|

市場調查報告書

商品編碼

2062168

黑磷:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Black Phosphorus - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

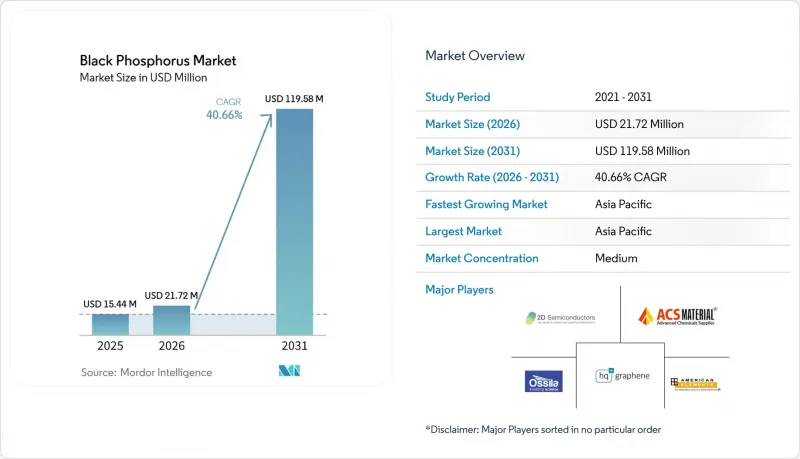

據 Mordor Intelligence 稱,黑磷市場在 2025 年的價值為 1,544 萬美元,預計到 2026 年將擴大到 2,172 萬美元,到 2031 年將達到 1.1958 億美元。

預計 2026 年至 2031 年的複合年成長率將達到 40.66%。

本報告按形態(粉末、晶體、剝離奈米片、薄膜)、應用領域(電子和半導體、儲能、光電和光電子學、生物醫學和生物感測器、環境催化劑和水處理、其他)以及地區(亞太地區、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元計價。

全球黑磷市場趨勢與洞察

軟性及高頻電子產品對2D半導體的需求激增。

2024年,以超音波剝離法製備的黑磷奈米帶電晶體展現出1.7 × 10⁶的開關比和1,506 cm²V⁻¹s⁻¹的遷移率,滿足了5奈米以下藍圖圖的要求。推動其應用的主要因素之一是其寬度相關的帶隙,帶隙範圍為0.29 eV至0.64 eV。這項特性使得設計人員能夠獨立於合金化製程改變邏輯電平,從而提供設計柔軟性。另一個重要因素是材料的面內異向性,這使得定向電荷控制成為可能。這項特性在可彎曲顯示器等需要精確電荷控制的應用中尤其重要。採用光滑邊緣的通道可以抑制短溝道效應,即使在柵極長度小於20 nm的情況下,也能保持200 µSµm⁻¹以上的跨導水平,而矽元件在20 nm以下通常會出現漏電流問題。此外,能夠在低於150 度C的轉變溫度下運作是製造商的關鍵考慮因素,因為它滿足了穿戴式技術中常用的聚醯亞胺基板的要求。此外,在美國國家科學基金會(NSF)的支持下,於2026年推出的表面配位化學技術實現了在室溫下長達一個月的穩定性。這種穩定性有望在加速這些電晶體的商業化過程中發揮關鍵作用,並成為黑磷市場的上游收入來源。

基於黑磷的光子積體電路的快速普及

Iris Light Technologies公司利用NanoBLACK™材料,在標準CMOS晶圓上實現了1550nm波長下11.2 A W⁻¹的驚人靈敏度。透過採用扭曲堆疊元件,探測範圍擴展至2700nm,並實現了雙極圓偏振鑑別——這是加密自由空間光學元件的關鍵功能。面外應變控制使得諧振模式在-3%壓縮下無需熱負載即可紅移超過100nm,為高密度光子佈線鋪平了道路。這種材料不僅在近紅外線頻譜內量子效率超越了二硫化鉬,而且與石墨烯不同,它具有帶隙,能夠實現高效調製。美國空軍研究實驗室(AFRL)於2025年簽署的契約,凸顯了最終用戶對這些先進技術應用於國防級中紅外線系統的信心。

在室溫和空氣中穩定性差,封裝成本高。

未保護的奈米片在72小時內紫外-可見光吸收率顯著下降60%。這種劣化需要手套箱操作和使用多層屏障,可能使總成本增加高達50%。與Oxaliplatin配位可將吸收率提高至62%。細胞膜塗層可進一步將吸收率提高至78%,但每增加一層都會增加材料和人事費用。聚多巴胺薄膜可將這些奈米片的壽命延長至數週,但這種改進會使原料成本增加30%。嵌入PLGA中可提供緩釋機制,但會導致成本增加35-45%。使用植酸進行電化學剝離可製備邊緣鈍化的薄片,從而最大限度地減少封裝後的後處理。然而,其處理能力仍低於每批10克,限制了其工業實用性。電池製造商面臨的挑戰是如何將陽極的價格控制在每克5美元以下,以保持與石墨的競爭力。相比之下,光電領域的買家更加靈活,願意為每克支付 500 至 1000 美元,並且更容易控制間接成本。

細分市場分析

2025年,粉狀黑磷佔了36.67%的市佔率。這主要得益於其在電池漿料和催化劑等領域的應用,這些應用能夠適應不規則形狀。剝離奈米片的價格在每克800至1200美元之間,預計將以41.23%的年成長率成長。這一成長源於裝置工程師對厚度小於10奈米且邊緣原子級光滑的奈米片的需求不斷成長。黑磷奈米片市場預計將從2026年的570萬美元成長到2031年的3,600萬美元。純度超過99.999%的晶體因其優異的性能而持續受到研究者的關注。然而,由於晶圓級化學氣相沉積(CMV)方法的競爭,其市場佔有率可能會下降。目前,諸如分子束外延等薄膜沉積方法在元件級材料的覆蓋率不足8%。 Chips-Act 試點生產線有望透過提高生產力和降低缺陷率 50% 來降低成本。

據設備製造商稱,超音波剝離技術可實現95%的奈米帶良率,有助於減少分類後的廢棄物。由於降低了邊緣粗糙度,奈米片在電晶體遷移率和檢測器靈敏度方面優於粉末燒結層。同時,粉末仍然是陽極原型的主要材料,成本上限為0.20美元/瓦時。這是因為粉末的下游研磨製程與現有的漿料生產線非常契合。隨著二氧化碳剝離技術的規模化應用,黑磷市場中奈米片的價格可能會降至每克150美元左右。這種價格調整有望消除傳統的溢價,並鞏固其在複合年成長率方面的地位。

區域分析

預計到2025年,亞太地區將佔全球銷售額的47.78%,複合年成長率達41.56%。在亞太地區,中國已採用瑞豐的二氧化碳工藝,將批次週期從15天縮短至3天。這項製程使變動成本顯著降低了98%,為江蘇和廣東兩省的本地電池工廠提供了支援。此外,日本和韓國正致力於光電和邏輯基準測試的進步。兩國已公佈了有關自旋輸運和掌性檢測的重要數據,預計將對計劃於2028年進行的晶圓廠評估產生影響。

在北美,美國空軍研究實驗室(AFRL)和國家科學基金會(NSF)的專案資金主要用於光電的安全通訊和氧化穩定性化學。然而,由於國內生產商尚未達到千噸產能,該地區仍依賴進口。這種依賴性使買家面臨來自亞太地區的運輸成本和前置作業時間風險。加拿大正積極進行自旋輸運研究,墨西哥則正在進行環境催化劑的試驗。儘管如此,該地區的商業化生產仍然有限。

在歐洲,REACH法規的模糊性帶來了許多挑戰,可能導致產品認證週期延長至多一年。儘管《晶片法案》的津貼旨在增強該地區的競爭力,但試點生產線仍依賴從中國進口的晶種。這種依賴性使得現貨價格居高不下,超過每克500美元。義大利和西班牙在生物醫學領域處於主導,正致力於研究可控分解技術,以加速骨再生支架的開發。此外,巴西和南非的新興產業叢集正在探索利用催化劑進行水淨化。然而,15%至25%的進口關稅阻礙了這些努力,延緩了舉措的實施。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 軟性電子和高頻電子領域對2D半導體的需求激增。

- 基於黑磷的光子積體電路的快速普及

- 下一代鋰/鈉離子電池主流BP負極材料的研究與開發資金

- 利用BP技術對中紅外線隱身和安全通訊塗層進行國防投資

- 歐盟的「晶片」試點生產線津貼正在加速晶圓級黑磷合成。

- 市場限制因素

- 大氣不穩定和封裝成本增加

- 奈米材料毒性方面的監管不確定性

- 由於智慧財產權集中在 BP(業務流程)分離路線上,導致授權成本上升。

- 價值鏈分析

- 波特五力分析

第5章:預測市場規模與成長率

- 按形狀

- 粉末

- 水晶

- 可剝離奈米片

- 薄膜

- 透過使用

- 電子和半導體

- 儲能(電池、超級電容)

- 光電和光電子學

- 生物醫學生物感測器

- 環境催化劑和水處理

- 其他(添加物、研究級等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 2D Semiconductor

- ACS Material

- American Elements

- Aritech Chemazone Pvt. Ltd.

- ATT Advanced elemental materials Co., Ltd.

- Borophene LLC

- HQ Graphene

- Merch KgGA

- Nanjing XFNANO Materials Tech Co.,Ltd

- NANOCHEMAZONE

- Nanografi Advanced Materials.

- Ossila Ltd

- RASA Industries, LTD.

- Shandong Ruifeng Chemical Co Ltd

- SixCarbon Technology(Shenzhen)

- Smart-Elements GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the black phosphorus market, valued at USD 15.44 million in 2025, is projected to grow to USD 21.72 million in 2026 and is expected to reach USD 119.58 million by 2031, with a CAGR of 40.66% from 2026 to 2031.

This report is Segmented by Form (Powder, Crystal, Exfoliated Nanosheets, Thin Films), Application (Electronics and Semiconductors, Energy Storage, Photonics and Optoelectronics, Biomedical and Biosensors, Environmental Catalysis and Water Treatment, Others), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Black Phosphorus Market Trends and Insights

Surging Demand for 2D Semiconductors in Flexible and High-Frequency Electronics

In 2024, nanoribbon transistors fabricated from sonochemically exfoliated black phosphorus demonstrated on/off ratios of 1.7 X 106 and mobilities of 1,506 cm2 V-1 s-1, meeting the sub-5 nm roadmap thresholds. One of the key drivers for their adoption is the width-dependent bandgaps, which range from 0.29 eV to 0.64 eV. This feature allows designers to modify logic levels without relying on alloying processes, providing flexibility in design. Another significant driver is the material's in-plane anisotropy, which enables directional charge control. This characteristic is particularly important for applications such as bendable displays, where precise charge control is essential. The use of smooth-edge channels addresses short-channel effects, ensuring that transconductance levels remain above 200 µS µm-1 at gate lengths smaller than 20 nm, a size where silicon typically encounters increased leakage issues. Additionally, the ability to operate at transfer temperatures below 150 °C is a critical factor for manufacturers, as it aligns with the requirements of polyimide substrates commonly used in wearable technology. Furthermore, surface-coordination chemistry supported by the NSF and introduced in 2026 provides ambient stability lasting up to a month. This stability is expected to play a significant role in accelerating the commercialization of these transistors.he upstream revenue stream of the black phosphorus market.

Rapid Uptake of BP-Based Photonic Integrated Circuits

Using NanoBLACK(TM), Iris Light Technologies achieved an impressive 11.2 A W-1 responsivity at 1,550 nm on standard CMOS wafers. By employing twist-stacked devices, they expanded detection capabilities to 2,700 nm and incorporated bipolar circular-polarization discrimination, a crucial feature for encrypted free-space optics. Through out-of-plane strain engineering, they successfully red-shifted cavity modes by over 100 nm under -3% compression, even without thermal loading, paving the way for dense photonic routing. This material not only surpasses molybdenum disulfide in quantum efficiency within the near-infrared spectrum but also boasts a bandgap, unlike graphene, facilitating efficient modulation. The 2025 contract from AFRL underscores the end-user's confidence in translating these advancements to defense-grade mid-IR systems.

Ambient-Air Instability and Encapsulation Cost Premium

Unprotected nanosheets experience a significant reduction of 60% in UV-visible absorption within 72 hours. This degradation necessitates the use of glovebox handling and multi-layer barriers, which can increase landed costs by up to 50%. Coordination bonding with oxaliplatin improves absorption retention to 62%. Cell-membrane coatings further enhance retention to 78%, although each additional layer contributes to increased material and labor costs. Polydopamine films are capable of extending the lifespan of these nanosheets to several weeks, but this improvement comes with a 30% rise in raw material expenses. Embedding in PLGA offers a slow-release mechanism but results in a cost increase of 35-45%. Electrochemical exfoliation in phytic acid produces edge-passivated flakes that require minimal post-encapsulation processing. However, the throughput remains limited to less than 10 grams per batch, which restricts its industrial relevance. Battery manufacturers encounter challenges as they must maintain anode prices below USD 5 per gram to remain competitive with graphite. In comparison, buyers in the photonics sector are more accommodating, with a willingness to pay between USD 500 and 1,000 per gram, making it easier for them to manage overhead costs.

Other drivers and restraints analyzed in the detailed report include:

- Mainstream R&D Funding for BP Anodes in Next-Gen Li/Na-Ion Batteries

- Defense Investment in BP-Enabled Mid-IR Stealth and Secure-Comms Coatings

- Regulatory Uncertainty Around Nanomaterial Toxicology

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, powder accounted for 36.67% of the Black phosphorus market share, supported by its application in battery slurries and catalysts that accommodate irregular morphologies. Exfoliated nanosheets, priced at USD 800-1,200 per gram, are expected to grow at a rate of 41.23%. This growth is attributed to the increasing demand from device engineers for thicknesses under 10 nm and atomically smooth edges. The market size for Black phosphorus nanosheets is projected to increase from USD 5.7 million in 2026 to USD 36 million by 2031. Crystals, with a purity level exceeding 99.999%, continue to attract interest for research purposes. However, their market share may decline due to competition from wafer-scale chemical-vapor growth. Thin-film methods, such as molecular beam epitaxy, currently achieve less than 8% device-grade coverage. The Chips-Act pilot lines are anticipated to improve output and reduce defectivity by 50%, potentially lowering costs.

Equipment manufacturers report that sonochemical exfoliation achieves 95% yield for nanoribbons, which helps reduce post-sorting waste. By reducing edge roughness, nanosheets demonstrate better performance than powder-derived sintered layers in both transistor mobility and photodetector responsivity. On the other hand, powder remains a key material for anode prototypes targeting a cost ceiling of USD 0.20 Wh-1, as its downstream milling aligns well with existing slurry lines. With the scaling of CO2 exfoliation, the Black phosphorus market may experience a reduction in nanosheet pricing to approximately USD 150 per gram. This price adjustment could eliminate the historical premium and strengthen their position in terms of compound annual growth rate.

Geography Analysis

In 2025, the Asia-Pacific region contributed 47.78% of global revenue and is projected to grow at a compound annual growth rate (CAGR) of 41.56%. Within the region, China has implemented Ruifeng's CO2 route, which reduces batch cycles from 15 days to 3 days. This process significantly lowers variable costs by 98% and supports local cell factories located in Jiangsu and Guangdong. Additionally, Japan and South Korea are concentrating on advancements in photonic and logic benchmarks. These countries have published notable data on spin-transport and chiral-detection, which are expected to influence fab evaluations planned for 2028.

In North America, funding from AFRL and NSF programs is directed toward secure-communication photonics and oxidative-stability chemistry. However, the region continues to rely on imports, as domestic producers have not yet achieved kilogram-scale throughput. This dependency exposes buyers to risks associated with freight and lead times from the Asia-Pacific region. Canada is actively collaborating on spin transport research, while Mexico is conducting tests on environmental catalysts. Despite these efforts, commercial production volumes in the region remain limited.

Europe is encountering challenges due to ambiguities in REACH regulations, which can extend product-qualification cycles by up to a year. Although Chips-Act grants are intended to enhance the region's competitiveness, pilot production lines still depend on seed crystals imported from China. This reliance keeps per-gram spot prices above USD 500. Italy and Spain are leading efforts in biomedical trials, focusing on controlled degradation techniques to accelerate the development of bone-regrowth scaffolds. In other regions, emerging clusters in Brazil and South Africa are exploring the use of water-purification catalysts. However, these efforts are hindered by import tariffs ranging from 15% to 25%, which delay the implementation of these initiatives.

- 2D Semiconductor

- ACS Material

- American Elements

- Aritech Chemazone Pvt. Ltd.

- ATT Advanced elemental materials Co., Ltd.

- Borophene LLC

- HQ Graphene

- Merch KgGA

- Nanjing XFNANO Materials Tech Co.,Ltd

- NANOCHEMAZONE

- Nanografi Advanced Materials.

- Ossila Ltd

- RASA Industries, LTD.

- Shandong Ruifeng Chemical Co Ltd

- SixCarbon Technology (Shenzhen)

- Smart-Elements GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for 2D semiconductors in flexible and high-frequency electronics

- 4.2.2 Rapid uptake of BP-based photonic integrated circuits

- 4.2.3 Mainstream R&D funding for BP anodes in next-gen Li/Na-ion batteries

- 4.2.4 Defense investment in BP-enabled mid-IR stealth and secure-comms coatings

- 4.2.5 European Union Chips-Act pilot-line grants catalysing wafer-scale BP synthesis

- 4.3 Market Restraints

- 4.3.1 Ambient-air instability and encapsulation cost premium

- 4.3.2 Regulatory uncertainty around nanomaterial toxicology

- 4.3.3 IP thicket on BP exfoliation routes drives licensing costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Form

- 5.1.1 Powder

- 5.1.2 Crystal

- 5.1.3 Exfoliated Nanosheets

- 5.1.4 Thin Films

- 5.2 By Application

- 5.2.1 Electronics and Semiconductors

- 5.2.2 Energy Storage (Batteries and Super-capacitors)

- 5.2.3 Photonics and Optoelectronics

- 5.2.4 Biomedical and Biosensors

- 5.2.5 Environmental Catalysis and Water Treatment

- 5.2.6 Others (Additives, Research-grade, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 2D Semiconductor

- 6.4.2 ACS Material

- 6.4.3 American Elements

- 6.4.4 Aritech Chemazone Pvt. Ltd.

- 6.4.5 ATT Advanced elemental materials Co., Ltd.

- 6.4.6 Borophene LLC

- 6.4.7 HQ Graphene

- 6.4.8 Merch KgGA

- 6.4.9 Nanjing XFNANO Materials Tech Co.,Ltd

- 6.4.10 NANOCHEMAZONE

- 6.4.11 Nanografi Advanced Materials.

- 6.4.12 Ossila Ltd

- 6.4.13 RASA Industries, LTD.

- 6.4.14 Shandong Ruifeng Chemical Co Ltd

- 6.4.15 SixCarbon Technology (Shenzhen)

- 6.4.16 Smart-Elements GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

黑磷市場:2026-2032年全球市場預測(按應用、製造方法、形態、層數和最終用戶分類)磷及其衍生物市場:按產品類型、製造技術、純度等級、應用和分銷管道分類的全球市場預測,2026-2032年黑磷陽極材料市場(按電池技術、類型、最終用途和等級分類),全球預測(2026-2032)2D黑磷市場依產品類型、層數、應用及銷售管道分類-2026-2032年全球預測多晶黑磷市場按產品類型、純度等級、製造方法、應用和最終用途產業分類-2026年至2032年全球預測永續磷市場:依來源、技術、形態、用途、終端用戶產業及通路分類,全球預測(2026-2032年)紅磷市場按用途、形態和等級分類 - 全球預測 2026-2032黑磷奈米片分散體市場:全球預測(2026-2032 年),按形態、製造方法、等級、應用和最終用途產業分類黑磷奈米片市場:2026-2032年全球預測(按應用、製造方法、層數和等級分類)黑磷粉市場依純度等級、粒徑、製造方法、應用和最終用途產業分類-2026-2032年全球預測

黑磷市場:2026-2032年全球市場預測(按應用、製造方法、形態、層數和最終用戶分類)磷及其衍生物市場:按產品類型、製造技術、純度等級、應用和分銷管道分類的全球市場預測,2026-2032年黑磷陽極材料市場(按電池技術、類型、最終用途和等級分類),全球預測(2026-2032)2D黑磷市場依產品類型、層數、應用及銷售管道分類-2026-2032年全球預測多晶黑磷市場按產品類型、純度等級、製造方法、應用和最終用途產業分類-2026年至2032年全球預測永續磷市場:依來源、技術、形態、用途、終端用戶產業及通路分類,全球預測(2026-2032年)紅磷市場按用途、形態和等級分類 - 全球預測 2026-2032黑磷奈米片分散體市場:全球預測(2026-2032 年),按形態、製造方法、等級、應用和最終用途產業分類黑磷奈米片市場:2026-2032年全球預測(按應用、製造方法、層數和等級分類)黑磷粉市場依純度等級、粒徑、製造方法、應用和最終用途產業分類-2026-2032年全球預測