|

市場調查報告書

商品編碼

2062258

阻燃液壓油:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Fire Resistant Hydraulic Fluid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

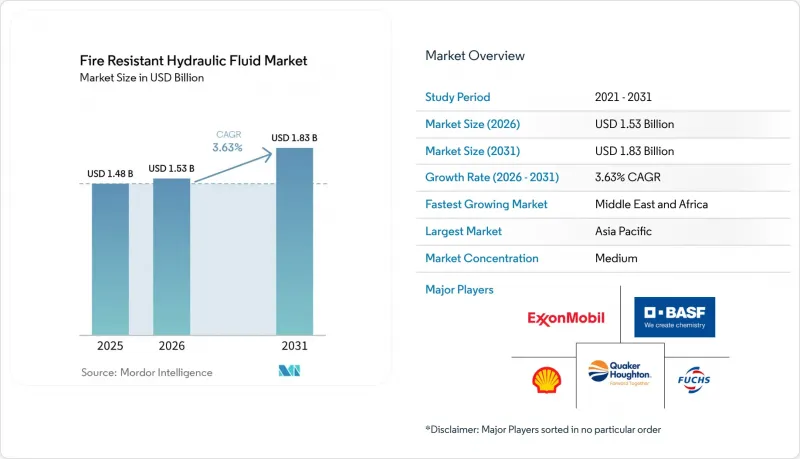

據 Mordor Intelligence 稱,2025 年阻燃液壓油市值為 14.8 億美元,預計到 2031 年將從 2026 年的 15.3 億美元成長至 18.3 億美元,預測期(2026-2031 年)複合年成長率為 3.63%。

本報告按流體類型(HFAE油包水乳液、HFAS合成溶液等)、應用領域(鋼鐵鑄造、採礦和隧道施工等)以及地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲)進行細分。市場預測以美元計價。

全球阻燃液壓油市場趨勢及洞察

自動化和電氣化提高了閃點閾閾值。

隨著移動機械電氣化的推進,將電池、逆變器和液壓驅動裝置整合到目的地的機身中,增加了火災風險,尤其是在使用礦物油的情況下。沃爾沃和Caterpillar等主要原始設備製造商 (OEM) 強制要求在電液轉向系統中使用阻燃液壓油,並採用專門設計的電路來降低電池相關火災的風險。使用電池驅動電動裝載機的地下礦井,透過從礦物油轉向使用 HFDU(高頻液壓導管)酯類液壓油,降低了保險費用。 HFDU 酯類油因其自熄性和在封閉隧道中低煙排放的特性而成為首選。採購團隊在推出新型號時,將符合 ISO 6743/4 HFDU 和 HFC(高頻液壓導管)標準作為優先考慮的指標。此外,在住宅附近作業的市政承包商也擴大選擇歐盟生態標籤認證的合成酯類油,因為它們毒性低、氣味小。這一趨勢凸顯了從設計階段就採用阻燃液壓油,而不是將其作為被動維修的轉變。

擴建配備電液變槳系統的離岸風力發電

最新的離岸風力發電機採用電油壓缸快速旋轉重達20噸的葉片,即使在高達50公尺/秒(m/s)的陣風中也能確保最佳的功率控制。這些變槳迴路在高達400巴的壓力下運行,必須在長時間靜止後立即做出反應,且不能發生空化現象。這項要求使得水性乳液無法使用,因為水性乳液在低溫和高鹽環境中容易發生分離。 OEM認證清單越來越傾向於HFDU酯類油,這類油即使在-25 度C的低溫下也能保持其體積模量,並為偏航驅動裝置中的青銅軸承提供卓越的潤滑性能。環保監管機構也強調了使用可生物分解潤滑油的必要性,尤其是在海上輪圈洩漏的情況下。隨著兆瓦級風力渦輪機在北海、台灣海峽和美國大西洋沿岸等地區部署,即使價格溢價高達20-25%,對高品質酯類油的需求依然旺盛,這是因為每個機艙需要反覆加註約1000公升的油液。這一趨勢正在推動阻燃液壓油市場的長期成長。

與密封件和彈性體的相容性有限,增加了維護負擔。

標準丁腈橡膠 (NBR) 密封件在接觸磷酸酯和某些酯類化學物質時會發生膨脹。此外,某些離子型流體在經過 70,000 次壓力循環後會降低氟橡膠 (FKM) 密封件的耐久性。因此,維修工程需要使用密封件套件,這會使零件成本增加高達 20%,對小規模企業來說是一個挑戰。另外,水-乙二醇基液壓油會腐蝕閥體中的鋅和鎂,除非採用特殊塗層來保護。這些相容性問題阻礙了現有設備的改造,並影響了阻燃液壓油市場的成長速度。

細分市場分析

到2025年,氫氟碳(HFC)水乙二醇將佔據阻燃液壓油市場31.22%的佔有率,這主要歸功於其成本優勢。這一點在鋼鐵廠的連鑄液壓系統中尤其明顯,因為其潤滑性差是一個重要因素。同時,通用液壓油(HFDU)酯類市場預計到2031年將以3.56%的複合年成長率成長。這一成長主要得益於船舶、礦業和建築業選擇符合FM 6930和ISO 15380標準的液壓油,以確保其免受水腐蝕。 Quaker Horton公司的「QUINTOLUBRIC 888」系列產品具有超過86%的生物分解性和357 度C的閃點,是海上起重機的推薦之選。 Total Energy 的「Hydransafe HFDU 46」閃點高達 310 度C,生物分解率超過 61%,使其成為磷酸鹽基液壓油的替代品,尤其是在日益嚴格的環境法規面前。磷酸鹽基液壓油 (HFDR) 因其 200 度C 的熱穩定性而在航太領域保持主導地位,但化學品註冊、評估、授權和限制 (REACH) 法規的強制性標籤要求正迫使終端用戶考慮替代方案。液壓油型水性乳液 (HFAE) 和液壓油型水溶液 (HFAS) 屬於油包水溶液,符合 30 CFR 75 法規,專為地下採礦設備設計。相較之下,聚亞烷基二醇 (PAG) 基液壓油和離子液體佔據特定的細分市場,但由於對其與密封件的兼容性研究仍在進行中,它們的市場佔有率總合仍低於 5%。

合成酯類雖然每公升成本高出約20%,但可透過預測性維護延長使用壽命,並降低生命週期成本溢價。來自風電、隧道掘進和水力發電等行業的原始設備製造商 (OEM) 的目的地進一步驗證了 HFDU 技術的有效性,並鞏固了其在未來配方中的地位。隨著環境、社會和管治(ESG) 要求的日益凸顯,業界正轉向使用酯類,促使人們重新評估阻燃液壓油市場的競爭策略。

區域分析

預計到2025年,亞太地區將佔全球銷售額的34.11%。這主要得益於中國鋼鐵生產以及印度哈德卡斯爾石油公司等本地供應商的推動。該地區的化學公司正透過提供價格極具競爭力的(每公斤2-5美元)的專用液壓油(HFDU),促進國內市場對該產品的需求。此外,由中國河北和山西兩省政府推行的綠色採礦措施也推動了可生物分解酯類的需求。同時,日本和韓國進口航空級磷酸酯,以滿足航太計畫嚴格的純度標準。

預計中東和非洲地區將經歷最快的成長,從2026年起年複合成長率將達到4.67%。這一成長主要得益於沙烏地阿拉伯和阿拉伯聯合大公國(阿拉伯聯合大公國)海上開採鑽機的建設,這些平台需要使用經工廠互助協會(FM)認證的液壓油以滿足保險要求。此外,紅海和蘇伊士灣新建的風發電工程也增加了對渦輪機液壓油的需求。在南非,由於金礦和鉑礦需要遵守更嚴格的地下防火法規,因此與氫化丁腈橡膠(HNBR)密封件相容的HFDU酯類液壓油的應用正在不斷擴大。

在北美,俄亥俄州和安大略省的乙二醇混合業務回流工作正在穩步推進,確保了五大湖區周邊鋼鐵廠的穩定供應。美國強勁的國防訂單支撐了磷酸酯的加工量,而大西洋沿岸的風力發電廠則推動了對酯類產品的穩定需求。在墨西哥,汽車鑄造廠正在轉型使用水-乙二醇基替代品,以滿足安全審核標準,這加強了《美墨加協定》(USMCA)下的跨國貿易。

歐洲,尤其是德國的重工業和英國的北海平台,是主要的消費市場。 REACH(化學品註冊、評估、授權和限制)法規下的毒性限制正在推動酯類替代,而歐盟的生態標籤法規則鼓勵採用可生物分解的選項,尤其是在阿爾卑斯山的水力發電設施中。雖然斯堪地那維亞的離岸風力發電行業的成長正在推動這一需求,但由於成本的考慮,東歐鋼鐵廠仍然更傾向於使用氫氟碳化合物(HFC)基液壓油。

南美洲雖然規模較小,但卻是具有重要戰略意義的地區。巴西的鐵礦石開採和阿根廷的近海探勘正在創造獨特的商機。然而,物流挑戰和外匯波動在短期內會減緩成長。儘管如此,與原始設備製造商 (OEM) 簽訂的服務合約正在為阻燃液壓油市場採用高品質酯類油奠定基礎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 自動化和電氣化的加速發展正在提高閃點閾閾值。

- 採用液壓變槳和錨碇系統的離岸風力發電平台擴建

- 太空產業安全關鍵液壓系統的發展

- 即時監測液壓油狀況可延長換油週期並降低總擁有成本。

- 關稅促使國內乙二醇混合物回歸市場:國內供應穩定性提高

- 市場限制因素

- 密封件/彈性體的相容性有限,增加了維護負擔。

- 磷酸酯原料供應瓶頸

- 原料價格波動和對環境、社會及公司治理 (ESG) 因素日益關注,導致氫氟碳化合物 (HFC) 的成本上升。

- 價值鏈分析

- 監理情勢

- 波特五力分析

第5章 市場規模與成長預測

- 按流體類型

- HFAE 油包水乳液

- HFAS合成溶液

- HFB水包油乳液

- HFC 乙二醇水溶液

- HFDR磷酸酯

- HFDU合成/酯

- 其他小眾化學品(聚丙烯酸酯、矽酮、離子液體)

- 透過使用

- 鋼鐵和鑄造

- 採礦和隧道建設

- 航空航太製造

- 發電(火力發電、核能、水力)

- 海上石油、天然氣和風能

- 建築和重型機械

- 汽車和金屬衝壓廠

- 其他行業(食品、壓鑄、造船)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Afton Chemical

- BASF

- Castrol Limited

- CLARIANT

- Exxon Mobil Corporation

- FUCHS

- Greenwood Aerospace

- Houghton International

- ICL

- Idemitsu Kosan

- Kawasaki KGR

- LANXESS

- Panolin AG

- Quaker Chemical Corporation

- Shell plc

- Sinopec Lubricants

- Solvay

- TotalEnergies

第7章 市場機會與未來展望

According to Mordor Intelligence, the fire resistant hydraulic fluid market size was valued at USD 1.48 billion in 2025 and is estimated to grow from USD 1.53 billion in 2026 to reach USD 1.83 billion by 2031, at a CAGR of 3.63% during the forecast period (2026-2031).

This report is Segmented by Fluid Type (HFAE Oil-In-Water Emulsion, HFAS Synthetic Solution, and More), Application (Steel and Foundry, Mining and Tunnelling, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Fire Resistant Hydraulic Fluid Market Trends and Insights

Automation and Electrification Raise Flash-Point Thresholds

As mobile machinery increasingly adopts electrification, the integration of batteries, inverters, and hydraulic drives into compact frames raises the risk of ignition, particularly in the presence of mineral oils. Major Original Equipment Manufacturers (OEMs) like Volvo and Caterpillar are mandating fire-resistant hydraulic fluids for electro-hydraulic steering systems and incorporating circuits designed to mitigate battery-related fires. Underground mines utilizing battery electric loaders have observed reduced insurance premiums when switching from mineral oils to HFDU (Hydraulic Fluid, Fire-Resistant, Synthetic Ester) esters. HFDU esters' self-extinguishing properties and minimal smoke emission in confined tunnels make them a preferred choice. Procurement teams are prioritizing ISO 6743/4 HFDU and HFC (Hydraulic Fluid, Fire-Resistant, Water-Containing) compliance as a standard for new model launches. Additionally, municipal contractors working near residential areas are increasingly opting for synthetic esters with EU Ecolabel credentials due to their low toxicity and odor profiles. This trend highlights a shift: fire-resistant hydraulic fluid products are now being integrated during the design phase rather than as retrofits.

Offshore Wind Expansion With Electro-Hydraulic Pitch Systems

Modern offshore wind turbines utilize electro-hydraulic cylinders to quickly pivot 20-ton blades, ensuring optimal power regulation even in 50 meters per second (m/s) wind gusts. These pitch circuits, operating at pressures up to 400 bar, must react promptly after periods of dormancy without succumbing to cavitation. This requirement eliminates the possibility of using water-based emulsions, which are prone to separation in cold, saline environments. OEM qualification lists are increasingly favoring HFDU esters, known for maintaining bulk modulus at -25°C and providing enhanced lubricity for bronze bearings in yaw drives. Environmental regulators are also emphasizing the need for fluids to be biodegradable, especially in scenarios of hub leakage at sea. With regions like the North Sea, Taiwan Strait, and the U.S. Atlantic coast introducing multi-megawatt turbines, each nacelle's recurring fill volume of nearly 1,000 liters is driving sustained demand for premium esters, even at a 20-25% price premium. This trend supports the long-term growth prospects of the fire-resistant hydraulic fluid market.

Seal and Elastomer Compatibility Limitations Elevate Maintenance Burden

Standard nitrile (NBR) seals can swell when exposed to phosphate-ester and certain ester chemistries. Additionally, some ionic fluids can reduce the durability of fluoroelastomer (FKM) seals after 70,000 pressure cycles. As a result, retrofit projects require seal kits, increasing component costs by up to 20%, which can be a challenge for smaller operators. Furthermore, water-glycol fluids may corrode zinc or magnesium in valve bodies unless mitigated by special coatings. These compatibility challenges hinder the conversion of installed equipment and impact the growth rate of the fire-resistant hydraulic fluid market.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Safety-Critical Hydraulics in Aerospace Production

- Real-Time Fluid Monitoring Extends Drain Intervals

- Phosphate-Ester Raw-Material Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Hydrofluorocarbon (HFC) water-glycol secured a 31.22% share of the fire-resistant hydraulic fluid market, primarily due to cost advantages. This was particularly evident in steel-mill caster hydraulics, which can accommodate its lower lubricity. Meanwhile, the market for Hydraulic Fluid Type Universal (HFDU) esters is set to grow at a 3.56% Compound Annual Growth Rate (CAGR) until 2031. This growth is driven by marine, mining, and construction fleets opting for fluids compliant with FM 6930 and ISO 15380, ensuring protection against water-related corrosion. Quaker Houghton's QUINTOLUBRIC 888 series offers over 86% biodegradability and a fire point of 357°C, making it a preferred choice for offshore cranes. TotalEnergies' Hydransafe HFDU 46, with a 310°C flash point and over 61% biodegradability, positions esters as alternatives to phosphate esters, especially as environmental regulations tighten. While phosphate-ester Hydraulic Fluid Type Resistant (HFDR) fluids maintain a niche leadership in aerospace due to their 200°C thermal stability, pressures from Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH) labeling are prompting end users to consider alternatives. Hydraulic Fluid Type Aqueous Emulsion (HFAE) and Hydraulic Fluid Type Aqueous Solution (HFAS) oil-in-water solutions are tailored for underground coal equipment, adhering to 30 CFR 75 regulations. In contrast, Polyalkylene Glycol (PAG)-based and ionic liquids, though occupying a specialty niche, hold a combined share of less than 5%, constrained by ongoing seal-compatibility research.

Synthetic esters, despite being priced about 20% higher per liter, offer extended service life through predictive maintenance, reducing the lifecycle premium. Endorsements from Original Equipment Manufacturers (OEMs) in sectors like wind, tunneling, and hydropower further validate HFDU technology, reinforcing its role in future formulations. As Environmental, Social, and Governance (ESG) mandates gain traction, the industry is shifting towards esters, prompting a reevaluation of competitive strategies in the fire-resistant hydraulic fluid market.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 34.11% of global revenue, supported by China's steel production and local suppliers like Hardcastle Petrofer in India. Chemical producers in the region are offering Hydraulic Fluid Designed for Use (HFDU) fluids at competitive rates of USD 2-5 per kg, driving domestic adoption. Additionally, government initiatives promoting green mining in China's Hebei and Shanxi provinces have increased demand for biodegradable esters. Meanwhile, Japan and South Korea are importing aviation-grade phosphate esters, ensuring compliance with stringent purity standards for aerospace programs.

The Middle East and Africa are projected to experience the fastest growth, with a Compound Annual Growth Rate (CAGR) of 4.67% from 2026. This growth is driven by offshore rigs in Saudi Arabia and the United Arab Emirates (UAE), which require Factory Mutual (FM)-approved fluids to meet insurance requirements. Furthermore, new wind concessions in the Red Sea and the Gulf of Suez are increasing demand for turbine hydraulic volumes. In South Africa, gold and platinum mines, adhering to stricter underground fire codes, are increasingly adopting HFDU esters compatible with Hydrogenated Nitrile Butadiene Rubber (HNBR) seals.

North America is benefiting from reshored glycol blending operations in Ohio and Ontario, ensuring a stable supply for steel plants around the Great Lakes. Steady defense orders in the United States (U.S.) are supporting phosphate ester throughput, while wind farms along the Atlantic coast are driving consistent demand for esters. In Mexico, automotive casting plants are transitioning to water-glycol alternatives to meet safety audit standards, strengthening cross-border trade under the United States-Mexico-Canada Agreement (USMCA).

Europe, led by Germany's heavy industry and platforms in the United Kingdom (U.K.) North Sea, is a key consumer. REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals) toxicity constraints are encouraging ester substitutions, and European Union (EU) Ecolabel regulations are promoting biodegradable options, particularly in Alpine hydropower assets. The growing offshore wind sector in Scandinavia is reinforcing this demand, while Eastern European steel mills continue to prefer Hydrofluorocarbon (HFC) fluids due to cost considerations.

South America, while smaller in scale, holds strategic importance. Brazilian iron-ore operations and offshore explorations in Argentina are creating niche opportunities. However, challenges such as logistical hurdles and currency fluctuations are moderating immediate growth. Nevertheless, service contracts with Original Equipment Manufacturers (OEMs) are laying the foundation for the adoption of premium esters in the fire-resistant hydraulic fluid market.

- Afton Chemical

- BASF

- Castrol Limited

- CLARIANT

- Exxon Mobil Corporation

- FUCHS

- Greenwood Aerospace

- Houghton International

- ICL

- Idemitsu Kosan

- Kawasaki KGR

- LANXESS

- Panolin AG

- Quaker Chemical Corporation

- Shell plc

- Sinopec Lubricants

- Solvay

- TotalEnergies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Acceleration of automation and electrification raises flash-point thresholds

- 4.2.2 Expansion of offshore wind platforms using hydraulic pitch and mooring systems

- 4.2.3 Growth of safety-critical hydraulics in aviation and aerospace production

- 4.2.4 Real-time fluid-condition monitoring extends drain intervals and lowers TCO

- 4.2.5 Tariff-driven reshoring of glycol blending improves domestic supply security

- 4.3 Market Restraints

- 4.3.1 Seal/elastomer compatibility limitations elevate maintenance burden

- 4.3.2 Supply bottlenecks for phosphate-ester raw materials

- 4.3.3 Feed-stock tariff volatility and ESG scrutiny inflate HFC costs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Fluid Type

- 5.1.1 HFAE Oil-in-Water Emulsion

- 5.1.2 HFAS Synthetic Solution

- 5.1.3 HFB Water-in-Oil Emulsion

- 5.1.4 HFC Water-Glycol Solution

- 5.1.5 HFDR Phosphate-Ester

- 5.1.6 HFDU Synthetic/Ester

- 5.1.7 Other Niche Chemistries (PAG, Silicone, Ionic liquids)

- 5.2 By Application

- 5.2.1 Steel and Foundry

- 5.2.2 Mining and Tunnelling

- 5.2.3 Aviation and Aerospace Manufacturing

- 5.2.4 Power Generation (Thermal, Nuclear, Hydro)

- 5.2.5 Offshore Oil, Gas and Wind

- 5.2.6 Construction and Heavy Equipment

- 5.2.7 Automotive and Metal-Press Shops

- 5.2.8 Other Industries (Food, Die-casting, Marine)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Afton Chemical

- 6.4.2 BASF

- 6.4.3 Castrol Limited

- 6.4.4 CLARIANT

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 FUCHS

- 6.4.7 Greenwood Aerospace

- 6.4.8 Houghton International

- 6.4.9 ICL

- 6.4.10 Idemitsu Kosan

- 6.4.11 Kawasaki KGR

- 6.4.12 LANXESS

- 6.4.13 Panolin AG

- 6.4.14 Quaker Chemical Corporation

- 6.4.15 Shell plc

- 6.4.16 Sinopec Lubricants

- 6.4.17 Solvay

- 6.4.18 TotalEnergies

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

2026年全球耐火砂漿市場報告2026年全球防火膠帶市場報告

2026年全球耐火砂漿市場報告2026年全球防火膠帶市場報告 防火膠帶市場:2026-2032年全球市場預測(按材料類型、黏合劑、形狀、應用和最終用途產業分類)耐火液壓油市場:按產品類型、性能特徵、最終用途和分銷管道分類的全球市場預測,2026-2032年2026年全球防火織物市場報告

防火膠帶市場:2026-2032年全球市場預測(按材料類型、黏合劑、形狀、應用和最終用途產業分類)耐火液壓油市場:按產品類型、性能特徵、最終用途和分銷管道分類的全球市場預測,2026-2032年2026年全球防火織物市場報告 耐火液壓油市場規模、佔有率及成長分析(按流體類型、應用產業及地區分類)-2026-2033年產業預測

耐火液壓油市場規模、佔有率及成長分析(按流體類型、應用產業及地區分類)-2026-2033年產業預測 全球防火織物市場:預測至 2032 年—按類型、材料、織物類型、處理流程、應用、最終用戶和地區進行分析

全球防火織物市場:預測至 2032 年—按類型、材料、織物類型、處理流程、應用、最終用戶和地區進行分析 全球防火膠帶市場

全球防火膠帶市場 全球防火織物市場(按類型、應用、加工、最終用途行業和地區分類)- 預測至 2030 年全球阻燃防護衣市場

全球防火織物市場(按類型、應用、加工、最終用途行業和地區分類)- 預測至 2030 年全球阻燃防護衣市場