|

市場調查報告書

商品編碼

2062291

矽橡膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Silicone Elastomers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

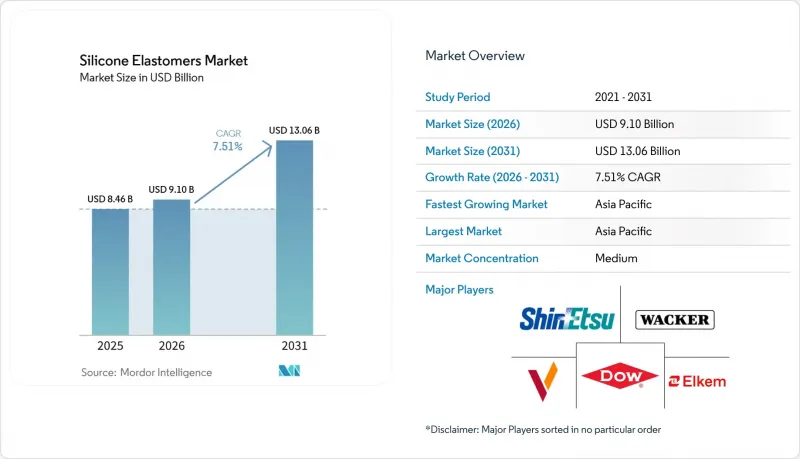

據 Mordor Intelligence 稱,2025 年矽橡膠市場價值為 84.6 億美元,預計到 2031 年將達到 130.6 億美元,而 2026 年為 91 億美元,預測期(2026-2031 年)的複合年成長率為 7.51%。

本報告按產品類型(高溫硫化膠 (HTV)、室溫硫化膠 (RTV) 等)、應用領域(電氣電子、汽車及交通運輸、工業機械、消費品、建築及其他)和地區(亞太、北美、歐洲、南美以及中東和非洲)進行細分。市場預測以美元計價。

全球矽橡膠市場趨勢及洞察

5G電子設備小型化和溫度控管

隨著第五代基地台和人工智慧加速器對更高功率密度的需求不斷成長,對高導熱矽導熱介面材料的需求變得至關重要。陶氏化學的DOWSIL TC-5550和瓦克化學的SEMICOSIL 9649 TC均能滿足這些要求。此外,這些材料還具有優異的電絕緣性能,並能承受寬廣的溫度循環。透過以氮化硼和石墨烯取代氧化鋁填料,製造商顯著降低了材料的熱阻。這項技術進步正在推動被動散熱解決方案在緊湊型家用電子電器和汽車電子產品的應用。同時,信越化學在中國平湖新建了一座工廠。該生產線專為滿足半導體封裝所需的嚴格離子純度標準而設計,這凸顯了該地區在高純度供應鏈中日益成長的重要性。

醫用LSR在穿戴式醫療設備的應用

在連續血糖監測儀、心臟貼片和藥物傳輸系統等設備中,製造商正逐步從熱可塑性橡膠轉向液態矽橡膠。液態矽橡膠不僅符合 ISO 10993 標準,而且可長時間接觸皮膚而不會引起刺激。杜邦公司推出了「Liveo C6-8XX」系列產品,該系列產品具有多種硬度和較長的適用期,可顯著減少自動化生產線的成型停機時間。同時,Elchem 公司的液態矽橡膠「SILBIONE EC 70」利用奈米碳管實現導電性,可用於製造心電圖貼片的乾電極。這項創新無需在使用前進行皮膚準備,簡化了臨床工作流程。

矽氧烷原料供應鏈的波動

金屬矽價格從年初到年末大幅上漲。此次上漲是由於伊朗甲醇供應中斷以及山東省一家工廠爆炸,導致二甲基二氯矽烷產能下降。未整合上游工程的歐洲加工企業利潤率大幅下滑,而整合了上游工程的企業則受惠於原物料成本降低,實現了營業利潤的回升。

細分市場分析

至2025年,液態矽橡膠將佔據矽橡膠市場45.22%的佔有率,預計2026年至2031年間,其市佔率將以8.34%的複合年成長率成長。其低粘度使其能夠快速完成自動化射出成型循環,並實現精確的公差控制。這種精度對於大批量生產的穿戴式設備和電動汽車感測器至關重要。杜邦公司的「Liveo C6-8XX」和Elchem公司的導電型「SILBIONE」液態矽橡膠均具有功能增強特性,從而維持了液態矽橡膠的競爭優勢。高溫硫化型液態矽橡膠對於需要高工作溫度和優異撕裂強度的應用至關重要,例如渦輪增壓器軟管和電線絕緣。另一方面,室溫硫化型矽橡膠則較適用於現場施工密封劑。它們在室溫下即可固化,並且揮發性有機化合物(VOC)排放極低。

液態矽橡膠在消費品領域的應用日益廣泛。奶瓶奶嘴、烤箱墊和個人護理刷等產品均受益於符合食品級標準的液態矽橡膠,確保高壓釜後不影響產品口感,並保持其耐用性。以瓦克公司的ELASTOSIL R 531/60為代表的經陶瓷化處理的液態矽橡膠,如今正被用於保護電動車匯流排免受熱失控的影響,凸顯了矽橡膠在下一代電池安全方面發揮的關鍵作用。

區域分析

亞太地區將引領矽橡膠市場,預計到2025年將佔據46.67%的市場佔有率,並預計在2026年至2031年間以8.11%的複合年成長率成長。信越化學對其平湖工廠的投資以及瓦克化學對其張家港工廠的擴建,均是為配合中國、印度和東南亞電子及電動汽車行業的快速成長而精心策劃的。中國政策主導的產業整合預計將顯著提高產能運轉率,從而導致上游供應趨緊,企業定價權增強。

北美已佔據顯著的市場佔有率。杜邦公司位於密西根州海姆洛克的工廠正在擴大醫用級液態矽橡膠的生產,以滿足生物製藥行業和日益成長的穿戴式設備市場的一次性使用需求。同時,矽橡膠密封件對於承受低於環境溫度的乙二醇循環系統至關重要,其在美國資料中心建置中的應用也日益廣泛。此外,墨西哥汽車產業的近岸外包趨勢正在將矽橡膠混煉業務集中在汽車組裝廠附近,從而增強了該地區的經濟韌性。

在歐洲,矽氧烷市場佔據了較大的市場佔有率,目前呈現溫和成長態勢。然而,監管限制增加了配方變更的成本。儘管如此,由於歐洲大陸大力推行淨零排放建築標準以及汽車電氣化進程加速,市場需求仍然強勁。特別是,西卡公司的「Sikasil WS-605 S」矽氧烷正被應用於眾多興建中的淨零排放高層建築。然而,隨著陶氏化學計劃關閉其位於英國巴里的工廠,預計當地的矽氧烷供應將趨於緊張,迫使加工商在亞洲尋找更全面的供應來源。

南美洲和中東/非洲地區合計僅佔全球矽酮消費量的一小部分。然而,巴西大力發展電動車以及沙烏地阿拉伯雄心勃勃的大型企劃「NEOM」正在大力推廣矽酮密封劑,這種密封劑以其能夠承受沙漠酷熱和沙礫侵蝕的能力而聞名,因此,這些地區正成為重要的成長區域。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 5G電子設備小型化和溫度控管

- 穿戴式醫療保健領域中醫療級LSR的應用

- 零能耗建築中的建築密封劑

- 矽膠零件的積層製造(3D/LAM)

- 用於衛生電子電氣應用的抗菌導電液態矽橡膠

- 市場限制因素

- 矽氧烷原料供應鏈的波動

- 使用高性能TPE作為替代品的風險

- 歐盟REACH法規關於環狀矽氧烷和重組成本的規定

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依產品

- 高溫硫化(HTV)

- 室溫硫化(RTV)

- 液態矽橡膠(LSR)

- 透過使用

- 電氣和電子設備

- 汽車和運輸業

- 工業機械

- 消費品

- 建造

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 泰國

- 越南

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Avantor, Inc.

- Bentec Medical

- Cabot Corporation

- China National Bluestar(Group)Co., Ltd.

- CHT Germany GmbH

- Dow

- DuPont

- Elkem ASA

- KCC Silicone Corporation

- Mesgo SpA

- Momentive

- Primasil Silicones Limited

- Reiss Manufacturing, Inc.

- Rogers Corporation

- Saint-Gobain

- Shin-Etsu Chemical Co., Ltd.

- Specialty Silicone Products, Inc.

- Stockwell Elastomerics

- Wacker Chemie AG

- Wynca Group

第7章 市場機會與未來展望

According to Mordor Intelligence, the silicone elastomers market size was valued at USD 8.46 billion in 2025 and is estimated to grow from USD 9.10 billion in 2026 to reach USD 13.06 billion by 2031, at a CAGR of 7.51% during the forecast period (2026-2031).

This report is Segmented by Product (High-Temperature Vulcanised (HTV), Room-Temperature Vulcanised (RTV), and More), Application (Electrical and Electronics, Automotive and Transportation, Industrial Machinery, Consumer Goods, Construction, Others), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Silicone Elastomers Market Trends and Insights

Electronics Miniaturization and 5G Thermal Management

As the demand for higher power densities increases in fifth-generation base stations and artificial intelligence accelerators, the requirement for silicone thermal-interface materials with advanced conductivity has become critical. Dow's DOWSIL TC-5550 and Wacker's SEMICOSIL 9649 TC meet these requirements. Additionally, these materials ensure excellent electrical insulation and can withstand a wide range of temperature cycles. By substituting alumina fillers with boron nitride and graphene, manufacturers have significantly reduced thermal resistance. This development supports the adoption of passive cooling solutions in both compact consumer electronics and automotive electronics. Meanwhile, Shin-Etsu has established a new facility in Pinghu, China. This line is specifically designed to meet the stringent ionic purity standards essential for semiconductor packaging, highlighting the region's growing importance in the high-purity supply chain.

Medical-Grade LSR Adoption in Wearable Healthcare

Manufacturers are transitioning from thermoplastic elastomers to liquid silicone rubber for devices like continuous glucose monitors, cardiac patches, and drug-delivery systems. Liquid silicone rubber not only complies with ISO 10993 standards but also allows for extended skin contact without irritating. DuPont introduced its Liveo C6-8XX series, offering a range of hardness and an extended pot life, significantly reducing molding downtime on automated lines. Meanwhile, Elkem's SILBIONE liquid silicone rubber EC 70 incorporates carbon-nanotube conductivity, enabling the creation of dry electrodes for electrocardiogram patches. This innovation eliminates the need for pre-use skin preparation and streamlines clinical workflows.

Siloxane Feedstock Supply-Chain Volatility

Metal silicon prices experienced a significant increase from the beginning to the latter part of the year. This rise was driven by disruptions in methanol supply from Iran and an explosion at a plant in Shandong, which collectively reduced the production capacity of dimethyldichlorosilane. Non-integrated European converters faced a notable decline in margins, while a company with upstream integration benefited from reduced feedstock costs and achieved a recovery in operating profit.

Other drivers and restraints analyzed in the detailed report include:

- Construction Sealants in Net-Zero Buildings

- Additive Manufacturing of Silicone Parts (3-D/LAM)

- EU REACH Cyclic-Siloxane Restrictions and Reformulation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid Silicone Rubber captured 45.22% silicone elastomer market share in 2025, and its slice of the silicone elastomer market size is forecast to widen at an 8.34% CAGR through 2026 to 2031. With a low viscosity, automated injection cycles can be completed quickly, achieving precise tolerances. This precision is vital for high-volume wearables and sensors in electric vehicles. DuPont's Liveo C6-8XX and Elkem's conductive SILBIONE liquid silicone rubber showcase functional enhancements that maintain the competitive edge of liquid silicone rubber. High-temperature vulcanized grades are crucial for applications demanding high service temperatures or significant tear strength, such as in turbocharger hoses and wire insulation. Meanwhile, room-temperature vulcanized silicone is preferred for on-site construction sealants, curing at ambient conditions and boasting ultra-low volatile organic compound emissions.

Liquid silicone rubber's growing prominence is evident in consumer products. Items like bottle nipples, baking mats, and personal-care brushes benefit from liquid silicone rubber's compliance with food-grade standards, ensuring taste neutrality and durability through autoclaving. Ceramifying liquid silicone rubber, exemplified by Wacker ELASTOSIL R 531/60, is now safeguarding electric vehicle busbars from thermal runaway, highlighting silicone's pivotal role in the safety of next-generation batteries.

Geography Analysis

Asia-Pacific dominated the silicone elastomer market with a 46.67% share in 2025 and is projected to compound at 8.11% through 2026 to 2031. Shin-Etsu's investment in its Pinghu plan and Wacker's expansion at Zhangjiagang are strategically timed with the burgeoning electronics and electric vehicle sectors in China, India, and Southeast Asia. Thanks to policy-driven consolidation in China, utilization rates are projected to significantly increase, tightening upstream supply and bolstering pricing power.

North America secured a notable share of the market. DuPont's Hemlock site in Michigan is ramping up production of medical-grade liquid silicone rubber to cater to the biopharmaceutical sector's single-use needs and the growing wearables market. Simultaneously, United States data-center constructions are increasingly opting for silicone seals, crucial for enduring sub-ambient glycol loops. Meanwhile, Mexico's automotive nearshoring trend is pulling silicone compounding operations closer to vehicle assembly hubs, bolstering the region's economic resilience.

