|

市場調查報告書

商品編碼

2062328

熱固性模塑膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Thermoset Molding Compound - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

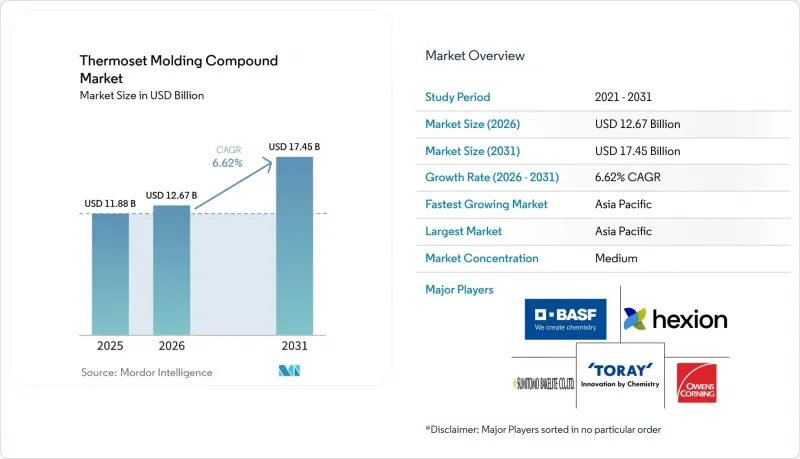

根據 Mordor Intelligence 預測,熱固性模塑化合物的市場規模預計將在 2025 年達到 118.8 億美元,在 2026 年達到 126.7 億美元,在 2031 年達到 174.5 億美元,從 2026 年到 2031 年的複合年成長率為 62%。

本報告按樹脂類型(環氧樹脂、三聚氰胺-甲醛樹脂、脲醛樹脂等)、纖維增強材料(玻璃纖維、碳纖維等)、應用領域(電氣電子、汽車、航太、建築等)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以美元計價。

全球熱固性模塑膠市場趨勢及洞察

在電氣和電子領域不斷擴大應用

800V電動車逆變器和5G基地台的溫度控管要求正推動環氧樹脂的導熱係數向0.80 W/m/K或更高、介電常數向4.0或更低的方向發展。混合hBN-AlN填料系統無需使用鹵素即可達到UL 94 V-0阻燃等級,並可用於資料中心電源,滿足其在105 度C下連續使用測試的要求。預計到2026年,中國印刷基板產值將達到546億美元,將帶動FR-4和高頻層壓板對環氧樹脂的需求。在人工智慧加速器的半導體封裝領域,玻璃化轉變溫度超過150 度C的環烷基環氧樹脂越來越受歡迎,這正在蠶食酚醛樹脂的市場佔有率。認證週期縮短至不到12個月,使能夠提供數位模擬和快速內部原型製作能力的供應商獲得了競爭優勢。

促進汽車和航太領域的減重

由於歐洲法規將車輛二氧化碳排放限制在95克/公里以內,整車製造商被迫將支架、橫樑和電池外殼等零件的材質從鋼材更換為玻璃纖維酚醛樹脂和碳纖維環氧樹脂,從而減輕車輛重量高達50%。BASF的噴塗傳遞模塑製程可在3分鐘內完成A級車身面板的生產,無需使用油漆固化爐,並可降低40%的能耗。在航太領域,HexPly M51預浸料可在180 度C下固化40分鐘,降低高壓釜能耗30%,並提高單班生產能力。在韓國供應鏈中,玻璃纖維氈熱塑性保險桿橫梁正作為酚醛片狀成型在非結構領域的潛在替代品進行試驗。在整體行動旅遊平台領域,減重可直接轉化為法規積分和更長的電池續航里程,從而提升熱固性模塑膠在市場上的價值提案。

可回收性和處置成本低

由於不可逆的交聯反應,大部分熱固性樹脂廢料只能掩埋或進行成本高成本的熱解熱解。熱解成本為每噸200至400美元,相當於原生材料價值的兩倍。歐盟指令2018/851的目標是到2030年實現複合材料70%的回收率,但機械破碎會將材料分解為低價值的填充材。一台3兆瓦的風力發電機就會產生20噸葉片廢棄物,預計歐洲將有14,000片葉片被丟棄,這給德國和丹麥的掩埋帶來了巨大壓力。可拆卸設計會使每輛車的人事費用增加50至100美元,除非擴大生產者延伸責任制,否則原始設備製造商不太可能採用這種設計。維特里默樹脂製造廠需要5000萬美元的投資,這筆資金只有大型綜合樹脂公司才能負擔得起,因此短期內將減緩其普及速度。

細分市場分析

受摩擦材料和電動車馬達外殼需求的推動,預計到2025年,酚醛樹脂將佔據熱固性模塑化合物市場28.02%的佔有率。隨著符合排放氣體法規的產品被廣泛應用於家用電器內部組件,酚醛樹脂熱固性模塑化合物的市場規模預計將逐步擴大。環氧樹脂市場領先,預計到2031年將以7.02%的複合年成長率成長,這主要得益於人工智慧半導體封裝和15兆瓦級風力渦輪機葉片外殼的需求。聚酯基模塑化合物在注重成本的衛浴設備領域發展滯後,而三聚氰胺和脲類衍生物則因排放法規日益嚴格而市場佔有率下滑。

環氧樹脂生產商正在研發玻璃化轉變溫度 (Tg) 達到 150 度C或更高、吸濕率低於 1% 的環烷基樹脂,以滿足 AI 加速劑的要求。預計到 2024 年,中國酚醛樹脂產量將超過 160 萬噸,其中山東盛泉以 25% 的市佔率位居榜首,凸顯了亞洲的成本優勢。乙烯基酯和鄰苯二甲酸二烯丙酯等小眾體系分別應用於耐腐蝕和高壓絕緣領域,價格高出 2-5 倍。熱固性模塑膠產業在容不得半點差錯的領域承擔了這部分成本。

區域分析

預計到2025年,亞太地區將佔熱固性模塑膠市場收入的45.72%,並在2031年之前以7.43%的複合年成長率成長,這主要得益於中國400萬噸環氧樹脂產能和離岸風力發電設施的蓬勃發展。印度的反傾銷稅正在刺激國內樹脂項目的發展,這些項目與一項價值1.4兆美元的基礎設施計劃相關。日本汽車製造商正在採用PM-5700酚醛樹脂化合物製造電動車零件,目標是到2030年實現1,300萬美元的銷售額。儘管韓國的長纖維熱塑性塑膠計畫顯示其面臨替代品的威脅,但由於強制性的阻燃要求,該地區的熱固性模塑膠市場仍保持強勁勢頭。

在北美,由於美國對中國環氧樹脂徵收反傾銷稅,供應緊張,迫使採購轉向墨西哥和加拿大,但國內產能仍僅為先前進口水準的40%。海克塞爾預計2025年銷售額將達到18.9億美元,顯示航太領域的需求強勁;同時,阿科瑪位於肯塔基州的Foran 1233zd工廠為美國的風力渦輪機葉片回收計畫提供支援。

在歐洲,甲醛含量0.1ppm(百萬分之一)的閾值與70%的複合材料回收義務之間的平衡,迫使現有的酚醛樹脂生產商在創新或退出市場之間做出選擇。德國和丹麥正面臨刀片廢棄物激增的問題,加速了玻璃態聚合物的研究合作。南美洲以及中東和非洲地區雖然規模較小,但成長勢頭強勁,正致力於開發用於石油化工和水利基礎設施的耐腐蝕乙烯基酯樹脂。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 在電氣和電子領域不斷擴大應用

- 促進汽車和航太領域的減重

- 對可再生能源的綜合需求快速成長

- 採用高耐久性複合材料製成的預製基礎設施。

- 反傾銷稅實施後各地區環氧樹脂產能擴張情形

- 用於可回收性的動態共用鍵結/玻璃態聚合物技術

- 市場限制因素

- 可回收性低/處置成本高

- 甲醛類化合物的健康、安全與環境風險

- 貿易保護主義壁壘導致供應鏈中斷

- 新興的熱塑性複合材料正在蠶食低溫應用市場的佔有率。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 環氧樹脂

- 酚醛樹脂

- 聚酯纖維

- 三聚氰胺和甲醛

- 尿素甲醛

- 其他熱固性樹脂

- 按類型分類的纖維增強材料

- 玻璃纖維

- 碳纖維

- 其他增強材料

- 透過使用

- 電氣和電子設備

- 車

- 航太

- 建造

- 消費品

- 其他用途

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- Strategic Developments

- 市佔率(%)/排名分析

- 公司簡介

- Arkema

- Ashland

- BASF

- Chang Chun Group

- Core Molding Technologies

- CSP

- DIC Corporation

- Hexcel Corporation

- Hexion Inc.

- Huntsman

- IDI Composites International

- Menzolit

- Mitsubishi Gas Chemical Next Company, Inc.

- Momentive

- Owens Corning

- Plenco

- Polynt SpA

- POLYTEC HOLDING AG

- Resonac Holdings Corporation

- Scott Bader Company Ltd

- Sumitomo Bakelite Co., Ltd.

- Toray Advanced Composites

第7章 市場機會與未來展望

According to Mordor Intelligence, the thermoset molding compound market size is projected to be USD 11.88 billion in 2025, USD 12.67 billion in 2026, and reach USD 17.45 billion by 2031, growing at a CAGR of 6.62% from 2026 to 2031.

This report is Segmented by Resin Type (Epoxy, Melamine Formaldehyde, Urea Formaldehyde, and More), Fiber Reinforcement (Glass Fiber, Carbon Fiber, and More), Application (Electrical and Electronics, Automotive, Aerospace, Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Thermoset Molding Compound Market Trends and Insights

Growing Use in Electrical and Electronics

Thermal-management requirements for 800-volt EV inverters and 5G base stations are driving epoxy specifications toward thermal conductivities above 0.80 W/m/K and dielectric constants below 4.0. Hybrid hBN-AlN filler systems now deliver UL 94 V-0 flame ratings without halogens, supporting data-center power supplies that must pass 105°C continuous-use tests. China's printed-circuit-board output is forecast to hit USD 54.6 billion by 2026, sustaining epoxy demand for FR-4 and high-frequency laminates. Semiconductor packaging for AI accelerators increasingly favors cycloaliphatic epoxies with glass-transition temperatures above 150°C, eroding phenolic share. Shorter qualification cycles, now under 12 months, reward suppliers offering digital simulation and in-house rapid prototyping capabilities.

Automotive and Aerospace Lightweighting Push

European fleet CO2 ceilings of 95 g/km are compelling OEMs to shift brackets, crossbeams, and battery enclosures from steel to glass-fiber phenolic and carbon-fiber epoxy, trimming vehicle mass by up to 50%. BASF's spray transfer molding process enables Class-A body panels in 3-minute cycles, eliminating paint-bake ovens and cutting energy usage 40%. In aerospace, HexPly M51 prepreg cures in 40 minutes at 180°C, reducing autoclave energy 30% and unlocking single-shift throughput. Korea's supply chain is piloting glass-mat thermoplastic bumper beams that threaten phenolic sheet-molding compounds in non-structural zones. Across mobility platforms, lightweighting ties directly to regulatory credits and extended battery range, enhancing the thermoset molding compound market value proposition.

Poor Recyclability and End of Life Costs

Irreversible cross-linking confines most thermoset scrap to landfill or costly pyrolysis, where gate fees run USD 200-400 per tonne, double virgin material value. EU Directive 2018/851 targets 70% composite recovery by 2030, yet mechanical grinding downgrades materials to low-value fillers. A single 3-MW wind turbine yields 20 tonnes of blade waste, and Europe expects 14,000 blade retirements, straining landfill space in Germany and Denmark. Design-for-disassembly adds USD 50-100 per vehicle in labor, discouraging OEM adoption unless extended producer responsibility regimes expand. Vitrimer plants require USD 50 million investment, affordable only for integrated resin majors, slowing near-term penetration.

Other drivers and restraints analyzed in the detailed report include:

- Renewable Energy Composite Demand Surge

- Infrastructure Prefabs Adopting High Durability Compounds

- Formaldehyde Based Compound HSE Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Phenolic resins delivered 28.02% of the Thermoset Molding Compound market share in 2025 on the back of friction materials and EV motor housings. The Thermoset Molding Compound market size for phenolics is projected to advance modestly as emission-controlled variants secure appliance interiors. Epoxy is pacing ahead at a 7.02% CAGR through 2031 on demand for AI semiconductor packaging and 15-MW wind-blade skins. Polyester BMC trails in cost-sensitive sanitary ware, while melamine and urea derivatives fade under emission scrutiny.

Epoxy formulators are commercializing cycloaliphatic grades with Tg above 150°C and 1% moisture uptake, aligning with AI accelerator packages. China's phenolic output surpassed 1.60 million tons in 2024, led by Shandong Shengquan with 25% share, underscoring Asia's cost edge. Niche systems such as vinyl-ester and diallyl phthalate occupy corrosion-resistant and high-voltage insulation segments, respectively, at 2-5X price premiums, which the thermoset molding compound industry absorbs where failure is not an option.

Geography Analysis

Asia-Pacific anchored 45.72% of the Thermoset Molding Compound market revenue in 2025 and is projected to rise at a 7.43% CAGR to 2031, propelled by China's 4.0 million-ton epoxy capacity and surging offshore wind installations. Indian anti-dumping duties are catalyzing domestic resin projects linked to a USD 1.4 trillion infrastructure pipeline. Japanese OEMs are adopting PM-5700 phenolic compounds in EV gears, targeting USD 13 million sales by 2030. Korean programs around long-fiber thermoplastics signal emerging substitution threats, yet the thermoset molding compound market in the region remains resilient on mandated flame performance.

North America faces supply tightness after U.S. anti-dumping margins on Chinese epoxy, shifting procurement to Mexico and Canada, while domestic capacity lags 40% below prior import volumes. Hexcel's USD 1.89 billion sales in 2025 underscore aerospace pull, and Arkema's Kentucky Forane 1233zd plant backs domestic wind-blade recyclability initiatives.

Europe balances 0.1 ppm (parts per million) formaldehyde thresholds with 70% composite recycling mandates, pressuring phenolic incumbents to innovate or exit. Germany and Denmark confront blade-waste surges, accelerating vitrimer research collaborations. South America and Middle East-Africa remain smaller but growth-oriented, emphasizing corrosion-resistant vinyl-ester systems for petrochemical and water infrastructure.

- Arkema

- Ashland

- BASF

- Chang Chun Group

- Core Molding Technologies

- CSP

- DIC Corporation

- Hexcel Corporation

- Hexion Inc.

- Huntsman

- IDI Composites International

- Menzolit

- Mitsubishi Gas Chemical Next Company, Inc.

- Momentive

- Owens Corning

- Plenco

- Polynt SpA

- POLYTEC HOLDING AG

- Resonac Holdings Corporation

- Scott Bader Company Ltd

- Sumitomo Bakelite Co., Ltd.

- Toray Advanced Composites

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing use in electrical and electronics

- 4.2.2 Automotive and aerospace lightweighting push

- 4.2.3 Renewable-energy composite demand surge

- 4.2.4 Infrastructure prefabs adopting high-durability compounds

- 4.2.5 Regional epoxy capacity build-up post anti-dumping duties

- 4.2.6 Dynamic-covalent/vitrimer technologies enabling recyclability

- 4.3 Market Restraints

- 4.3.1 Poor recyclability/end-of-life costs

- 4.3.2 Formaldehyde-based compound HSE risks

- 4.3.3 Protectionist trade barriers disrupting supply chains

- 4.3.4 Emergent thermoplastic composites cannibalising low-temperature uses

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Phenolic

- 5.1.3 Polyester

- 5.1.4 Melamine Formaldehyde

- 5.1.5 Urea Formaldehyde

- 5.1.6 Other Thermoset Resins

- 5.2 By Fiber Reinforcement

- 5.2.1 Glass Fiber

- 5.2.2 Carbon Fiber

- 5.2.3 Other Reinforcements

- 5.3 By Application

- 5.3.1 Electrical and Electronics

- 5.3.2 Automotive

- 5.3.3 Aerospace

- 5.3.4 Construction

- 5.3.5 Consumer Goods

- 5.3.6 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Strategic Developments

- 6.2 Market Share(%)/ Ranking Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Arkema

- 6.3.2 Ashland

- 6.3.3 BASF

- 6.3.4 Chang Chun Group

- 6.3.5 Core Molding Technologies

- 6.3.6 CSP

- 6.3.7 DIC Corporation

- 6.3.8 Hexcel Corporation

- 6.3.9 Hexion Inc.

- 6.3.10 Huntsman

- 6.3.11 IDI Composites International

- 6.3.12 Menzolit

- 6.3.13 Mitsubishi Gas Chemical Next Company, Inc.

- 6.3.14 Momentive

- 6.3.15 Owens Corning

- 6.3.16 Plenco

- 6.3.17 Polynt SpA

- 6.3.18 POLYTEC HOLDING AG

- 6.3.19 Resonac Holdings Corporation

- 6.3.20 Scott Bader Company Ltd

- 6.3.21 Sumitomo Bakelite Co., Ltd.

- 6.3.22 Toray Advanced Composites

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

熱塑性複合材料市場:依產品形式、纖維類型、樹脂類型、製造流程、終端應用產業及銷售管道分類-2026-2032年全球市場預測

熱塑性複合材料市場:依產品形式、纖維類型、樹脂類型、製造流程、終端應用產業及銷售管道分類-2026-2032年全球市場預測 熱塑性複合材料市場報告:按纖維類型、產品類型、樹脂類型、終端應用產業和地區分類(2026-2034 年)

熱塑性複合材料市場報告:按纖維類型、產品類型、樹脂類型、終端應用產業和地區分類(2026-2034 年) 熱塑性複合材料市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測

熱塑性複合材料市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測 2026年全球熱塑性複合材料市場報告工業用聚四氟乙烯複合材料市場(依複合材料類型、加工方法、形態、應用和最終用途產業分類)-2026-2032年全球預測氧化鋯陶瓷連續纖維市場:依纖維類型、等級、銷售管道、應用和最終用途產業分類-全球預測,2026-2032年熱可塑性橡膠化合物市場按產品類型、形態、應用和分銷管道分類-2026-2032年全球預測

2026年全球熱塑性複合材料市場報告工業用聚四氟乙烯複合材料市場(依複合材料類型、加工方法、形態、應用和最終用途產業分類)-2026-2032年全球預測氧化鋯陶瓷連續纖維市場:依纖維類型、等級、銷售管道、應用和最終用途產業分類-全球預測,2026-2032年熱可塑性橡膠化合物市場按產品類型、形態、應用和分銷管道分類-2026-2032年全球預測 熱固性模塑材料市場規模、佔有率及成長分析(依樹脂類型、成型類型、最終用途產業及地區分類)-2026-2033年產業預測

熱固性模塑材料市場規模、佔有率及成長分析(依樹脂類型、成型類型、最終用途產業及地區分類)-2026-2033年產業預測 熱塑性複合材料市場規模、佔有率和成長分析(按樹脂類型、纖維類型、產品類型、最終用途產業和地區分類)-2026年至2033年產業預測

熱塑性複合材料市場規模、佔有率和成長分析(按樹脂類型、纖維類型、產品類型、最終用途產業和地區分類)-2026年至2033年產業預測 氧化鋁纖維和氧化鋁連續纖維:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

氧化鋁纖維和氧化鋁連續纖維:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)