|

市場調查報告書

商品編碼

2062237

幀採集卡:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Frame Grabber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

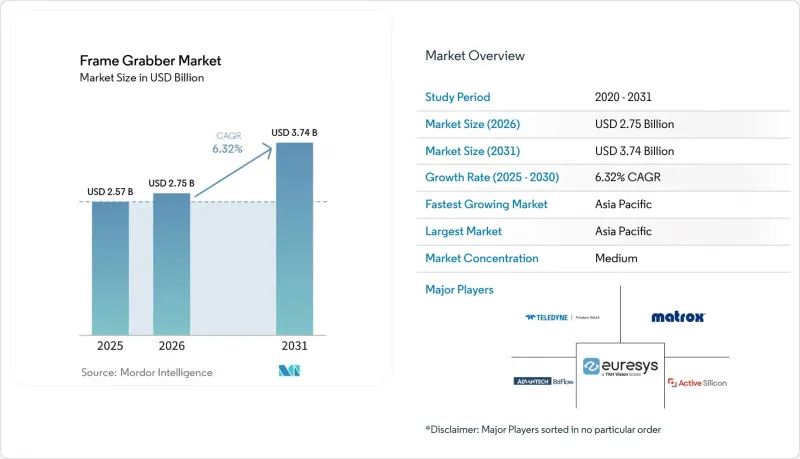

根據 Mordor Intelligence 預測,幀擷取器市場將從 2025 年的 25.7 億美元成長到 2026 年的 27.5 億美元,到 2031 年達到 37.4 億美元,2026 年至 2031 年的複合年成長率預計為 6.32%。

本報告按介面類型(Camera Link、Coaxpress、Gige Vision 等)、主機匯流排和外形規格(PCIe 和 PCI 卡、USB 外部擷取單元等)、影格速率能力(最高 60 FPS、60–120 FPS 等)、應用產業(工業和製造業、電子和半導體測試等)以及地區進行細分。市場預測以美元 (USD) 為單位。

全球影像擷取卡市場趨勢及洞察

生產線上擴大採用像素超過5000萬的影像感測器。

Canon的4.1億像素CMOS感測器和SONY的IMX927(1.05億像素)感測器,以每秒100幀的速度運行,充分體現了解析度的提升,迫使生產線整合商用和CoaXPress 2.0和Camera Link HS介面取代傳統的Camera Link Base和GigE Vision介面。以每秒100幀的速度拍攝的單張1.05億像素影像每秒會產生約10.5GB的原始拜耳數據,遠超過標準GigE Vision每秒Gigabit的頻寬限制。這種頻寬不匹配迫使製造商採用總合吞吐量超過每秒10GB的影像擷取卡,從而推動了對PCIe Gen4卡和CoaXPress多鏈路配置的需求。意法半導體的500萬像素混合式全快門/捲百葉窗感測器進一步說明了應用特定成像的趨勢,這種趨勢需要一種靈活的影像擷取卡架構,能夠在處理過程中切換全百葉窗和捲百葉窗模式。向像素超過 5000 萬的感測器的轉變在半導體晶圓檢測、平板顯示器缺陷檢測和汽車白車身測量中最為明顯,亞微米解析度直接轉化為更高的良率和更低的保固成本。

工業4.0的部署需要即時影像處理

工業4.0架構要求封閉回路型控制,從影像擷取到執行器響應的延遲小於10毫秒。這項要求使得基於FPGA且具備預處理能力的影像擷取卡優於運行在通用CPU上的純軟體管線。 Gidel的Proc1C10N影像擷取卡將每秒143兆次運算的INT8推理能力直接整合到擷取卡上,無需將像素資料四捨五入到主機GPU即可實現即時缺陷分類。這種板載智慧可緩解多攝影機單元中的網路擁塞,並保證即使在其他工作負載爭用主機資源的情況下也能實現確定性延遲。 Basler與西門子於2023年11月夥伴關係,將pylon SDK整合到西門子的工業邊緣設備中。這使得工廠營運商能夠將視覺應用部署為容器化的微服務,從而實現跨整條生產線的橫向擴展。時變網路協定、用於機器間通訊的 OPC UA 以及確定性幀捕獲器的融合,使得成像不再只是事後考慮的檢查步驟,而是成為工業IoT堆疊中的一流組件。

取代獨立影像擷取卡的智慧型相機

Allied Vision 的 Alecs 智慧相機整合了一個 NVIDIA Jetson Orin NX 模組,其 AI 性能高達每秒 100 兆次運算,無需單獨的影像擷取卡或主機,即可在裝置端進行缺陷分類、光學字元辨識和尺寸測量等推理。同樣,Teledyne 的 BOA3 AI 相機也整合了一個神經網路加速器,可在邊緣端處理影像,僅透過千兆乙太網路或 USB3 傳輸元資料和警報訊號,從而將網路頻寬降低兩個數量級。這種架構轉變適用於單相機即可滿足需求、安裝空間有限且專用影像擷取卡或主機成本過高的應用場景。然而,智慧相機在多相機同步場景、需要確定性延遲的應用(例如手術機器人)以及需要存檔未壓縮像素資料以實現可追溯性的高通量偵測單元中表現不佳。同時,幀擷取卡生態系統透過提供硬體觸發擷取(可在數十個攝影機上實現亞微秒級抖動)、基於 FPGA 的即時處理(可避免作業系統調度延遲)以及直接存取 GPU 記憶體(可加速推理流程)等方式,在這些細分領域保持著主導地位。

細分市場分析

從介面型影像擷取卡市場的規模來看,CoaXPress 預計到 2025 年將佔據 38.19% 的市場佔有率,複合年成長率 (CAGR) 為 6.97%,優於 Camera Link 和 GigE 等替代解決方案,並預示著其市場佔有率將在 2031 年前保持穩定成長。 CoaXPress 結合了每鏈路 12.5 Gbps 的傳輸速度和供電功能,從而簡化了線連接並延長了傳輸距離。這些特性對於半導體晶圓檢測和汽車噴漆室等應用至關重要。 Camera Link 由於其在航太和醫療 X光領域的穩固基礎,在現有設施維修項目中仍然適用,但對於新建項目而言,CoaXPress 2.0 和 Camera Link HS 的應對力和擴充性更勝一籌。 GigE Vision 雖然成本效益高,但封包遺失和 CPU 開銷會阻礙精確偵測,使其僅適用於分散式或對成本敏感的任務。

前瞻性的需求集中在CoaXPress 3.0草案標準上,該標準旨在實現單鏈路25 Gbps的傳輸速度,為平板顯示器測量領域單線纜2億像素相機鋪平道路。雖然Camera Link HS在需要抗輻射加固組件的領域仍然擁有一定的支援基礎,但工程領域的焦點正在轉向CoaXPress。 USB3 Vision由於其廣泛的應用和即插即用的便利性,在手持掃描器和實驗室設備中仍然佔據一定地位,但其5 Gbps的傳輸速度限制了中等影格速率下低於2000萬像素的解析度。因此,CoaXPress將繼續保持影像擷取卡市場的領先地位,定義效能預期並影響競爭對手的藍圖。

預計到2025年,PCIe和PCI卡將佔總銷售額的46.52%,反映出塔式和機架式工作站仍佔據傳統視覺架構的主導地位。緊湊型邊緣設備的興起使得M.2和Thunderbolt模組備受關注,預計到2031年,其複合年成長率將達到7.03%。 M.2模組直接連接到PCIe通道,其尺寸小於信用卡,因此可實現無風扇設計,並可安裝在機械臂背面或平板電腦內部。 Thunderbolt 4提供40 Gbps的總頻寬、菊鏈連接和熱插拔功能,從而降低了可攜式測試設備的安裝成本。

符合 PC/104 和 CompactPCI 標準的嵌入式闆卡仍然應用於航太和國防領域,因為這些領域對衝擊和振動的要求遠超商用 PC 的承受能力。 USB 外置擷取單元能夠滿足入門級需求,例如只需一台相機即可,但由於它們依賴主機 USB 控制器,因此延遲不穩定,不適用於嚴苛的測試。高密度擷取線仍依賴全高 PCIe 卡,這些卡片將 FPGA 資源集中到四個或更多攝影機鏈路上,凸顯了影像擷取卡市場需求曲線的兩極化。因此,在邊緣人工智慧日益普及的推動下,產品外形尺寸的轉變是漸進的,而非突飛猛進的。

區域分析

預計到2025年,亞太地區將佔全球影像擷取卡市場收入的32.43%,並將在2031年之前維持7.88%的複合年成長率。中國的半導體國產化政策、韓國在記憶體封裝領域的領先地位以及印度與電子生產連結獎勵計畫,正在推動該地區的發展勢頭。西方廠商正在加強在當地的佈局,以避免落後於靈活的本土競爭對手,例如Basler收購Alpha TechSys Automation India 76%的股份。此外,日本勞動力老化以及對自動化的需求,也推動了工廠維修中對影像處理的採用。

預計到2025年,北美和歐洲將佔全球銷售額的一半左右,這得益於成熟的產業基礎、嚴格的汽車品質標準以及航太和國防領域的強勁需求。在美國,用於MIL-STD認證專案的高性能採集卡需求持續旺盛;而德國一級汽車供應商則傾向於採用透過CoaXPress 2.0鏈路連接的多攝影機偵測單元。儘管FDA和IEC標準的統一簡化了醫療成像領域供應商的合規流程,但IEC 60601-1第四版的持續修訂將提高網路安全和軟體生命週期管理的標準,這將使擁有完善品質管理系統(QMS)的成熟企業更具優勢。

2025年,南美洲、中東和非洲總合合計銷售額佔不到15%。雖然巴西汽車產業佔最大佔有率,但外匯波動和資本投資限制抑制了對先進影像擷取卡的訂單。在中東的油氣綜合體中,機器視覺技術正被用於管道檢測和零件檢驗,但與亞太地區的半導體工廠相比,其部署規模仍然小規模。在非洲的採礦作業中,基於視覺的礦石分選技術因其能帶來即時的投資回報而正在被採用,但由於基礎設施和技能的匱乏,其廣泛應用進展緩慢。在全部區域,需要採用供應商資金籌措模式並建立緊密的一體化夥伴關係關係,才能挖掘潛在的市場需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 生產線上擴大採用像素超過5000萬的影像感測器。

- 工業4.0的引入需要即時影像處理。

- CoaXPress 2.0 和 PCIe 4.0 的頻寬增加

- 電子領域自動化光學檢測的發展

- 透過機載AI預處理降低主機CPU負載。

- 手術機器人對確定性影像的新需求

- 市場限制因素

- 取代獨立影像擷取卡的智慧型相機

- CoaXPress卡對中小企業而言初始成本較高

- 通道容量超過 25 Gbps 時的溫度控管挑戰(被忽略的問題)

- FPGA供應鏈緊張導致產品發布延遲(這個問題並未公開承認)。

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按介面類型

- Camera Link

- CoaXPress

- GigE Vision

- USB3 Vision

- LVDS 和平行數字

- 按主機匯流排/按外形尺寸

- PCIe/PCI卡

- USB外置擷取單元

- 嵌入式闆卡(PC/104、cPCI)

- M.2/Thunderbolt模組

- 以函數影格速率

- 最高可達 60 幀/秒

- 60~120 FPS

- 120幀或更高

- 透過使用

- 工業和製造業

- 電子和半導體測試

- 醫學與生命科學

- 安全監控

- 航太/國防

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Teledyne DALSA Inc.

- Matrox Electronic Systems Ltd.

- BitFlow, Inc.

- Euresys SA

- Active Silicon Ltd.

- KAYA Instruments Ltd.

- Pleora Technologies Inc.

- Advantech Co., Ltd.

- Gidel Ltd.

- Sensoray Company, Inc.

- Epix, Inc.

- Silicon Software GmbH

- Basler AG

- National Instruments Corporation

- Axiomtek Co., Ltd.

- dPict Imaging, Inc.

- Imperx, Inc.

- Raptor Photonics Ltd.

- ADLINK Technology Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the frame grabber market size is expected to increase from USD 2.57 billion in 2025 to USD 2.75 billion in 2026 and reach USD 3.74 billion by 2031, growing at a CAGR of 6.32% over 2026-2031.

This report is Segmented by Interface Type (Camera Link, Coaxpress, Gige Vision, and More), Host-Bus and Form Factor (PCIe and PCI Cards, USB External Capture Units, and More), Frame-Rate Capability (Up To 60 FPS, 60-120 FPS, and More), Application Industry (Industrial and Manufacturing, Electronics and Semiconductor Inspection, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Frame Grabber Market Trends and Insights

Rising Adoption of >50 MP Image Sensors on Production Lines

Canon's 410-megapixel CMOS sensor and Sony's IMX927 105-megapixel sensor running at 100 frames per second exemplify the resolution escalation that forces production-line integrators to replace legacy Camera Link Base or GigE Vision interfaces with CoaXPress 2.0 or Camera Link HS. A single 105-megapixel frame at 100 frames per second generates approximately 10.5 gigabytes per second of raw Bayer data, exceeding the 1 gigabit per second ceiling of standard GigE Vision by an order of magnitude. This bandwidth mismatch compels manufacturers to deploy frame grabbers with aggregate throughput beyond 10 gigabytes per second, driving demand for PCIe Gen4 cards and CoaXPress multi-link configurations. STMicroelectronics' 5-megapixel hybrid global-rolling-shutter sensor further illustrates the trend toward application-specific imaging that requires flexible frame-grabber architectures capable of switching between global-shutter and rolling-shutter modes midstream. The shift to >50-megapixel sensors is most pronounced in semiconductor wafer inspection, flat-panel-display defect detection, and automotive body-in-white measurement, where sub-micron resolution directly correlates with yield improvement and warranty-cost reduction.

Industry 4.0 Roll-Outs Requiring Real-Time Imaging

Industry 4.0 architectures mandate closed-loop control with sub-10-millisecond latency between image acquisition and actuator response, a requirement that favors frame grabbers with FPGA-based pre-processing over software-only pipelines running on general-purpose CPUs. Gidel's Proc1C10N frame grabber integrates 143 tera-operations per second of INT8 inference capacity directly on the capture card, enabling real-time defect classification without round-tripping pixel data to a host GPU. This on-board intelligence reduces network congestion in multi-camera cells and ensures deterministic latency even when other workloads contest host resources. Basler's November 2023 partnership with Siemens embedded the pylon SDK into Siemens Industrial Edge devices, allowing factory operators to deploy vision applications as containerized microservices that scale horizontally across production lines. The convergence of time-sensitive networking protocols, OPC UA for machine-to-machine communication, and deterministic frame grabbers positions imaging as a first-class citizen in the industrial Internet of Things stack, rather than a bolt-on inspection step.

Smart Cameras Replacing Discrete Frame Grabbers

Allied Vision's Alecs smart camera integrates an NVIDIA Jetson Orin NX module with 100 tera-operations per second of AI performance, enabling on-device inference for defect classification, optical character recognition, and dimensional measurement without a separate frame grabber or host PC. Teledyne's BOA3 AI camera similarly embeds a neural network accelerator that processes images at the edge, transmitting only metadata or alarm signals over GigE or USB3, thereby reducing network bandwidth by two orders of magnitude. This architectural shift appeals to applications where a single camera suffices, installation space is constrained, and the cost of a dedicated frame grabber and host PC cannot be justified. However, smart cameras struggle in multi-camera synchronization scenarios, deterministic-latency applications such as surgical robotics, and high-throughput inspection cells where uncompressed pixel data must be archived for traceability. The frame-grabber ecosystem retains an advantage in these niches by offering hardware-triggered acquisition across dozens of cameras with sub-microsecond jitter, FPGA-based real-time processing that bypasses operating-system scheduling latency, and direct GPU memory access for accelerated inference pipelines.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of CoaXPress 2.0 and PCIe 4.0 Bandwidth

- Growth of Automated Optical Inspection in Electronics

- High Up-Front Cost of CoaXPress Cards for SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The frame grabber market size for interface-type solutions shows CoaXPress occupying 38.19% revenue share in 2025, a share projected to climb steadily through 2031 as its 6.97% CAGR outpaces that of Camera Link and GigE alternatives. CoaXPress fusion of 12.5 Gbps per link and power delivery translates into simplified cable harnesses and extended reach, attributes crucial in semiconductor wafer inspection and automotive paint booths. Camera Link's entrenched base in aerospace and medical X-ray keeps it relevant for retrofit projects, yet new installations prefer the headroom and future-proofing of CoaXPress 2.0 and Camera Link HS. GigE Vision, while cost-friendly, suffers from packet loss and CPU overhead that undermine deterministic inspection, relegating it to distributed or cost-sensitive tasks.

Forward-looking demand centers on the draft CoaXPress 3.0 standard, which targets 25 Gbps per link, clearing the way for single-cable 200-MP cameras in flat-panel display metrology. Camera Link HS retains a specialized following where radiation-hard components are required, but engineering mindshare is pivoting toward CoaXPress. USB3 Vision maintains a foothold in handheld scanners and laboratory instruments thanks to its ubiquity and plug-and-play elegance, yet its 5 Gbps ceiling limits it to resolutions under 20 MP at moderate frame rates. Consequently, CoaXPress will remain the flagship of the frame grabber market, defining both performance expectations and competitive roadmaps.

PCIe and PCI cards supplied 46.52% of 2025 revenue, a testament to the dominance of tower and rackmount workstations in legacy vision architectures. The rise of compact edge appliances now lifts M.2 and Thunderbolt modules, forecast to log a 7.03% CAGR through 2031. M.2 modules mate directly to PCIe lanes in a footprint smaller than a credit card, enabling fanless designs that mount behind robot arms or inside panel PCs. Thunderbolt 4 provides 40 Gbps aggregate bandwidth, daisy-chaining, and hot-plug convenience, features that improve installation economics for portable inspection rigs.

Embedded boards in PC/104 and CompactPCI formats persist in aerospace and defense, where shock and vibration requirements exceed commercial PC tolerances. USB external capture units meet entry-level needs when a single camera suffices, but their reliance on host USB controllers introduces latency variability, disqualifying them for deterministic inspection. High-density lines still lean on full-height PCIe cards that pool FPGA resources across four or more camera links, underscoring a bifurcated demand curve inside the frame grabber market. The outcome is a gradual, not abrupt, form-factor transition driven by the rise of edge AI deployments.

Geography Analysis

Asia-Pacific accounted for 32.43% of the global frame grabber market revenue in 2025 and is projected to register a 7.88% CAGR through 2031. China's semiconductor localization mandates, South Korea's leadership in memory packaging, and India's production-linked incentives for electronics combine to anchor regional momentum. Western vendors, as illustrated by Basler's 76% purchase of Alpha TechSys Automation India, are deepening local footprints to keep pace with agile domestic competitors. Japan's aging workforce and the imperative of automation likewise propel adoption in factory retrofits that demand deterministic imaging.

North America and Europe jointly contributed roughly half of 2025 revenue, supported by mature industrial bases, stringent automotive quality standards, and robust demand in aerospace and defense. The United States continues to specify ruggedized capture cards for MIL-STD-qualified programs, while Germany's automotive tier-ones favor multi-camera inspection cells wired through CoaXPress 2.0 links. Harmonized FDA and IEC pathways streamline vendor compliance in medical imaging, yet the pending IEC 60601-1 Edition 4 upgrade will raise cybersecurity and software lifecycle bars, tilting the advantage toward incumbents with established QMS infrastructures.

South America, the Middle East, and Africa together generated less than 15% of 2025 revenue. Brazil's automotive hubs offer the largest parcel, but currency swings and capex constraints temper ordering patterns for advanced frame grabbers. Middle Eastern oil and gas complexes deploy machine vision for pipeline inspection and component verification, yet volumes remain modest compared to those in Asia-Pacific fabs. African mining operations adopt vision-based ore sorting where ROI is immediate, though infrastructure and skills gaps slow pervasive rollout. Collectively, these regions require vendor financing models and close integration partnerships to unlock latent demand.

- Teledyne DALSA Inc.

- Matrox Electronic Systems Ltd.

- BitFlow, Inc.

- Euresys SA

- Active Silicon Ltd.

- KAYA Instruments Ltd.

- Pleora Technologies Inc.

- Advantech Co., Ltd.

- Gidel Ltd.

- Sensoray Company, Inc.

- Epix, Inc.

- Silicon Software GmbH

- Basler AG

- National Instruments Corporation

- Axiomtek Co., Ltd.

- dPict Imaging, Inc.

- Imperx, Inc.

- Raptor Photonics Ltd.

- ADLINK Technology Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of >50 MP Image Sensors on Production Lines

- 4.2.2 Industry 4.0 Roll-Outs Requiring Real-Time Imaging

- 4.2.3 Expansion of CoaXPress 2.0 and PCIe 4.0 Bandwidth

- 4.2.4 Growth of Automated Optical Inspection in Electronics

- 4.2.5 On-Board AI Pre-Processing Reducing Host CPU Load

- 4.2.6 Emerging Demand for Deterministic Video in Surgical Robots

- 4.3 Market Restraints

- 4.3.1 Smart Cameras Replacing Discrete Frame Grabbers

- 4.3.2 High Up-Front Cost of CoaXPress Cards for SMEs

- 4.3.3 Thermal-Management Issues Beyond 25 Gbps per Channel (Under-the-Radar)

- 4.3.4 FPGA Supply-Chain Tightness Delaying Product Launches (Under-the-Radar)

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Interface Type

- 5.1.1 Camera Link

- 5.1.2 CoaXPress

- 5.1.3 GigE Vision

- 5.1.4 USB3 Vision

- 5.1.5 LVDS and Parallel Digital

- 5.2 By Host-Bus / Form Factor

- 5.2.1 PCIe / PCI Cards

- 5.2.2 USB External Capture Units

- 5.2.3 Embedded Boards (PC/104, cPCI)

- 5.2.4 M.2 / Thunderbolt Modules

- 5.3 By Frame-Rate Capability

- 5.3.1 Up to 60 FPS

- 5.3.2 60 - 120 FPS

- 5.3.3 Above 120 FPS

- 5.4 By Application Industry

- 5.4.1 Industrial and Manufacturing

- 5.4.2 Electronics and Semiconductor Inspection

- 5.4.3 Medical and Life Sciences

- 5.4.4 Security and Surveillance

- 5.4.5 Aerospace and Defense

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Teledyne DALSA Inc.

- 6.4.2 Matrox Electronic Systems Ltd.

- 6.4.3 BitFlow, Inc.

- 6.4.4 Euresys SA

- 6.4.5 Active Silicon Ltd.

- 6.4.6 KAYA Instruments Ltd.

- 6.4.7 Pleora Technologies Inc.

- 6.4.8 Advantech Co., Ltd.

- 6.4.9 Gidel Ltd.

- 6.4.10 Sensoray Company, Inc.

- 6.4.11 Epix, Inc.

- 6.4.12 Silicon Software GmbH

- 6.4.13 Basler AG

- 6.4.14 National Instruments Corporation

- 6.4.15 Axiomtek Co., Ltd.

- 6.4.16 dPict Imaging, Inc.

- 6.4.17 Imperx, Inc.

- 6.4.18 Raptor Photonics Ltd.

- 6.4.19 ADLINK Technology Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment