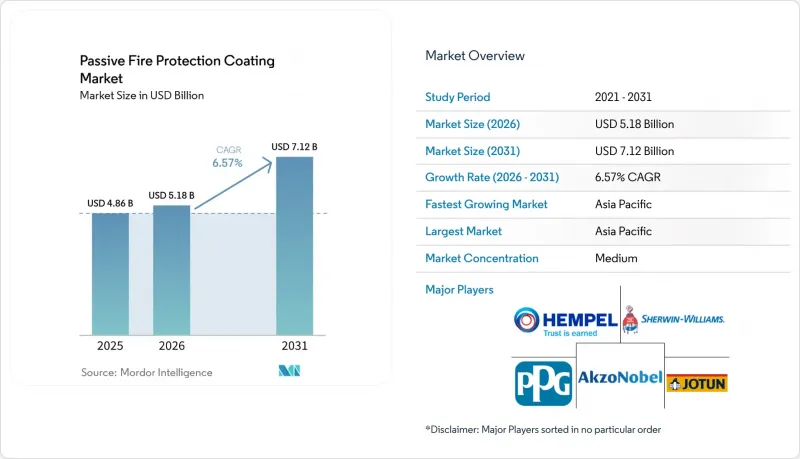

根據 Mordor Intelligence 預測,被動防火塗料市場規模將從 2025 年的 48.6 億美元成長到 2026 年的 51.8 億美元,到 2031 年將達到 71.2 億美元,2026 年至 2031 年的複合年成長率為 6.57%。

本報告按塗料類型(例如,膨脹塗料)、技術(例如,溶劑型塗料)、基材(例如,混凝土)、火災場景(例如,纖維素基防火塗料)、終端用戶行業(例如,石油和天然氣行業)以及地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以美元計價。

全球被動防火塗料市場趨勢及洞察

商業和工業物業需遵守嚴格的消防安全法規。

世界各國政府正日益採用基於性能的建築規範,強制要求塗料進行第三方認證,並縮短業主合規期限。 2025年12月,英國從BS 476標準過渡到BS EN 13501-1標準,實際上禁止在18公尺以上的建築物上使用易燃覆材,並刺激了對符合歐洲等級認證的膨脹塗料的需求。印度的《2024年國家建築規範》強制要求15公尺以上的商業建築使用符合IS 3809測試標準的塗料,目前孟買和班加羅爾共有120萬平方公尺的辦公空間正在進行維修工程。修訂後的歐盟建築產品法規將於2027年第三季生效,該法規將強制要求提供符合國際標準化組織(ISO)17025標準的性能聲明,並將對中小型供應商處以高額不合格罰款。在加州,一些先行企業正為2025年即將生效的第1113號規則修正案做準備。該修正案將建築塗料中揮發性有機化合物(VOC)的含量限制在每公升50克以內。隨著這些法規的日益普及,超薄、不含VOC的環氧塗料正逐漸成為被動防火塗料競標的標準配置。

全球高層建築和公共基礎設施建設的快速擴張

在新興市場都市化的推動下,超過300公尺的摩天大樓正以前所未有的速度拔地而起,這就要求塗料必須具備三小時的耐碳氫化合物暴露能力。到2025年,中國將建成87座超過200公尺的摩天大樓,每棟大樓的鋼骨上將使用約12,000平方公尺的膨脹薄膜。在印度的地鐵擴建工程中,地下月台必須使用符合UL 263標準的塗料,以抑製煙霧擴散。波灣合作理事會(GCC)正在推進一項價值1.3兆美元的基礎設施項目,涵蓋機場、港口和六座新城,並正在遵守阿拉伯聯合大公國的消防和生命安全標準,該標準要求關鍵部件具備兩小時的耐火性能。這些項目正在推動被動防火塗料市場的發展,而嚴格的耐火條款也正成為承包工程、採購和施工(EPC)合約中的常見條款。承包商擴大將塗層納入總價競標中,這簡化了採購流程,但增加了品質保證的成本。

與傳統覆材相比,建築成本更高

一套完整的可擴展防火系統安裝成本為每平方公尺35 至 85 美元,而非防火石膏的成本則為每平方公尺 15 至 30 美元。在火災保險覆蓋率低於房產價值 15% 的地區,這種成本差異會影響購屋決策。在已開發市場,人事費用佔總成本的比例高達 65%。此外,由於美國腐蝕工程師協會 (NACE) 或防腐蝕塗料與油漆協會 (SSPC) 認證的承包商短缺,導致美國和西歐的專案交付延遲 4 至 6 週。在南亞,預計 2023 年至 2025 年間年薪資成長率將超過 8%,許多開發商儘管認為噴淋系統的終身維護成本高出 40%,但仍選擇噴灌而非噴灌。

細分市場分析

到2025年,可膨脹塗料將佔銷售額的43.78%,其耐火時間僅為水泥基產品的十分之一。這項優勢在旨在限制額外靜載荷的抗震維修中意義重大。由於其兼具膨脹性和燒蝕吸熱的雙重保護機制,預計小型基材、混合產品和奈米增強薄膜的年複合成長率將達到6.87%。水泥基塗層曾因其成本較低而備受青睞,但由於其25毫米的厚度會減少可用占地面積並使暖通空調(HVAC)管道系統複雜化,因此其市場佔有率正在下降。燒蝕材料仍屬於小眾產品,主要用於航太和海軍艙室,這些艙室的峰值熱通量超過200千瓦/平方公尺(kW/m²)。

隨著加州設定2025年揮發性有機化合物(VOC)含量低於50克/公升(g/L)的目標,水性可膨脹塗料的應用日益廣泛。如今,它們已成為高層建築規範的標準配置,且在施工時無需佩戴呼吸防護設備。佐敦Steelmaster 1200WF符合ICC-ES AC23標準,乾膜厚度(DFT)達1350微米(µm),這顯示即使採用環保化學成分,也能滿足嚴格的性能標準。這些進步帶來了更高的利潤率和更短的施工時間,從而對被動防火塗料的市場前景產生了積極影響。

截至2025年,溶劑型塗料將佔34.88%的市場佔有率,尤其是在難以噴砂至接近金屬狀態的維修工程中。然而,由於其零VOC特性以及在居住的建築物中施工當天即可再次使用的優勢,預計到2031年,100%固態環氧塗料的複合年成長率將達到7.22%。水性塗料在高濕度地區面臨挑戰,因為當相對濕度(RH)達到80%時,其固化時間超過72小時,容易因雨水沖刷而造成徑流風險。同時,粉末塗料和紫外光固化塗料的應用僅限於汽車副車架和預製鋼模組等工廠生產線,因此需要投資靜電噴塗室和紫外線燈等設備。

自2026年1月起,歐盟工業排放指令將禁止未安裝熱氧化系統的VOC排放超過50毫克/標準立方公尺(mg/N m3)的作業。安裝一套熱氧化系統的成本在20萬至50萬歐元(23萬至58萬美元)之間。這項法規迫使業者轉向使用固態含量為80%或以上的塗料。 PPG預測,到2029年,這些高固態含量塗料將佔歐洲需求的55%,從而鞏固其在被動防火塗料市場的地位。

區域分析

預計到2025年,亞太地區將佔全球銷售額的37.43%,並在2031年之前維持7.21%的複合年成長率。中國在其「十四五」規劃中已撥款2.7兆元(約3,800億美元)用於都市更新。同時,印度的「智慧城市計畫」正100個城市加強消防安全標準。自2025年4月起,日本將強制要求高度超過31公尺的建築物使用膨脹型塗料。 2026年1月,韓國在其綠建築認證中引入了3小時被動防火性能的積分制,鼓勵私人開發人員採用高等級環氧樹脂。這些措施正在鞏固亞太地區在被動防火塗料市場的領先地位。

在北美,技術純熟勞工短缺正阻礙經濟成長,導致建築成本上漲15%至22%,工程工期延誤長達六週。儘管如此,耗資1,100億美元的《基礎設施投資與就業法案》已撥款用於18,000座橋樑和1,2,000個交通樞紐的塗料,確保了18億至24億美元的穩定需求。在加拿大,2025年建築規範修訂案規定,六層以上的木造建築必須具備兩小時的耐火性能,這導致不列顛哥倫比亞省和安大略省的塗料銷量激增。此外,在墨西哥的加工出口區(maquiladoras),用於處理易燃材料的倉庫必須強制使用符合美國保險商實驗室(UL)263標準的塗料,這正在推動該地區塗料的普及。

