|

市場調查報告書

商品編碼

2062242

金融領域的數位雙胞胎:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Digital Twin In Finance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

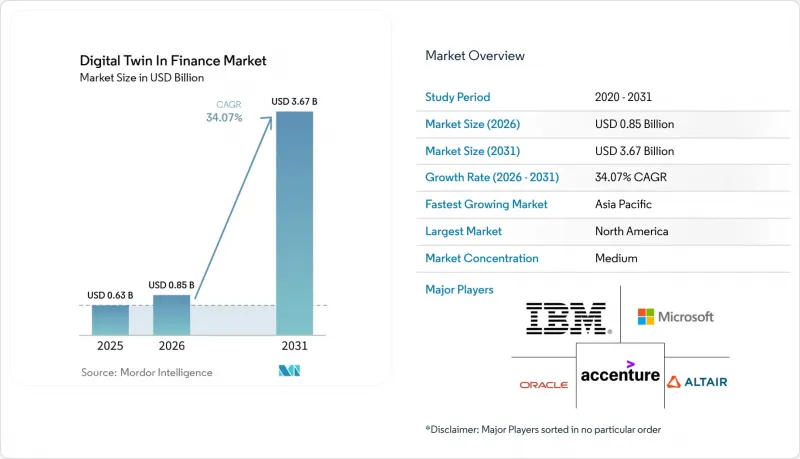

根據 Mordor Intelligence 預測,金融領域數位雙胞胎的市場規模預計在 2025 年達到 6.3 億美元,在 2026 年達到 8.5 億美元,在 2031 年達到 36.7 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 34.07%。

本報告按元件(軟體、平台等)、應用程式(風險管理、客戶體驗和個人化等)、部署方式(雲端、本地部署等)、組織規模(大型企業、中小企業)、最終用戶產業(銀行、保險等)和地區進行細分。市場預測以美元計價。

金融數位雙胞胎市場的全球趨勢與洞察

對即時風險管理的需求正在激增。

如今,各國央行和系統性機構依靠結算網路孿生技術在毫秒內模擬日內流動性衝擊,英格蘭銀行和加拿大支付協會的FNA實施計畫已展現了這項能力。貝萊德的Aladdin Risk平台每天處理約5,000個多重資產因子,並利用人工智慧輔助系統自動產生壓力測試情景,每周可為分析師節省10-15小時的工作時間。穆迪分析公司於2026年推出了Peril Metrics,整合了房地產情報和災害科學,使保險公司能夠針對特定位置重新評估投資組合。巴塞爾委員會2025-2026年的議程表明,監管機構將很快立法制定檢驗標準,加速強制實施。這些因素共同推動了金融市場對數位雙胞胎技術的應用,因為企業必須證明其資本和流動性即使在極端但現實的事件發生時也具有韌性。

銀行、金融服務和保險 (BFSI) 行業的雲端運算和人工智慧應用

混合雲端模式平衡了主權監管與GPU需求,從而能夠在生產規模上部署彈性運算和基於代理的AI工作流程。釘釘混合雲幫助一家香港金融機構實現了2.7倍的投資回報率和40%的成本降低,同時滿足了當地的數據監管要求。 IBM展示了多重雲端孿生聯盟,使銀行能夠在超大規模資料中心業者資料中心發生故障時立即進行容錯移轉轉移。微軟將於2026年3月為受監管產業提供符合歐盟《數位營運彈性法案》(DORA)的AI工作流程。星展銀行利用整合交易數據和情緒分析的生成孿生技術,將客戶身份驗證(KYC)流程縮短了33%,並將個人化驅動的轉換率提高了29%。快速且合規的計算正在顯著提升模擬的深度,並加速數位雙胞胎在金融市場的應用。

對資料隱私和網路安全的擔憂

客戶孿生體儲存著詳細的交易資料和推斷出的行為,因此極易成為駭客攻擊的目標,並引發了與授權相關的挑戰。國際證監會組織(IOSCO)的最終報告FR/17/2025將客戶孿生體歸類為非原生代幣,並指出當客戶孿生體與資料來源不一致時,資料所有權方面存在法律漏洞。 Banky Social Bank避免了3億新台幣(約980萬美元)的欺詐,但因未經明確授權推斷社交關係圖而受到審查。 Lucinity的一項調查發現,71%的公司使用基於客戶孿生體的詐欺偵測工具,但監管機構質疑資料保留期限是否違反了最小化原則。大規模資料外洩可能會暴露專有演算法,而安全措施也可能從單純的管理成本轉變為遏制金融市場採用數位雙胞胎的策略必要性。

細分市場分析

由於可組合的微服務,平台市場能夠實現分階段部署和快速整合,預計將以 35.03% 的複合年成長率成長。雖然預計到 2025 年軟體市場佔有率將達到 46.57%,但這主要反映的是與企業套件捆綁的傳統模擬引擎,而 SAP Signavio 和 Microsoft Azure數位雙胞胎現在已向第三方開發人員開放了可用的端點。隨著平台的普及,服務也將隨之發展,因為銀行仍需要流程映射和模型可解釋性方面的專家。

供應商的經濟效益有利於規模化發展。支付網路中每增加一個連接器,平台用戶留存率就會提高,並有助於簽訂多年合約。Accenture表明,整合商將平台專案視為諮詢交易的基礎。投資者在Twin Health融資2.83億美元時也表達了類似的觀點,這筆融資使其代謝健康數位孿生估值超過10億美元,並預示著跨行業的擴張。因此,預計該平台將在預測期內佔據金融數位雙胞胎市場的主導地位。

2025年,風險管理業務將佔總收入的30.21%,但隨著即時結算基礎設施的完善,無需批量處理即可進行審核,詐欺檢測業務預計將以34.98%的複合年成長率實現最高成長。 FICO的「聚焦序列模型」建構了行為分析模型,可減少即時結算中的誤報。 Aveni報告稱,警報噪音減少了60%,確認案例增加了22%,使員工能夠將資源分配到更深入的調查中。

嵌入行動應用中的客戶經驗孿生體能夠根據預測的情緒和行為對介面進行微調。流程自動化孿生體,例如PUY的配對工具,可將付款週期從T+1縮短至T+0,從而降低營運風險。合規孿生體能夠自動產生壓力測試模板,簡化向監管機構提交文件的流程。隨著房屋抵押貸款孿生體需要模擬託管時間,貿易融資孿生體需要複製國際貿易術語解釋通則和運輸里程碑,垂直領域的專業化程度正在不斷提高。這些細緻入微的需求正在推動數位雙胞胎在金融市場中的應用,以滿足特定應用場景的需求。

區域分析

預計到2025年,北美將佔據金融領域數位雙胞胎市場佔有率的35.19%,這得益於其強大的雲端基礎設施、熟練的人工智慧人才以及監管沙盒機制。美國經紀公司正在利用抵押品孿生來滿足即將訂定的氣候變遷資訊揭露要求,而加拿大支付公司(Payments Canada)則正在使用FNA RTGS孿生進行壓力測試。貝萊德的「阿拉丁風險」(Aladdin Risk)每天處理5000個因子,這顯示市場對規模化的需求十分強勁。穆迪的「風險指標」(Peril Metrics)允許美國保險公司逐個地塊地調整其房地產投資組合。各州隱私法要求在客戶孿生中加入同意邏輯,這影響了客戶孿生的應用特徵。

在歐洲,重點在於監管的清晰度,而非規模擴張。英國的數位證券沙盒於2023年啟動了分散式帳本技術試點項目,而歐盟的分散式帳本技術(DLT)試驗計畫在2025年初之前已向四家營運商頒發了許可證。巴塞爾委員會對數位化的關注表明,正式檢驗測試套件的開發將會取得進展。勞埃德銀行集團和Mapfle實施了韌性孿生模型,以滿足《企業永續發展報告指令》(CSRD)的最後期限要求。法國銀行的一項研究將洪水風險與違約機率聯繫起來,迫使該行實施環境、社會和治理(ESG)孿生模型。一家中東主權財富基金利用RiskThinking.ai的氣候變遷孿生模型將其資本緩衝減少了20%。一家非洲行動支付公司正在試驗流動性孿生模型,而一家南美監管機構正在製定相關法規之前,密切關注海外的試點計畫。

亞太地區以35.14%的複合年成長率 (CAGR) 領跑,這主要得益於各國監管機構批准了必須即時監控風險的數位銀行。印度的統一支付介面 (UPI) 每月處理超過120億筆交易,需要在不到一秒的時間內偵測出詐欺行為。星展銀行利用生成式孿生技術將客戶身份驗證 (KYC) 時間縮短了三分之一。Accenture收購Percipient增強了其獲取本地實施人才的能力。台灣的中國信託銀行和Bankee社會銀行已成功部署了詐欺預防孿生技術,準確率高達98.7%。在香港,釘釘的混合雲端正在幫助企業降低成本並提高合規性。新加坡金融管理局 (MAS) 和印度儲備銀行 (RBI) 的區域監管法規正在指南供應商風險評估,規範混合部署,並推動數位雙胞胎技術在金融市場的發展勢頭。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對即時風險管理的需求正在激增。

- 銀行、金融服務和保險 (BFSI) 行業的雲端運算和人工智慧應用

- 個性化主導的客戶孿生

- 專注於流程效率和成本降低

- 監管沙箱中的強制性壓力測試

- 用於 ESG 和氣候情境的數位雙胞胎

- 市場限制因素

- 對資料隱私和網路安全的擔憂

- 整合舊有系統的複雜性

- 前期成本高,投資報酬率不明確

- 演算法偏差導致的合規風險

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章:預測市場規模與成長率

- 按組件

- 軟體

- 平台

- 服務

- 透過使用

- 風險管理

- 客戶體驗與個人化

- 流程最佳化和自動化

- 合規與監理報告

- 詐欺檢測與預防

- 透過部署方法

- 雲

- 現場

- 混合

- 按公司規模

- 大公司

- 中小企業

- 按最終用戶行業分類

- 銀行

- 保險

- 資本市場和投資銀行

- 金融科技和支付

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- ASEAN

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- International Business Machines Corporation(IBM)

- Microsoft Corporation

- Oracle Corporation

- Accenture plc

- Altair Engineering Inc.

- Siemens AG

- Dassault Systemes SE

- SAP SE

- TIBCO Software Inc.

- ANSYS, Inc.

- Hexagon AB

- PTC Inc.

- Schneider Electric SE

- CGI Inc.

- Finastra Group Holdings Limited

- Palantir Technologies Inc.

- Kyriba Corp.

- Moody's Analytics, Inc.

- BlackRock, Inc.

- NCR Voyix Corporation

- Simudyne Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the digital twin in finance market size is projected to be USD 0.63 billion in 2025, USD 0.85 billion in 2026, and reach USD 3.67 billion by 2031, growing at a CAGR of 34.07% from 2026 to 2031.

This report is Segmented by Component (Software, Platforms, and More), Application (Risk Management, Customer Experience and Personalization, and More), Deployment Mode (Cloud, On-Premises, and More), Organisation Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (Banking, Insurance, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Digital Twin In Finance Market Trends and Insights

Real-Time Risk-Management Demand Surges

Central banks and systemically important institutions now depend on payment-network twins that simulate intraday liquidity shocks within milliseconds, a capability proved by FNA deployments at the Bank of England and Payments Canada. BlackRock's Aladdin Risk platform processes roughly 5,000 multi-asset factors daily and uses AI co-pilots to automatically generate stress scenarios, cutting analyst effort by 10-15 hours per week. Moody's Analytics added Peril Metrics in 2026, blending property intelligence with catastrophe science to enable insurers to re-underwrite portfolios at the individual-location level. The Basel Committee's 2025-2026 agenda signals that supervisors will soon codify validation standards, accelerating mandatory uptake. These factors jointly propel the digital twin in the finance market because firms must demonstrate resilient capital and liquidity under extreme but plausible events.

Cloud and AI Adoption Across BFSI

Elastic compute and agentic AI workflows hit production scale once hybrid-cloud models reconciled sovereignty rules with GPU demand. DingTalk Hybrid Cloud delivered a 2.7X return on investment and 40% cost savings for Hong Kong institutions while meeting local data mandates. IBM showcases multi-cloud twin federation to enable banks to fail over instantly if a hyperscaler falters. Microsoft enabled regulated-industry AI workflows in March 2026, aligning with the European Union's Digital Operational Resilience Act. DBS Bank shortened know-your-customer processing by 33% and lifted personalization conversion by 29% using generative twins that synthesize transactions and sentiment. Rapid, compliant compute unlocks new simulation depths, fuelling the digital twin in the finance market.

Data-Privacy and Cybersecurity Concerns

Customer twins pool granular transactions and inferred behaviors, making them lucrative targets for hackers and raising consent challenges. IOSCO's Final Report FR/17/2025 framed twins as non-native tokens and flagged legal gaps around data ownership when the twin and source diverge. Bankee Social Bank avoided NTD 300 million (USD 9.8 million) in fraud but faced scrutiny over social graph inference without explicit approval. Lucinity found 71% of firms use twin-driven fraud tools, yet regulators question whether retention periods breach minimization rules. A large breach could expose proprietary algorithms, turning security from a control cost into a strategic necessity that tempers the adoption of digital twins in the finance market.

Other drivers and restraints analyzed in the detailed report include:

- Personalization-Driven Customer Twins

- Process-Efficiency and Cost-Reduction Focus

- Legacy-System Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platforms are set to grow at a 35.03% CAGR, thanks to composable microservices that enable incremental rollouts and quick integrations. The 46.57% software share in 2025 reflected legacy simulation engines bundled in enterprise suites, but SAP Signavio and Microsoft Azure Digital Twins now expose open endpoints that third-party developers can consume. Services follow platform uptake as banks still need process mapping and model explainability experts.

Vendor economics favor scale: every new connector to a payment rail boosts platform stickiness, encouraging multi-year commitments. Accenture's 2025 purchase of Percipient suggests that integrators expect platform programs to anchor consulting pipelines. Investors echoed that view when Twin Health raised USD 283 million, valuing its metabolic-health twin above USD 1 billion and signaling cross-sector reach. As a result, platforms are on course to capture disproportionate market share in the finance digital twin market over the forecast horizon.

Risk-management twins accounted for 30.21% of revenue in 2025, but fraud twins will post the fastest 34.98% CAGR as real-time rails erase batch-review windows. FICO's Focused Sequence Models build behavioral twins that cut false positives for instant payments. Aveni reported 60% lower alert noise and 22% higher confirmed cases, enabling staff to redeploy to deeper investigations.

Customer-experience twins embedded in mobile apps fine-tune interfaces based on predicted sentiment and behavior. Process-automation twins, such as PUY's reconciler, move settlement from T+1 to T+0, shrinking operational risk. Compliance twins autogenerate stress-test templates, easing supervisory submissions. Vertical specialization is rising because a mortgage twin must model escrow timings, whereas a trade-finance twin must emulate incoterms and vessel milestones. These nuanced needs reinforce the expansion of the digital twin in the finance market for application-specific solutions.

Geography Analysis

North America held 35.19% of the digital twin market share in finance in 2025, thanks to deep cloud infrastructure, skilled AI talent, and supervisory sandboxes. U.S. broker-dealers use collateral twins to satisfy upcoming climate disclosures, while Payments Canada adopts FNA RTGS twins for stress scenarios. BlackRock's Aladdin Risk processes 5,000 factors daily, signaling a strong appetite for scale. Moody's Peril Metrics lets U.S. insurers adjust property portfolios at the parcel level. State privacy laws enforce consent logic in customer twins, shaping deployment features.

Europe moves on regulatory clarity instead of scale. The United Kingdom's Digital Securities Sandbox enabled ledger pilots in 2023, and the European Union's DLT Pilot licensed four operators by early 2025. The Basel Committee's focus on digitalization implies the development of formal validation test suites ahead. Lloyds Banking Group and Mapfre implemented resilience twins to meet the timelines of the Corporate Sustainability Reporting Directive. Banque de France research links flood exposure to probability of default, pushing banks toward ESG twins. Middle East sovereign funds use RiskThinking.ai climate twins to trim capital buffers by 20%. African mobile-money firms experiment with liquidity twins, while South American supervisors monitor overseas pilots before writing rules.

Asia-Pacific delivers the fastest 35.14% CAGR as domestic regulators green-light digital banks that must monitor risk in real time. India's Unified Payments Interface processes more than 12 billion monthly transactions, which demand sub-second fraud detection. DBS cut know-your-customer times by a third using generative twins. Accenture's Percipient buyout deepens local implementation talent. Taiwan's CTBC Bank and Bankee Social Bank deploy anti-fraud twins with 98.7% accuracy. DingTalk Hybrid Cloud shows cost and compliance gains in Hong Kong. Regional rules from the Monetary Authority of Singapore and the Reserve Bank of India guide vendor risk assessments, making hybrid deployments the norm and sustaining digital twin momentum in the finance market.

- International Business Machines Corporation (IBM)

- Microsoft Corporation

- Oracle Corporation

- Accenture plc

- Altair Engineering Inc.

- Siemens AG

- Dassault Systemes SE

- SAP SE

- TIBCO Software Inc.

- ANSYS, Inc.

- Hexagon AB

- PTC Inc.

- Schneider Electric SE

- CGI Inc.

- Finastra Group Holdings Limited

- Palantir Technologies Inc.

- Kyriba Corp.

- Moody's Analytics, Inc.

- BlackRock, Inc.

- NCR Voyix Corporation

- Simudyne Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Real-time Risk-Management Demand Surges

- 4.2.2 Cloud and AI Adoption Across BFSI

- 4.2.3 Personalization-Driven Customer Twins

- 4.2.4 Process-Efficiency and Cost-Reduction Focus

- 4.2.5 Regulatory Sandbox Stress-Test Mandates

- 4.2.6 ESG and Climate-Scenario Digital Twins

- 4.3 Market Restraints

- 4.3.1 Data-Privacy and Cybersecurity Concerns

- 4.3.2 Legacy-System Integration Complexity

- 4.3.3 High Up-Front Cost and Uncertain ROI

- 4.3.4 Algorithmic-Bias Compliance Exposure

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Platforms

- 5.1.3 Services

- 5.2 By Application

- 5.2.1 Risk Management

- 5.2.2 Customer Experience and Personalisation

- 5.2.3 Process Optimisation and Automation

- 5.2.4 Compliance and Regulatory Reporting

- 5.2.5 Fraud Detection and Prevention

- 5.3 By Deployment Mode

- 5.3.1 Cloud

- 5.3.2 On-premises

- 5.3.3 Hybrid

- 5.4 By Organisation Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-sized Enterprises (SMEs)

- 5.5 By End-User Industry

- 5.5.1 Banking

- 5.5.2 Insurance

- 5.5.3 Capital Markets and Investment Banking

- 5.5.4 Fintech and Payments

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Netherlands

- 5.6.2.7 Russia

- 5.6.2.8 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 ASEAN

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 Saudi Arabia

- 5.6.4.2 United Arab Emirates

- 5.6.4.3 Turkey

- 5.6.4.4 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Nigeria

- 5.6.5.3 Egypt

- 5.6.5.4 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 International Business Machines Corporation (IBM)

- 6.4.2 Microsoft Corporation

- 6.4.3 Oracle Corporation

- 6.4.4 Accenture plc

- 6.4.5 Altair Engineering Inc.

- 6.4.6 Siemens AG

- 6.4.7 Dassault Systemes SE

- 6.4.8 SAP SE

- 6.4.9 TIBCO Software Inc.

- 6.4.10 ANSYS, Inc.

- 6.4.11 Hexagon AB

- 6.4.12 PTC Inc.

- 6.4.13 Schneider Electric SE

- 6.4.14 CGI Inc.

- 6.4.15 Finastra Group Holdings Limited

- 6.4.16 Palantir Technologies Inc.

- 6.4.17 Kyriba Corp.

- 6.4.18 Moody's Analytics, Inc.

- 6.4.19 BlackRock, Inc.

- 6.4.20 NCR Voyix Corporation

- 6.4.21 Simudyne Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment