|

市場調查報告書

商品編碼

2062277

不織布過濾:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Nonwoven Filtration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

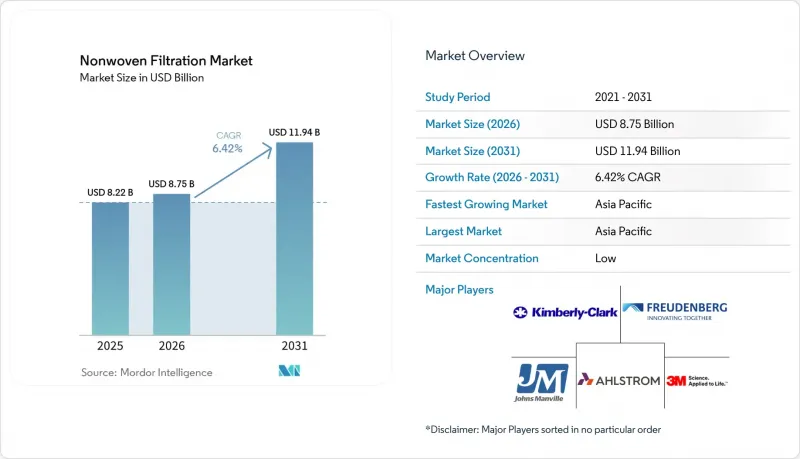

根據 Mordor Intelligence 預測,不織布過濾市場規模將從 2025 年的 82.2 億美元成長到 2026 年的 87.5 億美元,然後在 2031 年達到 119.4 億美元,2026 年至 2031 年的複合年成長率為 6.42%。

本報告根據不織布類型(紡粘、熔噴等)、過濾類型(空氣過濾、液體過濾、暖通空調系統、汽車及其他)、應用領域(水和污水處理、工業等)、最終用戶(工業、商業等)以及地區(亞太、北美、歐洲等)進行細分。市場預測以美元計價。

全球不織布過濾市場趨勢及洞察

快速的都市化正在推動對暖通空調和室內空氣品質 (IAQ) 的需求。

2025年,亞洲和中東多個地區採用了修訂後的ASHRAE 62.1通風率標準,該標準強制要求商業設施使用MERV 13級過濾器,迫使建築業主更頻繁地更換傳統的粗濾過濾器。資料中心營運商預計到2025年將佔全球電力消耗量的約2%,他們正在推廣使用低壓損褶皺不織布過濾器以降低風扇能耗,並傾向於使用靜電紡絲粘合基材的覆層。在北美,由公共產業資助的住宅維修補貼已將過濾器更換週期從傳統的五年縮短至約三年。透過將物聯網壓力感測器整合到新的過濾器外殼中,可以實現預測性維護,而那些能夠保證即使在高粉塵負荷下壓力上升曲線也呈線性變化的供應商將獲得獎勵。

疫情後醫療及製藥無塵室的發展

隨著mRNA疫苗生產線和生物相似藥生產設施的運作,2024年至2025年間,全球無菌填充能力成長了35%。同時,醫院中HEPA和ULPA過濾器的安裝量增加,H14終端過濾器也被引入手術室和加護病房。 2026年3月,MANN+HUMMEL在北卡羅來納州威爾遜市啟用了一間7級潔淨室,並開始檢驗用於OEM合約的藥用級濾材。儘管美國FDA和EMA對顆粒計數設定了嚴格的限制,要求在灌裝和包裝模組的上游安裝0.2微米絕對過濾濾芯,但連續生物製藥生產正在推動對可在長期生產過程中不間斷運作的一次性深度過濾器的需求。

多媒體處置和回收面臨的挑戰。

活性碳層壓不織布無法透過傳統的回收生產線進行經濟有效的分離。此外,歐洲接收廢舊過濾器的水泥窯對廢舊過濾器的預處理收費為每噸40至60美元。在新型熔融過濾回收系統中,多成分無紡布的回收率僅65%至70%,遠低於單組分無紡布。儘管法國和德國的生產者延伸責任制(EPR)法規強制要求回收廢棄過濾器,但遍遠地區的物流系統仍不完善,導致對掩埋處理的依賴性增加。 ISO和ASTM缺乏統一的回收標準,增加了設計的不確定性和合規成本。