歐洲、中東和非洲呈現不同的趨勢。歐盟計畫於2027年第三季修訂《建築產品法規》(CPR),預計將增加每種產品的合規成本,從而使擁有ISO 17025認證檢測實驗室的公司獲得優勢。在波灣合作理事會(GCC),一項價值1.3兆美元的專案計畫要求所有新建碼頭必須具備2小時的耐火性能,導致杜拜和阿布達比的油漆進口量激增23%。同時,撒哈拉以南非洲地區的應用仍然有限。由於火災保險的覆蓋範圍不足建築物價值的10%,且主要城市以外的建築規範不夠完善,被動防火塗料的市場主要局限於政府資助的醫院和電信樞紐。

在南美洲,情況各不相同。在巴西,2025年3月生效的建築規範將強制要求在23公尺以上的住宅大樓安裝被動式防火屏障,預計將影響約18,000棟建築。在阿根廷,布宜諾斯艾利斯的石化設施正在進行維修,以符合阿根廷標準化和認證協會(IRAM)的碳氫化合物標準第11910號。智利的抗震加固舉措在2030年撥款21億美元,用可膨脹材料取代防火材料。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 商業和工業物業需遵守嚴格的消防安全法規。

- 全球高層建築和公共基礎設施的快速發展

- 石油、天然氣和電力資產(包括液化天然氣)的擴張

- 超薄環氧樹脂和膨脹塗料配方技術的進步

- 數位雙胞胎和感測器整合式PFP系統可實現預測性維護

- 市場限制因素

- 與傳統覆層。

- 在高濕度環境、強紫外線輻射環境或極低溫環境下性能下降。

- 磷基阻燃原料供應鏈的波動

- 奈米添加劑生態毒性方面的監管不確定性

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按塗層類型

- 膨脹塗層

- 水泥基塗料

- 燒蝕塗層

- 混合/奈米增強塗層

- 透過技術

- 溶劑型

- 水溶液

- 100%固態環氧樹脂

- 粉末塗裝和紫外光固化型

- 按基礎材料

- 結構鋼

- 具體的

- 樹

- 其他基材(塑膠、電纜、複合材料)

- 火災場景

- 纖維素基阻燃劑

- 防止碳氫化合物池火和噴射火

- 低溫液體洩漏預防

- 按最終用戶行業分類

- 商業和住宅建築

- 石油和天然氣(上游、中游、下游)

- 能源和電力(傳統能源和可再生能源)

- 工業製造

- 運輸(航運、航太、鐵路)

- 公共和關鍵基礎設施

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Akzo Nobel NV

- BASF

- Contego International Inc.

- Etex Group

- Firefree Coatings, Inc.

- Hempel A/S

- Hilti Group

- Isolatek International

- Isolatek International

- Jotun

- Kansai Paint Co., Ltd.

- Morgan Advanced Materials plc

- No-Burn, Inc.

- PPG Industries, Inc.

- RPM International Inc.

- Sika AG

- Teknos Group

- The Sherwin-Williams Company

- Tremco Incorporated

第7章 市場機會與未來展望

According to Mordor Intelligence, the passive fire protection coating market size is expected to grow from USD 4.86 billion in 2025 to USD 5.18 billion in 2026 and is forecast to reach USD 7.12 billion by 2031 at 6.57% CAGR over 2026-2031.

This report is Segmented by Coating Type (Intumescent Coatings and More), Technology (Solvent-Based and More), Substrate (Concrete, and More), Fire Scenario (Cellulosic Fire Protection and More), End-User Industry (Oil and Gas and More), Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Passive Fire Protection Coating Market Trends and Insights

