|

市場調查報告書

商品編碼

2062206

單片陶瓷:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Monolithic Ceramics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

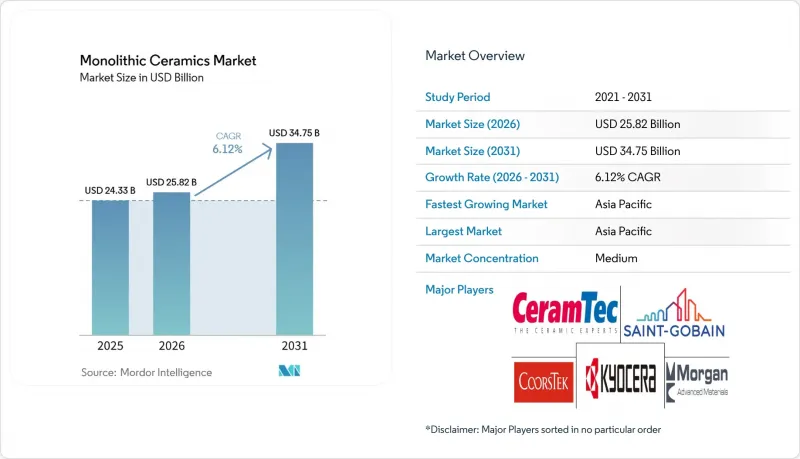

根據 Mordor Intelligence 預測,單片陶瓷市場規模將從 2025 年的 243.3 億美元成長到 2026 年的 258.2 億美元,到 2031 年達到 347.5 億美元,2026 年至 2031 年的複合年成長率為 6.12%。

本報告按材料類型(氧化鋁、氧化鋯、氮化矽等)、結構(透明、不透明、多孔)、終端用戶行業(電子和半導體、汽車和運輸設備等)以及地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲)進行細分。市場預測以美元計價。

全球單片陶瓷市場趨勢及洞察

電動車動力傳動系統的溫度控管

寬能隙碳化矽 (SiC) 逆變器的效率現已超過 99%,與矽 IGBT 相比,熱負載降低了一半,每次充電可延長車輛續航里程約 7%。 ROHM-Schaeffler、意法半導體和英飛凌等公司在 200 毫米晶圓上進行大規模生產,正在降低晶圓成本並擴大對陶瓷基板的需求。氧化鋁和氮化鋁 (AIN) 的直接接合銅基板對於散熱至關重要,但符合 ISO 26262 標準以降低分層風險對逆變器開發商仍然至關重要。單片陶瓷市場與 800V 電動車平台的成長密切相關。後端供應商已表示 AIN 片材的前置作業時間長達 9 個月,凸顯了其在定價方面持續的強大影響力。

對半導體蝕刻和CMP夾具的需求

台積電2026年560億美元的資本支出計畫以及英特爾18A製程的量產預計將增加每家晶圓廠對數千個氧化鋁晶圓載體、氧化釔塗層腔室襯墊和碳化矽基座的需求。 CHIPS法案的津貼預計將使美國先進邏輯元件的生產佔有率在2025年底前達到近15%,從而提振國內對半導體夾具的需求。 NGK絕緣體公司正將其HICERAM產能擴大三倍,目標是在2030年實現200億日圓的銷售額,並專注於整合元件製造和半導體晶圓廠。然而,人手不足導致設備安裝延遲,造成專用載體訂單積壓。單片陶瓷市場仍與半導體資本支出週期密切相關,預計2028年產量將保持穩定。

固有脆性和設計限制

陶瓷的斷裂韌性範圍為3至6 MPa√m,遠低於金屬,這限制了其在涉及拉伸和衝擊的應用中的使用。例如,電動車馬達用氮化矽軸承要求表面粗糙度低於14 nm,導致其加工成本是鋼材的四倍。為了確保尺寸裕度以承受應力,陶瓷的重量會增加;而積層製造雖然提供了幾何形狀的柔軟性,但會引入異向性缺陷。 ASTM C1161和C1239等標準為彎曲和威布爾試驗提供了指南,但對於安全至關重要的積層製造零件,目前尚無統一的認證流程。這些挑戰阻礙了陶瓷的廣泛應用,在設計標準完善之前,其目標市場仍將十分狹窄。

細分市場分析

儘管氧化鋁在2025年佔銷售額的47.12%,但預計到2031年,碳化矽的複合年成長率將達到6.58%,成為成長最快的材料。這主要歸功於電動車逆變器和可再生能源轉換器中寬能隙元件的普及。由於成本優勢,氧化鋁將繼續用於化學機械拋光(CMP)環和植入支台齒,而氧化鋯的相變強化特性正在拓展其作為固體氧化物電解槽電解質的應用。英飛凌向200毫米碳化矽晶圓的過渡使其外延成本降低了30%,從而增強了其價格競爭力。

隨著ST-Sanan的48萬片生產線於2028年全面運作,碳化矽基基板單片陶瓷的市場規模預計將顯著擴大。同時,氧化鋁仍繼續主導夾具用單片陶瓷市場。氮化矽和一些特殊氧化物材料雖然規模較小,但對於軸承和裝甲等應用具有重要的策略意義。京瓷的「BIOCERAM AZUL」混合材料,其抗彎強度高達1400兆帕,標誌著材料創新在主要材料之外的逐步發展。

區域分析

預計到2025年,亞太地區將佔全球銷售額的44.22%,並在2031年之前以6.88%的複合年成長率成長,這主要得益於中國先進陶瓷生產的強勁成長。淄博和佛山兩大產業叢集的銷售額總合超過1000億元人民幣,而日本製造商在2024年至2026年間將投資550億日元用於產能和研發。此外,隨著中國沿海地區人事費用的上升,東協地區的組裝基地也正在興起。

北美正受惠於《晶片保護與專利法案》(CHIPS Act)的優惠待遇。國防主導對太空陶瓷的需求也推動了成長。 NGK投資5,800萬美元在亞利桑那州的工廠計劃於2027年運作,屆時將實現晶圓載體的本地化供應。加拿大和墨西哥仍是小眾市場,分別專注於油田感測器和傳統瓦片。

在歐洲,陶瓷和氫能產業息息相關。憑藉托普索公司在丹麥的電解工廠(該計畫獲得了9,400萬歐元的資金支持),斯堪的斯堪地那維亞已成為綠氫能領域的領導者。德國的機械產業和英國的摩根先進材料公司是航太複合材料的主要供應商。然而,不斷上漲的碳邊境調節措施(CBAM)成本正在推動南歐各地熔爐的電氣化。對俄羅斯先進粉末出口的製裁正在促使獨立國協(獨立國協)地區的需求轉向國內工廠。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電動車動力傳動系統的溫度控管

- 對半導體蝕刻和CMP夾具的需求

- 醫療和牙科植入日益普及

- 用於綠色氫氣的固體氧化物電解堆

- 太空經濟(可重複使用火箭、高超音速飛機)

- 市場限制因素

- 固有脆性與設計極限

- 摻雜劑用氧化鋁氧化釔供應短缺

- 關於碳中和反應器的法規

- 價值鏈分析

- 波特五力分析

第5章:預測市場規模與成長率

- 依材料類型

- 氧化鋁

- 氧化鋯

- 氮化矽

- 碳化矽

- 其他材料類型(氧化鎂、莫來石、碳化硼等)

- 按結構

- 透明的

- 不透明

- 多孔

- 按最終用戶行業分類

- 電子和半導體

- 汽車和運輸機械

- 醫療和牙科護理

- 能源與電力

- 其他終端用戶產業(工業設備、化學、冶金等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- CeramTec GmbH

- CoorsTek Inc.

- Elan Technology

- HC Starck Tungsten GmbH

- Hitachi Chemical Co., Ltd.

- Kyocera Corporation

- Materion Corporation

- Morgan Advanced Materials

- Murata Manufacturing Co., Ltd.

- NGK INSULATORS, LTD.

- Rauschert Heinersdorf-Pressig GmbH

- Saint-Gobain

- SGL Carbon

- Sumitomo Electric Industries, Ltd.

- TOSOH CERAMICS CO., LTD.

- Vesuvius

第7章 市場機會與未來展望

According to Mordor Intelligence, the monolithic ceramics market size is expected to increase from USD 24.33 billion in 2025 to USD 25.82 billion in 2026 and reach USD 34.75 billion by 2031, growing at a CAGR of 6.12% over 2026-2031.

This report is Segmented by Material Type (Alumina, Zirconia, Silicon Nitride, and More), Structure (Transparent, Opaque, and Porous), End-User Industry (Electronics and Semiconductor, Automotive and Transportation, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Monolithic Ceramics Market Trends and Insights

EV Power-Train Thermal Management

Wide-bandgap silicon-carbide inverters now achieve over 99% efficiency, reducing heat loads by half compared to silicon IGBTs and increasing vehicle range by approximately 7% per charge. Mass production by ROHM-Schaeffler, STMicroelectronics, and Infineon on 200 mm wafers is lowering die costs and driving higher ceramic substrate volumes. Alumina and aluminum-nitride direct-bonded copper substrates are essential for dissipating these heat losses, while ISO 26262 compliance remains critical to mitigate delamination risks for inverter developers. The Monolithic ceramics market is well-aligned with the growth of 800-V e-mobility platforms. Back-end suppliers are already reporting nine-month lead times for AIN sheets, highlighting sustained pricing power.

Demand for Semiconductor Etch and CMP Fixtures

TSMC's USD 56 billion capital expenditure plan for 2026 and Intel's 18A ramp are expected to add thousands of alumina wafer carriers, yttria-coated chamber liners, and silicon-carbide susceptors per fab. CHIPS Act grants are projected to increase the U.S. share of advanced logic production to nearly 15% by the end of 2025, boosting local demand for semiconductor fixtures. NGK Insulators is tripling its HICERAM capacity to achieve JPY 20 billion in sales by 2030, emphasizing the integration of component manufacturing with semiconductor fabs. However, labor shortages are delaying tool installations, extending order backlogs for specialty carriers. The monolithic ceramics market remains closely tied to semiconductor capital expenditure cycles, ensuring volume visibility through 2028.

Intrinsic Brittleness and Design Limits

The fracture toughness of ceramics, ranging from 3-6 MPa√m, is significantly lower than that of metals, limiting their use in tensile or impact applications. For example, silicon-nitride EV motor bearings require surface roughness of ≤14 nm, increasing machining costs by four times compared to steel. Over-dimensioning to handle stress adds weight, while additive manufacturing introduces anisotropic flaws despite offering geometric flexibility. Standards such as ASTM C1161 and C1239 provide guidelines for flexural and Weibull testing, but no unified certification pathway exists for safety-critical additive-manufactured parts. These challenges constrain the broader adoption of ceramics, narrowing the addressable market until design standards evolve.

Other drivers and restraints analyzed in the detailed report include:

- Medical and Dental Implant Adoption Boom

- Green-Hydrogen Solid-Oxide Electrolyzer Stacks

- Carbon-Neutral Furnace Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Alumina held 47.12% of revenue dominance in 2025, but silicon carbide is anticipated to achieve a 6.58% CAGR through 2031, marking the fastest growth among materials. This is attributed to the shift towards wide-bandgap devices in EV inverters and renewable energy converters. Alumina's affordability ensures its continued use in CMP rings and implant abutments, while zirconia's transformation toughening enhances its application in solid-oxide electrolyzer electrolytes. Infineon's transition to 200 mm silicon carbide wafers has reduced epitaxy costs by 30%, supporting efforts to achieve price parity.

The monolithic ceramics market size for silicon carbide substrates is expected to grow significantly once ST-Sanan's 480,000-wafer production line reaches full capacity in 2028. Alumina, however, continues to dominate the monolithic ceramics market for fixtures. Silicon nitride and niche oxides, though smaller in scale, are strategically important for applications such as bearings and armor. Kyocera's BIOCERAM AZUL hybrid blend, with a flexural strength of 1,400 MPa, highlights incremental material innovations beyond the primary materials.

Geography Analysis

Asia-Pacific captured 44.22% of revenue in 2025 and is projected to grow at a 6.88% CAGR through 2031, driven by China's advanced ceramics production. Industrial clusters in Zibo and Foshan have a combined turnover exceeding CNY 100 billion, while Japanese manufacturers are investing JPY 55 billion in capacity and R&D between 2024 and 2026. ASEAN assembly hubs are also emerging as labor costs rise along China's coastal regions.

North America benefits from CHIPS Act incentives. Defense-driven demand for space ceramics is also contributing to growth. NGK's USD 58 million Arizona plant, set to become operational in 2027, will localize wafer-carrier supply. Canada and Mexico remain niche players, focusing on oil-field sensors and traditional tiles, respectively.

Europe interlinks ceramics with hydrogen goals. Topsoe's Danish electrolyzer plant, supported by EUR 94 million in funding, positions Scandinavia as a leader in green hydrogen. Germany's machinery sector and the U.K.'s Morgan Advanced Materials are key suppliers of aerospace composites. However, rising CBAM costs are prompting kiln electrification across southern Europe. Sanctions on Russia's advanced powder exports are redirecting demand within the CIS to domestic mills.

- 3M

- CeramTec GmbH

- CoorsTek Inc.

- Elan Technology

- H.C. Starck Tungsten GmbH

- Hitachi Chemical Co., Ltd.

- Kyocera Corporation

- Materion Corporation

- Morgan Advanced Materials

- Murata Manufacturing Co., Ltd.

- NGK INSULATORS, LTD.

- Rauschert Heinersdorf-Pressig GmbH

- Saint-Gobain

- SGL Carbon

- Sumitomo Electric Industries, Ltd.

- TOSOH CERAMICS CO., LTD.

- Vesuvius

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV power-train thermal management

- 4.2.2 Demand for semiconductor etch and CMP fixtures

- 4.2.3 Medical and dental implant adoption boom

- 4.2.4 Green-hydrogen solid-oxide electrolyzer stacks

- 4.2.5 Space economy (re-usable launchers, hypersonics)

- 4.3 Market Restraints

- 4.3.1 Intrinsic brittleness and design limits

- 4.3.2 Dopant-grade alumina and yttria supply squeeze

- 4.3.3 Carbon-neutral furnace regulations

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Alumina

- 5.1.2 Zirconia

- 5.1.3 Silicon Nitride

- 5.1.4 Silicon Carbide

- 5.1.5 Other Material Types (Magnesia, Mullite, Boron Carbide, etc.)

- 5.2 By Structure

- 5.2.1 Transparent

- 5.2.2 Opaque

- 5.2.3 Porous

- 5.3 By End-user Industry

- 5.3.1 Electronics and Semiconductor

- 5.3.2 Automotive and Transportation

- 5.3.3 Medical and Dental

- 5.3.4 Energy and Power

- 5.3.5 Other End-user Industries (Industrial Equipment, Chemical, Metallurgy, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 CeramTec GmbH

- 6.4.3 CoorsTek Inc.

- 6.4.4 Elan Technology

- 6.4.5 H.C. Starck Tungsten GmbH

- 6.4.6 Hitachi Chemical Co., Ltd.

- 6.4.7 Kyocera Corporation

- 6.4.8 Materion Corporation

- 6.4.9 Morgan Advanced Materials

- 6.4.10 Murata Manufacturing Co., Ltd.

- 6.4.11 NGK INSULATORS, LTD.

- 6.4.12 Rauschert Heinersdorf-Pressig GmbH

- 6.4.13 Saint-Gobain

- 6.4.14 SGL Carbon

- 6.4.15 Sumitomo Electric Industries, Ltd.

- 6.4.16 TOSOH CERAMICS CO., LTD.

- 6.4.17 Vesuvius

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

超高溫陶瓷(UHTC)市場預測至2034年-全球材料類型、技術、形狀、製造流程、應用、最終用戶和地區分析

超高溫陶瓷(UHTC)市場預測至2034年-全球材料類型、技術、形狀、製造流程、應用、最終用戶和地區分析 堇青石市場規模、佔有率和成長分析:按類型、產品類型、應用、最終用戶產業、等級、分銷管道和地區分類-2026-2033年產業預測

堇青石市場規模、佔有率和成長分析:按類型、產品類型、應用、最終用戶產業、等級、分銷管道和地區分類-2026-2033年產業預測 2026年全球整體式耐火材料市場報告

2026年全球整體式耐火材料市場報告 陶瓷市場:2026-2032年全球市場預測(依產品類型、原料、產品形態、製造流程、表面處理、銷售管道及最終用途產業分類)陶瓷市場預測至2034年-全球分析(按類型、材料、產品類型、先進陶瓷材料、製造流程、應用、分銷管道和地區分類)

陶瓷市場:2026-2032年全球市場預測(依產品類型、原料、產品形態、製造流程、表面處理、銷售管道及最終用途產業分類)陶瓷市場預測至2034年-全球分析(按類型、材料、產品類型、先進陶瓷材料、製造流程、應用、分銷管道和地區分類) 2026-2030年全球陶瓷和天然石瓷磚市場

2026-2030年全球陶瓷和天然石瓷磚市場 HTCC封裝與管殼市場報告:趨勢、預測與競爭分析(至2035年)

HTCC封裝與管殼市場報告:趨勢、預測與競爭分析(至2035年) 陶瓷市場報告:按產品、應用、最終用途和地區分類(2026-2034 年)高溫共燒陶瓷基板市場報告:趨勢、預測及競爭分析(至2035年)

陶瓷市場報告:按產品、應用、最終用途和地區分類(2026-2034 年)高溫共燒陶瓷基板市場報告:趨勢、預測及競爭分析(至2035年) 陶瓷坩堝市場規模、佔有率和成長分析:按材料類型、製造流程、應用、溫度範圍和地區分類-產業預測,2026-2033年

陶瓷坩堝市場規模、佔有率和成長分析:按材料類型、製造流程、應用、溫度範圍和地區分類-產業預測,2026-2033年