|

市場調查報告書

商品編碼

2062252

多元羧酸醚:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Polycarboxylate Ether - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

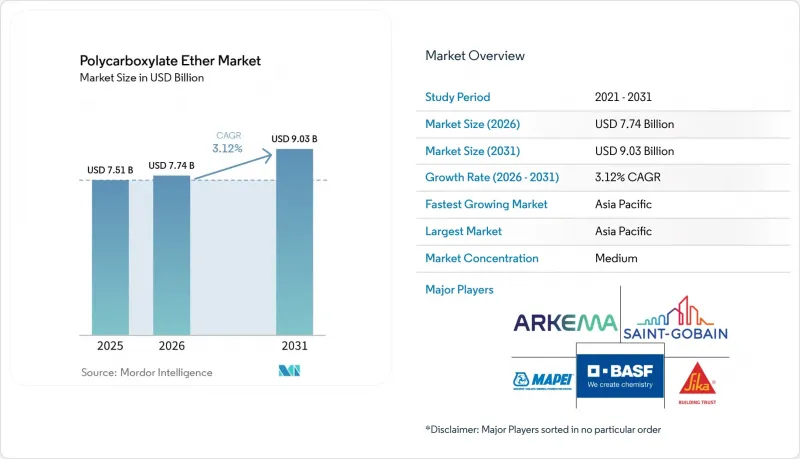

根據 Mordor Intelligence 預測,多元羧酸醚市場規模將從 2025 年的 75.1 億美元和 2026 年的 77.4 億美元成長到 2031 年的 90.3 億美元,2026 年至 2031 年的複合年成長率為 3.12%。

本報告按類型(MPEG基、TPEG基及其他)、形態(液體、粉末)、應用(預拌混凝土、高性能混凝土及其他)、終端用戶產業(住宅建築、商業建築及其他)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以美元計價。

全球多羧酸醚市場趨勢及洞察

亞太和非洲基礎建設投資快速成長

南亞、東南亞和非洲已共同撥款超過2,500億美元用於2026年至2028年規劃的交通走廊、電網和水利工程。光是亞洲開發銀行就為此撥款986億美元。這些資金正被投資於橋樑、公路和地鐵系統所需的混凝土,其中,由於TPEG基化學品能夠維持120分鐘的坍落度,因此在長距離泵送中備受青睞。非洲每年約1,700億美元的基礎設施缺口刺激了對粉狀外加劑的需求,可將運輸量減少70%,從而在內陸運輸中帶來顯著的成本優勢。預計到2031年,這些資本項目將推動聚羧酸醚市場以約1.2個百分點的複合年成長率成長。

加強綠建築標準中水灰比的規定。

加州柏克萊市的一項法令規定,面積超過5000平方英尺的項目,其水灰比不得超過0.40,這實際上強制要求使用高效減水劑,例如聚羧酸醚,以保持混凝土的可施工性。歐盟的環境產品聲明(EPD)系統對水泥以輔助材料取代15%至20%的混合物給予生命週期排碳權,但如果沒有高性能減水劑,這一目標很難實現。 LEED v5和BREEAM 2024現在對水灰比達到0.40或更低的樓板給予額外加分,這將在2031年之前持續推動結構需求的成長。

對不可生物分解聚合物殘留物的環境審查

歐盟《2023/2055號微塑膠法規》強制要求外加劑生產商記錄聚環氧乙烷側鏈的分解途徑。 2028年的審查可能會撤銷目前建築領域的豁免。同樣,美國環保署(EPA)更新的《有毒物質管制法》(TSCA)清單要求生產商揭露分子量分佈,這將使每種配方增加5萬至10萬美元的合規成本。這些壓力正在加速木質素基替代品的研究,此類替代品可減少28%至32%的用水量,但成本高出20%至25%。

細分市場分析

MPEG 的成本比 TPEG 低 20-25%,在 2025 年佔據了聚羧酸醚市場 41.14% 的佔有率。然而,由於 TPEG 在 35-45°C 的溫度下澆築後能保持 120 分鐘的坍落度,這對於偏遠地區的基建工程至關重要,因此預計 TPEG 在預測期(2026-2031 年)內將以 3.26% 的複合年成長率成長。如果目前的規格保持不變,到 2031 年,基於 TPEG 的聚羧酸醚市場規模可能會擴大,而 APEG 預計仍將是預製件領域的利基產品。BASF於 2025 年 5 月提高了 Pluriol A2400I 的產能,證實了市場對 TPEG 的需求正在加速成長。

區域趨勢各異。在中東的大型企劃中,TPEG被廣泛指定使用,而中國二線承包商則使用MPEG作為替代方案以贏得競標。在歐洲,隨著基礎建設導致運輸時間延長,TPEG的使用正在逐漸增加。由於原料和工藝瓶頸,預計到2031年,新興的木質素基和膦酸改性樹脂的市場佔有率將非常小,但在生物基和耐黏土性能至關重要的領域,它們有望以溢價出售。

2025年,液態產品佔多元羧酸醚市場規模的74.56%。這主要得益於其即插即用的批量生產能力。同時,粉狀產品預計在預測期(2026-2031年)內將以3.78%的複合年成長率成長,並在非洲、中東和中亞地區獲得市場佔有率。這些地區的長途海運和陸運成本預計將降低40%以上。即使粉狀產品的市佔率僅成長5個百分點,到2031年也能大幅提升其營收貢獻。

噴霧乾燥技術的進步已將溶解時間縮短至3分鐘內,消除了高產能工廠的一大操作障礙。在歐洲和北美,乾混砂漿和自流平砂漿中粉末級產品的採用,支持了即時預製策略,鞏固了一個高階細分市場,其售價比液體產品高出10%至15%。

區域分析

預計到2025年,亞太地區將佔據聚羧酸醚市場45.25%的佔有率,並在2031年之前保持3.79%的複合年成長率。印度的聚羧酸醚市場受益於預拌混凝土的擴張,那格浦爾、蘭契、賴布爾和甘地訥格爾等地新建的混凝土攪拌站推動了需求成長。同時,在中國,住宅市場下滑45%抑制了主要大都會圈的聚合物需求,但1兆元人民幣的基礎設施獎勵策略使2024年的混凝土產量維持在24億立方公尺。在正在實施東協互聯互通總體規劃走廊的東南亞國家,預計到2026年,聚羧酸醚在預拌混凝土市場的滲透率將達到約60%。

2025年,北美市場佔有率的提升得益於5,500億美元的《基礎設施投資與就業法案》,該法案為需要高性能混凝土的橋樑和寬頻基礎設施建設提供資金。該地區超大規模資料中心的激增也加速了市場成長。光是2025年,就有超過40個建設項目啟動,每個工程都指定使用超低收縮混凝土。西卡位於佛羅裡達州的自動化工廠於2025年12月投產,顯示當地產能正在擴大,以滿足美國東南部的需求。

歐洲市佔率反映出市場正從2023-2024年的低迷中復甦。德國和法國停滯的城市交通計畫正在重啟,東歐也正利用歐盟凝聚基金進行交通基礎建設升級改造。BASF提高了Pluriol A2400I的產量,確保了在日益嚴格的環境產品聲明(EPD)法規下,TPEG基產品的區域原料供應穩定。中東、非洲和南美洲市場均呈現高於平均的成長。在沙烏地阿拉伯和阿拉伯聯合大公國,TPEG聚合物被指定用於大型企劃,這些項目的施工現場溫度高達攝氏45度C;而在南非一個價值1兆蘭特(約594億美元)的基礎設施項目中,則使用了粉末級TPEG聚合物,以避免長途液體運輸的成本。隨著西卡公司擴大面向礦業和預拌混凝土(RMC)客戶的外加劑生產,巴西市場也呈現復甦跡象。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 亞太和非洲基礎建設投資快速成長

- 加強綠建築標準中水灰比的規定

- 二線城市預拌混凝土攪拌站的擴建

- 3D列印混凝土需要具有調整後的流變性能的高性能減水劑。

- 水冷資料中心的樓板需要使用超低收縮混凝土。

- 市場限制因素

- 不可生物分解聚合物殘留物的環境監測

- 與梳狀聚合物結構相關的專利密集區域

- LC3 和無機聚合物混凝土的興起導致 PCE 使用量減少。

- 價值鏈分析

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- MPEG系統

- APEG系統

- TPEG系統

- 其他

- 按形式

- 液體

- 粉末

- 透過使用

- 預拌混凝土(RMC)

- 預製混凝土

- 高性能混凝土

- 自密實混凝土

- 其他

- 按最終用戶行業分類

- 住宅

- 商業建築

- 基礎設施項目

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Arkema

- BASF

- Chembond Chemicals Limited

- CICO Group

- Dow

- Enaspol as

- Fosroc, Inc.

- Ha-Be Betonchemie GmbH

- Kao Chemicals Europe, SLU

- LOTTE Fine Chemical CO,.Ltd.

- MAPEI SpA

- MUHU (China) Construction Materials Co., Ltd.

- Saint-Gobain

- Sika AG

- Sobute New Materials Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the polycarboxylate ether market size is projected to expand from USD 7.51 billion in 2025 and USD 7.74 billion in 2026 to USD 9.03 billion by 2031, registering a CAGR of 3.12% between 2026 and 2031.

This report is Segmented by Type (MPEG-Based, TPEG-Based, and More), Form (Liquid and Powder), Application (Ready-Mix Concrete, High-Performance Concrete, and More), End-User Industry (Residential Construction, Commercial Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Polycarboxylate Ether Market Trends and Insights

Rapid Infrastructure Investment Across Asia-Pacific and Africa

South Asia, Southeast Asia, and Africa together earmarked more than USD 250 billion for transport corridors, power grids, and water projects slated for 2026-2028; the Asian Development Bank alone allocated USD 98.6 billion for that window. Funds are channeling toward concrete used in bridges, highways, and metro systems, where long-haul pumping favors TPEG-based chemistries thanks to 120-minute slump retention. Africa's annual infrastructure gap of roughly USD 170 billion is stimulating demand for powder-grade admixtures that cut freight volumes by 70%, a decisive cost advantage on landlocked routes. These capital programs collectively lift the Polycarboxylate Ether market by an estimated 1.2 percentage-point CAGR contribution through 2031.

Tightening Water-Cement-Ratio Rules in Green Building Codes

Municipal ordinances in Berkeley, California, cap water-cement ratios below 0.40 for projects above 5,000 ft2, effectively mandating high-range water reducers such as Polycarboxylate Ether products to maintain workability. The EU's Environmental Product Declaration scheme grants life-cycle-carbon credits for mixes that substitute 15-20% cement with supplementary materials, a target difficult to reach without advanced superplasticizers. LEED v5 and BREEAM 2024 now award extra points to slabs achieving the same sub-0.40 ratio, reinforcing a structural pull through 2031.

Environmental Scrutiny of Non-Biodegradable Polymer Residues

The European Union (EU) microplastics restriction 2023/2055 forces admixture producers to document degradation paths for polyethylene-oxide side chains; a 2028 review could rescind current construction exemptions. The U.S. EPA's updated Toxic Substances Control Act inventory likewise obliges manufacturers to disclose molecular-weight distributions, adding USD 50,000-100,000 compliance cost per formulation. These pressures accelerate research into lignin-based alternatives that deliver 28-32 % water reduction yet command 20-25 % higher cost.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of RMC Batching Plants in Tier-2 Cities

- 3D-Printed Concrete Needs Rheology-Tuned Super-Plasticizers

- Patent Thickets Around Comb-Polymer Architectures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

MPEG held 41.14% Polycarboxylate Ether market share in 2025 because its cost sits 20-25% below TPEG. TPEG, however, is forecast for a 3.26% CAGR during the forecast period (2026-2031) owing to 120-minute slump retention in 35-45°C pours, essential for remote infrastructure segments. The Polycarboxylate Ether market size for TPEG-based grades could rise by 2031 if current specifications persist, while APEG remains niche for precast. BASF's May 2025 boost in Pluriol A2400I capacity confirms accelerating TPEG demand.

Regional preferences diverge: Middle East megaprojects overwhelmingly specify TPEG, China's tier-2 builders substitute MPEG to win bids, and Europe is slowly pivoting toward TPEG as infrastructure specs lengthen transport windows. Emerging lignin-based and phosphonate-modified types are expected to have a minimal share by 2031, owing to feedstock and process bottlenecks, but may command premium pricing where bio-based or clay-tolerant credentials are mandated.

Liquid products dominated 74.56% of the Polycarboxylate Ether market size in 2025 due to plug-and-play batching. Powder forms, though, are anticipated to grow at 3.78% CAGR during the forecast period (2026-2031), taking share in Africa, the Middle East, and Central Asia, where freight savings exceed 40% on long ocean-plus-road voyages. A shift of even five percentage points toward powder could lift its revenue contribution substantially by 2031.

Dissolution times have shrunk below three minutes through spray-drying advances, removing the chief operational barrier for high-throughput plants. In Europe and North America, powder-grade uptake in dry-mix mortars and self-leveling compounds supports just-in-time prefabrication strategies, solidifying a premium sub-segment that sells at 10-15% price lifts over liquid equivalents.

Geography Analysis

Asia-Pacific commanded 45.25% of the Polycarboxylate Ether market share in 2025 and should sustain a 3.79% CAGR to 2031. India's Polycarboxylate Ether market is buoyed by a ready-mix expansion, with new batching plants in Nagpur, Ranchi, Raipur, and Gandhinagar driving uptake. Conversely, China's 45% residential downturn curtailed polymer demand in top-tier metros, though a CNY 1 trillion infrastructure stimulus preserved concrete production at 2.4 billion m3 in 2024. Southeast Asian nations executing the ASEAN Connectivity master-plan corridors increased Polycarboxylate Ether market penetration in ready-mix to roughly 60% by 2026.

North America's share in 2025 was strengthened by the USD 550 billion Infrastructure Investment and Jobs Act, which is channeling funds to bridges and broadband foundations requiring high-performance concrete. The region's hyperscale data-center boom is another accelerant: more than 40 sites broke ground in 2025 alone, each specifying ultra-low-shrinkage mixes. Sika's December 2025 automated plant in Florida demonstrates local capacity buildup to meet Southeastern U.S. demand.

Europe's market share reflects recovery from the 2023-2024 slump; Germany and France resumed stalled urban-mobility projects, while Eastern Europe leverages EU Cohesion Funds for transport upgrades. BASF's Pluriol A2400I expansion provides regional feedstock security for TPEG-based grades amid stricter EPD rules. The Middle East & Africa and South America exhibit above-average growth. Saudi Arabia and the UAE specify TPEG polymers for mega-projects facing 45°C site temperatures, whereas South Africa's ZAR 1 trillion (USD 59.4 billion) infrastructure pipeline uses powder grades to sidestep long-haul liquid shipping costs. Brazil's market is rebounding as Sika extends admixture output to serve mining and ready-mix clients.

- Arkema

- BASF

- Chembond Chemicals Limited

- CICO Group

- Dow

- Enaspol a.s.

- Fosroc, Inc.

- Ha-Be Betonchemie GmbH

- Kao Chemicals Europe, S.L.U.

- LOTTE Fine Chemical CO,.Ltd.

- MAPEI S.p.A.

- MUHU (China) Construction Materials Co., Ltd.

- Saint-Gobain

- Sika AG

- Sobute New Materials Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid infrastructure investment across Asia-Pacific and Africa

- 4.2.2 Tightening water-cement-ratio rules in green building codes

- 4.2.3 Expansion of RMC batching plants in tier-2 cities

- 4.2.4 3D-printed concrete needs rheology-tuned super-plasticizers

- 4.2.5 Liquid-cooled data-center slabs demand ultra-low-shrinkage mixes

- 4.3 Market Restraints

- 4.3.1 Environmental scrutiny of non-biodegradable polymer residues

- 4.3.2 Patent thickets around comb-polymer architectures

- 4.3.3 Rise of LC3 and geopolymer concrete reducing PCE dosage

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 MPEG-Based

- 5.1.2 APEG-Based

- 5.1.3 TPEG-Based

- 5.1.4 Others

- 5.2 By Form

- 5.2.1 Liquid

- 5.2.2 Powder

- 5.3 By Application

- 5.3.1 Ready-Mix Concrete (RMC)

- 5.3.2 Precast Concrete

- 5.3.3 High-Performance Concrete

- 5.3.4 Self-Compacting Concrete

- 5.3.5 Others

- 5.4 By End-user Industry

- 5.4.1 Residential Construction

- 5.4.2 Commercial Construction

- 5.4.3 Infrastructure Projects

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 NORDIC Countries

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Arkema

- 6.4.2 BASF

- 6.4.3 Chembond Chemicals Limited

- 6.4.4 CICO Group

- 6.4.5 Dow

- 6.4.6 Enaspol a.s.

- 6.4.7 Fosroc, Inc.

- 6.4.8 Ha-Be Betonchemie GmbH

- 6.4.9 Kao Chemicals Europe, S.L.U.

- 6.4.10 LOTTE Fine Chemical CO,.Ltd.

- 6.4.11 MAPEI S.p.A.

- 6.4.12 MUHU (China) Construction Materials Co., Ltd.

- 6.4.13 Saint-Gobain

- 6.4.14 Sika AG

- 6.4.15 Sobute New Materials Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

全球混凝土高性能減水劑市場

全球混凝土高性能減水劑市場 高性能混凝土減水劑市場:按類型、最終用途、形式和應用分類 - 2026-2032年全球市場預測

高性能混凝土減水劑市場:按類型、最終用途、形式和應用分類 - 2026-2032年全球市場預測 多元羧酸醚市場:依產品類型、建設產業和地區分類。

多元羧酸醚市場:依產品類型、建設產業和地區分類。 全球聚羧酸係高性能減水劑單體市場規模、佔有率、趨勢及成長分析報告(2026-2034)全球超塑性塑膠市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球聚羧酸係高性能減水劑單體市場規模、佔有率、趨勢及成長分析報告(2026-2034)全球超塑性塑膠市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 高性能混凝土減水劑市場規模、佔有率、趨勢及預測(按形式、產品類型、應用和地區分類,2026-2034年)

高性能混凝土減水劑市場規模、佔有率、趨勢及預測(按形式、產品類型、應用和地區分類,2026-2034年) 2026年全球多元羧酸醚市場報告

2026年全球多元羧酸醚市場報告 混凝土高效減水劑市場規模、佔有率和趨勢分析報告:按產品、應用、形態、地區和細分市場預測,2026-2033年

混凝土高效減水劑市場規模、佔有率和趨勢分析報告:按產品、應用、形態、地區和細分市場預測,2026-2033年 聚羧酸醚市場規模、佔有率及成長分析(按形態、聚合度、應用和地區分類)-2026-2033年產業預測

聚羧酸醚市場規模、佔有率及成長分析(按形態、聚合度、應用和地區分類)-2026-2033年產業預測 高效能節水器市場規模、佔有率及成長分析(按類型、形式、應用和地區分類)-2026-2033年產業預測

高效能節水器市場規模、佔有率及成長分析(按類型、形式、應用和地區分類)-2026-2033年產業預測