Stringent Fire-Safety Regulations In Commercial & Industrial Real Estate

Governments are increasingly adopting performance-based codes, mandating third-party certification of coatings and shortening compliance timelines for asset owners. In December 2025, the United Kingdom transitioned from BS 476 to BS EN 13501-1, effectively prohibiting combustible cladding on structures exceeding 18 meters and driving demand for Euroclass-rated intumescents. India's National Building Code 2024 mandates IS 3809-tested coatings for commercial buildings over 15 meters, leading to retrofits across 1.2 million square meters of office space in Mumbai and Bengaluru. The European Union's updated Construction Products Regulation, effective Q3 2027, requires International Organization for Standardization (ISO) 17025-verified performance declarations, imposing significant non-compliance penalties on smaller suppliers. In California, early adopters are addressing 2025 amendments to Rule 1113, capping volatile organic compound (VOC) content at 50 grams per liter for architectural coatings. As these regulations gain traction, ultra-thin, zero-VOC epoxies are becoming standard in passive fire protection coating bids.

Rapid Build-Out Of High-Rise & Public Infrastructure Worldwide

Urbanization in emerging markets is driving the construction of record numbers of super-tall structures exceeding 300 meters, necessitating coatings with three-hour hydrocarbon exposure ratings. In 2025, China completed 87 buildings, surpassing 200 meters, each utilizing approximately 12,000 square meters of intumescent film on steel columns. India's metro-rail expansion mandates Underwriters Laboratories (UL) 263-compliant coatings for underground platforms to curb smoke spread. The Gulf Cooperation Council, with a USD 1.3 trillion infrastructure agenda spanning airports, seaports, and six new cities, adheres to the United Arab Emirates Fire and Life Safety Code, which demands two-hour resistance for primary members. Such projects are bolstering the passive fire protection coating market, with stringent fire-rating clauses now common in turnkey Engineering, Procurement, and Construction (EPC) contracts. Contractors are increasingly integrating coatings into lump-sum bids, streamlining procurement but raising quality-assurance expenses.

High Installed Cost Versus Conventional Cladding

Fully installed intumescent systems cost USD 35-85/m2 compared to USD 15-30/m2 for unrated plaster, representing a cost difference that impacts purchasing decisions in regions where fire insurance penetration is below 15% of asset value. In developed markets, labor accounts for up to 65% of the total cost. Additionally, a shortage of National Association of Corrosion Engineers (NACE) or Society for Protective Coatings (SSPC)-certified applicators has extended project handover timelines by four to six weeks in the United States and Western Europe. In South Asia, annual wage inflation exceeding 8% between 2023 and 2025 has prompted many developers to choose sprinklers over coatings, despite the 40% higher lifetime maintenance costs associated with sprinklers.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Oil, Gas & Power Assets Including LNG

- Advances In Ultra-Thin Epoxy-Intumescent Formulations

- Performance Degradation In Humid, UV-Rich Or Cryogenic Settings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Intumescents accounted for 43.78% of the revenue, achieving 60-180 minute ratings with just a tenth of the weight of cementitious products. This advantage is significant for seismic retrofits, which aim to limit added dead load. While starting from a smaller base, hybrids and nano-enhanced films are set to grow at a projected 6.87% compound annual growth rate (CAGR), due to their dual-mechanism protection that combines intumescence with ablative heat absorption. Cementitious layers, previously preferred for their low price, are losing ground due to their 25 mm thickness, which reduces usable floor space and complicates HVAC (heating, ventilation, and air conditioning) routing. Ablatives remain niche, catering to aerospace and naval compartments where peak heat flux surpasses 200 kilowatts per square meter (kW/m2).

Water-based intumescents gained traction following California's 2025 volatile organic compound (VOC) cap of 50 grams per liter (g/L). They are now standard in high-rise specifications, allowing application without respirators. Jotun's Steelmaster 1200WF, achieving ICC-ES AC23 compliance at 1,350 micrometers (µm) dry film thickness (DFT), demonstrates that eco-friendly chemistry can meet stringent performance standards. Such advancements improve profit margins and reduce installation time, positively influencing the market outlook for passive fire protection coatings.

In 2025, solvent-borne systems captured 34.88% of the market, especially in refurbishment jobs where near-white-metal blasting isn't feasible. However, 100% solids epoxies are on track for a 7.22% CAGR through 2031, driven by their zero-VOC credentials and the ability to return to service on the same day in occupied buildings. Water-based films face challenges in humid areas, where 80% relative humidity (RH) can extend curing beyond 72 hours, risking rain washout. Meanwhile, powder and ultraviolet (UV)-cured variants are limited to factory lines, used for automotive subframes and prefabricated steel modules, justifying their capital expenditure with electrostatic booths and UV lamps.

Starting January 2026, the European Union (EU) Industrial Emissions Directive will ban operations emitting over 50 milligrams per normal cubic meter (mg/N m3) VOC without thermal oxidizers, which come with a price tag of EUR 0.2-0.5 million (USD 0.23-0.58 million). This regulation is pushing the industry towards greater than or equal to 80% volume-solids chemistry. PPG forecasts that by 2029, these high-solids grades will make up 55% of European demand, solidifying their position in the passive fire protection coating market.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 37.43% of the revenue and is set to grow at a 7.21% Compound Annual Growth Rate (CAGR) through 2031. Under its 14th Five-Year Plan, China allocated CNY 2.7 trillion (USD 380 billion) for urban renewal. Meanwhile, India's Smart Cities Mission is enhancing fire codes in 100 municipalities. Starting April 2025, Japan will require intumescent coatings on buildings taller than 31 meters. In January 2026, South Korea's Green Building Certification introduced bonus points for three-hour passive protection, encouraging private developers to opt for premium epoxies. These initiatives position the Asia-Pacific region as a leader in the passive fire protection coating market.

North America's growth faces challenges due to a skilled labor shortage, leading to a 15-22% increase in installation costs and extending project timelines by up to six weeks. Nevertheless, the USD 110 billion Infrastructure Investment and Jobs Act allocates funds for coatings on 18,000 bridges and 12,000 transit stations, ensuring a consistent demand valued between USD 1.8-2.4 billion. In Canada, a 2025 code update mandates two-hour ratings for timber buildings exceeding six stories, resulting in a sales surge in British Columbia and Ontario. Additionally, Mexico's maquiladora corridors now require Underwriters Laboratories (UL) 263 coatings for warehouses handling flammable goods, broadening the regional adoption.

Europe, the Middle East, and Africa are witnessing varied developments. The European Union's (EU) Q3 2027 Construction Products Regulation (CPR) revision is set to elevate compliance costs per product, favoring firms equipped with International Organization for Standardization (ISO) 17025 laboratories. In the Gulf Cooperation Council (GCC), a USD 1.3 trillion pipeline mandates two-hour ratings for all new terminals, leading to a 23% spike in coating imports in Dubai and Abu Dhabi. Conversely, Sub-Saharan Africa's adoption is limited; with fire insurance covering under 10% of building values and weak codes outside major capitals, the market for passive fire protection coatings is largely confined to government-funded hospitals and telecom hubs.

South America sees a mix of developments. Brazil's code, effective March 2025, mandates passive barriers on residential towers exceeding 23 meters, impacting 18,000 buildings. In Argentina, Buenos Aires petrochemical sites are being retrofitted to meet Instituto Argentino de Normalizacion y Certificacion (IRAM) 11910 hydrocarbon standards. Chile's seismic resilience initiative is directing USD 2.1 billion towards intumescent upgrades until 2030.

- 3M

- Akzo Nobel N.V.

- BASF

- Contego International Inc.

- Etex Group

- Firefree Coatings, Inc.

- Hempel A/S

- Hilti Group

- Isolatek International

- Isolatek International

- Jotun

- Kansai Paint Co., Ltd.

- Morgan Advanced Materials plc

- No-Burn, Inc.

- PPG Industries, Inc.

- RPM International Inc.

- Sika AG

- Teknos Group

- The Sherwin-Williams Company

- Tremco Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent fire-safety regulations in commercial & industrial real-estate

- 4.2.2 Rapid build-out of high-rise & public infrastructure worldwide

- 4.2.3 Expansion of oil, gas & power assets (including LNG)

- 4.2.4 Advances in ultra-thin epoxy-intumescent formulations

- 4.2.5 Digital-twin & sensor-embedded PFP systems enabling predictive maintenance