Europe, holding a significant market share, is witnessing modest growth. However, regulatory constraints are inflating reformulation costs. Despite this, the continent's commitment to net-zero building codes and a push towards automotive electrification are keeping demand robust. Notably, Sika's Sikasil WS-605 S is being utilized in numerous net-zero towers currently under construction. Yet, with Dow planning to shutter its Barry, United Kingdom site, the local merchant siloxane supply is set to tighten, nudging converters to seek integrated sources in Asia.

South America and the combined regions of the Middle East and Africa account for a smaller portion of global silicone consumption. Brazil's push towards electric vehicles and Saudi Arabia's ambitious NEOM megaproject are emerging as significant growth areas, capitalizing on silicone sealants renowned for withstanding the desert's scorching heat and abrasive sand.

- Avantor, Inc.

- Bentec Medical

- Cabot Corporation

- China National Bluestar (Group) Co., Ltd.

- CHT Germany GmbH

- Dow

- DuPont

- Elkem ASA

- KCC Silicone Corporation

- Mesgo S.p.A.

- Momentive

- Primasil Silicones Limited

- Reiss Manufacturing, Inc.

- Rogers Corporation

- Saint-Gobain

- Shin-Etsu Chemical Co., Ltd.

- Specialty Silicone Products, Inc.

- Stockwell Elastomerics

- Wacker Chemie AG

- Wynca Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electronics miniaturisation and 5G thermal management

- 4.2.2 Medical-grade LSR adoption in wearable healthcare

- 4.2.3 Construction sealants in net-zero buildings

- 4.2.4 Additive manufacturing of silicone parts (3-D/LAM)

- 4.2.5 Antimicrobial and conductive LSR for hygienic EandE uses

- 4.3 Market Restraints

- 4.3.1 Siloxane feedstock supply-chain volatility

- 4.3.2 Substitution risk from high-performance TPEs

- 4.3.3 EU REACH cyclic-siloxane restrictions and reformulation cost

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of Substitution

- 4.5.4 Threat of New Entrants

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 High-Temperature Vulcanised (HTV)

- 5.1.2 Room-Temperature Vulcanised (RTV)

- 5.1.3 Liquid Silicone Rubber (LSR)

- 5.2 By Application

- 5.2.1 Electrical and Electronics

- 5.2.2 Automotive and Transportation

- 5.2.3 Industrial Machinery

- 5.2.4 Consumer Goods

- 5.2.5 Construction

- 5.2.6 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Australia

- 5.3.1.6 Indonesia

- 5.3.1.7 Thailand

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Avantor, Inc.

- 6.4.2 Bentec Medical

- 6.4.3 Cabot Corporation

- 6.4.4 China National Bluestar (Group) Co., Ltd.

- 6.4.5 CHT Germany GmbH

- 6.4.6 Dow

- 6.4.7 DuPont

- 6.4.8 Elkem ASA

- 6.4.9 KCC Silicone Corporation

- 6.4.10 Mesgo S.p.A.

- 6.4.11 Momentive

- 6.4.12 Primasil Silicones Limited

- 6.4.13 Reiss Manufacturing, Inc.

- 6.4.14 Rogers Corporation

- 6.4.15 Saint-Gobain

- 6.4.16 Shin-Etsu Chemical Co., Ltd.

- 6.4.17 Specialty Silicone Products, Inc.

- 6.4.18 Stockwell Elastomerics

- 6.4.19 Wacker Chemie AG

- 6.4.20 Wynca Group

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

矽橡膠市場-2026-2032年全球市場預測

矽橡膠市場-2026-2032年全球市場預測 全球矽橡膠市場:按類型、製程、終端應用產業及地區分類-預測至2031年

全球矽橡膠市場:按類型、製程、終端應用產業及地區分類-預測至2031年 矽橡膠市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年

矽橡膠市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年 矽橡膠市場:依產品類型、應用、終端用戶產業及地區分類

矽橡膠市場:依產品類型、應用、終端用戶產業及地區分類 矽橡膠市場規模、佔有率和成長分析:按類型、製造流程、形態、應用、終端用戶產業和地區分類-2026-2033年產業預測

矽橡膠市場規模、佔有率和成長分析:按類型、製造流程、形態、應用、終端用戶產業和地區分類-2026-2033年產業預測 全球矽橡膠市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球矽橡膠市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球矽橡膠市場報告

2026年全球矽橡膠市場報告 全球矽橡膠市場,2026-2030年

全球矽橡膠市場,2026-2030年 矽橡膠市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年)日本矽橡膠市場報告(依產品(高溫硫化、常溫硫化、液態矽橡膠)、應用與地區分類,2026-2034年)

矽橡膠市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年)日本矽橡膠市場報告(依產品(高溫硫化、常溫硫化、液態矽橡膠)、應用與地區分類,2026-2034年)