細分市場分析

到2025年,紡粘不織布將佔銷售額的35.57%,成為不織布過濾市場中最大的銷售細分市場。同時,預計到2031年,靜電紡絲不織布的年複合成長率將達到6.79%。

疫情期間建立的熔噴生產線利潤率承壓,導致亞洲企業要么閒置產能,要么將其改造用於生產電池隔膜。將紡粘基材與靜電紡絲層複合而成的複合材料結構,在保持褶皺剛性的同時,縮小了HEPA和ULPA等級之間的性能差距。 HIFYBER和Espin Nanotech等公司展示的技術創新,將奈米纖維直徑減小到50-500奈米,使供應商能夠實現PM0.3 99.97%的收集效率,同時壓降比傳統HEPA降低30-40%,從而增強了高階過濾層的性能。逆滲透膜支撐層中使用濕式成型的合成纖維,其微纖維直徑減小到0.04 dtex,這進一步徵兆,專業製造流程將與高產能的紡粘平台並存。

在不織布過濾市場,空氣過濾仍將保持其主導地位,預計到2025年將佔據50.22%的銷售佔有率,而液體過濾預計將以6.90%的複合年成長率快速成長至2031年。東麗公司於2025年3月推出超過濾產品,杜邦公司於2026年3月升級奈米過濾技術,顯示供應商正致力於在市政回收專案中實現節能和減少污染。

當工業製造商升級冷卻塔迴路以及食品飲料廠逐步淘汰 PFAS 時,現在紛紛訂購結合了紡粘預過濾器和奈米纖維拋光級的多層濾芯組件。用於半導體製造廠的混合型(顆粒+分子)過濾器,透過在不織布褶皺中加入氣體吸附層,模糊了傳統的「空氣」和「液體」界限。因此,擁有跨平台產品系列的供應商可以提升銷售捆綁式解決方案,從而提高不織布過濾市場的平均單次安裝收入。

區域分析

預計到 2025 年,亞太地區將佔全球銷售額的 39.97%,並將以 7.12% 的複合年成長率成長至 2031 年。中國大力推動半導體自給自足,推動了對新型靜電紡絲和熔噴生產線的投資,而印度的產能正在擴大至每年 18,740 噸,以滿足暖通空調和車廂過濾器的激增需求。

北美和歐洲的替換濾芯市場已趨於成熟,但由於PM2.5法規和建築能源效率指令的日益嚴格,預計成長率將僅為個位數中段。 Avgol在北卡羅來納州投資1億美元的紡黏膜工廠以及MANN+HUMMEL的7級潔淨室,都體現了企業對本土化生產能力的信心。

儘管南美洲、中東和非洲的銷售額佔比不高,但預計這些地區在巴西水處理設施升級、阿根廷鋰礦粉塵控制、沙烏地阿拉伯潔淨室以及用於旅遊業離網海水淡化的微過濾器等領域將強勁成長。電池回收能力集中在中國、歐洲和北美,這迫使濾材供應商建立區域技術支援實驗室,從而加強了整個不織布過濾市場的服務合作。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 快速的都市化正在推高對暖通空調和室內空氣品質的需求。

- 疫情後醫療及製藥無塵室的發展

- 關於低壓損耗過濾器的資料中心能源法規

- 需要顆粒過濾的電池回收廠

- 離網旅遊海水淡化微濾

- 市場限制因素

- 多媒體處置和回收面臨的挑戰。

- 監管機構關注微纖維脫落問題

- 中小加工企業缺乏人工智慧實施資金

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按不織布類型

- 紡粘

- 熔噴

- 針刺機

- 複合材料

- 靜電紡絲

- 其他類型的不織布(濕式織造、氣流成網網織)

- 過濾法

- 空氣過濾

- 液體過濾

- 其他類型(氣體、石油、血液)

- 透過使用

- 供水和廢水處理

- 工業(製造業、化工、電力)

- 暖通空調系統

- 車

- 醫療和藥品

- 食品/飲料加工

- 電子設備

- 其他用途(採礦、製漿和造紙)

- 最終用戶

- 產業

- 商業的

- 住宅

- 市政當局/政府

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Ahlstrom

- DuPont

- Fibertex Nonwovens A/S

- Fitesa SA and Affiliates

- Freudenberg SE

- Hollingsworth and Vose

- Huvis Corp.

