|

市場調查報告書

商品編碼

2062275

硫酸鈷:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Cobalt Sulphate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

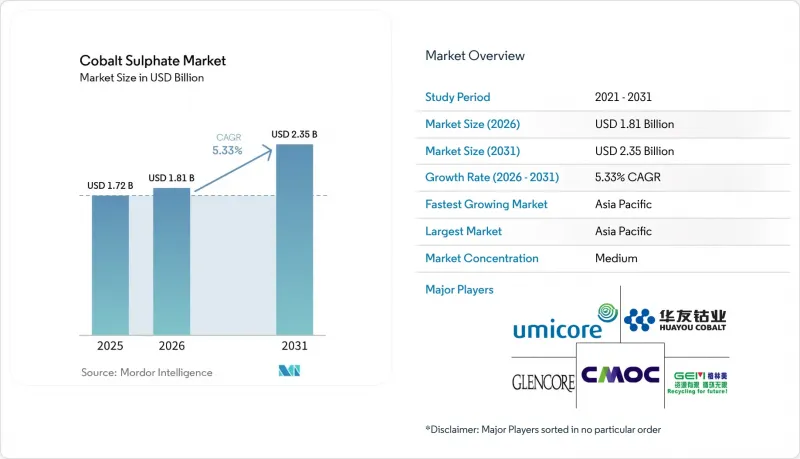

預計硫酸鈷市場將從 2025 年的 17.2 億美元成長到 2026 年的 18.1 億美元,到 2031 年達到 23.5 億美元,2026 年至 2031 年的複合年成長率為 5.33%。

本報告按等級(電池級和工業級)、應用(電池、催化劑、乾燥劑、電鍍、顏料和染料等)、終端用戶行業(汽車、電子、化學、油漆和塗料等)以及地區(亞太地區、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元計價。

全球硫酸鈷市場趨勢與洞察

歐洲和美國為實現供應鏈在地化而採取的支持措施,正在推動中國以外地區煉油產能的擴張。

隨著《通貨膨脹抑制法案》(IRA)和歐盟《關鍵原料法案》旨在減少對中國的依賴,自2023年以來宣布的價值約20億美元的項目正湧入北美和歐洲的硫酸鈷精煉廠。 Electra Battery Materials公司已獲得1億加幣(7,157萬美元)的資金,用於在安大略省建造一座年產能6,500噸的工廠,該項目由美國主導提供資金支持,並與LG Energy Solutions公司簽署了一項長期啟動協議。這表明,在僅憑現貨價格難以證明建設合理性的情況下,國防主導的資金籌措仍然存在。韓國已獲得45.8兆韓元的資金和10兆韓元的儲備,旨在2030年將其對單一國家的依賴度降低到50%以下,這與2026年加拿大和韓國簽署的關於電池金屬的合作備忘錄相輔相成。

印尼鎳產品產量增加,改變了成本曲線。

寶石礦業集團旗下的青梅邦和華友礦山集散中心以邊際成本運輸鈷,低於傑沃伊斯(Jervois)愛達荷鈷礦等原生礦山的成本。愛達荷鈷礦已於2024年停產,並於2025年申請破產保護。生命週期分析表明,印尼的高壓酸浸(HPAL)製程排放的溫室氣體比剛果民主共和國(DRC)和中國的水處理流程多70%,這使得低成本生產與歐盟的碳足跡聲明相悖。隨著鈷成為鎳收益的商品,鈷的生產更多地受到鎳價訊號而非鈷價訊號的影響,這使得硫酸鈷市場的價格形成更加複雜。

ESG 和人權監督限制了剛果民主共和國小規模採礦的供應。

2024年,剛果民主共和國約5-6%的鈷產量來自小規模採礦,但有關童工的指控迫使電池製造商採取零容忍採購政策。儘管2024年82%的精煉鈷符合RMAP(負責任礦產採購原則),但剩餘的供應對汽車製造商的聲譽構成風險。 ERG旗下的Metakol和CMOC旗下的Tenke Fungurume等工業設施已獲得Copper Mark和普華永道認證,但在面積達25.5萬平方公裡的銅纜,認證的實施情況各不相同。韓國2024年減少對單一來源依賴的策略與美國國防部對Electra公司2000萬美元的投資一致,凸顯了硫酸鈷市場的地緣政治多元化。合約條款中提及 ISO 26000 和 OECD實質審查正在逐漸標準化,缺乏審核能力的小規模礦工正在被淘汰。

細分市場分析

2025年,電池級材料佔總需求的76.22%,預計在預測期(2026-2031年)內,該領域硫酸鈷市場規模將以5.57%的複合年成長率成長。工業級材料在催化劑、顏料和電鍍應用領域的成長與GDP成長同步,但成長速度較慢。

由於雜質含量限制更為嚴格(金屬含量低於10 ppm,硫酸鹽含量低於50 ppm),電池級鈷的價格比工業級鈷高出30-50%。隨著超高鎳正極材料的普及,預計這一價格差距將進一步擴大。 Elektra位於安大略省的工廠將於2027年投產,屆時每年將供應6,500噸電池級鈷,佔全球(不包括中國)產量的27%。像伊士曼化學公司這樣的工業生產商每月向25個國家出口超過300噸電池級鈷,這表明該細分市場監管相對寬鬆且穩定。然而,硫酸鈷市場仍兩極化,溢價與負責任礦產保證流程(RMAP)認證密切相關。

區域分析

預計到2025年,亞太地區將佔據全球硫酸鈷市場佔有率的61.34%,並在2031年之前以5.89%的複合年成長率持續成長,這主要得益於中國78.6%的精煉產量以及印尼高壓酸浸(HPAL)製程的蓬勃發展。中國政府在2024年策略性採購1.66萬噸硫酸鈷,有效穩定了中國鉬業公司先前的供應過剩局面,並凸顯了國家干預硫酸鈷市場的能力。

在北美,《通膨控制法案》和 Electra 公司在安大略省建設的年產 6,500 噸的工廠可能會在 2031 年前擴大該地區的硫酸鈷市場。到 2027 年,Sherritt 公司位於亞伯達的冶煉廠(年產量 2729 噸)仍將是北美唯一的主要生產基地,而 Jervois 公司位於愛達荷州的礦山將繼續處於維護狀態。

歐洲的佔有率取決於歐盟40%的加工目標和16%的強制性再生鈷使用比例。優美科在比利時和芬蘭的資產在2024年加工了18,500噸鈷,但由於汽車正極材料需求放緩,利潤率下降。在南美洲和中東及非洲地區,剛果民主共和國(剛果(金))的鈷礦開採量佔全球62%,並且仍然擁有定價權。其影響力之大可見一斑:在剛果(金)於2025年實施出口禁令後的六週內,硫酸鈷價格飆升了92%。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電網級 LFP+LMFP 儲能系統需要富含鈷的穩定劑。

- 支持歐洲和美國供應鏈本地化的措施(IRA 和歐盟 CRM 法案)

- 鎳產品生產的擴張導致低成本硫酸鈷(CoSO4)產量增加。

- 採用CoSO4基抑制劑的AI伺服器溫度控管液

- 從高鎳電池中回收的硫酸鈷提高了供應的柔軟性。

- 市場限制因素

- 對剛果民主共和國(剛果(金))小規模礦業公司的ESG和人權審查

- 正極材料成本快速降低和磷酸鋰鐵電池市佔率擴大

- 從 2029 年起,強制使用再生材料將減緩原生材料的需求成長。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按年級

- 電池級

- 工業級

- 透過使用

- 電池

- 催化劑

- 乾燥劑

- 電鍍

- 顏料和染料

- 其他用途

- 按最終用戶行業分類

- 車

- 電子設備

- 化學品

- 油漆和塗料

- 儲能整合商

- 其他

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- American Elements

- CMOC

- Cobalt Blue Holdings Limited

- Electra Battery Materials

- Eurasian Resources Group

- Fortum

- GEM Co., Ltd.

- Glencore Plc

- Huayou Cobalt

- Jervois

- Jiangsu Xiongfeng Technology Co., Ltd

- Jinchuan Group International Resources Co. Ltd

- Norilsk Nickel

- Sherritt International Corporation

- Sumitomo Metal Mining Co., Ltd.

- Umicore

- Vale SA

第7章 市場機會與未來展望

According to Mordor Intelligence, the cobalt sulphate market size is expected to increase from USD 1.72 billion in 2025 to USD 1.81 billion in 2026 and reach USD 2.35 billion by 2031, growing at a CAGR of 5.33% over 2026-2031.

This report is Segmented by Grade (Battery Grade and Industrial Grade), Application (Batteries, Catalysts, Drying Agents, Electroplating, Pigments and Dyes, and More), End-User Industry (Automotive, Electronics, Chemicals, Paints and Coatings, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Cobalt Sulphate Market Trends and Insights

Western Supply-Chain Localization Subsidies Drive Refining Capacity Outside China

Roughly USD 2 billion in announced projects since 2023 are flowing into North American and European cobalt sulphate market refineries as the Inflation Reduction Act and the EU Critical Raw Materials Act seek to cut Chinese dependence. Electra Battery Materials secured CAD 100 million (USD 71.57 million) for a 6,500 tons per annum Ontario plant backed by U.S. Department of Defense funding and a long-term LG Energy Solution offtake, illustrating defense-led underwriting when spot prices alone would not justify construction. South Korea has earmarked 45.8 trillion won in financing and a 10 trillion-won stockpile to lower single-country reliance below 50% by 2030, complementing a 2026 Canada-Korea memorandum on battery metals.

Nickel-By-Product Expansions in Indonesia Reshape Cost Curves

GEM's Qingmei Bang and Huayou's MHP hubs ship cobalt at marginal cost, undercutting primary mines such as Jervois' Idaho Cobalt Operations, which halted in 2024 and filed Chapter 11 in 2025. Life-cycle analyses show Indonesia HPAL routes carry 70% higher greenhouse-gas footprints than DRC-China hydromet processes, putting low-cost output at odds with EU carbon-footprint declarations. As cobalt becomes a residual from nickel revenue, production responds to nickel, not cobalt, signals, complicating price discovery in the cobalt sulphate market.

ESG and Human-Rights Scrutiny Constrains DRC Artisanal Mining Supply

Artisanal operations delivered about 5-6% of DRC cobalt in 2024, yet allegations of child labor have pushed battery makers toward zero-tolerance sourcing policies. While 82% of refined cobalt was RMAP-conformant in 2024, the residual volume exposes auto OEMs to reputational hazards. Industrial sites like ERG's Metalkol and CMOC's Tenke Fungurume have secured Copper Mark and PwC assurance, but enforcement across the 255,000 km2 Copperbelt is inconsistent. South Korea's 2024 strategy to cut single-source exposure mirrors the U.S. Department of Defense's USD 20 million Electra investment, highlighting geopolitical diversification in the cobalt sulphate market. Contract clauses referencing ISO 26000 and OECD due diligence are becoming standard, excluding smaller miners lacking audit capacity.

Other drivers and restraints analyzed in the detailed report include:

- Recycled Cobalt-Sulfate Streams Offer Supply Flexibility Amid Regulatory Mandates

- Grid-Scale Energy Storage Chemistries Evolve Toward Mid-Nickel Formulations

- Rapid Cathode Thrifting and LFP Market-Share Gains Reduce Cobalt Intensity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Battery-grade material captured 76.22% of 2025 demand, and its Cobalt Sulphate market size for this segment is expected to grow at a 5.57% CAGR during the forecast period (2026-2031). Industrial-grade is advancing at a slower pace as catalysts, pigments, and plating applications grow in line with GDP.

Tighter impurity thresholds, less than or equal to 10 ppm metals and less than or equal to 50 ppm sulfate, allow battery-grade to command a 30-50% premium over industrial grades, a spread likely to widen as ultra-high-nickel cathodes become mainstream. Electra's Ontario plant will supply 6,500 tons per annum of battery-grade cobalt, or 27% of ex-China output, when commercial production starts in 2027. Industrial producers such as Eastmen Chemicals ship over 300 tons monthly to 25 countries, signaling a stable but less regulated niche. The Cobalt Sulphate market nevertheless remains bifurcated, with premium pricing tied to Responsible Minerals Assurance Process certification.

Geography Analysis

Asia-Pacific commanded 61.34% Cobalt Sulphate market share in 2025 and should advance at 5.89% CAGR through 2031, buoyed by China's 78.6% refined output and Indonesia's HPAL surge. Beijing's 16,600-ton strategic purchase in 2024 helped stabilize prices after China Molybdenum's surplus, affirming state intervention capacity in the Cobalt Sulphate market.

In North America, the Inflation Reduction Act and Electra's 6,500 tons per annum Ontario plant could lift the Cobalt Sulphate market size regionally by 2031. Sherritt's 2,729-tonne Alberta refinery remains the continent's only significant producer until 2027, while Jervois' Idaho mine stays on care-and-maintenance.

Europe's share hinges on the EU's 40% processing target and 16% recycled-cobalt mandate. Umicore's Belgian and Finnish assets processed 18,500 tons in 2024, though margins tightened as auto cathode demand softened. South America and MEA, dominated by the DRC's 62% mined share, remain price setters; the 2025 DRC export ban that spiked sulfate prices 92% within six weeks exemplifies that leverage.

- American Elements

- CMOC

- Cobalt Blue Holdings Limited

- Electra Battery Materials

- Eurasian Resources Group

- Fortum

- GEM Co., Ltd.

- Glencore Plc

- Huayou Cobalt

- Jervois

- Jiangsu Xiongfeng Technology Co., Ltd

- Jinchuan Group International Resources Co. Ltd

- Norilsk Nickel

- Sherritt International Corporation

- Sumitomo Metal Mining Co., Ltd.

- Umicore

- Vale S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Grid-scale LFP + LMFP storage pivot needs Co-rich stabiliser additives

- 4.2.2 Western supply-chain localisation subsidies (IRA and EU CRM Act)

- 4.2.3 Nickel-by-product expansions raising low-cost CoSO4 output

- 4.2.4 AI-server thermal-management fluids using CoSO4 inhibitors

- 4.2.5 Recycled cobalt-sulfate from high-Ni battery streams expanding supply flexibility

- 4.3 Market Restraints

- 4.3.1 ESG and human-rights scrutiny in DRC artisanal mines

- 4.3.2 Rapid cathode thrifting and LFP share gains

- 4.3.3 Recycled-content mandates dampen virgin demand growth post-2029

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Grade

- 5.1.1 Battery Grade

- 5.1.2 Industrial Grade

- 5.2 By Application

- 5.2.1 Batteries

- 5.2.2 Catalysts

- 5.2.3 Drying Agents

- 5.2.4 Electroplating

- 5.2.5 Pigments and Dyes

- 5.2.6 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Electronics

- 5.3.3 Chemicals

- 5.3.4 Paints and Coatings

- 5.3.5 Energy Storage Integrators

- 5.3.6 Others

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 American Elements

- 6.4.2 CMOC

- 6.4.3 Cobalt Blue Holdings Limited

- 6.4.4 Electra Battery Materials

- 6.4.5 Eurasian Resources Group

- 6.4.6 Fortum

- 6.4.7 GEM Co., Ltd.

- 6.4.8 Glencore Plc

- 6.4.9 Huayou Cobalt

- 6.4.10 Jervois

- 6.4.11 Jiangsu Xiongfeng Technology Co., Ltd

- 6.4.12 Jinchuan Group International Resources Co. Ltd

- 6.4.13 Norilsk Nickel

- 6.4.14 Sherritt International Corporation

- 6.4.15 Sumitomo Metal Mining Co., Ltd.

- 6.4.16 Umicore

- 6.4.17 Vale S.A.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

鈷酸鋰市場機會、成長要素、產業趨勢分析及2026-2035年預測

鈷酸鋰市場機會、成長要素、產業趨勢分析及2026-2035年預測 鈷市場:2026-2032年全球市場預測(依產品類型、原料來源、形態、純度、應用、終端用戶產業及通路分類)

鈷市場:2026-2032年全球市場預測(依產品類型、原料來源、形態、純度、應用、終端用戶產業及通路分類) 鈷合金粉末:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

鈷合金粉末:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 硫酸鈷市場報告:按形態、應用和地區分類(2026-2034 年)硬脂酸鈷市場:依形態、等級、應用、終端用戶產業及銷售管道分類-2026-2032年全球市場預測碳酸鈷市場:依純度等級、形態、應用及通路分類-2026-2032年全球市場預測

硫酸鈷市場報告:按形態、應用和地區分類(2026-2034 年)硬脂酸鈷市場:依形態、等級、應用、終端用戶產業及銷售管道分類-2026-2032年全球市場預測碳酸鈷市場:依純度等級、形態、應用及通路分類-2026-2032年全球市場預測 全球碳酸鈷市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球碳酸鈷市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 鈷市場分析及預測(至2035年):類型、產品類型、應用、最終用戶、形態、技術、組件、材料類型、製程、安裝類型依來源、最終用途、純度等級、回收製程和產品形式分類的再生鈷市場-2026-2032年全球預測依純度等級、通路、應用和最終用途產業分類的醋酸鈷晶體市場-2026年至2032年全球預測

鈷市場分析及預測(至2035年):類型、產品類型、應用、最終用戶、形態、技術、組件、材料類型、製程、安裝類型依來源、最終用途、純度等級、回收製程和產品形式分類的再生鈷市場-2026-2032年全球預測依純度等級、通路、應用和最終用途產業分類的醋酸鈷晶體市場-2026年至2032年全球預測