- 4.3 Market Restraints

- 4.3.1 High installed cost versus conventional cladding

- 4.3.2 Performance degradation in humid, UV-rich or cryogenic settings

- 4.3.3 Supply-chain volatility for phosphorus-based flame-retardant feedstocks

- 4.3.4 Regulatory uncertainty around nano-additive ecotoxicity

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Coating Type

- 5.1.1 Intumescent Coatings

- 5.1.2 Cementitious Coatings

- 5.1.3 Ablative Coatings

- 5.1.4 Hybrid/Nano-enhanced Coatings

- 5.2 By Technology

- 5.2.1 Solvent-based

- 5.2.2 Water-based

- 5.2.3 100%-Solids Epoxy

- 5.2.4 Powder & UV-cured

- 5.3 By Substrate

- 5.3.1 Structural Steel

- 5.3.2 Concrete

- 5.3.3 Wood

- 5.3.4 Other Substrates (Plastics, Cables, Composites)

- 5.4 By Fire Scenario

- 5.4.1 Cellulosic Fire Protection

- 5.4.2 Hydrocarbon Pool & Jet-Fire Protection

- 5.4.3 Cryogenic Spill Protection

- 5.5 By End-user Industry

- 5.5.1 Commercial & Residential Construction

- 5.5.2 Oil & Gas (Up-, Mid- & Down-stream)

- 5.5.3 Energy & Power (Conventional & Renewable)

- 5.5.4 Industrial Manufacturing

- 5.5.5 Transportation (Marine, Aerospace, Rail)

- 5.5.6 Public & Critical Infrastructure

- 5.6 By Geography

- 5.6.1 Asia-Pacific

- 5.6.1.1 China

- 5.6.1.2 India

- 5.6.1.3 Japan

- 5.6.1.4 South Korea

- 5.6.1.5 ASEAN Countries

- 5.6.1.6 Rest of APAC

- 5.6.2 North America

- 5.6.2.1 United States

- 5.6.2.2 Canada

- 5.6.2.3 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Nordic Countries

- 5.6.3.8 Rest of Europe

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East & Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle East & Africa

- 5.6.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles {(includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)}

- 6.4.1 3M

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 BASF

- 6.4.4 Contego International Inc.

- 6.4.5 Etex Group

- 6.4.6 Firefree Coatings, Inc.

- 6.4.7 Hempel A/S

- 6.4.8 Hilti Group

- 6.4.9 Isolatek International

- 6.4.10 Isolatek International

- 6.4.11 Jotun

- 6.4.12 Kansai Paint Co., Ltd.

- 6.4.13 Morgan Advanced Materials plc

- 6.4.14 No-Burn, Inc.

- 6.4.15 PPG Industries, Inc.

- 6.4.16 RPM International Inc.

- 6.4.17 Sika AG

- 6.4.18 Teknos Group

- 6.4.19 The Sherwin-Williams Company

- 6.4.20 Tremco Incorporated

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

防火塗料市場:類型、基材類型、技術、應用方法、最終用途—2026-2032年全球市場預測阻燃噴霧劑市場按產品類型、銷售管道、應用和最終用戶分類,全球預測(2026-2032年)

防火塗料市場:類型、基材類型、技術、應用方法、最終用途—2026-2032年全球市場預測阻燃噴霧劑市場按產品類型、銷售管道、應用和最終用戶分類,全球預測(2026-2032年) 被動防火塗料市場規模、佔有率和成長分析(按產品、技術、分銷管道、最終用途產業和地區分類)—產業預測(2026-2033 年)

被動防火塗料市場規模、佔有率和成長分析(按產品、技術、分銷管道、最終用途產業和地區分類)—產業預測(2026-2033 年) 防火木器塗料市場-2025-2030年預測

防火木器塗料市場-2025-2030年預測 阻燃木器塗料:全球市佔率及排名、總收入及需求預測(2025-2031年)

阻燃木器塗料:全球市佔率及排名、總收入及需求預測(2025-2031年) 全球防火塗料市場

全球防火塗料市場 阻燃塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)全球木材防火塗料市場規模(按產品、應用、地區、範圍和預測)全球防火塗料市場:2024-2030

阻燃塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)全球木材防火塗料市場規模(按產品、應用、地區、範圍和預測)全球防火塗料市場:2024-2030 被動阻燃塗料市場報告:2030 年趨勢、預測與競爭分析

被動阻燃塗料市場報告:2030 年趨勢、預測與競爭分析