- Johns Manville

- KCWW

- Lydall, Inc.

- Mann+Hummel

- Parker Hannifin Corp

- Sandler AG

- TORAY INDUSTRIES, INC.

第7章 市場機會與未來展望

According to Mordor Intelligence, the non-Woven filtration market size is expected to grow from USD 8.22 billion in 2025 to USD 8.75 billion in 2026 and is forecast to reach USD 11.94 billion by 2031 at 6.42% CAGR over 2026-2031.

This report is Segmented by Type of Nonwoven (Spunbond, Meltblown, and More), Filtration Type (Air Filtration, Liquid Filtration, HVAC Systems, Automotive, and Other Types), Application (Water and Waste-Water Treatment, Industrial, and More), End-User (Industrial, Commercial, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Nonwoven Filtration Market Trends and Insights

Rapid Urbanization Boosting HVAC and IAQ Demand

Revised ASHRAE 62.1 ventilation rates, adopted by several Asian and Middle-Eastern jurisdictions during 2025, now lock MERV 13 as the baseline for commercial sites, compelling building owners to replace legacy coarse filters more frequently. Data-center operators, already consuming roughly 2% of global electricity in 2025, are standardizing on low-pressure-drop pleated nonwovens to temper fan-energy draw, favoring electrospun overlays on spunbond carriers. Utility-funded residential retrofit rebates across North America are accelerating replacement cycles to roughly three years, down from five. Embedded IoT pressure sensors in new housings allow predictive maintenance, rewarding vendors that guarantee linear pressure-rise curves under dust loading.

Post-Pandemic Growth of Healthcare and Pharma Cleanrooms

Global aseptic-fill capacity expanded 35% between 2024 and 2025 as mRNA vaccine lines and biosimilar suites came online. HEPA and ULPA filter installations in hospitals rose in parallel, embedding H14 terminal filters in operating theaters and intensive-care wards. In March 2026, MANN+HUMMEL opened a Level 7 cleanroom in Wilson, North Carolina, to validate pharma-grade media for OEM contracts. Strict particle-count limits from both U.S. FDA and EMA now mandate 0.2-micron absolute cartridges upstream of fill-finish modules, while continuous biologics manufacturing pushes single-use depth-filter demand that can run uninterrupted for longer campaigns.

Disposal and Recycling Hurdles of Composite Media

Activated-carbon laminated nonwovens cannot be economically separated in traditional recycling lines, and European cement kilns that accept spent filters charge USD 40-60 per metric ton in pretreatment fees. New melt-filtration reclaim systems achieve only 65-70% yield with multi-component webs, well below mono-material streams. Extended producer responsibility rules in France and Germany now force manufacturers to collect end-of-life filters, but rural logistics remain undeveloped, increasing landfill reliance. Lack of harmonized ISO or ASTM recyclability standards adds design uncertainty and compliance cost.

Other drivers and restraints analyzed in the detailed report include:

- Data-Center Energy Mandates for Low-Pressure-Drop Filters

- Battery-Recycling Plants Needing Fine-Particle Filtration

- Regulatory Focus on Microfiber Shedding

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Spunbond nonwoven delivered 35.57% of 2025 revenue and underpins the largest revenue tier of the nonwoven filtration market. Electro-spun nonwoven, however, is projected to advance at a 6.79% CAGR through 2031.

Margin pressure on melt-blown lines built during the pandemic is prompting Asian firms to idle or repurpose capacity toward battery separators. Composite constructions that laminate spunbond backers with electrospun layers are narrowing the performance gap between HEPA and ULPA classes while preserving pleat stiffness. Breakthroughs that cut nanofiber diameters to 50-500 nm, demonstrated by HIFYBER and Espin Nanotech, let suppliers hit 99.97% PM0.3 efficiency at 30-40% lower pressure drop than conventional HEPA, strengthening the premium tier. Adoption of wet-laid synthetics with microfibers down to 0.04 dtex in reverse-osmosis support layers is another sign that specialty processes will coexist with high-output spunbond platforms.

Air filtration maintained a commanding 50.22% share of 2025 revenue in the nonwoven filtration market share landscape, yet liquid filtration is accelerating fastest at a 6.90% CAGR through 2031. Toray's ultrafiltration launch in March 2025 and DuPont's March 2026 nanofiltration upgrade illustrate vendor focus on lower energy and fouling profiles for municipal reuse projects.

