|

市場調查報告書

商品編碼

2062269

調度控制台:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031)Dispatch Console - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

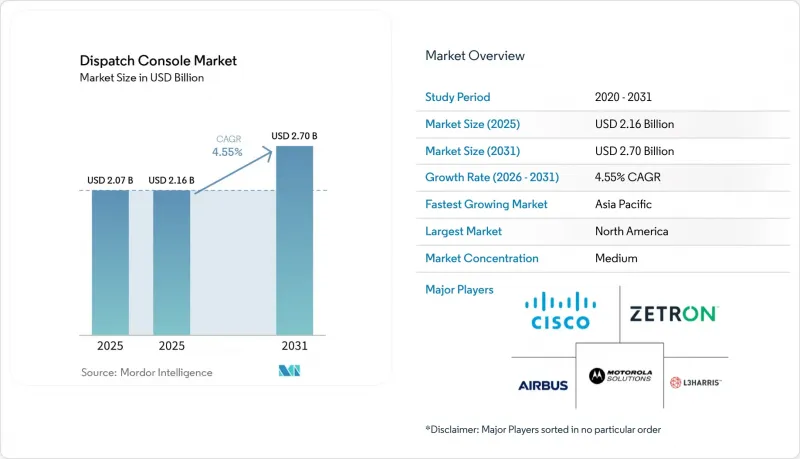

根據 Mordor Intelligence 預測,調度控制台市場規模將從 2025 年的 20.7 億美元和 2026 年的 21.6 億美元成長到 2031 年的 27 億美元,2026 年至 2031 年的複合年成長率為 4.55%。

本報告按組件(硬體和軟體)、類型(基於IP的調度控制台和基於TDM的調度控制台)、功能(語音調度、文字調度、定位服務、即時監控等)、最終用戶行業(公共安全機構、政府和國防、交通運輸和物流等)以及地區進行細分。市場預測以價值(美元)表示。

全球調度控制台市場趨勢及洞察

NG9-1-1 的推出將加速主機升級。

聯邦和州政府法規要求客服中心必須能夠接收語音、文字、圖像和影片,這迫使公共安全機構淘汰無法處理多媒體對話啟動協定(SIP) 的主機。堪薩斯州、奧克拉荷馬州和其他一些領先州已經證明,如果該項目由中央統一撥款,到 2026 年實現聯邦目標,並運作應急服務 IP 網路,是完全可以實現的。加州的成本超支(支出已超過 4.5 億美元)凸顯了分散採購帶來的預算風險。除了硬體升級外,各機構還必須更新錄音系統和培訓課程,從而形成一個全面的多年資本投資週期。能夠快速認證設備並支援分階段過渡的供應商將獲得先發優勢。

在物流領域實施雲端原生CAD和調度

車輛營運商正擴大採用基於雲端的調度套件,這種套件無需本地伺服器,並允許主管人員透過任何設備管理營運。喬治亞和威斯康辛州的提案書 (RFP) 明確要求近乎零停機時間、基於瀏覽器的介面和分析儀表板。月費模式對中小型車隊營運商極具吸引力,因為它將資本投資轉化為營運成本,並縮短了內部核准週期。隨著停機風險從本地硬體轉移到廣域網路連接,供應商必須提供冗餘通訊環境和嚴格的服務等級協定 (SLA),以應對安全性至關重要的應用場景。

公共採購延誤與預算障礙

公共安全機構面臨多階段核准流程、公開聽證會以及競標異議的可能性,最終敲定合約可能需要18到36個月的時間。伊利諾州新增財政收入僅勉強涵蓋其營運成本的一半,迫使各部門延後主機升級,直到州津貼到位。阿根廷也出現了類似的延誤,一項耗資230億阿根廷披索(約2300萬美元)的911系統升級項目被拆分到兩個預算週期中,這表明宏觀經濟波動甚至會使已通過核准的項目脫軌。供應商需要提供過渡性擔保和靈活的付款計劃才能保持競爭力。

細分市場分析

2025年,硬體收入佔總收入的55.55%,因為各機構繼續將主機、無線閘道器和可調節家具的成本分攤到7到10年內。奧克拉荷馬州的全州合約和堪薩斯州的縣級批准證實,客製化的人體工學辦公桌的價格仍然高於普通辦公家具。軟體收入成長超過硬體,年成長率達4.63%,因為雲端訂閱、地圖擴展和分析模組正在將一次性許可轉變為可預測的月度收費。過去伺服器安裝需要堆高機,而現在新的部署方式使得虛擬機器可以在幾分鐘內啟動並運行,更新會在夜間自動完成。這種轉變降低了整體擁有成本,但同時也使政府機構受制於供應商的藍圖,導致轉換供應商的成本很高。隨著人工智慧 (AI) 工作負載的增加,硬體升級將需要額外的圖形處理能力、高解析度顯示器和 10Gigabit網路上行鏈路,即使在 SaaS 主導的世界中,這也將促進硬體銷售。

捆綁式採購的趨勢仍在持續,預計到2026年,超過60%的競標將要求由單一整合商提供家具、無線介面和軟體。雖然捆綁式合約簡化了管治,但卻給小規模的專業公司帶來了價格壓力,因為它們無法負擔多年的保固費用。採用最佳實踐方案的買家強烈要求基於標準的API和物件級資料匯出功能,以便於未來的系統遷移,但這些條款很少出現在市政招標文件中,導致供應商持續被鎖定。

到2025年,基於IP的主機將佔總銷售額的67.75%,但調度控制台市場仍售出數千台TDM終端,主要面向礦山、石油鑽井設施和地方公共產業,這些部門更重視確定性延遲和獨立可靠性,而非功能性。 IP系統能夠與寬頻網路無縫整合,支援多媒體通話,並實現虛擬化災害復原基地——所有這些優勢對都市區機構都極具吸引力。同時,TDM 5.05%的成長率反映出新興市場中缺乏光纖的公共產業正在鋪設新的銅纜或微波鏈路。由於各機構都在努力避免突然轉型,因此能夠實現對話啟動協定(SIP)和電路交換訊號之間轉換的互通性閘道器仍然是一個蓬勃發展的細分市場。受混合架構普及的推動,預計到2031年,閘道器的調度控制台市場規模將達到2.7億美元。

根據廠商藍圖,預計2020年代末期將迎來轉捩點,屆時通訊業者將逐步淘汰窄頻專用線路。隨著服務供應商向全IP骨幹網路遷移,更新需求將激增,原本需要十年才能完成的升級工作將集中在三年內完成。擁有可現場更換的IP介面卡和針對不同使用規模客製化的授權模式的供應商,將能夠充分利用這項需求激增的機會。

區域分析

截至2025年,北美佔據了調度控制台市場36.67%的佔有率。華盛頓州耗資4800萬美元的全州緊急服務IP網路擴建項目和紐約州耗資8500萬美元的縣級津貼計劃等跨省契約,為2031年之前的訂單。加拿大正在加速主機訂單的成長,強制要求在2027年前在全國部署下一代911功能,並分階段提供2500萬加元(約1800萬美元)的資金。然而,美國2025年預算取消了聯邦政府的配套資金,將財政負擔轉移到了各州,延長了小規模轄區的採購週期。與FirstNet的整合需要額外的認證,這將使部署計畫的周期從6個月延長到9個月,但一旦完成,將能夠直接將高頻寬影像和無人機影像導入主機。

亞太地區以4.76%的複合年成長率呈現最高增速。印度的智慧城市計畫涵蓋100個城市,正在部署整合指揮控制中心,監控超過14.2萬個鏡頭,顯示市場對具備先進影像分析功能的IP攝影機需求大規模。中國的特大特大城市正在經歷更大規模的部署,但國內採購政策優先考慮本地供應商。杜拜的企業指揮控制中心協調2.8萬輛車,每天處理44億個資料點,這顯示中東地區對高吞吐量、人工智慧賦能的主機有著強勁的需求。日本和韓國則專注於分階段升級,在不完全更換系統的情況下,將現有投資應用於5G和自動駕駛汽車測試。

在歐洲,為滿足《電子通訊法典》的要求,現代化進程正在進行中。英國「守護者中心」(Guardian Hub)計畫和一項為期十年的行動巡邏系統合約表明,各方願意投入長期營運預算。 Hexagon公司斥資1,000萬歐元(約1,130萬美元)收購了一家歐洲錄音解決方案供應商,此舉增強了符合歐盟資料居住要求的互通性解決方案。南美洲蘊藏著巨大的機遇,但市場較為分散。阿根廷和巴西的地方政府負責人已發布大規模競標,但面臨難以預測的外匯波動和聯邦政府資金轉移的限制。中東的大型企劃,例如沙烏地阿拉伯的“吉迪亞智慧指揮中心”,正在成為全球供應商競相效仿的典範。非洲市場仍在發展中,但南非、奈及利亞和埃及的一些大都會圈已啟動可行性研究,這表明在預測期後期可能會出現一波待開發區的IP主機部署浪潮。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- NG9-1-1 的推出加速了主機的升級換代。

- 在物流領域實施雲端原生CAD和調度

- 電網現代化正在提振電力公司的需求。

- 公共安全寬頻網路的部署

- 透過人工智慧驅動的車輛調度最佳化響應工作流程。

- 工業園區內的私有5G示範實驗支援IP調度

- 市場限制因素

- 公共採購延誤與預算挑戰

- 網路安全升級成本高昂

- 整合套件中供應商鎖定風險

- 1 GHz 以下的即時頻寬匱乏

- 產業生態系分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 硬體

- 軟體

- 按類型

- 基於 IP 的調度控制台

- 基於時分複用 (TDM) 的調度控制台

- 功能性別

- 語音調度

- 簡訊發送

- 定位服務

- 即時監控

- 數據分析與報告撰寫

- 按最終用戶行業分類

- 公共安全機關

- 政府/國防

- 運輸/物流

- 衛生保健

- 製造業

- 採礦、能源和公共產業

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 科威特

- 巴林

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Motorola Solutions, Inc.

- Hexagon AB

- CentralSquare Technologies, LLC

- Airbus SE

- Hytera Communications Corporation Limited

- L3Harris Technologies, Inc.

- Omnitronics Pty Limited

- Cisco Systems, Inc.

- RapidDeploy, Inc.

- EFJohnson Technologies, Inc.

- Catalyst Communications Technologies, Inc.

- Saab AB

- Telex Radio Dispatch

- Avaya LLC

- InterTalk Critical Information Systems

- Frequentis AG

- Esri, Inc.

- ZETRON Inc.

- Synch Systems, Inc.

- Avtec Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the dispatch console market size is projected to expand from USD 2.07 billion in 2025, USD 2.16 billion in 2026, to USD 2.70 billion by 2031, registering a 4.55% CAGR over 2026-2031.

This report is Segmented by Component (Hardware and Software), Type (IP-Based Dispatch Console and TDM-Based Dispatch Console), Functionality (Voice Dispatch, Text Dispatch, Geo-Location Services, Real-Time Monitoring, and More), End-User Industry (Public Safety Agencies, Government and Defense, Transportation and Logistics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Dispatch Console Market Trends and Insights

NG9-1-1 Deployments Speeding Up Console Upgrades

Federal and state mandates require call centers to accept voice, text, image, and video, prompting public safety agencies to scrap consoles incapable of multimedia Session Initiation Protocol feeds. Kansas, Oklahoma, and other early movers brought Emergency Services IP Networks online in 2026, validating that centrally funded programs can meet the 2026 federal target. Cost overruns in California, where spending already exceeds USD 450 million, underscore the budget risk when procurement is fragmented. Alongside hardware refreshes, agencies must modernize recording systems and training curricula, creating a bundled multi-year capital cycle. Vendors that certify equipment quickly and support phased cutovers gain an early-mover advantage.

Cloud-Native CAD and Dispatch Adoption in Logistics

Fleet operators increasingly subscribe to cloud dispatch suites that eliminate on-premises servers and allow supervisors to manage operations from any device. Requests for proposals in Georgia and Wisconsin call explicitly for near-zero downtime, browser-based interfaces, and analytics dashboards. Monthly fees convert capital outlays into operating expenses, shortening internal approval cycles and making solutions attractive to small and mid-sized fleets. Downtime risk shifts from local hardware to wide-area connectivity, so suppliers must bundle redundant telecommunications and rigorous Service Level Agreements to satisfy safety-critical use cases.

Slow Public Procurement and Budget Hurdles

Public safety agencies navigate multi-step approval chains, public hearings, and potential bid protests that can stretch contract awards to 18-36 months. Illinois surcharge revenue funds barely cover half of operational costs, forcing departments to defer console refreshes until state grants materialize. Similar delays in Argentina, where funding for a ARS 23 billion (USD 23 million) 911 upgrade is split across two budget cycles, illustrate how macro-economic swings derail even approved projects. Vendors must provide bridge warranties and flexible payment schedules to remain competitive.

Other drivers and restraints analyzed in the detailed report include:

- Grid Modernization Boosting Demand from Utilities

- Roll-Out of Public-Safety Broadband Networks

- High Cost of Cyber-Security Upgrades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware contributed 55.55% of 2025 sales as agencies continued to amortize consoles, radio gateways, and adjustable furniture over 7-10 years. A statewide contract in Oklahoma and county-level approvals in Kansas affirmed that purpose-built ergonomic desks still command a premium over generic office fixtures. Growth in software revenue outpaces hardware at 4.63% annually because cloud subscriptions, mapping extensions, and analytics modules transform one-time licenses into predictable monthly recurring charges. Where servers once required forklifts, new deployments spin up virtual machines in minutes, and updates push automatically after midnight. This shift cuts total cost of ownership yet locks agencies into vendor roadmaps, making exit switches expensive. As artificial intelligence workloads rise, hardware refreshes will require additional graphics processing, higher-resolution monitors, and 10 gigabit network uplinks, fueling incremental hardware sales even in a SaaS world.

The bundling trend continues: more than 60% of 2026 solicitations require a single integrator to supply furniture, radio interface, and software. Bundled deals simplify governance but put price pressure on smaller specialists that cannot finance multi-year warranties. Best-of-breed buyers insist on standards-based APIs and object-level data export so future migrations remain possible, but those clauses rarely appear in municipal RFP templates, perpetuating supplier lock-in.

IP-based consoles accounted for 67.75% revenue in 2025, yet the dispatch console market still sold thousands of TDM positions to mines, oil rigs, and rural utilities where deterministic latency and standalone reliability trump features. IP systems integrate seamlessly with broadband networks, support multimedia calls, and enable virtualized disaster-recovery positions, all compelling perks for urban agencies. Conversely, a 5.05% growth rate for TDM reflects emerging-market utilities laying new copper or microwave links where fiber is scarce. Interoperability gateways that translate between Session Initiation Protocol and circuit-switched signaling remain a thriving subsegment, as agencies avoid flash-cut migrations. The dispatch console market size for gateways is projected to reach USD 270 million by 2031, rising alongside hybrid architectures.

Vendor roadmaps suggest the inflection point will arrive as carriers sunset narrowband private lines in the late 2020s. Once service providers roll over to all-IP backbones, replacement demand will spike, compressing a decade of upgrades into a three-year window. Suppliers with field-swappable IP interface cards and pay-as-you-grow licensing will be positioned to capture the surge.

Geography Analysis

North America represented 36.67% of the dispatch console market in 2025. Multi-state contracts, such as Washington's USD 48 million statewide Emergency Services IP Network extension and New York's USD 85 million county grant program, underpin a visible pipeline through 2031. Canada mandated Next Generation 911 functionality nation-wide by 2027, releasing CAD 25 million (USD 18 million) funding tranches that accelerate console orders. Nonetheless, the removal of federal matching funds from the 2025 U.S. budget shifted financial burden to states, elongating procurement for smaller jurisdictions. FirstNet integration obliges additional certification, increasing deployment planning from six to nine months but, once complete, enabling high-bandwidth video and drone feeds to flow directly into consoles.

Asia-Pacific offers the fastest 4.76% CAGR. India's 100-city smart-city initiative rolled out Integrated Command and Control Centers that monitor 142,000-plus cameras, evidence of large orders for IP positions with advanced video analytics. China's megacity clusters replicate this at even larger scales, though domestic procurement policies favor local suppliers. Dubai's Enterprise Command and Control Center coordinates 28,000 vehicles and ingests 4.4 billion daily data points, showcasing the Middle Eastern appetite for high-throughput, AI-enabled consoles. Japan and South Korea focus on incremental upgrades, ensuring existing investments interface with 5G and autonomous vehicle trials without wholesale rip-and-replace.

Europe modernizes to meet Electronic Communications Code requirements. Contracts in the United Kingdom for Guardian Hub and 10-year mobile policing suites demonstrate willingness to commit long-term operating budgets. Hexagon's EUR 10 million (USD 11.3 million) acquisition of a European recording solutions provider strengthens interoperability offerings that fit EU data residency mandates. South America's opportunity is real but fragmented; provincial buyers in Argentina and Brazil publish sizable tenders yet face unpredictable foreign-exchange swings and constrained federal transfers. Middle East mega-projects such as Saudi Arabia's Qiddiya Smart Command Center create lighthouse references that vendors cite globally. Africa remains nascent but selected metros in South Africa, Nigeria, and Egypt are starting feasibility studies, hinting at a potential wave of greenfield IP console deployments late in the forecast horizon.

- Motorola Solutions, Inc.

- Hexagon AB

- CentralSquare Technologies, LLC

- Airbus SE

- Hytera Communications Corporation Limited

- L3Harris Technologies, Inc.

- Omnitronics Pty Limited

- Cisco Systems, Inc.

- RapidDeploy, Inc.

- EFJohnson Technologies, Inc.

- Catalyst Communications Technologies, Inc.

- Saab AB

- Telex Radio Dispatch

- Avaya LLC

- InterTalk Critical Information Systems

- Frequentis AG

- Esri, Inc.

- ZETRON Inc.

- Synch Systems, Inc.

- Avtec Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 NG9-1-1 Deployments Speeding Up Console Upgrades

- 4.2.2 Cloud-Native CAD and Dispatch Adoption in Logistics

- 4.2.3 Grid Modernization Boosting Demand from Utilities

- 4.2.4 Roll-Out of Public-Safety Broadband Networks

- 4.2.5 AI-Assisted Dispatch Optimising Response Workflows

- 4.2.6 Private 5G Pilots in Industrial Campuses Enabling IP Dispatch

- 4.3 Market Restraints

- 4.3.1 Slow Public Procurement and Budget Hurdles

- 4.3.2 High Cost of Cyber-Security Upgrades

- 4.3.3 Vendor Lock-In Risks in Integrated Suites

- 4.3.4 Scarcity of Dispatch-Ready Spectrum Bands Below 1 GHz

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Threat of Substitutes

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Bargaining Power of Buyers

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.2 By Type

- 5.2.1 IP-Based Dispatch Console

- 5.2.2 TDM-Based Dispatch Console

- 5.3 By Functionality

- 5.3.1 Voice Dispatch

- 5.3.2 Text Dispatch

- 5.3.3 Geo-Location Services

- 5.3.4 Real-Time Monitoring

- 5.3.5 Data Analytics and Reporting

- 5.4 By End-User Industry

- 5.4.1 Public Safety Agencies

- 5.4.2 Government and Defense

- 5.4.3 Transportation and Logistics

- 5.4.4 Healthcare

- 5.4.5 Manufacturing

- 5.4.6 Mining, Energy, and Utilities

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Kuwait

- 5.5.5.4 Bahrain

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Motorola Solutions, Inc.

- 6.4.2 Hexagon AB

- 6.4.3 CentralSquare Technologies, LLC

- 6.4.4 Airbus SE

- 6.4.5 Hytera Communications Corporation Limited

- 6.4.6 L3Harris Technologies, Inc.

- 6.4.7 Omnitronics Pty Limited

- 6.4.8 Cisco Systems, Inc.

- 6.4.9 RapidDeploy, Inc.

- 6.4.10 EFJohnson Technologies, Inc.

- 6.4.11 Catalyst Communications Technologies, Inc.

- 6.4.12 Saab AB

- 6.4.13 Telex Radio Dispatch

- 6.4.14 Avaya LLC

- 6.4.15 InterTalk Critical Information Systems

- 6.4.16 Frequentis AG

- 6.4.17 Esri, Inc.

- 6.4.18 ZETRON Inc.

- 6.4.19 Synch Systems, Inc.

- 6.4.20 Avtec Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

調度控制台市場規模、佔有率和成長分析:按組件、類型、功能、部署模式、應用和地區分類-2026-2033年產業預測

調度控制台市場規模、佔有率和成長分析:按組件、類型、功能、部署模式、應用和地區分類-2026-2033年產業預測 調度控制台市場 - 全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、地區和競爭格局分類,2021-2031年

調度控制台市場 - 全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、地區和競爭格局分類,2021-2031年 調度控制台市場:按組件、產品類型、應用、產業和銷售管道分類-2026-2032年全球市場預測

調度控制台市場:按組件、產品類型、應用、產業和銷售管道分類-2026-2032年全球市場預測 全球IP對講和公共廣播系統市場:按產品、最終用戶和競爭對手分類

全球IP對講和公共廣播系統市場:按產品、最終用戶和競爭對手分類 全球調度主機市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球無線電調度控制台市場(按類型、組件、設計、技術、連接性和應用)預測(2025-2030 年)

全球調度主機市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球無線電調度控制台市場(按類型、組件、設計、技術、連接性和應用)預測(2025-2030 年) 全球調度主機市場

全球調度主機市場 調度主機市場規模、佔有率、趨勢分析報告:按類型、按應用、按地區、細分市場預測,2025-2030 年

調度主機市場規模、佔有率、趨勢分析報告:按類型、按應用、按地區、細分市場預測,2025-2030 年