|

市場調查報告書

商品編碼

2062290

醋酸乙烯酯聚合物乳劑:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Vinyl Acetate Homopolymer Emulsion - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

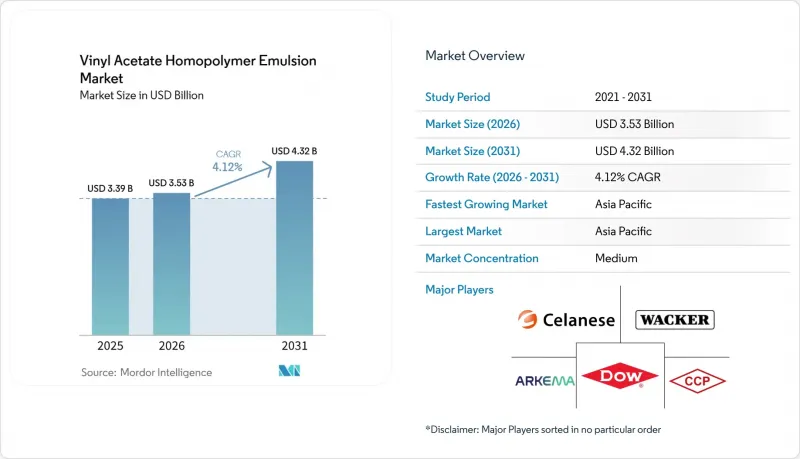

預計醋酸乙烯酯聚合物乳劑市場將從 2025 年的 33.9 億美元和 2026 年的 35.3 億美元成長到 2031 年的 43.2 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 4.12%。

本報告按應用領域(油漆和塗料、黏合劑等)、終端用戶產業(建築和施工、包裝、汽車和運輸以及其他終端用戶產業)和地區(亞太地區、北美地區、歐洲地區、南美地區以及中東和非洲地區)進行細分。市場預測以美元計價。

全球醋酸乙烯聚合物乳劑市場趨勢及洞察

低VOC塗料和油漆的監管趨勢

2026年6月1日,中國實施了GB 30981.1-2025和GB 30981.2-2025標準,加強了對甲醛、重金屬、芳香族化合物和揮發性有機化合物(VOCs)的限制。同時,GB 37824-2019標準要求大幅降低參考區域內超過特定閾值的非甲烷烴排放。這些法規迫使配方設計人員轉向水性體系。在這方面,醋酸乙烯聚合物乳劑無需昂貴的熱氧化設備即可確保合規性。歐洲也出現了類似的趨勢,對全氟烷基和多氟烷基物質的監管範圍擴大,揮發性有機化合物的排放標準降低。同時,美國環保署(EPA)的氣霧劑塗料法規將於2027年初到期。在全球範圍內,下游用戶優先選擇不含芳香族化合物且殘留單體含量極低的黏合劑。這一趨勢為提供預先認證和受監管等級產品的供應商創造了競爭優勢。更嚴格的法規正在加速工業金屬和塑膠塗料領域從高固態含量溶劑體係轉向水性系統的轉變。這種轉變正在擴大醋酸乙烯酯聚合物乳劑的市場。尤其是在亞太地區,許多塗料生產商在採購決策中優先考慮“符合水性塗料法規”,這凸顯了政策對採購選擇的影響。

亞洲和歐洲紙張和衛生紙生產的擴張

都市化和衛生用品的廣泛使用正推動中國、印度和東南亞國協紙巾產能的顯著擴張。醋酸乙烯酯聚合物乳劑以其均勻的成膜性和強附著力而著稱,在高速塗佈機中備受青睞,並且與苯乙烯-丙烯酸類粘合劑相比,仍然是一種經濟高效的替代方案。在歐洲,隨著造紙企業從印刷紙生產線轉向可回收包裝紙生產線,對具有客製化流變性能的低氣味黏合劑的需求激增。近期推出的產品凸顯了衛生、包裝和可回收性三大優先事項的整合。這項創新使得熱敏性零食和糖果甜點的包裝從傳統塑膠轉向更永續的阻隔塗層紙。這些阻隔塗佈產品通常採用醋酸乙烯酯均聚物聚合物乳劑。這些乳液不僅能與礦物或奈米纖維素添加劑良好配合,而且還具有對水性食品模擬物的耐受性,與溶劑型系統相比,提供了更大的配方柔軟性。這形成了一個良性循環。隨著紙漿產量的擴大,塗料需求也隨之增加,塗料技術的創新進一步加劇了紙張和柔軟性塑膠之間的競爭。

VAM原物料價格波動

由乙烯和乙酸製取的醋酸乙烯單體的成本與原油和天然氣等上游基準價格密切相關,而這些價格的季度波動幅度很大。台灣和美國主要醋酸乙烯單體生產廠的停產導致現貨價格飆升,凸顯了該產業對意外停產的脆弱性。區域價格差異,加上運輸瓶頸和關稅變化的影響,迫使亞洲乳液生產商在國產乙烯和進口乙烯之間艱難權衡。這種價格波動不僅降低了固定價格合約的利潤率,也使成本加成定價模式更加複雜,對中小規模的混煉生產商構成了特別嚴峻的挑戰。雖然像Serenes和Wacker這樣的大型企業已經後向整合了醋酸乙烯單體產能和乙烯供應鏈,減輕了部分價格波動的影響,但它們仍在年度報告中承認,原料價格波動對其盈利能力構成重大風險。為此,採購部門正在努力實現供應來源多元化,並確保長期乙烯互換協議,但同時也意識到此類避險交易涉及額外的管理費用和交易對手風險。

細分市場分析

塗料產業對總銷售額貢獻顯著,預計到2025年將佔總銷售額的36.22%,鞏固其在醋酸乙烯酯聚合物乳劑應用領域的市場領先地位。在該領域,建築塗料配方佔據主導地位,這主要得益於中國向水性體系的轉變以及歐洲日益嚴格的VOC法規。同期,採用共聚單體接枝技術的高性能乳液預計將逐步從溶劑型工業塗料中奪取市場佔有率,並擴大其應用範圍。

不織布應用預計初期市場規模相對較小,但預計2026年至2031年間將以4.22%的複合年成長率成長。衛生用品製造商越來越青睞醋酸乙烯酯均聚物黏合劑,因為它們氣味低、質地柔軟。尤其是在東南亞,許多大型尿布製造商都認可本地供應的產品。同時,黏合劑市場也呈現穩定成長態勢。這主要得益於可回收單一材料包裝的普及,從而增加了對可重複密封和冷封系統的需求。這些系統依賴高黏度均聚物分散體。雖然紡織品和其他應用在整體價值中所佔比例較小,但它們是數位印刷黏合劑和特殊密封劑的重要試驗場。這些領域的成功創新往往轉化為大規模生產,從而確保產品平臺的持續發展。

區域分析

亞太地區仍是需求中心,預計2025年將佔全球銷售額的46.67%,並預計在2026年至2031年間以4.65%的複合年成長率成長。中國在塗料生產領域的領先地位,以及印度衛浴產品生產的蓬勃發展,正在推動市場成長。 Serenes位於南京的工廠擁有大規模的醋酸乙烯單體和醋酸乙烯酯乳液生產能力,是本地化供應策略的典範,該策略對於滿足該地區龐大的消費需求至關重要。監管趨勢,特別是中國的GB 30981系列標準,正在鞏固向水性產品的轉變。同時,東協地區的衛浴產品工廠也提供了進一步的推動力。印度雄心勃勃的住宅供應翻倍目標,支撐了對建築相關塗料的需求。此外,擬議降低水性塗料的商品和服務稅(GST)有望顯著加速其普及。

北美和歐洲合計佔據全球消費的相當大一部分。在美國,環保署對氣霧劑塗料的監管期限,以及各州對揮發性有機化合物(VOC)的監管,正在推動消費品中醋酸乙烯酯均聚物的應用。同時,瓦克公司在肯塔基州的擴張正在加強國內供應鏈。在歐洲,循環經濟的努力正在提振單一材料阻隔應用的需求。阿科瑪對陶氏軟性包裝黏合劑業務的策略性收購,使該公司能夠更好地利用這項政策利好。建築市場已趨於成熟,現有建築的節能維修要求以及對輕量化汽車的關注,將繼續推動該市場保持溫和成長。

儘管南美洲在全球銷售額中所佔比例較小,但它受益於巴西的基礎設施項目和對汽車原始設備製造商 (OEM) 的投資。然而,外匯波動構成挑戰,尤其是在原料進口成本方面。這種不確定性正促使加工商轉向在地採購。為了因應這一趨勢,Synthemar 正在實現產品本地化,將先前從歐洲進口的等級產品轉移到其位於美國和拉丁美洲的工廠生產,從而降低對運輸成本和關稅的依賴。中東和非洲地區雖然絕對規模較小,但在一些地區呈現顯著成長。這種成長在沙烏地阿拉伯和南非等地區尤其明顯,這些地區的住宅政策正在推進,同時可支配收入也在增加,衛生用品的消費量也在成長,但該地區的基數小規模,並且由於聚合產能有限而面臨限制。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 法規轉向低VOC塗料和塗層

- 亞洲和歐洲紙張和衛生紙生產的擴張

- 南亞和東南亞不織布衛生用品產量激增

- 可作為可回收單一材料包裝的功能性阻隔塗層

- 數位印刷用黏合劑乳液的需求

- 市場限制因素

- VAM原物料價格波動

- 與丙烯酸和VAE共聚物乳液的競爭

- 不使用昂貴的交聯劑,難以滿足食品接觸轉移標準。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 透過使用

- 油漆和塗料

- 黏合劑

- 紡織品

- 不織布

- 其他用途(密封劑等)

- 按最終用戶行業分類

- 建築/施工

- 包裝

- 汽車和運輸業

- 其他終端用戶產業(家具、鞋類、紙張和印刷)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Allnex GmbH

- Arkema(Bostik)

- Celanese Corporation

- Chang Chun Group

- Dow

- HB Fuller Company

- Henkel AG & Co. KGaA

- Hexion Inc.

- Kuraray Co., Ltd.

- Shaanxi XuTai Technology Co., Ltd

- Sinopec Sichuan Vinylon Works

- Synthomer plc

- Tailored Adhesives.

- Vinavil SpA

- Wacker Chemie AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the vinyl acetate homopolymer emulsion market size is projected to expand from USD 3.39 billion in 2025 and USD 3.53 billion in 2026 to USD 4.32 billion by 2031, registering a CAGR of 4.12% between 2026 to 2031.

This report is Segmented by Application (Paints and Coatings, Adhesives, and More), End-User Industry (Building and Construction, Packaging, Automotive and Transportation, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Vinyl Acetate Homopolymer Emulsion Market Trends and Insights

Regulatory Shift Toward Low-VOC Paints And Coatings

On June 1, 2026, China enforced its GB 30981.1-2025 and GB 30981.2-2025 regulations, tightening limits on formaldehyde, heavy metals, aromatics, and volatile organic compounds. Concurrently, GB 37824-2019 mandates a significant level of abatement efficiency for non-methane hydrocarbon emissions exceeding a specific threshold in standard regions. These regulations steer formulators towards waterborne systems. Here, vinyl acetate homopolymer emulsions ensure compliance, sidestepping the need for expensive thermal oxidizers. Europe mirrors this trend with expanding bans on per- and polyfluoroalkyl substances and reduced volatile organic compound limits, while the United States sets a deadline in early 2027 for aerosol-coating regulations issued by the Environmental Protection Agency. Across the globe, downstream users prioritize binders devoid of aromatics and with minimal residual monomers. This trend gives a competitive advantage to suppliers who provide pre-qualified, regulation-compliant grades. The tightening regulations are also hastening the shift away from high-solids solvent systems in industrial metal and plastic coatings. This shift broadens the market for vinyl acetate homopolymer emulsions. Notably, a large proportion of Asia-Pacific coating formulators now prioritize "waterborne compliance" in their purchasing decisions, highlighting the influence of policy on procurement choices.

Growing Paper And Tissue Production In Asia And Europe

Urbanization and the increasing adoption of sanitary products are driving significant growth in tissue machine capacity in China, India, and ASEAN. Vinyl acetate homopolymer emulsions, known for their uniform film formation and strong adhesion, are favored by high-speed coaters and remain a cost-effective choice compared to styrene-acrylic alternatives. In Europe, as mills pivot from graphic-paper lines to recyclable packaging grades, there is a surge in demand for low-odor binders with customized rheology. A recent product launch highlights the merging priorities of hygiene, packaging, and recyclability. This innovation allows heat-sensitive snacks and confections to transition from traditional plastics to a more sustainable barrier-coated paper. Typically, these barrier-coated formats rely on vinyl acetate homopolymer emulsions. These emulsions not only harmonize with mineral or nanocellulose additives but also resist aqueous food simulants, offering greater formulation flexibility compared to solvent systems. This creates a beneficial cycle: as pulp expansion boosts coating demand, innovations in coating further propel paper's competition with flexible plastics.

VAM Feedstock Price Volatility

Produced from ethylene and acetic acid, the cost of vinyl acetate monomer is closely linked to upstream benchmarks of crude oil and natural gas, which experienced significant quarterly fluctuations. Outages at major vinyl acetate monomer units in Taiwan and the United States caused a significant increase in spot prices, highlighting the industry's susceptibility to unexpected downtimes. Regional price disparities, intensified by freight bottlenecks and tariff changes, compel Asian emulsion producers to navigate a tightrope between domestic and imported ethylene. This price volatility not only diminishes margins on fixed-price contracts but also complicates the cost-plus price pass-through, a challenge especially pronounced for smaller formulators. While major players like Celanese and Wacker, with their backward-linked vinyl acetate monomer capacities and ethylene pipelines, enjoy some insulation from these swings, they still acknowledge feedstock fluctuations as a significant earnings risk in their annual reports. In response, procurement teams are broadening their supply sources and securing longer-term ethylene swap contracts, albeit with the understanding that these hedges introduce additional overhead and counterparty risks.

Other drivers and restraints analyzed in the detailed report include:

- Boom In Non-Woven Hygiene Output Across South And Southeast Asia

- Adoption As Functional Barrier Coatings For Recyclable Mono-Material Packaging

- Competition From Acrylic And VAE Copolymer Emulsions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Paints and Coatings contributed significantly to the overall revenue, equivalent to 36.22% of 2025 revenue, anchoring the vinyl acetate homopolymer emulsion market share lead in applications. Architectural formulations dominate within this slice, buoyed by China's shift to waterborne systems and Europe's tightening VOC ceilings. During the same horizon, performance-grade emulsions with co-monomer grafting are expected to chip away at solvent-borne industrial coatings, broadening the application base.

Non-Woven applications are anticipated to begin from a relatively smaller market base. are forecast to rise at a 4.22% CAGR between 2026 and 2031. Hygiene converters are increasingly favoring vinyl acetate homopolymer binders due to their low-odor profile and softness. Notably, a significant number of leading diaper producers in Southeast Asia have approved grades supplied locally. Meanwhile, the adhesive segment is experiencing steady growth. This is largely driven by a shift towards recyclable mono-material packaging, which has heightened the demand for resealable and cold-seal systems. These systems, in turn, depend on high-tack homopolymer dispersions. Although textile and other applications contribute a smaller share to the overall value, they serve as crucial testing grounds for digital-printing binders and specialty sealants. Innovations that prove successful in these areas often transition to higher-volume segments, ensuring a continuous flow in the product pipeline.

Geography Analysis

Asia-Pacific remains the demand epicenter, accounting for 46.67% of 2025 revenue and expanding at a 4.65% CAGR through 2026 to 2031. China's dominance in coatings volumes, coupled with India's surge in hygiene production, drives the market's momentum. Celanese's Nanjing complex, with significant production capacity for vinyl acetate monomer and vinyl acetate ethylene emulsion, stands as a testament to the localized supply strategies essential for catering to the region's vast consumption. Regulatory momentum, particularly China's GB 30981 series, solidifies the shift towards waterborne products. Meanwhile, hygiene plants in the Association of Southeast Asian Nations region offer an incremental boost. India's ambitious goal to double housing availability anchors the demand for construction-related coatings. Furthermore, a proposed reduction in the goods and services tax on water-based paints could significantly accelerate their adoption.

North America and Europe collectively represent a substantial portion of global spending. In the United States, the Environmental Protection Agency's deadline for aerosol coatings, combined with state-level regulations on volatile organic compounds, promotes the adoption of vinyl acetate homopolymer in consumer goods. Concurrently, Wacker's expansion in Kentucky fortifies the domestic supply chain. Europe's push towards a circular economy fuels demand for mono-material barrier applications. Arkema's strategic acquisition of Dow's flexible-packaging adhesives business positions it to benefit from this policy momentum. Despite the maturity of construction markets, mandates for retrofit energy efficiency and a focus on automotive lightweighting continue to drive modest growth.

While South America accounts for a smaller share of global revenue, it reaps benefits from Brazilian infrastructure projects and investments in original equipment manufacturer automotive. However, currency volatility poses challenges, especially in raw-material import costs. This unpredictability nudges converters towards local sourcing. Responding to this trend, Synthomer has localized its products, transitioning previously imported European grades to its United States and Latin American plants, thereby reducing exposure to freight and duties. The Middle East and Africa, though smaller in absolute size, witness pockets of significant growth. This expansion is particularly notable where Saudi and South African housing initiatives align with a rising disposable income and increased hygiene consumption, albeit starting from a modest base and facing constraints due to limited polymerization capacity.

- Allnex GmbH

- Arkema (Bostik)

- Celanese Corporation

- Chang Chun Group

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hexion Inc.

- Kuraray Co., Ltd.

- Shaanxi XuTai Technology Co., Ltd

- Sinopec Sichuan Vinylon Works

- Synthomer plc

- Tailored Adhesives.

- Vinavil S.p.A.

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory shift toward low-VOC paints and coatings

- 4.2.2 Growing paper and tissue production in Asia and Europe

- 4.2.3 Boom in non-woven hygiene output across South and Southeast Asia

- 4.2.4 Adoption as functional barrier coatings for recyclable mono-material packaging

- 4.2.5 Demand for digital-printing-grade binder emulsions

- 4.3 Market Restraints

- 4.3.1 VAM feed-stock price volatility

- 4.3.2 Competition from acrylic and VAE copolymer emulsions

- 4.3.3 Difficulty meeting food-contact migration limits without costly cross-linkers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Application

- 5.1.1 Paints and Coatings

- 5.1.2 Adhesives

- 5.1.3 Textiles

- 5.1.4 Non-woven

- 5.1.5 Other Applications (Sealants, etc.)

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Packaging

- 5.2.3 Automotive and Transportation

- 5.2.4 Other End-user Industries (Furniture, Footwear, Paper and Printing)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Allnex GmbH

- 6.4.2 Arkema (Bostik)

- 6.4.3 Celanese Corporation

- 6.4.4 Chang Chun Group

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Hexion Inc.

- 6.4.9 Kuraray Co., Ltd.

- 6.4.10 Shaanxi XuTai Technology Co., Ltd

- 6.4.11 Sinopec Sichuan Vinylon Works

- 6.4.12 Synthomer plc

- 6.4.13 Tailored Adhesives.

- 6.4.14 Vinavil S.p.A.

- 6.4.15 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

醋酸乙烯單體市場:依純度、製程、製造方法、應用、銷售管道和最終用戶分類-2026-2032年全球市場預測

醋酸乙烯單體市場:依純度、製程、製造方法、應用、銷售管道和最終用戶分類-2026-2032年全球市場預測 醋酸乙烯單體市場:按應用和地區分類

醋酸乙烯單體市場:按應用和地區分類 全球醋酸乙烯單體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球醋酸乙烯單體市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球醋酸乙烯單體市場報告

2026年全球醋酸乙烯單體市場報告 醋酸乙烯單體市場規模、佔有率及成長分析(依純度、應用、最終用戶及地區分類)-2026-2033年產業預測

醋酸乙烯單體市場規模、佔有率及成長分析(依純度、應用、最終用戶及地區分類)-2026-2033年產業預測 醋酸乙烯單體市場機會、成長要素、產業趨勢分析及2026年至2035年預測

醋酸乙烯單體市場機會、成長要素、產業趨勢分析及2026年至2035年預測 醋酸乙烯酯單體市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、地區和競爭格局分類,2020-2030年預測醋酸乙烯酯衍生物市場(依衍生物類型、形式、技術、包裝類型和應用)-2025-2030 年全球預測

醋酸乙烯酯單體市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、地區和競爭格局分類,2020-2030年預測醋酸乙烯酯衍生物市場(依衍生物類型、形式、技術、包裝類型和應用)-2025-2030 年全球預測 醋酸乙烯單體市場評估:用途·終端用戶產業·各地區的機會及預測 (2018-2032年)

醋酸乙烯單體市場評估:用途·終端用戶產業·各地區的機會及預測 (2018-2032年) 全球乙烯 - 醋酸乙烯共聚物粉末市場按類型、最終用途產業、應用、地區、趨勢分析、競爭格局、預測 2019-2031 年

全球乙烯 - 醋酸乙烯共聚物粉末市場按類型、最終用途產業、應用、地區、趨勢分析、競爭格局、預測 2019-2031 年