Industrial processors upgrading cooling-tower loops and food and beverage plants phasing out PFAS now order multi-layer cartridge trains that pair spunbond prefilters with nanofiber polisher stages. Hybrid particulate-plus-molecular filters for semiconductor fabs blur classical air versus liquid boundaries by embedding gas-adsorption layers into nonwoven pleats. Consequently, vendors with cross-platform portfolios can upsell bundled solutions, raising average sales per installation in the nonwoven filtration market.

Geography Analysis

Asia-Pacific held 39.97% of 2025 sales and is forecast to expand at a 7.12% CAGR through 2031. China's semiconductor self-sufficiency drive funds new electrospinning and melt-blown lines, while India's capacity surge to 18,740 tpa satisfies surging HVAC and cabin-filter demand.

North America and Europe form mature replacement markets, yet gain mid-single-digit lift from stricter PM2.5 and building-energy directives. Avgol's USD 100 million North Carolina spunbond plant and MANN+HUMMEL's Level 7 cleanroom demonstrate confidence in domestic capacity localization.

South America, and Middle-East and Africa contribute smaller revenues but see high-growth pockets in Brazilian water-treatment upgrades, Argentine lithium-mine dust control, Saudi cleanroom zones, and off-grid desalination micro-filters for tourism. Battery-recycling capacity, clustered in China, Europe, and North America, compels media suppliers to install regional tech-support labs, tightening service links across the nonwoven filtration market.

- 3M

- Ahlstrom

- DuPont

- Fibertex Nonwovens A/S

- Fitesa SA and Affiliates

- Freudenberg SE

- Hollingsworth and Vose

- Huvis Corp.

- Johns Manville

- KCWW

- Lydall, Inc.

- Mann+Hummel

- Parker Hannifin Corp

- Sandler AG

- TORAY INDUSTRIES, INC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid urbanisation boosting HVAC and IAQ demand

- 4.2.2 Post-pandemic growth of healthcare and pharma cleanrooms

- 4.2.3 Data-centre energy mandates for low-pressure drop filters

- 4.2.4 Battery-recycling plants needing fine-particle filtration

- 4.2.5 Off-grid tourist desalination micro-filters

- 4.3 Market Restraints

- 4.3.1 Disposal and recycling hurdles of composite media

- 4.3.2 Regulatory focus on microfiber shedding

- 4.3.3 Capital scarcity for AI retrofits at SME converters

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type of Nonwoven

- 5.1.1 Spunbond

- 5.1.2 Meltblown

- 5.1.3 Needle-punched

- 5.1.4 Composite

- 5.1.5 Electro-spun

- 5.1.6 Other Nonwoven Types (Wet-laid, Air-laid)

- 5.2 By Filtration Type

- 5.2.1 Air Filtration

- 5.2.2 Liquid Filtration

- 5.2.3 Other Types (Gas, Oil, Blood)

- 5.3 By Application

- 5.3.1 Water and Waste-water Treatment

- 5.3.2 Industrial (Manufacturing, Chemical, Power)

- 5.3.3 HVAC Systems

- 5.3.4 Automotive

- 5.3.5 Healthcare and Pharmaceuticals

- 5.3.6 Food and Beverage Processing

- 5.3.7 Electronics

- 5.3.8 Other Applications (Mining, Pulp and Paper)

- 5.4 By End-user

- 5.4.1 Industrial

- 5.4.2 Commercial

- 5.4.3 Residential

- 5.4.4 Municipal/Government

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Ahlstrom

- 6.4.3 DuPont

- 6.4.4 Fibertex Nonwovens A/S

- 6.4.5 Fitesa SA and Affiliates

- 6.4.6 Freudenberg SE

- 6.4.7 Hollingsworth and Vose

- 6.4.8 Huvis Corp.

- 6.4.9 Johns Manville

- 6.4.10 KCWW

- 6.4.11 Lydall, Inc.

- 6.4.12 Mann+Hummel

- 6.4.13 Parker Hannifin Corp

- 6.4.14 Sandler AG

- 6.4.15 TORAY INDUSTRIES, INC.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment