|

市場調查報告書

商品編碼

2062332

FRP容器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)FRP Vessels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

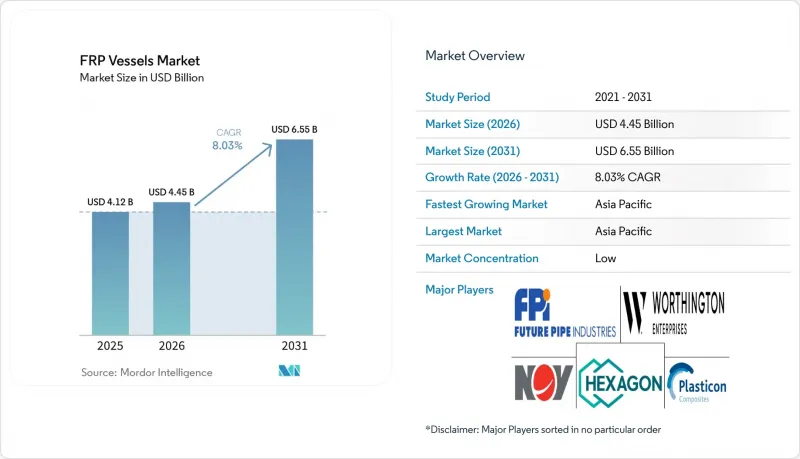

預計到 2025 年,FRP 貨櫃市場規模將達到 41.2 億美元,到 2026 年將達到 44.5 億美元,到 2031 年將達到 65.5 億美元,2026 年至 2031 年的複合年成長率為 8.03%。

本報告按容器類型(儲罐、塔器等)、壓力等級(低壓(10巴或以下))、纖維類型(玻璃纖維、碳纖維等)、應用領域(用水和污水處理、電力和能源等)、終端用戶行業(工業和化工等)以及地區(亞太地區、北美地區等)進行細分。市場預測以美元計價。

全球FRP貨櫃市場趨勢及洞察

使用輕質耐腐蝕材料

玻璃鋼(FRP)容器比鋼製容器輕約70%,便於運輸,並能減輕維修工程期間對基礎的負荷。在海上平台和海水淡化廠中,複合材料因其能消除電流腐蝕,無需塗漆即可實現30年以上的使用壽命,而備受青睞。化工廠採用雙層結構來耐受酸鹼腐蝕,避免了鋼製容器常見的內襯分層問題。 Encor Arabia於2025年向沙烏地阿拉伯水資源轉換公司(Saudi Water Conversion Corporation)供應了這類儲罐,充分展現了FRP在高溫海水環境中的卓越性能。在嚴苛的運作環境下,FRP的生命週期成本優勢遠超過其較高的初始成本。

來自用水和污水處理公司的需求不斷成長

在北美,由於腐蝕導致的故障,2024年至2025年間,北美各市政當局加速以FRP(玻璃鋼)儲槽取代鋼製儲槽。第七區水務局和佛羅裡達州公共產業部指出,降低維護成本和符合NSF/ANSI 61標準是主要原因。 First Line公司為青海省的一個鋰礦項目訂單了3019套FRP儲罐,這表明工業用水和採礦領域對FRP儲罐的需求正在擴大。在印度,預製污水處理系統中擴大採用FRP儲槽來處理高濃度氯化物廢水,並利用模組化移動床生物膜設計實現快速安裝。先前因維護積壓而推遲的維護工作,如今正推動著FRP儲罐的採購熱潮,而這一熱潮預計將持續數年。

高昂的初始資本支出(CAPEX)和安裝成本

複合材料儲罐的成本是鋼製儲罐的1.5到2.5倍,儘管其全生命週期總成本較低,但這仍然阻礙了預算緊張的公共產業採用複合材料儲罐。大直徑捲筒機的價格超過50萬美元,而專用起重設備又會使交付價格增加10%到15%。在維修工程中,荷載路徑的改變可能需要對地基維修,從而增加土木工程預算。此外,即使儲槽的使用壽命因腐蝕失效而縮短,由於熟悉程度和固有觀念,買家往往仍傾向於選擇鋼製產品。

細分市場分析

到2025年,儲槽將佔總銷售額的41.76%,憑藉其在水處理和化學品儲存領域的廣泛應用,繼續保持其在FRP容器市場的主導地位。反應器預計到2031年將以8.69%的複合年成長率成長,這主要得益於其在製程工業中抵抗化學和熱應力的可靠性。採用混合器和夾套的儲槽和反應器混合設計正在重新定義傳統類別,而用於食品和生物技術應用的衛生發酵槽也推動了市場需求的成長。

為了避免不銹鋼常見的點蝕問題,加工廠擴大指定使用符合 ASME RTP-1 或 BPE 標準的反應器。製藥公司採用內壁光滑的 1000 至 20000 公升纏繞成型容器,以方便進行原位就地清洗(CIP) 操作。食品加工企業使用 FRP 發酵槽生產醬油和醋等產品,而氫能運輸的發展則推動了車輛維修站採用球形圓柱體組件。在 FRP 容器市場,針對特定應用的工程設計仍然比標準化解決方案更為重要。

2025年,中壓容器(10-250巴)將佔銷售額的46.01%,推動工業氣體和城市燃氣管網領域的玻璃鋼容器市場成長。高壓容器(250巴及以上)預計到2031年將以8.92%的複合年成長率成長,主要受350巴物流氣瓶和700巴移動氣瓶需求的驅動。

ASME RTP-1:2023 標準規定了壓力低於 1 bar 的容器,而 UN R134、TPED 和 ISO 14692 則規範了高壓氫氣應用,這增加了測試成本。焊接研究委員會 (WRC) 2025 年發布的第 601 號公告解決了業主關注的問題,並提供了在用測試方面的指南。標準的協調統一仍然是一個挑戰,但透過聯合工作小組,正在取得進展。

區域分析

預計到2025年,亞太地區將佔全球銷售額的44.89%,並在2031年之前以9.18%的複合年成長率成長。這主要得益於中國日產600台逆滲透儲槽的生產設施以及印度的水循環利用計畫。韓國計劃在2040年引進620萬輛燃料電池汽車,將推動對高壓儲槽的需求。此外,東南亞國協的棕櫚油和水產養殖設施也正在使用玻璃鋼(FRP)。政府補貼和本地紡織品供應鏈有助於降低生產成本,進一步增強該地區的競爭優勢。

在北美,與頁岩氣相關的鋼鐵基礎設施更新和水處理正在推動這一趨勢。第七區和佛羅裡達州的相關部門計劃在2025年前安裝FRP飲用水罐,並報告維護成本降低。 Hexagon Puras公司正在將其位於馬裡蘭州的產能擴大到每年1萬個儲罐,而FRP已被用於加拿大油砂作業的尾礦水管理。根據美國《通膨控制法案》提供的氫氣補貼正在促進新建高壓容器工廠的建設。

在歐洲,嚴格的循環經濟法規與氫能發展舉措正在融合。歐盟清潔氫能夥伴關係正在資助研發工作,德國工廠每年生產4萬個氫氣瓶。在南歐和北非,海水淡化管道採用玻璃纖維(FRP)外殼以防止海水腐蝕。在中東,複合材料正被應用於大規模海水淡化和石化專案中,沙烏地阿美公司正與未來管道工業公司(Future Pipe Industries)合作,實現在地化供應。在拉丁美洲,墨西哥的氫氣瓶訂單和巴西化學工業的擴張推動了初步發展勢頭,但其產能仍落後於亞太地區。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 使用輕質耐腐蝕材料

- 用水和污水處理需求增加

- 擴大化工和石化產品的加工能力

- 可再生能源和海水淡化項目的成長

- 燃料電池交通運輸中氫氣儲存的快速普及

- 政府強制推廣綠氫能將刺激長期固定需求。

- 市場限制因素

- 較高的初始資本投入與安裝成本

- 可回收性和使用後處置途徑的局限性

- 大直徑纏繞成型技術純熟勞工短缺

- 關於FRP壓力容器的全球標準和法規存在不一致之處。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按容器類型

- 坦克

- 塔

- 管道

- 反應爐

- 球形束(IV型儲氫)

- 按壓力分類

- 低壓(10 巴或以下)

- 中壓(10-250 巴)

- 高壓(250巴或以上)

- 依纖維類型

- 玻璃纖維

- 碳纖維

- 醯胺纖維

- 混合纖維(玻璃-碳纖維/玻璃-玄武岩纖維)

- 透過使用

- 用水和污水處理

- 化學處理和儲存

- 石油、天然氣和石化產品的上游領域

- 食品/飲料加工

- 發電和海水淡化

- 氫氣和替代燃料的儲存

- 製藥和生物技術用液體

- 按最終用戶行業分類

- 工業和化學

- 石油、天然氣和石化產品

- 公營和私營供水事業

- 電力和能源

- 食品/飲料

- 其他終端用戶產業(紙漿和造紙、採礦、製藥)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Aquanomics Systems Limited

- Creative Composites Group

- EPP Composites Pvt Ltd.

- Fiber Tech Composite Pvt. Ltd.

- Fibro Plastichem

- Future Pipe Industries

- Hengshui Jiubo Composites Co., Ltd.

- Hexagon Composites ASA

- International Fiberglass LLC

- Jiangsu Jiuding New Material Co., Ltd.

- Mitsubishi Chemical Infratec Co., Ltd.

- NOV

- Plasticon

- RPS Composites

- Shalin Composites(India)Private Ltd.

- Worthington Enterprises

第7章 市場機會與未來展望

According to Mordor Intelligence, the fRP vessels market size is projected to be USD 4.12 billion in 2025, USD 4.45 billion in 2026, and reach USD 6.55 billion by 2031, growing at a CAGR of 8.03% from 2026 to 2031.

This report is Segmented by Vessel Type (Tanks, Columns, and More), Pressure Classification (Low Pressure (<=10 Bar), and More), Fiber Type (Glass Fiber, Carbon Fiber, and More), Application (Water and Wastewater Treatment, Power and Energy, and More), End-User Industry (Industrial and Chemical, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Value (USD).

Global FRP Vessels Market Trends and Insights

Adoption of Lightweight, Corrosion-Resistant Materials

FRP vessels reduce weight by approximately 70% compared to steel, easing transport and lowering foundation loads in retrofits. Offshore platforms and marine desalination sites prefer composites to eliminate galvanic corrosion, extending service life beyond 30 years without coatings. Chemical plants integrate dual-laminate designs for acids and alkalis, avoiding liner delamination seen in steel. Encore Arabia supplied such tanks to the Saudi Water Conversion Corporation in 2025, reinforcing FRP's viability in high-temperature seawater service. The lifetime-cost advantage outweighs higher upfront prices in harsh operating environments.

Rising Demand from Water and Wastewater Utilities

North American municipalities accelerated steel-to-FRP replacements in 2024-2025 after corrosion failures, with the Zone 7 Water Agency and the Florida Governmental Utility Authority citing lower maintenance and NSF/ANSI 61 compliance. First Line's 3,019-unit order for Qinghai lithium projects shows cross-sector pull between industrial water and mining. India's prefabricated sewage systems increasingly specify FRP for chloride-rich waste streams, leveraging modular moving-bed biofilm designs for rapid installation. Deferred maintenance backlogs now fuel a multiyear procurement wave.

High Initial CAPEX and Installation Costs

Composite vessels cost 1.5-to-2.5X steel alternatives, deterring budget-constrained utilities despite lower lifecycle totals. Large-diameter winders exceed USD 500,000, and specialized lifting gear adds another 10-15% to the delivered price. Retrofit sites may need foundation upgrades due to altered load paths, inflating civil budgets. Familiarity bias also steers buyers toward steel even after corrosion failures shorten tank life.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Chemical and Petrochemical Processing Capacity

- Growth in Renewable Energy and Desalination Projects

- Limited Recyclability and End-of-Life Pathways

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tanks accounted for 41.76% of the 2025 revenue, maintaining their dominance in the FRP vessels market due to their extensive use in water treatment and chemical storage. Reactors are projected to grow at a CAGR of 8.69% through 2031, driven by their reliability in handling chemical and thermal stress in process industries. Hybrid tank-reactor designs, incorporating mixers and jackets, are redefining traditional categories, while sanitary fermenters for food and biotech applications contribute to additional market demand.

Process plants increasingly specify ASME RTP-1 or BPE-compliant reactors to avoid pitting issues associated with stainless steel. Pharmaceutical manufacturers are adopting 1,000-20,000 L filament-wound vessels for their smooth inner surfaces, which facilitate CIP operations. Food processors are utilizing FRP fermenters for products like soy sauce and vinegar, while hydrogen mobility is driving the adoption of spherical cylinder bundles in fleet depots. The FRP vessels market continues to emphasize application-specific engineering over standardized solutions.

Medium pressure vessels (10-250 bar) contributed 46.01% of the 2025 revenue, dominating the FRP vessels market across industrial gases and municipal networks. High pressure vessels (>=250 bar) are expected to grow at a CAGR of 8.92% through 2031, driven by demand for 350-bar logistics and 700-bar mobility cylinders.

The ASME RTP-1:2023 standard governs sub-1 bar vessels, while UN R134, TPED, and ISO 14692 regulate high pressure hydrogen applications, leading to increased testing costs. The Welding Research Council's 2025 Bulletin 601 provides guidance for in-service inspections, addressing owner concerns. While code convergence remains a challenge, progress is being made through collaborative working groups.

Geography Analysis

Asia-Pacific captured 44.89% of the 2025 revenue and is projected to grow at a CAGR of 9.18% through 2031, supported by China's 600-unit-per-day RO vessel production facility and India's water renewal programs. South Korea's goal of deploying 6.2 million fuel-cell vehicles by 2040 sustains demand for high pressure cylinders, while ASEAN countries adopt FRP for palm-oil and aquaculture facilities. Government subsidies and local fiber supply chains help maintain low production costs, reinforcing the region's dominance.

North America benefits from steel infrastructure replacements and shale-gas water handling. Zone 7 and Florida authorities installed FRP potable-water tanks in 2025, reporting reduced maintenance costs. Hexagon Purus increased its Maryland production capacity to 10,000 cylinders annually, while Canada's oil sands adopted FRP for tailings water management. The U.S. Inflation Reduction Act's hydrogen credits are supporting the establishment of new high pressure vessel plants.

Europe blends strict circular-economy regulations with hydrogen development initiatives. The EU Clean Hydrogen Partnership funds R&D, and German facilities produce 40,000 cylinders annually. Southern Europe and North Africa are opting for FRP housings in desalination pipelines to prevent seawater corrosion. The Middle-East relies on composites for large-scale desalination and petrochemical projects, with Saudi Aramco partnering with Future Pipe Industries to localize supply. Latin America is showing early momentum with Mexico's hydrogen-cylinder order and Brazil's chemical expansions, though its capacity lags behind Asia-Pacific.

- Aquanomics Systems Limited

- Creative Composites Group

- EPP Composites Pvt Ltd.

- Fiber Tech Composite Pvt. Ltd.

- Fibro Plastichem

- Future Pipe Industries

- Hengshui Jiubo Composites Co., Ltd.

- Hexagon Composites ASA

- International Fiberglass LLC

- Jiangsu Jiuding New Material Co., Ltd.

- Mitsubishi Chemical Infratec Co., Ltd.

- NOV

- Plasticon

- RPS Composites

- Shalin Composites (India) Private Ltd.

- Worthington Enterprises

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of lightweight, corrosion-resistant materials

- 4.2.2 Rising demand from water and wastewater utilities

- 4.2.3 Expansion of chemical and petrochemical processing capacity

- 4.2.4 Growth in renewable-energy and desalination projects

- 4.2.5 Rapid hydrogen storage roll-out for fuel-cell mobility

- 4.2.6 National green-hydrogen mandates unlocking long-run captive demand

- 4.3 Market Restraints

- 4.3.1 High initial CAPEX and installation costs

- 4.3.2 Limited recyclability and end-of-life pathways

- 4.3.3 Skilled-labour shortages in large-diameter filament winding

- 4.3.4 Inconsistent global codes and standards for FRP pressure vessels

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Vessel Type

- 5.1.1 Tanks

- 5.1.2 Columns

- 5.1.3 Pipes

- 5.1.4 Reactors

- 5.1.5 Spherical Bundles (Type-IV H2 storage)

- 5.2 By Pressure Classification

- 5.2.1 Low Pressure (<=10 bar)

- 5.2.2 Medium Pressure (10-250 bar)

- 5.2.3 High Pressure (>=250 bar)

- 5.3 By Fiber Type

- 5.3.1 Glass Fiber

- 5.3.2 Carbon Fiber

- 5.3.3 Aramid Fiber

- 5.3.4 Hybrid Fiber (Glass-Carbon/Glass-Basalt)

- 5.4 By Application

- 5.4.1 Water and Wastewater Treatment

- 5.4.2 Chemical Processing and Storage

- 5.4.3 Oil, Gas and Petrochemical Upstream

- 5.4.4 Food and Beverage Processing

- 5.4.5 Power Generation and Desalination

- 5.4.6 Hydrogen and Alternative-Fuels Storage

- 5.4.7 Pharmaceutical and Biotech Fluids

- 5.5 By End-user Industry

- 5.5.1 Industrial and Chemical

- 5.5.2 Oil, Gas and Petrochemicals

- 5.5.3 Municipal and Private Water Utilities

- 5.5.4 Power and Energy

- 5.5.5 Food and Beverage

- 5.5.6 Other End-user Industries (Pulp and Paper, Mining, Pharma)

- 5.6 By Geography

- 5.6.1 Asia-Pacific

- 5.6.1.1 China

- 5.6.1.2 Japan

- 5.6.1.3 India

- 5.6.1.4 South Korea

- 5.6.1.5 ASEAN Countries

- 5.6.1.6 Rest of Asia-Pacific

- 5.6.2 North America

- 5.6.2.1 United States

- 5.6.2.2 Canada

- 5.6.2.3 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle-East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle-East and Africa

- 5.6.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Aquanomics Systems Limited

- 6.4.2 Creative Composites Group

- 6.4.3 EPP Composites Pvt Ltd.

- 6.4.4 Fiber Tech Composite Pvt. Ltd.

- 6.4.5 Fibro Plastichem

- 6.4.6 Future Pipe Industries

- 6.4.7 Hengshui Jiubo Composites Co., Ltd.

- 6.4.8 Hexagon Composites ASA

- 6.4.9 International Fiberglass LLC

- 6.4.10 Jiangsu Jiuding New Material Co., Ltd.

- 6.4.11 Mitsubishi Chemical Infratec Co., Ltd.

- 6.4.12 NOV

- 6.4.13 Plasticon

- 6.4.14 RPS Composites

- 6.4.15 Shalin Composites (India) Private Ltd.

- 6.4.16 Worthington Enterprises

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

2026年全球纖維增強聚合物(FRP)和複合材料市場報告

2026年全球纖維增強聚合物(FRP)和複合材料市場報告 纖維增強塑膠市場:依纖維類型、樹脂類型和終端用戶產業分類-2026-2032年全球預測

纖維增強塑膠市場:依纖維類型、樹脂類型和終端用戶產業分類-2026-2032年全球預測 2026 年至 2035 年模壓 FRP 格柵的市場機會、成長要素、產業趨勢和預測。

2026 年至 2035 年模壓 FRP 格柵的市場機會、成長要素、產業趨勢和預測。 FRP管材市場報告:按類型、製造流程、應用和地區分類(2026-2034年)FRP貨櫃市場:按貨櫃類型、製造流程和應用分類-2026-2032年全球市場預測FRP儲槽市場:按類型、容量、製造流程、材質等級、應用和最終用戶分類-2026-2032年全球市場預測FRP橋樑市場:按橋樑類型、纖維類型、樹脂類型、組件和應用分類-2026-2032年全球市場預測FRP格柵市場:2026-2032年全球市場預測(依成型製程、樹脂類型、應用及終端用戶產業分類)玻璃纖維增強塑膠管道市場機會、成長要素、產業趨勢分析及預測(2026-2035年)2026年全球FRP儲槽市場報告

FRP管材市場報告:按類型、製造流程、應用和地區分類(2026-2034年)FRP貨櫃市場:按貨櫃類型、製造流程和應用分類-2026-2032年全球市場預測FRP儲槽市場:按類型、容量、製造流程、材質等級、應用和最終用戶分類-2026-2032年全球市場預測FRP橋樑市場:按橋樑類型、纖維類型、樹脂類型、組件和應用分類-2026-2032年全球市場預測FRP格柵市場:2026-2032年全球市場預測(依成型製程、樹脂類型、應用及終端用戶產業分類)玻璃纖維增強塑膠管道市場機會、成長要素、產業趨勢分析及預測(2026-2035年)2026年全球FRP儲槽市場報告