|

市場調查報告書

商品編碼

2062172

EMC屏蔽和測試設備:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031年)EMC Shielding And Test Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

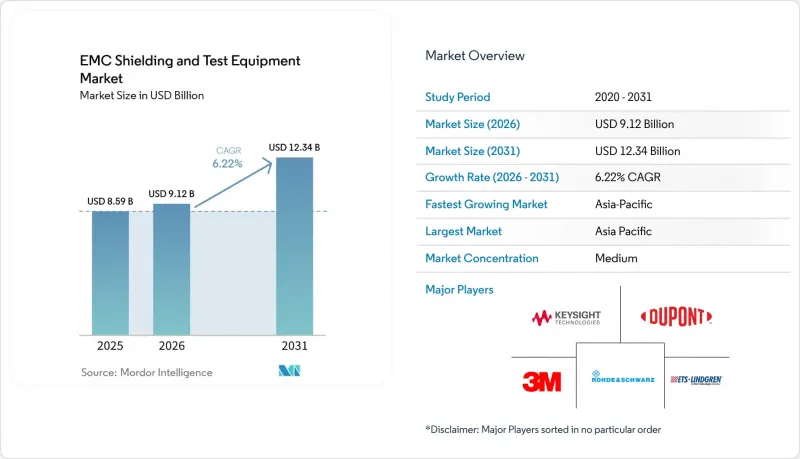

據 Mordor Intelligence 稱,2025 年電磁干擾屏蔽和測試設備市場價值為 85.9 億美元,預計到 2031 年將達到 123.4 億美元,而 2026 年為 91.2 億美元,2026 年至 2031 年的複合年成長率為 6.2%。

本報告按產品類型(屏蔽材料和EMC測試設備)、屏蔽材料類型(導電塗層和塗料、導電墊片和O型圈等)、測試設備類型(EMI接收機和頻譜分析儀等)、終端用戶行業(家用電子電器、汽車等)以及地區進行細分。市場預測以美元(USD)為單位。

全球電磁屏蔽與測試設備市場趨勢及洞察

電動車和高級駕駛輔助系統 (ADAS) 的電氣化增加了每個平台上與電磁相容性 (EMC) 相關的組件數量。

電動驅動系統正推動電磁相容性(EMC)屏蔽和測試設備市場朝向更複雜的屏蔽架構發展。這是因為工作頻率超過10 kHz、電壓高達800 V的牽引逆變器會透過電池電纜、底盤接地和ADAS線束產生傳導和輻射干擾。 TE Connectivity將電動車平台的屏蔽分為三個獨立的層:機殼、模組層和PCB層,每一層都有其自身的衰減目標和檢驗要求。發表在《能源》(Energies)雜誌上的一項2025年研究發現,標準線路感應網路(LISN)無法完全捕捉牽引驅動系統中的差模傳導電磁干擾。這意味著電動車專案將需要更多客製化的測量裝置和更長的測試週期。材料設計也在發生變化,Neklar推出了用於電動車電池機殼的雙功能屏蔽層,將EMC屏蔽和阻燃性能整合於單一結構中。此外,聯合國歐洲經濟委員會第 10 號條例第七次修訂版將電子子組件輻射發射的上限頻率從 2,000 MHz 提高到 6,000 MHz(2025 年 6 月生效),加強了所有旨在獲得聯合國歐洲經濟委員會認證的汽車測試實驗室的天線和接收器要求。

5G和高頻無線技術的擴展

隨著5G的部署,EMC屏蔽和測試設備市場也從中受益,通訊業者和設備製造商需要能夠有效覆蓋整個24 GHz至44 GHz頻寬的新型無線測試系統和屏蔽材料。 ETSI EN 301 489-50 V2.4.1將於2025年9月正式發布,其中規定了行動電話基地台、中繼器及相關設備的最新EMC要求,從而滿足了對修訂後的OTA測試配置的新需求。發表在《計算電子學雜誌》(Journal of Computational Electronics)上的一項研究展示了共形表面擇頻元件(FSS)的設計,該表面在26 GHz 5G n258頻段內,入射角從0°到80°均能保持穩定的抑製作用,凸顯了大規模生產中材料性能精度的重要性。這種轉變也推動了精密加工的發展,因為毫米波性能不僅取決於材料的體電導率和填料含量,還取決於其形狀、配合度和一致性。隨著歐盟成員國計畫於 2026 年 6 月全面採用 ETSI EN 301 489-50 V2.4.1 標準,以及 2027 年 6 月將逐步淘汰相互衝突的標準,EMC 屏蔽和測試設備市場整體上正持續向符合標準的方向發生強勁轉變。

電腔和射頻測量儀器的資本密集度很高

由於完全符合標準的暗房和射頻測量設備需要大量的初始投資,電磁相容性(EMC)屏蔽和測試設備市場在推廣應用方面仍面臨巨大的障礙。新建一個完全消音室的成本在50萬至200萬美元之間,翻新系統的成本在8萬至40萬美元之間,更換吸音材料的成本在4萬至20萬美元之間,而年度校準成本在3000至1.5萬美元之間。隨著聯合國歐洲經濟委員會(UNECE)R10修訂版7對部分汽車測試增加了混響室的要求,旨在完全符合標準的實驗室可能需要多種類型的測試暗室,而不僅僅是一個消音室。這種成本負擔迫使許多中小製造商使用第三方測試實驗室,導致整個EMC屏蔽和測試設備市場測試能力集中化和測試週期緊張。為此,ATEC 和 NTD Shielding 於 2025 年 6 月推出了共用密閉室租賃池。這表明,在難以完全擁有設備的情況下,「設備即服務」模式正在成為一種切實可行的解決方案。

細分市場分析

至2025年,屏蔽材料將佔EMC屏蔽和測試設備市場的62.41%。這反映了屏蔽材料在電子製造幾乎所有領域的應用,從消費性電子產品到航空航太電子設備。 EMC屏蔽和測試設備市場的這一細分領域包括導電塗層、墊片、層壓板、膠帶、箔片和金屬機殼,許多產品在同一組件中使用了多層此類材料。預計EMC測試設備將以6.35%的複合年成長率成長,成為2031年成長最快的產品類型。這是由於隨著標準的修訂,認證測試實驗室和OEM設計團隊必須不斷測量不斷變化的要求。

在電磁相容性(EMC)屏蔽和測試設備產業,這兩類產品系列之間的界線正在逐漸模糊。這是因為預合規測試台擴大與參考屏蔽組件和設計團隊應用指南一同銷售。汽車零件供應商也在採購預合規測試台,這些測試台能夠模擬聯合國歐洲經濟委員會(UNECE)R10修訂版7要求的瞬態容差特性,從而在早期設計階段減少對外部測試實驗室的依賴。 Nolato公司報告稱,其2025年工程解決方案部門的銷售額將達到41.01億瑞典克朗(約合4.24億美元,約合3.87億美元),其中材料子部門在2025年第四季度實現了近10%的調整後成長,這主要得益於資料中心和通訊行業的需求成長。這種結構轉變表明,儘管透過製程導電塗層可以輕鬆更換部分材料層,但EMC屏蔽和測試設備行業仍然重視能夠滿足新型計算和通訊專案需求的供應商。

層壓板、膠帶和箔片是屏蔽材料中成長最快的細分市場,預計2026年至2031年間,該類別下的EMC屏蔽和測試設備市場將以6.42%的複合年成長率成長。這些材料的優勢在柔軟性,因為在諸如弧形電動汽車電池外殼、ADAS模組內的扁平電纜以及折疊式顯示器組件等應用中,往往難以在不犧牲空間或重量的情況下採用剛性屏蔽結構。同時,金屬外殼和機櫃仍然發揮著重要作用,尤其是在工業電力電子、伺服器和機架系統中,在這些應用中,屏蔽體積比品質更為重要。

由於導電塗層具有高效的屏蔽性能、輕巧的特性、生產柔軟性和成本效益,因此在電磁相容性(EMC)屏蔽和測試設備市場中佔據了31.63%的佔有率。隨著智慧型手機、平板電腦、筆記型電腦、穿戴式裝置、物聯網產品和5G技術的日益普及,用於保護電子元件免受訊號干擾的電磁干擾(EMI)屏蔽解決方案的需求顯著成長。這些塗層和塗料之所以被廣泛採用,是因為它們可以輕鬆應用於緊湊型設備機殼和印刷電路基板。與傳統的金屬屏蔽不同,導電塗層能夠在不顯著增加重量或體積的情況下提供可靠的電磁防護,使其成為小型攜帶式電子設備的理想選擇。

區域分析

預計到2025年,亞太地區將佔據47.84%的市場佔有率,該地區的EMC屏蔽和測試設備市場預計到2031年將以6.51%的複合年成長率成長。中國繼續發揮主導領導作用,因為大規模的EMC合規性投資對於電動車生產、5G部署和國內半導體投資至關重要。 2025年2月發布的GB/T 18655-2025標準將汽車EMC測試頻率範圍擴展至5925 MHz,並增加了電動車專用測試設定和V2X保護要求。 2025年12月發布的GB/T 46894-2025標準引入了IC級汽車EMC測試,華為和奇瑞汽車等參與了標準起草,這表明中國汽車EMC標準的發展路徑將更加獨立自主。日本和韓國對顯示器、功率半導體和消費性電子產品的需求仍然強勁,而印度正在崛起為製造地。為了支持本地電子產品生產,Nolato 在班加羅爾開設了一家符合 EMC 標準的工廠。

北美是電磁相容性屏蔽和測試設備的第二大區域市場,這得益於其成熟的商業測試能力以及航太和國防領域的高價值需求。美國聯邦通訊委員會(FCC)在2025年至2026年間採取的一系列措施(包括撤銷已獲認可測試實驗室的認證、逐步停止在非互認國家/地區進行測試,以及於2026年6月15日生效的「可信賴測試實驗室」流程)正在重塑美國認證的收入分成結構。此外,美國和加拿大正在大力支持人工智慧資料中心的建設,從而催生了對屏蔽外殼、墊圈以及與800G硬體相關的高頻檢驗工具的新需求。墨西哥尤其受益於電動車電池組製造地的近岸汽車組裝,這推動了當地對預合規能力和屏蔽整合的需求。

歐洲仍然是電磁相容屏蔽和測試設備市場,政策主導市場佔據主導地位。 EN 61000-6-4:2026、ETSI EN 301 489-50 V2.4.1 和 UNECE R10 第 7 版均積極採納或實施。德國羅德與施瓦茨公司繼續保持其測量設備中心的地位,而總部位於法國的 Emitech 公司於 2026 年 1 月收購了 ExoTest 3E 的資產,從而鞏固了其在汽車電磁兼容服務領域的地位。南美洲市場規模雖小,但正穩步成長,這主要得益於 ANATEL 相關合規性需求和當地汽車組裝的推動。中東地區則透過阿拉伯聯合大公國和沙烏地阿拉伯等國主導的5G 部署和資料中心投資,正在培育未來的需求。在非洲,認證仍然主要依賴歐洲認可的測試實驗室,導致當地測試基礎設施有限,儘管仍有空間滿足電信和工業設備進口帶來的材料需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 5G和高頻無線技術的普及

- 電動車和高級駕駛輔助系統 (ADAS) 的電氣化增加了每個平台上的電磁相容性 (EMC) 組件數量。

- 更嚴格的電磁相容性法規和認證義務

- 裝置小型化和電子密度提高

- 根據聯合國歐洲經濟委員會(UNECE)和GB/T標準的修訂,汽車電磁相容性(EMC)測試範圍擴大。

- 800G 基礎架構中的 AI 伺服器和 EMI 熱點

- 市場限制因素

- 電鏡及射頻設備資本密集度高

- 電磁相容性工程人員短缺和測試日益複雜。

- 毫米波及40 GHz以上頻段的校準不確定度

- 先進電子產品中熱學、氣流和電磁干擾重新設計中的權衡取捨

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 屏蔽材料

- EMC測試設備

- 按屏蔽材料類型

- 導電塗料和油漆

- 導電墊片和O形圈

- 層壓板/膠帶和箔片

- 金屬外殼和機櫃

- 按測試設備類型

- EMI接收器和頻譜分析儀

- 射頻功率放大器

- 天線和探針

- 瞬態現象/靜電放電發生器

- EMC考試軟體

- 按最終用戶行業分類

- 家用電子產品

- 車

- 通訊和IT基礎設施

- 航太/國防

- 醫療器材

- 工業和能源

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 以色列

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Rohde & Schwarz GmbH & Co. KG

- Keysight Technologies, Inc.

- ETS-Lindgren Inc.

- 3M Company

- Parker-Hannifin Corporation

- DuPont de Nemours, Inc.(Laird Performance Materials)

- Henkel AG & Co. KGaA

- PPG Industries, Inc.

- TE Connectivity Ltd.

- Amphenol Corporation

- Nolato AB

- Methode Electronics, Inc.

- Leader Tech Inc.

- Boyd Corporation

- Teseq AG

- Intertek Group plc

- SGS SA

- Bureau Veritas SA

- Yokogawa Electric Corporation

- Anritsu Corporation

- Kitagawa Industries Co., Ltd.

- EM Test(GmbH)

- LISUN Group

- TDK Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the eMC shielding and test equipment market was valued at USD 8.59 billion in 2025 and is estimated to grow from USD 9.12 billion in 2026 to reach USD 12.34 billion by 2031, growing at a CAGR of 6.22% from 2026 to 2031.

This report is Segmented by Product Type (Shielding Materials, and EMC Test Equipment), Shielding Material Type (Conductive Coatings and Paints, Conductive Gaskets and O-Rings, and More), Test Equipment Type (EMI Receivers and Spectrum Analyzers, and More), End-User Industry (Consumer Electronics, Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global EMC Shielding And Test Equipment Market Trends and Insights

EV And ADAS Electrification Raising EMC Content Per Platform

Electric drivetrains are pushing the EMC shielding and test equipment market toward more complex shielding architectures because traction inverters above 10 kHz and up to 800 V create conducted and radiated interference across battery cables, chassis grounds, and ADAS harnesses. TE Connectivity identified 3 separate shielding layers for EV platforms: enclosure, module, and PCB level, and each layer has its own attenuation target and validation requirements. A 2025 study in Energies found that standard LISNs do not fully capture differential-mode conducted EMI in traction drives, which means more custom measurement setups and longer test cycles for EV programs. Material design is also shifting, as Neklar introduced dual-function shielding for EV battery enclosures that combines EMC containment with flame resistance in one structure. UNECE Regulation No. 10, Revision 7, also extended the upper radiated emissions frequency for electronic sub-assemblies from 2,000 MHz to 6,000 MHz in June 2025, raising the antenna and receiver requirements for every automotive laboratory seeking UNECE accreditation.

5G And High-Frequency Wireless Expansion

The EMC shielding and test equipment market is also benefiting from the 5G rollout, as operators and device makers need new over-the-air test systems and shielding materials that remain effective across the 24 GHz to 44 GHz range. ETSI EN 301 489-50 V2.4.1 formalized updated EMC conditions for cellular base stations, repeaters, and related equipment in September 2025, which supports fresh demand for revised OTA test configurations. Research in the Journal of Computational Electronics demonstrated a conformal frequency-selective surface design with stable suppression from 0° to 80° incidence at the 26 GHz 5G n258 band, underscoring the need for precise material performance at the production scale. The same shift favors precision fabrication, because mmWave performance depends heavily on geometry, fit, and consistency rather than only on bulk conductivity or filler loading. National adoption of ETSI EN 301 489-50 V2.4.1 across European Union member states is due by June 2026, and conflicting standards are scheduled for withdrawal by June 2027, which keeps the compliance transition active across the EMC shielding and test equipment market.

High Capital Intensity Of Chambers And RF Instrumentation

The EMC shielding and test equipment market still faces a significant adoption barrier because full-compliance chambers and RF instrumentation require substantial upfront spending. New fully anechoic chambers cost USD 500,000 to USD 2 million; refurbished systems cost USD 80,000 to USD 400,000; absorber replacement runs USD 40,000 to USD 200,000; and annual calibration adds USD 3,000 to USD 15,000. UNECE R10 Revision 7 adds reverberation chamber requirements for some automotive tests, so labs seeking full compliance may need more than one chamber type instead of a single anechoic setup. That cost burden pushes many small and mid-sized manufacturers toward third-party labs, which concentrate test capacity and create scheduling pressure during launch periods across the EMC shielding and test equipment market. ATEC and NTD Shielding responded with a shared-chamber rental pool in June 2025, demonstrating that equipment-as-a-service models are becoming a practical answer when outright ownership is difficult.

Other drivers and restraints analyzed in the detailed report include:

- Stricter EMC Regulations And Certification Mandates

- AI Server And 800G Infrastructure EMI Hot Spots

- EMC Engineering Talent Shortage And Test Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Shielding materials accounted for 62.41% of the EMC shielding and test equipment market in 2025, reflecting their use across nearly every electronics manufacturing category, from consumer devices to aircraft avionics. This side of the EMC shielding and test equipment market covers conductive coatings, gaskets, laminates, tapes, foils, and metal enclosures, and many products use more than one of these layers in the same assembly. That broad distribution across enclosures, modules, and PCB structures explains why materials revenue outpaced test equipment revenue in 2025. At the same time, EMC test equipment with 6.35% CAGR is the faster-growing product type through 2031 because revised standards keep changing what qualified laboratories and OEM design teams need to measure.

The line between the 2 product groups is narrowing across the EMC shielding and test equipment industry, because pre-compliance benches are increasingly sold with reference shielding assemblies and application guidance for design teams. Automotive suppliers are also buying pre-compliance benches that mirror the transient immunity profiles required under UNECE R10 Revision 7, thereby reducing dependence on external labs during early design work. Nolato reported FY2025 Engineered Solutions revenue of SEK 4,101 million (USD 424 million), which was approximately USD 387 million, and its materials sub-segment posted adjusted growth of nearly 10% in Q4 2025, led by data center and telecom demand. That mix shift suggests the EMC shielding and test equipment industry is rewarding suppliers that can serve newer compute and communications programs, even as in-process conductive coatings make switching easier in parts of the materials tier.

Laminates, tapes, and foils are the fastest-growing subsegment of shielding materials, with the EMC shielding and test equipment market for this category forecast to expand at a 6.42% CAGR from 2026 to 2031. Their advantage lies in flexibility, as curved EV battery housings, ribbon cables in ADAS modules, and foldable display assemblies often cannot use rigid shielding structures without incurring space or weight penalties. Metal enclosures and cabinets remain important where bulk shielding matters more than mass, especially in industrial power electronics, servers, and rack systems.

Conductive coatings accounted for 31.63% share of the EMC shielding and test equipment market due to their ability to combine effective shielding performance with lightweight characteristics, production flexibility, and cost efficiency. The growing use of smartphones, tablets, laptops, wearable devices, IoT products, and 5G technologies has significantly increased the demand for EMI shielding solutions that protect electronic components from signal interference. These coatings and paints are extensively adopted because they can be easily applied to compact device enclosures and printed circuit boards. Unlike conventional metal shielding, conductive coatings provide reliable electromagnetic protection without adding substantial weight or bulk, making them highly suitable for compact, portable electronic devices.

Geography Analysis

Asia-Pacific held a 47.84% share in 2025, and the regional EMC shielding and test equipment market is forecast to grow at a 6.51% CAGR through 2031. China remains the center of that lead because EV production, 5G deployment, and domestic semiconductor investment all carry mandatory EMC compliance spending at scale. GB/T 18655-2025 extended vehicle EMC test coverage to 5,925 MHz and added EV-specific setups and V2X protection requirements in February 2025. GB/T 46894-2025, published in December 2025, introduced IC-level vehicle EMC testing and included Huawei and Chery Automobile among the drafters, which points to a more independent automotive EMC standards path in China. Japan and South Korea add strong demand from displays, power semiconductors, and consumer appliances, while India is emerging as a manufacturing base, with Nolato opening an EMC-capable facility in Bangalore to support local electronics production.

North America is the second-largest regional market for EMC shielding and test equipment, supported by mature commercial test capacity and high-value demand from the aerospace and defense sector. FCC actions across 2025 and 2026, including revoked lab recognitions, the proposed phase-out of non-reciprocal country testing, and the Trusted Test Lab process effective June 15, 2026, are reshaping where certification revenue goes within the United States. The United States and Canada also anchor much of the AI data center build-out, which is adding a fresh demand stream for shielded enclosures, gaskets, and high-frequency validation tools tied to 800G hardware. Mexico is benefiting from nearshored automotive assembly, especially in EV battery pack manufacturing corridors, which is raising local demand for pre-compliance capability and shielding integration.

Europe remains a policy-led market for EMC shielding and test equipment, as EN 61000-6-4:2026, ETSI EN 301 489-50 V2.4.1, and UNECE R10 Revision 7 are all in active adoption or implementation. Germany remains the instrumentation hub through Rohde and Schwarz, while France-based Emitech strengthened its automotive EMC service position by acquiring ExoTest 3E assets effective January 2026. South America is smaller but growing steadily, driven by ANATEL-related compliance demand and local automotive assembly, while the Middle East is building future demand through 5G densification and data center investment led by the United Arab Emirates and Saudi Arabia. Africa still relies mainly on European-accredited laboratories for certification, which limits local testing infrastructure but leaves room to shield material demand in telecom and industrial equipment imports.

- Rohde & Schwarz GmbH & Co. KG

- Keysight Technologies, Inc.

- ETS-Lindgren Inc.

- 3M Company

- Parker-Hannifin Corporation

- DuPont de Nemours, Inc. (Laird Performance Materials)

- Henkel AG & Co. KGaA

- PPG Industries, Inc.

- TE Connectivity Ltd.

- Amphenol Corporation

- Nolato AB

- Methode Electronics, Inc.

- Leader Tech Inc.

- Boyd Corporation

- Teseq AG

- Intertek Group plc

- SGS SA

- Bureau Veritas SA

- Yokogawa Electric Corporation

- Anritsu Corporation

- Kitagawa Industries Co., Ltd.

- EM Test (GmbH)

- LISUN Group

- TDK Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G and High-Frequency Wireless Expansion

- 4.2.2 EV and ADAS Electrification Raising EMC Content Per Platform

- 4.2.3 Stricter EMC Regulations and Certification Mandates

- 4.2.4 Device Miniaturization and Higher Electronics Density

- 4.2.5 Expanded Automotive EMC Test Scope Under UNECE and GB/T Updates

- 4.2.6 AI Server and 800G Infrastructure EMI Hot Spots

- 4.3 Market Restraints

- 4.3.1 High Capital Intensity of Chambers and RF Instrumentation

- 4.3.2 EMC Engineering Talent Shortage and Test Complexity

- 4.3.3 mmWave and Above-40 GHz Calibration Uncertainty

- 4.3.4 Thermal-Airflow and EMI Redesign Tradeoffs in Advanced Electronics

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Shielding Materials

- 5.1.2 EMC Test Equipment

- 5.2 By Shielding Material Type

- 5.2.1 Conductive Coatings and Paints

- 5.2.2 Conductive Gaskets and O-rings

- 5.2.3 Laminates / Tapes and Foils

- 5.2.4 Metal Enclosures and Cabinets

- 5.3 By Test Equipment Type

- 5.3.1 EMI Receivers and Spectrum Analyzers

- 5.3.2 RF Power Amplifiers

- 5.3.3 Antennas and Probes

- 5.3.4 Transient / ESD Generators

- 5.3.5 EMC Test Software

- 5.4 By End-user Industry

- 5.4.1 Consumer Electronics

- 5.4.2 Automotive

- 5.4.3 Telecom and IT Infrastructure

- 5.4.4 Aerospace and Defense

- 5.4.5 Medical Devices

- 5.4.6 Industrial and Energy

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Israel

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Rohde & Schwarz GmbH & Co. KG

- 6.4.2 Keysight Technologies, Inc.

- 6.4.3 ETS-Lindgren Inc.

- 6.4.4 3M Company

- 6.4.5 Parker-Hannifin Corporation

- 6.4.6 DuPont de Nemours, Inc. (Laird Performance Materials)

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 PPG Industries, Inc.

- 6.4.9 TE Connectivity Ltd.

- 6.4.10 Amphenol Corporation

- 6.4.11 Nolato AB

- 6.4.12 Methode Electronics, Inc.

- 6.4.13 Leader Tech Inc.

- 6.4.14 Boyd Corporation

- 6.4.15 Teseq AG

- 6.4.16 Intertek Group plc

- 6.4.17 SGS SA

- 6.4.18 Bureau Veritas SA

- 6.4.19 Yokogawa Electric Corporation

- 6.4.20 Anritsu Corporation

- 6.4.21 Kitagawa Industries Co., Ltd.

- 6.4.22 EM Test (GmbH)

- 6.4.23 LISUN Group

- 6.4.24 TDK Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

EMC屏蔽與測試設備市場:2026-2032年全球市場預測(產品類型、測試類型、頻寬、客戶類型、最終用戶產業和銷售管道)

EMC屏蔽與測試設備市場:2026-2032年全球市場預測(產品類型、測試類型、頻寬、客戶類型、最終用戶產業和銷售管道) 全球電磁相容屏蔽和測試設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球電磁相容屏蔽和測試設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年) EMC屏蔽和測試設備市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、材質、設備、部署類型和最終用戶分類

EMC屏蔽和測試設備市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、材質、設備、部署類型和最終用戶分類 EMC屏蔽和測試設備市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、地區和競爭格局分類,2020-2030年預測

EMC屏蔽和測試設備市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、地區和競爭格局分類,2020-2030年預測 EMC 屏蔽和測試設備市場預測(至 2032 年):按類型、測試類型、頻率範圍、最終用戶和地區進行的全球分析

EMC 屏蔽和測試設備市場預測(至 2032 年):按類型、測試類型、頻率範圍、最終用戶和地區進行的全球分析 全球EMC屏蔽和測試設備市場

全球EMC屏蔽和測試設備市場 EMC 屏蔽和測試設備市場報告:趨勢、預測和競爭分析(至 2031 年)

EMC 屏蔽和測試設備市場報告:趨勢、預測和競爭分析(至 2031 年)