|

市場調查報告書

商品編碼

2062219

單組分聚氨酯泡棉:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)One Component Polyurethane Foam - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

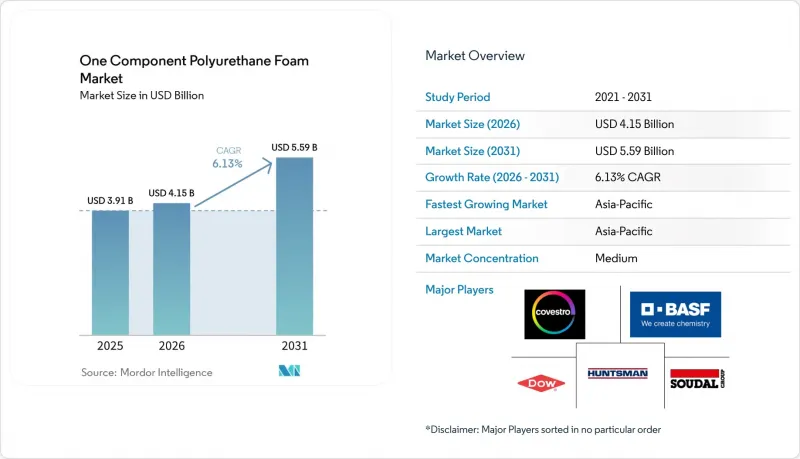

據 Mordor Intelligence 稱,2025 年單組分聚氨酯泡棉市值為 39.1 億美元,預計到 2031 年將從 2026 年的 41.5 億美元成長至 55.9 億美元,預測期(2026-2031 年)複合年成長率為 6.13%。

本報告按類型(傳統型、阻燃型及其他)、應用(門窗密封、暖通空調及管道保溫及其他)、終端用戶行業(住宅建築、商業建築及其他)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲)進行細分。市場預測以美元計價。

全球單組分聚氨酯泡棉市場趨勢及洞察

防火防潮泡沫技術的擴展

隨著建築管理部門收緊防火和煙霧毒性基準值,預計到2031年,耐火單組分聚氨酯泡棉的年成長率將達到6.68%,超過傳統等級。英國L部分法規於2026年修訂,將牆體的U值設定為0.18 W/m²K,鼓勵承包商使用既能保持隔斷性又不影響隔熱性能的縫隙填充材。在沿海地區和冷庫等需要在地下或高濕度環境下使用的產品中,閉孔、防潮產品更受歡迎。在這些環境中,吸水率低於2%(體積比)可確保耐久性。BASF於2026年2月推出的Autofroth系統,與溴化標準相比,可將菸霧毒性降低30%,同時在生產過程中減少高達20%的碳排放。在全球範圍內,可膨脹混合密封泡沫系統的趨勢,旨在平衡被動防火、隔音和節能目標。

擴大在門窗框架結構中的應用

2025年,門窗框密封件的銷售額佔比達到38.89%,因為三層玻璃窗已成為維修工程的主流選擇。固化過程中壓力低於5磅/平方英吋(psi)的低膨脹泡棉可防止框架變形,並且是許多製造商保固條款中的一項要求。 SikaWall-3000 Rapid Bond於2025年4月上市,可將固化時間縮短一半至4小時以內,並將高層建築外觀施工的人事費用降低40%。隨著歐盟《建築能源性能指令》的修訂(該指令要求披露整個生命週期的碳排放),建築師擴大採用生物基、低揮發性有機化合物(VOC)的泡沫材料。這些材料目前正逐漸被市場接受,並且略微溢價。在加州和安大略省,公共產業的補貼計畫(補貼高達50%的密封材料成本,包括線上購買)正在推動北美DIY計畫中此類材料的使用。

嚴格限制異氰酸排放和保障工人安全

由於美國職業安全與健康管理局 (OSHA) 將甲基二異氰酸酯 (MDI) 的允許濃度限制在 20 ppb(8 小時平均值),以及歐盟 REACH 法規強制要求對二異氰酸酯進行培訓,小規模承包商的合規成本正在不斷增加。英國健康與安全管理局 (HSE) 於 2025 年 3 月發布的指南規定,當暴露量超過暴露限值的 50% 時,必須進行局部排氣通風和生物監測,這增加了住宅裝修承包商的專案管理費用。澳洲的 SafeWork 示範指南假定存在風險,除非透過空氣監測證明安全,否則不得使用此類產品,這正在加速向低異氰酸酯配方的轉變。低異氰酸酯配方雖然抗壓強度降低了 10-15%,但避免了昂貴的通風系統維修。小規模承包商擴大在結構荷載較小的區域改用矽酮和丙烯酸乳膠。

細分市場分析

截至2025年,傳統單組分聚氨酯泡棉佔據了單組分聚氨酯泡棉市場43.35%的佔有率,這主要得益於注重成本的通用縫隙填充應用。預計在預測期(2026-2031年)內,耐火產品將以6.68%的年均成長率成長,這主要得益於混合用途塔樓中ASTM E84 A級和NFPA 286標準的採用。預計到2031年,耐火單組分聚氨酯泡棉的市場規模將達到更高水平,凸顯了密封材料法規的轉變,安全性已成為重中之重。隨著製造商將保固範圍與框架壓力限制掛鉤,低發泡製品在高檔窗框安裝中逐漸取代高發泡泡棉。此外,繼日產汽車在2025年展示了提升乘坐舒適性的成果後,用於電動車NVH(噪音、振動和聲振粗糙度)包裝的專用隔音和相變配方正受到關注。

第二代產品兼具安全性和永續性。BASF的「Autofroth」可降低30%的煙霧毒性,並減少高達20%的碳排放,使其成為對室內空氣品質要求嚴格的醫療機構的理想選擇。到2026年,傳統耐火罐和耐火罐之間的價格差異將縮小至2美元以下,這將進一步推動耐火罐在注重成本的住宅維修中普及。在閣樓和地下室維修中,施工速度比精確度更為重要,因此成熟的高膨脹型耐火罐仍然是首選。然而,隨著注重人事費用成本的承包商採用快速固化、低壓的替代產品,預計耐火罐的市佔率將會萎縮。

區域分析

預計到2025年,亞太地區將以47.74%的市佔率主導單組分聚氨酯泡棉市場,並在2031年之前維持6.92%的複合年成長率。先前原料短缺的問題已因中國2024年聚氨酯產量的增加以及萬華化學於2025年1月新增180萬噸MDI產能而得到緩解。印度聚氨酯需求的逐年成長以及基礎設施建設的推進表明市場需求將持續成長,而印尼冷藏棕櫚油倉庫的激增也使泡沫的使用量保持在兩位數水平。在日本,預製住宅市場預計到2024年將達到18%,工廠預裝的泡沫材料將用於實現房屋的氣密性目標。

北美聚氨酯產業正面臨高全球暖化潛勢(GWP)推進劑的禁令,該禁令將於2025年根據美國環保署(EPA)的規定生效。然而,預計到2025年,資料中心建設將成長35%,從而推動對工業發泡體的需求。加拿大建築規範的修訂將氣候區6的隔熱要求提高了20%,擴大了安大略省和魁北克省高隔熱泡沫的銷售量。在墨西哥,近岸外包浪潮導致無塵室和濕度控制工廠的數量增加,這些工廠需要暖通空調管道周圍無縫隙的隔熱層。

在歐洲,建築能源性能指令 (EPBD) 的修訂要求到 2030 年新建建築實現零排放,並要求從 2028 年起,面積超過 1000平方公尺的建築必須進行全生命週期碳排放報告。德國的 GEG 2024、英國的 Part L 2026 和法國的 RE2020 都收緊了對熱傳導係數的限制,從而提振了對經認證的防火泡沫的需求。 2025 年 7 月,科思創位於多爾馬根的 TDI 工廠發生不可抗力事件,導致年產量減少 30 萬噸,加劇了歐洲的供應緊張。這迫使承包商改用預混合料單罐泡沫,以減少現場異氰酸酯的暴露。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 防火防潮泡沫技術的擴展

- 擴大在門窗框框中的應用

- 關於隔熱性能的監管壓力

- 預製模組化建築數量激增,需要預硬化泡棉材料

- 電子商務的DIY通路正在加速單罐泡沫的普及。

- 市場限制因素

- 嚴格的異氰酸排放和工人安全法規

- 替代密封劑和絕緣方法的可用性

- 歐洲和北美即將禁止使用高全球暖化潛勢推進劑

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 傳統的

- 阻燃劑

- 低發泡

- 高發泡

- 其他類型(特殊發泡體)

- 透過使用

- 門窗框密封

- 暖通空調和管道保溫

- 縫隙填充和裂縫修復

- 屋頂和牆壁上的空腔

- 其他用途(建築、工業等)

- 按最終用戶行業分類

- 住宅

- 商業建築

- 工業基礎設施

- 汽車和運輸業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Akfix

- Arkema

- BASF

- Covestro AG

- Dow

- fischer Group of Companies

- Huntsman International LLC

- ICP Building Solutions Group

- QUILOSA-Selena Iberia SLU

- SEKISUI CHEMICAL CO., LTD.

- Shanghai Haohai Chemical Co., Ltd.

- Sika AG

- Soudal Group

- Trelleborg AB

- Wanhua

第7章 市場機會與未來展望

According to Mordor Intelligence, the one component polyurethane foam market size was valued at USD 3.91 billion in 2025 and is estimated to grow from USD 4.15 billion in 2026 to reach USD 5.59 billion by 2031, at a CAGR of 6.13% during the forecast period (2026-2031).

This report is Segmented by Type (Traditional, Fire-Resistant, and More), Application (Window and Door-Frame Sealing, HVAC and Pipeline Insulation, and More), End-User Industry (Residential Construction, Commercial Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global One Component Polyurethane Foam Market Trends and Insights

Expansion of Fire-Rated and Moisture-Resistant Foam Technologies

Fire-resistant one component polyurethane foam will grow 6.68% per year to 2031, outpacing legacy grades as building authorities tighten flame-spread and smoke-toxicity thresholds. Updated UK Part L 2026 rules set wall U-values at 0.18 W/m2K, encouraging contractors to specify gap fillers that preserve compartmentation without compromising thermal targets. Closed-cell, moisture-resistant variants are favored in coastal regions and cold-storage hubs for below-grade or high-humidity service, where water-absorption limits below 2% by volume protect durability. BASF's Autofroth system, introduced in February 2026, reduces smoke toxicity 30% versus brominated baselines while trimming embodied carbon by up to 20%. A global trend toward intumescent, hybrid sealant-foam systems aligns passive fire protection with acoustic and energy-performance objectives.

Increased Use in Window and Door-Frame Installations

Window and door-frame sealing represented 38.89% of 2025 revenue as triple-glazed units mainstreamed across renovation programs. Low-expansion foams that exert under 5 psi during cure prevent frame distortion and have become mandatory in many manufacturers' warranties. SikaWall-3000 Rapid Bond, launched April 2025, halves curing time to under four hours, cutting labor costs 40% on high-rise facades. Revised EU Energy Performance of Buildings Directive requirements for whole-life carbon disclosure push architects toward bio-based, low-VOC foams, which now command a modest premium amid growing acceptance. Utility rebates in California and Ontario that cover up to 50% of air-sealing materials, including online purchases, amplify do-it-yourself uptake in North America.

Strict Limits on Isocyanate Emissions and Worker Safety

OSHA's 20 ppb eight-hour MDI limit and EU REACH's mandatory diisocyanate training regime elevate compliance costs across small-scale contracting. The UK Health and Safety Executive's March 2025 guidelines require local exhaust ventilation and biological monitoring above 50% of exposure limits, raising project overhead for residential remodelers. Australia's SafeWork model Code of Practice presumes hazard unless air monitoring proves otherwise, accelerating the shift to low-free-isocyanate formulas that sacrifice 10-15% compressive strength but avoid costly ventilation retrofits. Smaller contractors increasingly switch to silicone or acrylic latex where structural loads are minimal.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Pressure on Thermal-Insulation Compliance

- Surge in Prefabricated Modular Construction Requiring Pre-Cured Foams

- Availability of Alternative Sealants and Insulation Methods

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional one component polyurethane foam accounted for 43.35% of one component polyurethane foam market share in 2025, anchored in general-purpose gap filling, where cost sensitivity dominates. Fire-rated products are set to grow 6.68% annually during the forecast period (2026-2031), propelled by ASTM E84 Class A and NFPA 286 adoption in mixed-use towers. The one-component polyurethane foam market size for fire-rated variants is projected to reach a greater value in 2031, underscoring a regulatory pivot toward safety-critical seals. Low-expansion lines continue to displace high-expansion foams in premium fenestration installations as manufacturers link warranty coverage to frame-pressure limits. Niche acoustic and phase-change formulations are gaining traction in electric-vehicle NVH packages following Nissan's demonstration of ride comfort improvement in 2025.

Second-generation products layer sustainability onto safety. BASF's Autofroth reduces smoke toxicity 30% and carbon footprint up to 20%, positioning the company for specification in health-care facilities with stringent indoor-air protocols. Price differentials between traditional and fire-resistant cans narrowed to under USD 2 in 2026, supporting mainstream adoption even in cost-focused residential upgrades. Mature high-expansion lines remain favored in attic and crawl-space retrofits where speed outweighs precision, yet volumetric share is expected to erode as labor-sensitive contractors embrace quick-curing, low-pressure alternatives.

Geography Analysis

Asia-Pacific dominated the one component polyurethane foam market with a 47.74% revenue share in 2025 and is projected to grow at 6.92% CAGR through 2031. China's polyurethane output in 2024 and Wanhua Chemical's 1.8 million-ton MDI capacity expansion in January 2025 alleviated prior feedstock tightness. India's annual polyurethane volume growth and infrastructure push signal continued demand, while Indonesia's palm-oil cold-storage boom sustains double-digit foam usage. Japan's prefab housing share reached 18% in 2024, integrating factory-applied foams to hit airtightness targets.

North America's polyurethane sector faces high-GWP propellant bans effective 2025 under the EPA rule set. Yet data-center construction climbed 35% in 2025, driving industrial-grade foam uptake. Canada's code updates raise Climate Zone 6 insulation requirements 20%, boosting high-R foam sales in Ontario and Quebec. Mexico's near-shoring wave adds cleanroom and humidity-controlled factories that specify gap-free insulation around HVAC ductwork.

Europe confronts the Energy Performance of Buildings Directive redo, mandating zero-emission new buildings by 2030 and whole-life carbon reporting for structures over 1,000 m2 starting 2028. Germany's GEG 2024, the UK's Part L 2026, and France's RE2020 toughen thermal transmittance limits, underpinning demand for certified, fire-rated foams. Covestro's Dormagen TDI force majeure in July 2025 cut 300,000 tons per annum and tightened European supply, nudging contractors toward premixed, single-can formats that curb site-level isocyanate exposure.

- Akfix

- Arkema

- BASF

- Covestro AG

- Dow

- fischer Group of Companies

- Huntsman International LLC

- ICP Building Solutions Group

- QUILOSA - Selena Iberia S.L.U.

- SEKISUI CHEMICAL CO., LTD.

- Shanghai Haohai Chemical Co., Ltd.

- Sika AG

- Soudal Group

- Trelleborg AB

- Wanhua

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of fire-rated and moisture-resistant foam technologies

- 4.2.2 Increased use in window and door-frame installations

- 4.2.3 Regulatory pressure on thermal-insulation compliance

- 4.2.4 Surge in prefabricated modular construction requiring pre-cured foams

- 4.2.5 E-commerce DIY channels accelerating single-can foam adoption

- 4.3 Market Restraints

- 4.3.1 Strict limits on isocyanate emissions and worker safety

- 4.3.2 Availability of alternative sealants and insulation methods

- 4.3.3 Upcoming bans on high-GWP propellants in Europe and North America

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Traditional One Component Polyurethane Foam

- 5.1.2 Fire-Resistant One Component Polyurethane Foam

- 5.1.3 Low-Expansion One Component Polyurethane Foam

- 5.1.4 High-Expansion One Component Polyurethane Foam

- 5.1.5 Other Types (Specialized Foams)

- 5.2 By Application

- 5.2.1 Window and Door-Frame Sealing

- 5.2.2 HVAC and Pipeline Insulation

- 5.2.3 Gap Filling and Crack Sealing

- 5.2.4 Roofing and Wall Cavities

- 5.2.5 Other Applications (Construction and Industrial, etc.)

- 5.3 By End-user Industry

- 5.3.1 Residential Construction

- 5.3.2 Commercial Construction

- 5.3.3 Industrial and Infrastructure

- 5.3.4 Automotive and Transportation

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Akfix

- 6.4.2 Arkema

- 6.4.3 BASF

- 6.4.4 Covestro AG

- 6.4.5 Dow

- 6.4.6 fischer Group of Companies

- 6.4.7 Huntsman International LLC

- 6.4.8 ICP Building Solutions Group

- 6.4.9 QUILOSA - Selena Iberia S.L.U.

- 6.4.10 SEKISUI CHEMICAL CO., LTD.

- 6.4.11 Shanghai Haohai Chemical Co., Ltd.

- 6.4.12 Sika AG

- 6.4.13 Soudal Group

- 6.4.14 Trelleborg AB

- 6.4.15 Wanhua

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

導電軟性聚氨酯市場規模、佔有率和成長分析:按導電填料類型、產品形式、功能、應用、最終用途產業、分銷通路和地區分類-2026-2033年產業預測

導電軟性聚氨酯市場規模、佔有率和成長分析:按導電填料類型、產品形式、功能、應用、最終用途產業、分銷通路和地區分類-2026-2033年產業預測 2026-2030年全球聚氨酯泡沫塗料市場

2026-2030年全球聚氨酯泡沫塗料市場 聚氨酯泡棉市場分析:按結構、產品類型、密度、終端用途產業和地區分類(2026-2034 年)

聚氨酯泡棉市場分析:按結構、產品類型、密度、終端用途產業和地區分類(2026-2034 年) 彩色聚氨酯泡棉市場:按類型、應用和地區分類

彩色聚氨酯泡棉市場:按類型、應用和地區分類 聚氨酯泡棉市場:按類型、應用和最終用途分類-2026-2032年全球市場預測

聚氨酯泡棉市場:按類型、應用和最終用途分類-2026-2032年全球市場預測 聚氨酯泡棉市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034年

聚氨酯泡棉市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034年 聚氨酯泡棉市場規模、佔有率和成長分析:按產品類型、密度、應用、最終用途產業、地區和產業預測分類,2026-2033年依軟管結構、工作壓力範圍、內徑範圍和最終用途產業分類的聚氨酯增強軟管市場-全球預測,2026-2032年鋼絲增強聚氨酯軟管市場:依結構、壓力等級、材料類型、應用及通路分類,全球預測(2026-2032年)

聚氨酯泡棉市場規模、佔有率和成長分析:按產品類型、密度、應用、最終用途產業、地區和產業預測分類,2026-2033年依軟管結構、工作壓力範圍、內徑範圍和最終用途產業分類的聚氨酯增強軟管市場-全球預測,2026-2032年鋼絲增強聚氨酯軟管市場:依結構、壓力等級、材料類型、應用及通路分類,全球預測(2026-2032年) 聚氨酯泡棉市場分析及預測(至2035年):類型、產品、應用、形式、材料類型、製造流程、最終用戶、技術、安裝類型、解決方案

聚氨酯泡棉市場分析及預測(至2035年):類型、產品、應用、形式、材料類型、製造流程、最終用戶、技術、安裝類型、解決方案