|

市場調查報告書

商品編碼

2062180

隔音窗簾:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Soundproof Curtains - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

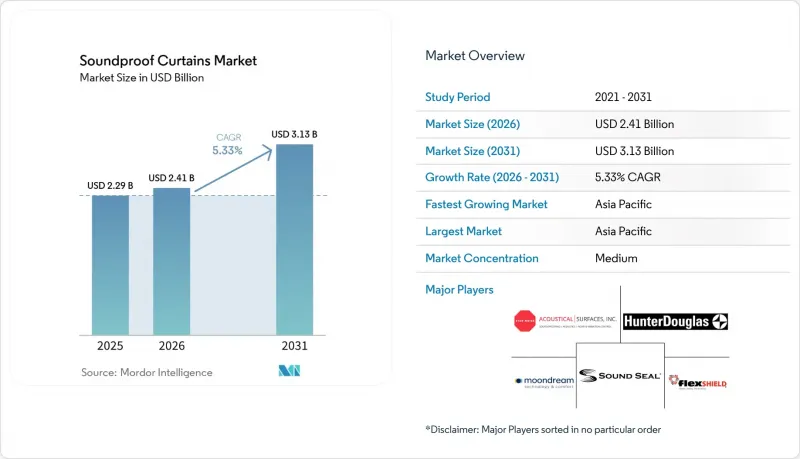

據 Mordor Intelligence 稱,2025 年隔音窗簾市場價值 22.9 億美元,預計到 2031 年將從 2026 年的 24.1 億美元成長至 31.3 億美元,預測期(2026-2031 年)複合年成長率為 5.33%。

本報告按類型(隔音、降噪、隔音)、材料(玻璃絨、岩絨、泡沫塑膠、天然纖維及其他)、最終用戶(住宅、商業、工業、醫療/教育設施)和地區(亞太、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元計價。

全球隔音窗簾市場趨勢及洞察

工業噪音暴露限值已收緊。

隨著美國職業安全與健康管理局 (OSHA) 和歐盟監管機構加強對工廠和倉庫噪音水平的審核,企業現在只要在8小時輪班期間噪音分貝超過閾值,就會投資採取工程措施。可移動隔音屏障擴大應用於汽車、電子商務和食品加工廠,它們不僅比固定式隔音罩更具成本效益,而且還具有佈局調整時可移動的額外優勢。德國、法國和義大利將於2025年強制實施季度噪音監測,這導致厚乙烯基層壓簾的訂單激增,這類窗簾以其卓越的隔音性能而聞名。在快速成長的亞太市場,即使在當地法規仍在製定中的地區,對經認證的隔音窗簾的需求也在不斷成長,因為跨國公司正在使其員工安全報告標準與嚴格的歐盟標準接軌。

評估聲學舒適度的綠建築認證

隨著LEED v4.1對室內聲學品質的認可以及WELL v2制定背景噪音基準值,開發商開始採用簾式吸音系統來配合天花板和聲音掩蔽技術。由於LEED認證的辦公大樓在主要城市通常租金更高,這些與聲學相關的認證指標備受業主青睞,從而建立了簾式吸音系統投資與盈利能力提升之間的直接聯繫。認證機構目前更重視環境產品聲明(EPD),重點在於生產過程中的碳排放,而PVC層壓板產品則因回收問題而受到冷落。像Knauf Insulation這樣的供應商正在其玻璃棉芯材中添加生物基粘合劑,以確保符合VOC和甲醛標準,同時也使其聲學產品符合綠色建築標準。

高濕度氣候下的性能下降

當相對濕度超過70%時,聚酯纖維窗簾的吸音性能會下降。測試結果表明,纖維會膨脹,降低其內部孔隙率。在印尼、越南和菲律賓等沿海地區,一年中的大部分時間濕度都超過80%。這種差異導致實驗室STC(隔音等級)評估值與實際環境中的表現有偏差。未經處理的有機纖維織物容易發黴,散發出違反醫療衛生標準的異味,需要事先更換。目前,規範制定者缺乏統一的防潮等級標準,只能依賴經驗法則,導致競標週期延長。缺乏專門的ISO標準意味著與潮濕相關的挑戰仍然存在,阻礙了其在快速成長的熱帶市場的應用。

細分市場分析

預計在2026年至2031年的預測期內,隔音窗簾的複合年成長率將達到5.72%,逐步蠶食降噪產品在2025年佔據的46.68%的市場佔有率。這一趨勢表明,終端用戶在視訊通話中對完全隔音的需求日益成長,因為即使是1分貝的差異都至關重要。因此,隔音窗簾市場,尤其是隔音型隔音窗簾市場,其成長速度超過了整體市場需求。符合企業採購標準的規格也支撐了這一成長。在綜合用途建築中,業主擴大選擇隔音窗簾作為隔間牆,以有效隔離住宅單元與相鄰零售和娛樂場所非營業時段的噪音。

隔音窗簾集隔音、遮光和隔熱功能於一體,在寒冷地區越來越受歡迎,節能效果足以彌補高成本。 Moondream 的取得專利的設計採用金屬化層反射中頻噪音,並配以棉氈襯裡吸收室內混響,從而兼具多種性能。雖然工業用戶過去通常偏好厚重的乙烯基覆膜產品以滿足降噪標準,但如今更輕的住宅隔音窗簾也能達到類似的性能水平,縮小了不同用戶群之間的差距。

區域分析

到2025年,亞太地區將佔全球銷售額的41.78%,預計在2026年至2031年的預測期內將以6.05%的複合年成長率成長,這主要得益於中國出口主導工廠的發展以及印度都市化進程的加快。青島凱迪蘭在2024年實現了銷售額的成長,其產品主要出口到北美和歐洲,鞏固了在亞太地區標準化窗簾供應領域的主導地位。廣東創亞利用規模經濟和勞動力優勢,將大部分產品出口海外,並將產品價格設定在遠低於歐美競爭對手的水平。日本和韓國正積極回應消費者對環境議題的關注,將生產重點轉向高利潤的天然纖維和再生PET產品。在東協沿海城市,潮濕氣候抑制了聚酯產品的銷售,促使企業加大對防潮混紡織物的研發投入。

在北美,市場情勢呈現兩極化。紐約、西雅圖和多倫多等沿海城市優先選擇符合LEED認證標準且帶有清晰環境產品聲明(EPD)的窗簾,而內陸各州則更注重降低初始成本,並透過位於加拿大和墨西哥的回收中心從亞太地區採購產品。美國人均支出最高,主要得益於企業政策,例如為在家工作的員工提供隔音補貼。同時,加拿大將於2025年7月生效的「生產者延伸責任制」(EPR)法規,強制要求在公共工程中增加再生材料的使用。

歐洲已製定了最高的環保合規標準。自2000年以來,歐盟在PVC回收方面取得了顯著進展,一項新的「綠色交易」旨在到2030年將紡織廢棄物的收集量翻倍。由於沒有舊窗簾回收系統的產品會受到買家的處罰,因此PET氈和羊毛的使用量正在增加。 EN 13501-1標準的消防安全法規已嚴格執行,未經認證的進口產品實際上被排除在公共競標之外。此外,由於能源價格波動,德國和義大利的設施業主越來越傾向於使用多層窗簾,因為這種窗簾可以顯著降低冬季供暖成本。

南美洲、中東和非洲等地區正迎來發展機會。在巴西,經濟實惠的聚氨酯產品在聖保羅和里約熱內盧的高層建築市場佔據主導地位,這些城市優先考慮隔音和隱私,同時又避免採用嚴格的消防安全標準。在海灣合作理事會(GCC)地區,沙烏地阿拉伯的大型企劃(如新未來城)正在接受高階供應商,但由於對快速交付的需求,擁有本地庫存的供應商更具優勢。同時,在南非,儘管外匯波動導致進口量下降,但電子商務的興起使得小型窗簾能夠直接送達消費者手中。然而,全部區域缺乏統一的標準,導致平均售價下降,並延長了認證投資的回報週期。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 遠距辦公與家庭工作室文化的興起

- 工業噪音的暴露限值已經收緊。

- 評估聲學舒適度的綠建築積分

- 基於物聯網的聲學監測正在推動維修需求。

- 促進循環經濟的法規鼓勵使用可回收窗簾。

- 市場限制因素

- 潮濕氣候下的性能下降

- 新興市場消防安全認證的差異

- 多層PVC複合材料的可回收性低

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 隔音

- 降噪

- 隔音

- 材料

- 玻璃絨

- 岩絨

- 發泡塑膠

- 天然纖維

- 高密度乙烯基層壓板

- 再生PET氈

- 最終用戶

- 住宅

- 商業

- 產業

- 醫療和教育設施

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Acoustical Surfaces Inc.

- Amcraft Manufacturing

- Enviro

- Flexshield Group Pty Ltd

- Guangzhou Dajulong Acoustic Material

- Haining Juncheng Textile Co.,Ltd

- Hofa-Akustik

- Hunter Douglas

- Impact Acoustic AG

- Kinetics Noise Control Inc.

- LANTAL

- MMT Acoustix

- Moondream

- Quiet Curtains

- Quietco

- Rose Brand

- Shanghai Zaiqiang Acoustic

- Sound Seal

第7章 市場機會與未來展望

According to Mordor Intelligence, the soundproof curtains market size was valued at USD 2.29 billion in 2025 and is estimated to grow from USD 2.41 billion in 2026 to reach USD 3.13 billion by 2031, at a CAGR of 5.33% during the forecast period (2026-2031).

This report is Segmented by Type (Sound-Insulating, Noise-Reducing, Sound-Blocking), Material (Glass Wool, Rock Wool, Plastic Foams, Natural Fibers, and More), End-User (Residential, Commercial, Industrial, Healthcare and Educational Facilities), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Soundproof Curtains Market Trends and Insights

Industrial Noise-Exposure Limits Becoming Stricter

With OSHA and European Union (EU) regulators ramping up audits on sound levels in factories and warehouses, operators are now investing in engineering controls whenever decibel readings exceed the threshold over an 8-hour shift. Movable barriers, increasingly adopted by automotive, e-commerce, and food-processing plants, are not only more cost-effective than rigid enclosures but also offer the added advantage of being relocated during layout changes. Quarterly noise-monitoring mandates, introduced in 2025 across Germany, France, and Italy, have resulted in a spike in order backlogs for heavy vinyl-laminate curtains known for their high attenuation. In the rapidly expanding Asia-Pacific markets, multinationals are aligning their worker-safety reporting with stringent European Union (EU) standards, leading to a heightened demand for certified acoustic drapes, even in areas where local regulations are still evolving.

Green-Building Credits Rewarding Acoustic Comfort

Developers are turning to curtain-based absorption systems, which complement ceiling panels and sound masking, as LEED v4.1 awards credits for indoor acoustic quality and WELL v2 sets background limits. These acoustic credits are in high demand among landlords, as LEED-certified offices can command premium rents in major cities, establishing a direct link between curtain investments and revenue boosts. Certification bodies are now emphasizing Environmental Product Declarations that spotlight embodied carbon, sidelining PVC-laminate products due to their recyclability issues. Suppliers like Knauf Insulation are integrating bio-based binders into their glass-wool cores, ensuring compliance with VOC and formaldehyde standards, and aligning their acoustic products with green-building criteria.

Performance Degradation in Humid Climates

When relative humidity exceeds 70%, polyester-fiber curtains experience a drop in attenuation. Test observations indicate that swollen fibers reduce internal porosity. In coastal regions such as Indonesia, Vietnam, and the Philippines, humidity levels often exceed 80% for most of the year. This discrepancy leads to a gap between laboratory STC ratings and real-world performance. Untreated organic fabrics, which are susceptible to mold and mildew, emit odors that violate healthcare hygiene standards, necessitating premature replacement. Currently, specifiers lack a unified humidity-resilience label and rely on anecdotal evidence, which extends tender cycles. Without a dedicated ISO standard, humidity challenges have persisted, hindering adoption in tropical growth markets.

Other drivers and restraints analyzed in the detailed report include:

- IoT-Enabled Acoustic Monitoring Spurring Retrofit Demand

- Circular-Economy Mandates Favoring Recyclable Drapes

- Fire-Safety Certification Gaps in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sound-blocking curtains are projected to grow at a 5.72% CAGR during the forecast period of 2026-2031, gradually reducing the 46.68% revenue share held by noise-reducing products in 2025. This trend highlights the demand among end-users for complete acoustic isolation during video calls, where every decibel is critical. As a result, the market for soundproof curtains, particularly sound-blocking variants, is expanding at a faster rate than overall demand. This growth is supported by specifications that align with enterprise procurement criteria. In mixed-use buildings, owners are increasingly selecting sound-blocking curtains for party walls to effectively shield apartments from the after-hours noise of adjacent retail entertainment.

Sound-insulating curtains, which combine noise reduction with blackout and thermal benefits, are gaining popularity in colder regions, where energy savings justify the higher costs. Moondream's patented design features a metalized layer that reflects mid-frequency noise and a cotton-felt backing that absorbs internal echoes, showcasing a blend of diverse performance attributes. While industrial buyers have traditionally preferred heavy vinyl laminate to meet noise reduction standards, lighter residential-grade blocking curtains are now achieving comparable performance levels, narrowing the distinctions between user categories.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 41.78% of global revenue and is projected to grow at a 6.05% CAGR through the forecast period of 2026-2031, fueled by China's export-driven factories and India's urban expansion. Qingdao Catilan, having boosted its 2024 revenue, predominantly exports to North America and Europe, reinforcing the region's leadership in standardized curtain supplies. Guangdong Chuangya, leveraging scale and competitive labor, exports most of its production overseas, pricing its products significantly lower than Western counterparts. Japan and South Korea are pivoting towards high-margin natural fibers and recycled PET variants, resonating with consumer environmental concerns. In coastal ASEAN cities, humidity-related challenges are curbing polyester sales, prompting intensified research and development into moisture-resistant blends.

North America showcases a split landscape. Coastal hubs such as New York, Seattle, and Toronto prioritize LEED-compliant drapes with explicit Environmental Product Declarations (EPDs), while inland states focus on upfront costs, sourcing Asia-Pacific products via consolidation centers in Canada and Mexico. The United States tops per-capita spending, aided by corporate policies reimbursing employees for home-office acoustic enhancements. At the same time, Canada's Extended Producer Responsibility (EPR) regulations, effective July 2025, are mandating heightened recycled content in public initiatives.

Europe sets the gold standard for environmental compliance. Since 2000, the bloc has made significant strides in PVC recycling, and with the new Green Deal, aims to double textile-waste recovery by 2030. Curtains lacking end-of-life take-back schemes face buyer penalties, leading to a rise in PET felt and wool usage. Fire regulations in EN 13501-1 are rigorously enforced, effectively excluding non-certified imports from public tenders. Additionally, energy price fluctuations are prompting facility owners in Germany and Italy to favor multi-layer curtains, which offer substantial winter heating savings.

Regions such as South America, the Middle-East and Africa are ripe for exploration. In Brazil, high-rise markets in Sao Paulo and Rio emphasize acoustic privacy, sidestepping stringent fire ratings, allowing cost-effective polyurethane products to dominate. In the Gulf Cooperation Council, mega-projects such as Saudi Arabia's Neom are receptive to premium suppliers but demand rapid turnarounds, benefiting vendors with local storage. While currency shifts in South Africa curtail import volumes, e-commerce is stepping in, delivering small-format curtains to consumers. However, a lack of standardized benchmarks across these regions depresses average selling prices and elongates the payback period for certification investments.

- Acoustical Surfaces Inc.

- Amcraft Manufacturing

- Enviro

- Flexshield Group Pty Ltd

- Guangzhou Dajulong Acoustic Material

- Haining Juncheng Textile Co.,Ltd

- Hofa-Akustik

- Hunter Douglas

- Impact Acoustic AG

- Kinetics Noise Control Inc.

- LANTAL

- MMT Acoustix

- Moondream

- Quiet Curtains

- Quietco

- Rose Brand

- Shanghai Zaiqiang Acoustic

- Sound Seal

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in remote-working and home-studio culture

- 4.2.2 Industrial noise-exposure limits becoming stricter

- 4.2.3 Green-building credits rewarding acoustic comfort

- 4.2.4 IoT-enabled acoustic monitoring spurring retrofit demand

- 4.2.5 Circular-economy mandates favouring recyclable drapes

- 4.3 Market Restraints

- 4.3.1 Performance degradation in humid climates

- 4.3.2 Fire-safety certification gaps in emerging markets

- 4.3.3 Limited recyclability of multi-layer PVC composites

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Sound-insulating

- 5.1.2 Noise-reducing

- 5.1.3 Sound-blocking

- 5.2 By Material

- 5.2.1 Glass Wool

- 5.2.2 Rock Wool

- 5.2.3 Plastic Foams

- 5.2.4 Natural Fibers

- 5.2.5 High-density Vinyl Laminate

- 5.2.6 Recycled PET Felt

- 5.3 By End-user

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Healthcare and Educational Facilities

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Acoustical Surfaces Inc.

- 6.4.2 Amcraft Manufacturing

- 6.4.3 Enviro

- 6.4.4 Flexshield Group Pty Ltd

- 6.4.5 Guangzhou Dajulong Acoustic Material

- 6.4.6 Haining Juncheng Textile Co.,Ltd

- 6.4.7 Hofa-Akustik

- 6.4.8 Hunter Douglas

- 6.4.9 Impact Acoustic AG

- 6.4.10 Kinetics Noise Control Inc.

- 6.4.11 LANTAL

- 6.4.12 MMT Acoustix

- 6.4.13 Moondream

- 6.4.14 Quiet Curtains

- 6.4.15 Quietco

- 6.4.16 Rose Brand

- 6.4.17 Shanghai Zaiqiang Acoustic

- 6.4.18 Sound Seal

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

隔音窗簾市場:2026-2032年全球市場預測(依產品類型、材料、應用、銷售管道和最終用戶分類)

隔音窗簾市場:2026-2032年全球市場預測(依產品類型、材料、應用、銷售管道和最終用戶分類) 全球隔音門市場:市場規模、佔有率和趨勢分析(按材料類型、應用和地區分類),細分市場預測(2026-2033 年)

全球隔音門市場:市場規模、佔有率和趨勢分析(按材料類型、應用和地區分類),細分市場預測(2026-2033 年) 隔音窗簾市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,預測2026-2034年

隔音窗簾市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,預測2026-2034年 2026年全球隔音窗簾市場報告

2026年全球隔音窗簾市場報告 隔音窗簾市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、材料、最終用途、地區和競爭格局分類,2021-2031年)

隔音窗簾市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、材料、最終用途、地區和競爭格局分類,2021-2031年) 隔音窗簾市場規模、佔有率和成長分析(按材料、產品功能、最終用途、通路和地區分類)-2026-2033年產業預測隔音塗料市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、應用、地區和競爭細分,2020-2030 年)

隔音窗簾市場規模、佔有率和成長分析(按材料、產品功能、最終用途、通路和地區分類)-2026-2033年產業預測隔音塗料市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、應用、地區和競爭細分,2020-2030 年)