|

市場調查報告書

商品編碼

2062329

軸承隔離器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Bearing Isolators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

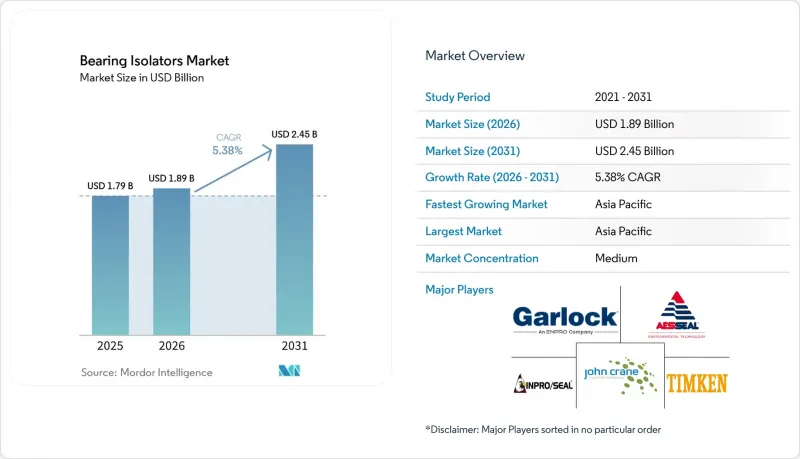

根據 Mordor Intelligence 預測,軸承隔離器市場規模預計在 2025 年達到 17.9 億美元,2026 年達到 18.9 億美元,到 2031 年達到 24.5 億美元,2026 年至 2031 年的複合年成長率為 5.38%。

本報告按類型(例如,非接觸式軸承隔振器)、材料(例如,金屬(青銅、不銹鋼、鋁))、應用(例如,泵浦、馬達)、終端用戶產業(例如,石油和天然氣、化學和石化產業)以及地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以美元計價。

全球軸承隔離器市場趨勢及洞察

對免維護軸承保護的需求日益成長

工業買家現在優先考慮的是整體擁有成本。利勃海爾2024年推出的固體潤滑系統承諾10-15年無需重新潤滑的使用壽命。隨後,阿姆斯壯在2025年推出了一款循環泵,進一步強化了這一價值提案,該循環泵結合了永久密封和NSF/ANSI 61合規性。一個售價300美元的非接觸式隔離器可以避免15,000美元的泵浦拆卸成本,並透過防止首次故障收回成本。舍弗勒2025年推出的感應加熱工具使工人能夠在計畫停電期間安裝隔離器,從而將停機時間縮短一半。因此,面臨每天50,000美元服務中斷罰款的水處理運營商正在將迷宮式或磁性系統作為標準配置。

對設備運作和可靠性的要求日益提高

數位雙胞胎技術的應用正在不斷推進。西門子能源的Omnivise套件於2025年開始採集軸承座的振動數據,提早90天預測密封件表面磨損狀況,並將強制停機次數減少40%。購電協議(PPA)的違約金條款規定,一座500兆瓦電廠的運轉率每下降1%,就會損失200萬美元的收入。約翰·克萊恩公司於2025年中期推出的93AX型同軸密封件,可防止軸跳動超過0.5毫米,從而維持接觸壓力,避免洩漏導致汽輪機跳閘。根據歐洲航空安全局(EASA)2024年的一項研究,過量潤滑脂的使用造成了36%的馬達故障,這加速了向無潤滑脂隔離器的轉變。

與接觸式密封件相比,初始成本較高

非接觸式軸承隔振器的成本通常是彈性體唇形密封的三到五倍。儘管其總體擁有成本 (TCO) 較低,但在成本受限的市場中,採購團隊很難證明這種價格差異的合理性。例如,一台 100 匹馬力馬達的青銅迷宮式隔振器零售價為 250 至 350 美元,而丁腈橡膠唇形密封件的零售價僅為 60 至 80 美元,初始成本相差 190 至 270 美元,需要多年投資回收期才能證明其合理性。鐵姆肯公司的「EcoTurn」隔振器將於 2025 年起以 180 美元的價格出售,正在縮小這一價格差距,但由於採購和維護部門之間的獎勵存在分歧,該產品在印度和東南亞的普及速度仍然緩慢。

細分市場分析

到2025年,非接觸式迷宮結構仍將佔據軸承隔離器市場46.89%的佔有率,但目前主要用於泵浦和標準轉速馬達。 ISO 16281:2025標準對唇形密封件在污染條件下的性能退化進行了更嚴格的定義,加速了磁性結構的普及。磁性結構在預測期(2026-2031年)內將以5.90%的複合年成長率成長,並在需要零磨損的高速燃氣渦輪機中越來越受歡迎。聯合循環燃氣渦輪機運營商報告稱,Isomag的混合陶瓷型號已將檢查間隔延長至60,000小時。

在磁性流體和彈性體無法承受極端環境的低溫泵和海底驅動裝置中,迷宮式、螺旋槽式和其他專用密封件仍然至關重要。對於可能出現軸偏心的情況,採用混合O型圈和聚四氟乙烯(PTFE)相結合的設計,例如John Crane的8628VL,可允許1.0毫米的跳動量,從而擴大了適用的安裝範圍。

2025年軸承隔振器市場中,金屬(青銅、不銹鋼和鋁)材質的隔振器將佔據50.87%的市場佔有率,其中青銅和不銹鋼在石油天然氣和製藥行業的高腐蝕性清洗環境中發揮主導作用。然而,複合材料/混合材料隔振器市場在預測期(2026-2031年)內預計將以6.34%的年成長率成長。 PEEK增強PTFE材料在風力發電機中的應用正在加速,其更輕的機艙將降低每千瓦的成本,因為在2025年的實驗室測試中,該材料已將磨損降低了60%。

在聚合物化學技術進一步成熟之前,青銅仍將是酸性氣體和硫酸環境下的標準選擇。隨著派克漢尼芬公司推出符合美國食品藥物管理局(食品藥物管理局)標準、可承受 150 度C蒸氣滅菌循環的 316L 不銹鋼產品,316L 不銹鋼的應用勢頭日益強勁。鋁比青銅輕 65%,目前正逐漸取代天花板式暖通空調維修中較重的零件。

區域分析

預計到2025年,亞太地區將佔據軸承隔離器市場40.78%的佔有率,並以6.39%的年均成長率成長至2031年。中國2024年電機產量將達到18億台,將推動OEM(目的地設備製造商)和維修需求的成長。印度機械進口成長22%,以及東協地區2,260億美元的外國直接投資,都強化了設計階段採用隔離器規範的趨勢。日本和韓國採用ISO 17956:2025標準,進一步削弱了接觸式密封件的競爭力,並加速了區域轉型。

在北美,OSHA 2025 Guard法規正在推動食品和製藥廠從唇形密封件轉向NSF H1認證的隔離器。加拿大油砂的測試表明,引入VBMag後,軸承更換頻率降低了80%。墨西哥的近岸外包也推動了無塵室組裝輸送機對迷宮式密封的需求。

2025年,歐洲市場佔有率的成長得益於離岸風力發電的擴張。 System Seals的複合材料單元目前已應用於北海60%的新建風力發電機。修訂後的2006/42/EC指令提高了高速觸發閾值,加速了德國和法國的升級改造。在俄羅斯,儘管供應鏈中斷,自主設計正在逐步推進。南美洲和中東及非洲(MEA)地區的市佔率總合不足10%,但在採礦、石化和海水淡化產業有局部需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對免維護軸承保護的需求日益成長

- 對設備運作和可靠性的要求日益提高

- 新興市場製造業與重工業的擴張

- 加強職業安全和機械方面的法規

- 引入軸承隔振器以防止變頻器造成的電火花加工損傷。

- 用於維修可再生能源渦輪機重量的增材成型複合複合材料隔振器。

- 市場限制因素

- 與接觸式密封件相比,初始成本較高

- 高速或錯位應用中的技術限制

- OEM廠商轉向全封閉式「免維護」電機,正在降低維修的需求。

- 銅鎳合金原料價格波動

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 非接觸式軸承隔離器

- 混合式(接觸式+非接觸式)隔離器

- 磁軸承隔振器

- 迷宮/螺旋槽/其他特殊設計

- 材料

- 金屬(青銅、不鏽鋼、鋁)

- 非金屬材料(聚四氟乙烯、超高分子量聚乙烯、彈性體)

- 複合材料/混合材料

- 透過使用

- 泵浦

- 引擎

- 變速箱

- 壓縮機

- 風扇和鼓風機

- 渦輪機(蒸氣、瓦斯、風力)

- 其他旋轉設備(輸送機、攪拌機、攪拌器)

- 按最終用戶行業分類

- 石油和天然氣

- 化工/石油化工

- 發電

- 供水和廢水處理

- 食品/飲料加工

- 製藥和生命科學

- 紙漿和造紙

- 採礦和金屬

- 製造和工業機械

- 船舶、運輸和暖通空調

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、合作、產品發布)

- 市佔率和排名分析

- 公司簡介

- ABB

- Advanced Sealing International

- AESSEAL

- EagleBurgmann

- Flowserve Corporation

- Freudenberg Sealing Technologies

- Garlock(Enpro Inc.)

- Huhnseal AB

- Inpro/Seal

- ISOMAG Corporation

- John Crane

- NSK Ltd.

- Parker Hannifin Corp

- Schaeffler India Limited

- SEPCO Inc.

- SKF Group

- The Timken Company

- Trelleborg Marine and Infrastructure

- Trico Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the bearing isolators market size is projected to be USD 1.79 billion in 2025, USD 1.89 billion in 2026, and reach USD 2.45 billion by 2031, growing at a CAGR of 5.38% from 2026 to 2031.

This report is Segmented by Type (Non-Contact Bearing Isolators, and More), Material (Metallic (Bronze, Stainless, and Aluminum), and More), Application (Pumps, Motors, and More), End-User Industry (Oil and Gas, Chemical and Petrochemical, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Bearing Isolators Market Trends and Insights

Growing Demand for Maintenance-Free Bearing Protection

Industrial buyers now prioritize total cost of ownership. Liebherr's 2024 solid-lubrication system set expectations for 10-15-year service life without re-greasing. Armstrong followed by launching circulators in 2025 that pair permanent seals with NSF/ANSI 61 compliance, further validating the value narrative. A USD 300 non-contact isolator averts pump teardowns that cost USD 15,000, paying for itself at the first avoided failure. Schaeffler's induction-heating tools, released in 2025, let crews install isolators during planned outages, cutting downtime in half. Water-treatment operators, facing USD 50,000-per-day penalties for service interruptions, are therefore standardizing on labyrinth or magnetic formats.

Increasing Equipment Uptime and Reliability Requirements

Digital-twin adoption is deepening. Siemens Energy's Omnivise suite began ingesting bearing-housing vibration data in 2025 to predict seal-face wear 90 days ahead, reducing forced outages by 40%. Penalty clauses in power-purchase agreements make each 1% availability shortfall worth USD 2 million in lost revenue on a 500 MW station. John Crane's Type 93AX coaxial seal, launched mid-2025, holds contact pressure over 0.5 mm of shaft runout, preventing leaks that would otherwise trip turbines. An EASA (European Union Aviation Safety Agency) 2024 study found that over-greasing causes 36% of electric-motor failures, intensifying the pivot toward grease-free isolators.

Higher Initial Cost Versus Contact Seals

Non-contact bearing isolators typically command a 3-5X price premium over elastomeric lip seals, a gap that procurement teams in cost-constrained markets struggle to justify despite superior total cost of ownership. A bronze labyrinth isolator for a 100 HP motor retails at USD 250-350, whereas a nitrile lip seal costs USD 60-80, creating a USD 190-270 upfront delta that requires multi-year payback modeling to rationalize. Timken's EcoTurn, priced at USD 180 since 2025, narrows the gap, yet split incentives between procurement and maintenance still slow adoption in India and Southeast Asia.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Manufacturing and Heavy Industries in Emerging Markets

- Stricter Workplace Safety and Machinery Regulations

- Technical Limits in High-Speed or Misaligned Applications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Non-contact labyrinth formats, while still representing the 46.89% of the Bearing Isolators market in 2025, now serve mainly pumps and standard-speed motors. Compliance with ISO 16281:2025, which more harshly derates lip seals under contamination, is hastening the pivot toward magnetic forms. Magnetic architectures are advancing at a CAGR of 5.90% for the forecast period (2026-2031) and are increasingly preferred for high-speed turbines that demand zero wear. Combined-cycle gas-turbine operators find that Isomag's hybrid ceramic models extend service intervals to 60,000 hours.

Labyrinth, spiral-groove, and other specialized niches remain essential for cryogenic pumps and subsea drives where magnetic fluids or elastomers cannot survive extreme conditions. For misalignment-prone shafts, hybrid O-ring plus PTFE concepts such as John Crane's 8628VL tolerate 1.0 mm runout, broadening addressable installations.

Metallic (Bronze, Stainless, and Aluminum) designs held 50.87% share of the Bearing Isolators market size in 2025, led by bronze and stainless steel in corrosive oil-and-gas or pharma wash-down situations. Yet the composite/hybrid materials segment is on a 6.34% expansion trajectory for the forecast period (2026-2031). PEEK-reinforced PTFE achieved 60% lower wear in 2025 lab tests, accelerating wind-turbine adoption where nacelle weight savings translate to cost per kilowatt.

Bronze will remain the default for sour-gas or sulfuric-acid exposure until polymer chemistry matures further. Stainless 316L gained momentum after Parker Hannifin introduced an FDA (Food and Drug Administration)-compliant version that survives 150°C steam-sterilization cycles. Aluminum, 65% lighter than bronze, now replaces heavier units in ceiling-mounted HVAC retrofits.

Geography Analysis

Asia-Pacific held 40.78% of the Bearing Isolators market share in 2025 and will grow at 6.39% through 2031. China's output of 1.8 billion motors in 2024 provides both OEM (Original Equipment Manufacturer) and retrofit pull. India's 22% machinery-import rise and ASEAN's USD 226 billion FDI wave reinforce a pattern of design-stage isolator specification. ISO 17956:2025 adoption in Japan and South Korea further penalizes contact seals, accelerating regional transitions.

In North America, OSHA's 2025 guarding rule is nudging food and pharma plants to swap lip seals for NSF H1-rated isolators. Canadian oil-sands trials showed an 80% cut in bearing swaps after VBMag installations. Near-shoring in Mexico is fueling labyrinth-seal demand for cleanroom assembly conveyors.

Europe's market share in 2025 was anchored by offshore-wind uptake. System Seals' composite units now appear in 60% of new North Sea turbines. The revised 2006/42/EC directive's higher-speed trigger levels catalyze upgrades across Germany and France. Russia pivots to in-house designs amid supply-chain rifts. South America and MEA together represent less than 10% but show pockets of demand in mining, petrochemicals, and desalination.

- ABB

- Advanced Sealing International

- AESSEAL

- EagleBurgmann

- Flowserve Corporation

- Freudenberg Sealing Technologies

- Garlock (Enpro Inc.)

- Huhnseal AB

- Inpro/Seal

- ISOMAG Corporation

- John Crane

- NSK Ltd.

- Parker Hannifin Corp

- Schaeffler India Limited

- SEPCO Inc.

- SKF Group

- The Timken Company

- Trelleborg Marine and Infrastructure

- Trico Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for maintenance-free bearing protection

- 4.2.2 Increasing equipment uptime and reliability requirements

- 4.2.3 Expansion of manufacturing and heavy industries in emerging markets

- 4.2.4 Stricter workplace-safety and machinery regulations

- 4.2.5 Integration of shaft-grounding bearing isolators to prevent VFD-induced EDM damage

- 4.2.6 Additive-manufactured composite isolators for lightweight retrofits in renewable-energy turbines

- 4.3 Market Restraints

- 4.3.1 Higher initial cost vs contact seals

- 4.3.2 Technical limits in high-speed or mis-aligned applications

- 4.3.3 OEM shift to fully sealed "maintenance-free" motors reducing retrofit demand

- 4.3.4 Raw-material price volatility for copper-/nickel-based alloys

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Non-Contact Bearing Isolators

- 5.1.2 Hybrid (Contact + Non-Contact) Isolators

- 5.1.3 Magnetic Bearing Isolators

- 5.1.4 Labyrinth/Spiral-Groove/Other Specialized Designs

- 5.2 By Material

- 5.2.1 Metallic (Bronze, Stainless, and Aluminum)

- 5.2.2 Non-Metallic (PTFE, UHMWPE, and Elastomers)

- 5.2.3 Composite/Hybrid Materials

- 5.3 By Application

- 5.3.1 Pumps

- 5.3.2 Motors

- 5.3.3 Gearboxes

- 5.3.4 Compressors

- 5.3.5 Fans and Blowers

- 5.3.6 Turbines (Steam, Gas, and Wind)

- 5.3.7 Other Rotating Equipment (Conveyors, Mixers, and Agitators)

- 5.4 By End-user Industry

- 5.4.1 Oil and Gas

- 5.4.2 Chemical and Petrochemical

- 5.4.3 Power Generation

- 5.4.4 Water and Waste-water Treatment

- 5.4.5 Food and Beverage Processing

- 5.4.6 Pharmaceuticals and Life Sciences

- 5.4.7 Pulp and Paper

- 5.4.8 Mining and Metals

- 5.4.9 Manufacturing and Industrial Machinery

- 5.4.10 Marine, Transportation and HVAC

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (MandA, Partnerships, Product Launches)

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 ABB

- 6.4.2 Advanced Sealing International

- 6.4.3 AESSEAL

- 6.4.4 EagleBurgmann

- 6.4.5 Flowserve Corporation

- 6.4.6 Freudenberg Sealing Technologies

- 6.4.7 Garlock (Enpro Inc.)

- 6.4.8 Huhnseal AB

- 6.4.9 Inpro/Seal

- 6.4.10 ISOMAG Corporation

- 6.4.11 John Crane

- 6.4.12 NSK Ltd.

- 6.4.13 Parker Hannifin Corp

- 6.4.14 Schaeffler India Limited

- 6.4.15 SEPCO Inc.

- 6.4.16 SKF Group

- 6.4.17 The Timken Company

- 6.4.18 Trelleborg Marine and Infrastructure

- 6.4.19 Trico Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment