|

市場調查報告書

商品編碼

2062267

冷軋鋼捲:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Cold-Rolled Steel Coil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

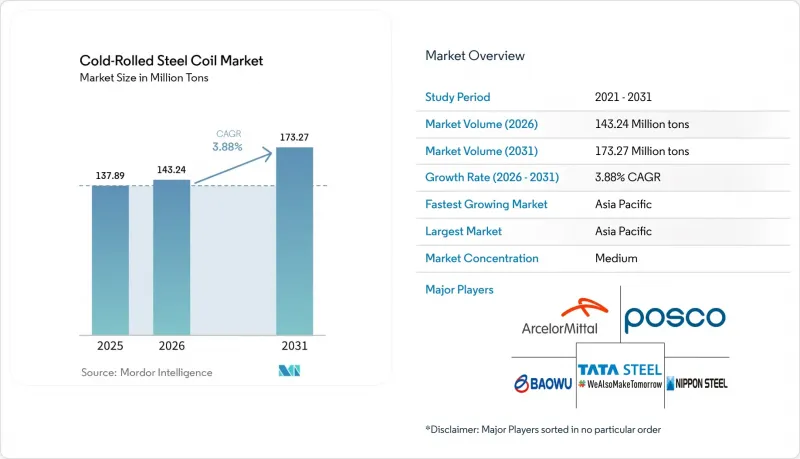

預計冷軋鋼捲市場規模將從 2025 年的 1.3789 億噸擴大到 2026 年的 1.4324 億噸,到 2031 年將達到 1.7327 億噸,預計 2026 年至 2031 年的複合年成長率為 3.88%。

本報告依鋼材等級(低碳鋼、高碳鋼、高強度低合金鋼等)、應用領域(汽車車體及結構件、消費性電子產品、工業機械及設備等)及地區(亞太地區、北美地區、歐洲地區、南美地區、中東及非洲地區)進行細分。市場預測以噸為單位。

全球冷軋鋼捲市場趨勢及洞察

來自汽車和消費性電子產業的需求不斷成長。

預計到2025年,電池式電動車)產量將達到1400萬輛,為了抵消電池重量並滿足碰撞安全標準,每款車型平台所需的先進熱穩定鋼(AHSS)用量將比傳統內燃機汽車高出15%至20%。 SSAB將於2025年推出抗張強度超過1500兆帕的電動車最佳化型AHSS,使汽車製造商能夠在保持結構完整性的前提下,將板材厚度減少10%至15%。中國和印度的冷藏庫和洗衣機製造商正在從傳統的0.6-0.7毫米厚的塗漆鋼捲轉向0.4-0.5毫米厚的塗漆鋼卷,從而降低高達12%的材料成本並減少能源標籤罰款。即使成熟經濟體的汽車組裝量趨於穩定,這兩種需求仍支撐著冷軋鋼捲市場。擁有高精度軋延和先進塗層技術的鋼廠最能抓住不斷成長的利潤空間,而通用鋼材製造商則面臨日益激烈的進口競爭。

在建築和基礎設施項目中得到更廣泛的應用

北美建築規範將於2024年至2025年間在多層建築和抗震應用中採用冷彎型鋼框架,從而將目標需求擴展到單戶住宅之外。光是在維吉尼亞、德克薩斯州和愛爾蘭,資料中心建設在2025年就將消耗約120萬噸鋼捲,用於框架、暖通空調管道和電纜配線架。在海灣合作理事會(GCC)國家,鋼鐵需求將在2025年加速成長,冷軋產品將用於太陽能發電廠的屋頂和海水淡化廠的覆材。歐洲和北美的模組化建築正在推動每年30萬至40萬噸的需求成長,但價格仍然十分敏感,如果鋼材溢價超過框架成本的20%,供應商將面臨替代品的風險。監管協調和勞動力短缺持續推動冷彎型鋼解決方案的發展,並支撐著非汽車產業冷軋鋼捲市場的成長動能。

原物料價格波動

2025年,鐵礦石交易價格在每噸90至130美元之間,而美國廢鋼價格則在每噸300至450美元之間,這使得沒有自有資源的生產商的利潤率下降了200至300個基點。像塔塔鋼鐵和克利夫蘭克里夫斯這樣的綜合性鋼鐵廠透過內部轉移定價來緩解價格波動的影響,而公司旗下的鋼鐵廠則直接受到現貨市場的影響。電弧爐(EAF)製造商在廢鋼價格低迷時受益,但當廢鋼價格比生鐵價格高出100美元時,其成本優勢便會喪失。這種供需失衡將持續到2027年,使冷軋鋼捲市場的價格協商更加複雜。

細分市場分析

2025 年冷軋鋼板捲市場中,低碳鋼佔出貨量的 46.61%,但隨著汽車製造商從傳統鋼材轉向高強度鋼以滿足平均車輛排放氣體目標,預計到 2031 年,高抗張強度鋼 (AHSS) 將以每年 4.55% 的速度成長。

冷軋不銹鋼捲材市場雖仍屬小眾,但盈利豐厚,尤其是在食品加工和化學工業。 Autokump 和 SSAB 等公司供應符合歐盟生態設計標準的低碳鋼,使利潤率提高了 40% 至 60%。由於電氣化導致驅動系統用鋼量減少,高碳鋼(AHSS) 或特殊不銹鋼,鋼廠在冷軋鋼捲材市場面臨邊際效益下降的風險。

區域分析

亞太地區到2025年將佔全球鋼鐵產量的59.94%,預計到2031年將以每年4.36%的速度成長,這主要得益於印度和東南亞產能的提升以及中國家用電器出口的成長。光是在印度,塔塔鋼鐵、JSW鋼鐵、AM/NS印度公司和暹羅金屬公司在2024年至2025年間就運作了350萬噸產能,以滿足國內需求和對歐盟的出口。越南到2025年產能將達800萬噸,其交付成本比東北亞鋼廠低10%至15%。

北美冷軋鋼板市場的成長主要得益於紐柯公司位於西維吉尼亞州的工廠(年產能300萬噸)和現代鋼鐵公司於2026年3月宣布的投資58億美元的美國待開發區電弧爐(EAF)項目等投資。墨西哥的佩斯克里亞綜合體(年產能150萬噸)使墨西哥根據美墨加協定(USMCA)的規定成為區域中心。

在歐洲,由於汽車產量停滯不前和能源成本高企,經濟成長正在放緩,但碳邊境調節機制(CBAM)的獎勵正推動波蘭、西班牙和義大利的產能回流。南美洲的成長主要得益於巴西和阿根廷汽車產業的復甦,而中東和非洲地區的成長預計將來自沙烏地阿拉伯和阿拉伯聯合大公國的基礎設施項目,其中包括EMSTEEL公司投資6.25億迪拉姆的擴建計劃,該計畫旨在滿足海灣合作理事會(GCC)國家的空調和建築需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 汽車和消費性電子產業的需求不斷成長

- 在建築和基礎設施項目中得到更廣泛的應用

- 軋延鋼板的優點:強度高,表面光潔度佳。

- 新興國家製造業的擴張

- 模組化建築和資料中心建設中的冷彎型鋼框架

- 市場限制因素

- 原料價格(鐵礦石和廢鋼)波動劇烈。

- 能源密集型製程和二氧化碳排放法規

- 鋁和複合材料在減重方面的替代方案

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按年級

- 低碳鋼

- 高碳鋼

- 高強度低合金鋼(HSLA)

- 先進高抗張強度鋼(AHSS)

- 不銹鋼

- 透過使用

- 汽車車體和結構件

- 電器產品

- 結構(屋頂、牆板、框架)

- 工業機械和設備

- 家具和儲物系統

- 包裝(桶、罐、容器)

- 電力、空調和暖氣

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- ArcelorMittal

- China Baowu Steel Group Corporation Limited

- Cleaveland-Cliffs Inc.

- CRS Holdings, LLC.

- Hyundai Steel

- JFE Steel Corporation

- JSW Steel

- Nippon Steel Corporation

- Nucor Corporation

- Outokumpu

- POSCO

- Salzgitter Flachstahl GmbH

- SSAB AB

- Tata Steel

- Thyssenkrupp Steel Europe

- United States Steel Corporation.

- Voestalpine Stahl GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the cold-Rolled steel coil market size is expected to increase from 137.89 Million tons in 2025 to 143.24 Million tons in 2026 and reach 173.27 Million tons by 2031, growing at a CAGR of 3.88% over 2026-2031.

This report is Segmented by Grade (Low-Carbon Steel, High-Carbon Steel, High-Strength Low-Alloy (HSLA) Steel, and More), Application (Automotive Body and Structural Parts, Consumer Appliances, Industrial Machinery and Equipment, and More), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Global Cold-Rolled Steel Coil Market Trends and Insights

Growing Demand From Automotive And Appliance Industries

Battery-electric-vehicle output reached 14 million units in 2025, each platform consuming 15%-20% more AHSS than its internal-combustion predecessor to offset battery mass and meet crash requirements. SSAB launched EV-optimized AHSS in 2025 with tensile strengths beyond 1,500 MPa, allowing automakers to trim gauge thickness 10%-15% while holding structural integrity. Refrigerator and washing-machine makers in China and India shifted to 0.4-0.5 mm pre-painted coil from traditional 0.6-0.7 mm, reducing material costs up to 12% and cutting energy-label penalties. These twin pulls sustain the cold-rolled steel coil market even where vehicle assembly flattens in mature economies. Mills with tight-tolerance rolling and advanced coating are best placed to capture expanding margins, whereas commodity producers face intensified import competition.

Increasing Use In Construction And Infrastructure Projects

North American building codes adopted cold-formed steel framing for multi-story and seismic applications in 2024-2025, widening addressable demand beyond single-family housing. Data-center construction in Virginia, Texas, and Ireland alone consumed roughly 1.2 million tons of coil in 2025 for framing, HVAC ducting, and cable trays. GCC countries registered an increase in steel-demand growth in 2025, channeling cold-rolled products into solar-farm roofing and desalination cladding. Modular building in Europe and North America adds 300,000-400,000 tons annually but stays price sensitive, exposing suppliers to substitution if steel premiums exceed 20% of framing cost. Regulatory alignment and labor shortages continue to favor cold-formed solutions, supporting the cold-rolled steel coil market trajectory in non-automotive sectors.

Volatile Raw-Material Prices

Iron ore traded between USD 90 and USD 130 per ton in 2025, while U.S. scrap ranged from USD 300 to USD 450 per ton, squeezing margins by 200-300 basis points for producers lacking captive resources. Integrated mills such as Tata Steel or Cleveland-Cliffs cushioned swings through internal transfer pricing, whereas merchant mills faced spot-market exposure. EAF operators benefited during scrap troughs but lost cost edge when scrap rose USD 100 above pig-iron parity. This asymmetry will persist into 2027, complicating price negotiations in the cold-rolled steel coil market.

Other drivers and restraints analyzed in the detailed report include:

- High-Strength And Surface-Finish Advantages Over Hot-Rolled Steel

- Manufacturing Expansion In Emerging Economies

- Energy-Intensive Processing And Carbon Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Low-carbon steel controlled 46.61% of 2025 volume in the cold-rolled steel coil market, yet Advanced High-Strength Steel (AHSS) is forecast to grow at 4.55% to 2031 as OEMs replace conventional grades to meet fleet-average emission targets.

Stainless cold-rolled coil remains a niche but lucrative slice, especially for food equipment and chemical processing, where Outokumpu and SSAB supply low-carbon variants meeting EU ecodesign norms at 40%-60% margin uplifts. High-carbon and HSLA steels trail overall growth as electrification reduces drivetrain steel content. Mills are unable to produce AHSS or specialty stainless risk margin compression within the cold-rolled steel coil market.

Geography Analysis

Asia-Pacific commanded 59.94% of 2025 volume, expanding at 4.36% through 2031 on the back of Indian and Southeast Asian capacity additions and Chinese appliance exports. India alone commissioned 3.5 million tons of new capacity across Tata Steel, JSW Steel, AM/NS India, and Shyam Metalics during 2024-2025 to satisfy domestic demand and EU-bound exports. Vietnam reached 8 million tons capacity in 2025 with delivered costs 10%-15% under Northeast Asian mills.

North America's cold-rolled steel coil market's growth is propelled by EAF investments such as Nucor's 3-million-ton West Virginia mill and Hyundai Steel's USD 5.8 billion U.S. greenfield EAF announced in March 2026. Mexico's 1.5 million-ton Pesqueria complex positions the country as a regional hub under USMCA rules.

Europe faces slower growth given stagnant auto output and high energy costs, yet CBAM incentives are triggering capacity reshoring to Poland, Spain, and Italy. South America's growth is led by Brazilian and Argentine automotive recovery, while the Middle East and Africa will advance on Saudi and UAE infrastructure pipelines, including EMSTEEL's AED 625 million expansion targeting GCC HVAC and construction buyers.

- ArcelorMittal

- China Baowu Steel Group Corporation Limited

- Cleaveland-Cliffs Inc.

- CRS Holdings, LLC.

- Hyundai Steel

- JFE Steel Corporation

- JSW Steel

- Nippon Steel Corporation

- Nucor Corporation

- Outokumpu

- POSCO

- Salzgitter Flachstahl GmbH

- SSAB AB

- Tata Steel

- Thyssenkrupp Steel Europe

- United States Steel Corporation.

- Voestalpine Stahl GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand from Automotive and Appliance Industries

- 4.2.2 Increasing Use in Construction and Infrastructure Projects

- 4.2.3 High-Strength and Surface-Finish Advantages over Hot-Rolled Steel

- 4.2.4 Manufacturing Expansion in Emerging Economies

- 4.2.5 Cold-Formed Steel Framing in Modular and Data-Center Builds

- 4.3 Market Restraints

- 4.3.1 Volatile Raw-Material (Iron-Ore And Scrap) Prices

- 4.3.2 Energy-Intensive Processing and Carbon Dioxide Regulations

- 4.3.3 Aluminium and Composites Substitution in Lightweighting

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Grade

- 5.1.1 Low-Carbon Steel

- 5.1.2 High-Carbon Steel

- 5.1.3 High-Strength Low-Alloy (HSLA) Steel

- 5.1.4 Advanced High-Strength Steel (AHSS)

- 5.1.5 Stainless Steel

- 5.2 By Application

- 5.2.1 Automotive Body and Structural Parts

- 5.2.2 Consumer Appliances

- 5.2.3 Construction (Roofing, Wall Panels, Framing)

- 5.2.4 Industrial Machinery and Equipment

- 5.2.5 Furniture And Storage Systems

- 5.2.6 Packaging (Drums, Barrels, Containers)

- 5.2.7 Electrical And HVAC

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 ArcelorMittal

- 6.4.2 China Baowu Steel Group Corporation Limited

- 6.4.3 Cleaveland-Cliffs Inc.

- 6.4.4 CRS Holdings, LLC.

- 6.4.5 Hyundai Steel

- 6.4.6 JFE Steel Corporation

- 6.4.7 JSW Steel

- 6.4.8 Nippon Steel Corporation

- 6.4.9 Nucor Corporation

- 6.4.10 Outokumpu

- 6.4.11 POSCO

- 6.4.12 Salzgitter Flachstahl GmbH

- 6.4.13 SSAB AB

- 6.4.14 Tata Steel

- 6.4.15 Thyssenkrupp Steel Europe

- 6.4.16 United States Steel Corporation.

- 6.4.17 Voestalpine Stahl GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

不鏽鋼圓棒市場 - 全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、地區和競爭格局分類,2021-2031年

不鏽鋼圓棒市場 - 全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、地區和競爭格局分類,2021-2031年 熱加工鋼筋市場:依等級、尺寸、最終用戶和通路分類-2026-2032年全球市場預測

熱加工鋼筋市場:依等級、尺寸、最終用戶和通路分類-2026-2032年全球市場預測 鋼筋市場:依產品類型、製造流程、表面處理、最終用途及地區分類,2026-2034年鋼筋市場:2026-2032年全球市場預測(依產品類型、材質、製造流程、鋼筋直徑、應用及最終用途產業分類)

鋼筋市場:依產品類型、製造流程、表面處理、最終用途及地區分類,2026-2034年鋼筋市場:2026-2032年全球市場預測(依產品類型、材質、製造流程、鋼筋直徑、應用及最終用途產業分類) 鋼筋市場:按類型、塗層、應用和地區分類

鋼筋市場:按類型、塗層、應用和地區分類 2026-2030年全球鋼筋市場

2026-2030年全球鋼筋市場 2026年全球鋼筋市場報告特種不鏽鋼棒材市場:依產品類型、製造流程、等級、應用和通路分類,全球預測(2026-2032年)軋延鋼棒材及型材市場:依產品、材質等級、最終用途及通路分類-2026-2032年全球預測日本鋼筋市場規模、佔有率、趨勢及預測(依產品類型、製程、表面處理類型、最終用途及地區分類,2026-2034年)

2026年全球鋼筋市場報告特種不鏽鋼棒材市場:依產品類型、製造流程、等級、應用和通路分類,全球預測(2026-2032年)軋延鋼棒材及型材市場:依產品、材質等級、最終用途及通路分類-2026-2032年全球預測日本鋼筋市場規模、佔有率、趨勢及預測(依產品類型、製程、表面處理類型、最終用途及地區分類,2026-2034年)