|

市場調查報告書

商品編碼

2062163

數位教育出版:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Digital Education Publishing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

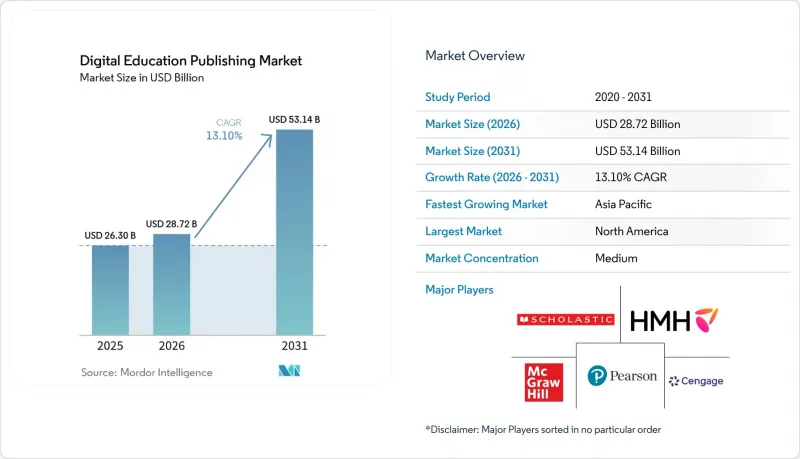

據 Mordor Intelligence 稱,2025 年數位教育出版市場價值 263 億美元,預計到 2031 年將達到 531.4 億美元,而 2026 年為 287.2 億美元,預測期(2026-2031 年)複合年成長率為 13.10%。

本報告依內容類型(數位教材、互動課件等)、最終使用者(中小學教育機構、高等教育機構等)和學習形式(自主學習、教師主導學習、混合式學習等)進行分類。市場預測以美元計價,並基於現有數據。

全球數位教育出版市場趨勢與洞察

制度化的混合式學習採購週期可確保多年的收入來源。

學區和教育系統層面強制推行的混合式學習正推動支出轉向3至5年的許可協議,將一次性交易轉變為與學習管理系統(LMS)整合、內容可訪問性和供應商認證進展掛鉤的可續約合約。在美國19個州和華盛頓特區,教科書的採用已實現集中化,正式的徵求提案書(RFP)已將LTI 1.3、WCAG 2.2和Section 508的合規性從“理想”屬性提升為州級核准的強制性要求,通過在多年採用周期內獎勵合規供應商,穩定了數字教育出版市場。政府平台越來越重視數位化優先的內容,印度的PM e-VIDYA和DIKSHA就是支持全國分發的典型例子。隨著政府機構對儲存庫和內容元資料進行標準化,出版商正在調整其產品藍圖,以適應公共工作流程和多語言需求。中國的「人工智慧+教育」行動計畫涵蓋從小學到高等教育的各個階段,目標是在2030年前將人工智慧融入所有課程體系。這推動了對可與省級平台整合的數位化學習材料以及人工智慧賦能的在地化內容的需求。在歐洲,「數位教育行動計畫」著重於互通性和教師能力建設,鼓勵內容提供者參與標準化,並在設計階段就考慮可近性。這使他們能夠在跨境計畫中保持影響力,並維持整個數位教育出版市場的創新潛力。由於採購優先考慮的是持續整合而非單一產品,數位教育出版市場的轉型成本正在上升,這使得那些與學區工作流程和數據系統緊密相關的供應商更具優勢。

與課程相符的強制性數位化評估將重塑內容開發的經濟結構。

強制性的形成性評估和學習進度監測正在將出版商從單純的內容提供者轉變為持續的診斷和分析合作夥伴,為課程規劃和課堂教學介入提供資訊支援。當教育部門明確定義數位技能目標時,此框架最為有效。正如歐盟政策指南所示,它正在重塑數位教育出版市場的需求結構,鼓勵投資於可互通的平台,這些平台能夠跨學校託管和共用評估結果,同時提升學生的電腦素養和資訊素養。中國的「人工智慧+教育」方向催生了對多語言、多文字內容在地化和人工智慧輔助評估的需求,省級智慧平台服務於大規模的用戶群體,能夠利用內建的診斷功能解決學習滯後問題。雖然人工智慧正在加速試題生成,但人工參與的工作流程仍然至關重要。同行評審的人工智慧輔助試題生成研究也支持了這一點,這些研究表明,人工智慧輔助試題生成具有可擴展性,但仍需要專家審核以確保品質和公平性。因此,內容、評估和分析將整合到與教育機構許可證相關的持續服務中,而不是成為單獨的教科書週期的一部分,從而加強數位教育出版市場的持續收入來源。

盜版和薄弱的數位版權管理阻礙了新興市場的收入成長。

在網路連線不穩定的地區,交付方式的選擇不僅會影響未經授權的再分發風險,尤其是在教育資料需要長時間離線存取的情況下。在行動和固定寬頻價格過高的市場,用戶往往更依賴快取和側載內容,這增加了資料外洩的風險,也使得數位教育出版市場中優質內容的投資報酬率 (ROI) 計算變得更加複雜。在學校網路部署仍處於早期階段的地區,持續的身份驗證和許可檢查往往不足,降低了基於雲端的 DRM檢驗工作流程的有效性,迫使內容提供者考慮適用於間歇性網路連接環境的替代管理方法。當國家平台預設開放基礎資料的存取權限時,出版商會透過對自適應和分析功能等高級功能進行分割來保護其價值,從而影響數位教育出版市場的整體產品策略。在這種環境下,針對本地網路連接和學校設備策略量身定做的打包模型和交付保護措施的需求仍然存在,這可能會改變 DRM 架構的設計理念。

細分市場分析

到2025年,數位教科書將佔數位教育出版市場佔有率的44.36%。這反映了各國引進週期的持續推進以及核心課程在正規採購中確立的既定地位。預計到2031年,身臨其境型和模擬式教學模式將以21.87%的複合年成長率快速成長,隨著教育機構和雇主對模擬臨床、工程和安全關鍵環境的體驗式學習的需求不斷成長,數位教育出版市場的範圍也將隨之擴大。歐洲對國家數位平台和學校網路的投資正在推動以多媒體為中心的教學方法的發展。這提高了內容包裝和可訪問性的標準,而這些標準僅靠教科書無法滿足,從而影響了出版商靜態內容和互動式內容的組合平衡。數位教育出版產業也在優先考慮能夠與技能追蹤和包容性存取等政策目標相契合的、可進行分析的資源。這使得自適應和可評估的內容成為正規教育創新策略的核心。雖然國家級資源庫提供基礎學習材料,但出版商正專注於高級功能,例如自適應反饋、進度儀表板和安全的考試監考,從而在開放內容之外建立獨特的優勢,並與數位教育出版市場的教育機構保持合約關係。

隨著人工智慧驅動的創作工具縮短開發週期,互動式課件和評估材料的應用持續擴展。同時,人工檢驗確保了心理測量的質量,這已透過專家監督下進行的、經同行評審的人工智慧生成測試題研究得到證實。寬頻和設備的普及推動了多媒體內容在更豐富格式領域的應用。此外,數據整合夥伴關係將評估與課程連結起來,在課堂和學區層面實現個人化學習。受教育機構採用基於情境的、可衡量的、嵌入式任務和分析的學習方式的推動,身臨其境型和模擬內容的數位教育出版市場預計到2031年將以21.87%的複合年成長率成長。在參考和補充內容領域,與開放教育資源(OER)的競爭日益激烈,需要透過適應性、可近性和經證實的學習效果來實現差異化,以滿足公共部門的期望。這些變化共同推動著整個數位教育出版市場從靜態PDF轉向具有評估功能的動態模組,以符合新的標準和政策目標。

到2025年,K-12和高等教育機構總合將佔據37.75%的市場佔有率,但預計到2031年,企業和專業學習者市場將以19.39%的複合年成長率成長,因為各機構都在投資於有針對性的技能發展和檢驗的資格認證,這些認證可以在其整個人力資源系統中進行追蹤。企業需求集中在技能評估、持續評估和基於角色的內容路徑上,這些都能提高員工的工作效率,從而推動數位教育出版市場向訂閱模式和分析功能整合方向發展。大學相關平台和出版商正在建立技術合作夥伴關係,將人工智慧驅動的搜尋、內容發現和檢驗功能整合到教育工作流程中,從而在數位教育出版市場中維持認證使用和引用的高價。此外,隨著教育買家要求提供符合資料保護法規、可整合到學習管理系統(LMS)目錄中的「無障礙設計」組件,數位教育出版業也從中受益。這促使企業投資於平台可靠性和客戶支持,以滿足社會期望。隨著時間的推移,雇主越來越將經過檢驗的技能與工作準備聯繫起來,基於績效的內容和認證網路將成為競爭優勢,從而提高嵌入式評估在數位教育和出版市場中的價值。

技術和職業培訓機構正受益於國家擴大實驗室、網路連接和教師培訓覆蓋範圍的目標,從而推動了數位教育出版市場中與本地就業路徑相契合的模組化、可堆疊內容的普及。企業專案需要能夠與內部系統相容並支援基於角色的分析的內容,同時又不影響對本地數據的預期,這與歐盟和其他地區不斷發展的標準化趨勢相一致。同時,在K-12和高等教育領域,一致的評估、教師培訓和符合無障礙要求仍然是優先事項,即使在地區和校園層面預算波動的情況下,也能確保合約的穩定續約。這些趨勢表明,數位教育出版市場對檢驗技能發展並支持各類用戶合規性的、富含分析功能的內容有著持續的需求。

區域分析

預計到2025年,北美將佔據31.74%的市場。這得歸功於資金充足的K-12學區和大學項目,這些項目優先考慮將學習管理系統(LMS)產品和分析功能整合到全面的訪問許可中。美國19個州和華盛頓特區集中採用教科書,凸顯了遵守LTI 1.3、WCAG 2.2和Section 508標準的重要性,這些標準已成為數位教育出版市場產品設計和競標資格的基準。教育機構仍然傾向於使用整合輔助功能工具和身分管理的基於瀏覽器的存取方式,以支援以網路為先的學習資源庫。同時,行動應用程式可以滿足特定的使用場景和以往服務不足的情況。該地區課程中診斷和分析功能的普及,增強了數位教育出版市場供應商的永續收入模式,這些供應商能夠證明其學習效果和政策一致性。隨著時間的推移,這些功能將增加轉換成本,並使那些能夠證明其與學區教學和評估資料流整合和相容性的供應商更具優勢。

亞太地區是成長最快的地區,預計到2031年將以15.99%的複合年成長率成長,這得益於公共部門對網路連接、設備和智慧教育平台的大規模投資。印度近期預算撥款持續支持學校的數位資源和基礎設施建設,促使政府系統更多地使用平台,教師也積極採納,這與PM e-VIDYA和DIKSHA等國家舉措相契合。這促進了數位教育出版市場的大規模內容髮現和分發。中國的「人工智慧+教育」行動計畫設定了2030年廣泛應用人工智慧課程的目標,透過利用支援大量學習者的省級平台,加速大規模區域性數位教育出版內容和評估能力。東協市場的網路存取和連線速度差異顯著。因此,出版商需要調整產品頻寬情況,同時為國家計畫推動的數位經濟發展做好準備。隨著有關國家雲端和資料居住的法規不斷發展,供應商正在採用特定區域的託管和隱私保護措施,這使得公共採購以及與數位教育出版市場的教育機構建立長期夥伴關係成為可能。

在歐洲,隨著歐盟層級的專案引導互通解決方案和技能成果的發展方向,以及成員國負責採購和共同資金籌措,數位教育正穩步成長。 「2021-2027年數位教育行動計畫」優先考慮教師能力、平台互通性和學生數位技能方面的可衡量進展,從而影響著數位教育出版市場供應商在可訪問性、標準化和分析方面的優先事項。德國的「數位計畫2.0」為2026年至2030年的Wi-Fi、設備和培訓撥款,一旦獲得地方政府的配套資金,這將大大擴展富媒體和混合式教學能力。歐盟對資料保護的期望正在推動託管和分析模式的發展,這些模式既支持教育機構的使用,又不會損害隱私,這進一步促使數位教育出版市場的內容打包和評估設計與公共部門的要求保持一致。在中東、非洲和拉丁美洲的一些市場,連接性和學校網路正在根據國家數位總體規劃進行擴展,預計這將逐步擴大學校和職場中以數位優先內容傳送的用戶群。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 制度化的混合式學習採購週期

- 與課程相符的強制性數位化評估

- LMS原生內容包日益普及

- 行動優先的存取方式推動了消費成長。

- 互通性認證正日益影響採購決策。

- GenAI題庫速度測驗準備

- 市場限制因素

- 盜版和薄弱的數位版權管理導致資訊外洩。

- 寬頻和設備取得方面的差距

- LMS收入正在對利潤率造成壓力。

- 無障礙維修會增加生產成本

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 為教育工作者提供支援和實施服務

- 內容創作與生命週期經濟(問題庫、元資料、更新)

- 波特五力分析

第5章 市場規模與成長預測

- 按內容類型

- 電子教科書

- 互動式課件

- 評估和考試準備材料

- 參考資料和補充資料

- 多媒體內容

- 身臨其境型與模擬內容

- 最終用戶

- K-12教育機構

- 高等教育機構

- 商業和專業的學習者

- 技術與職業培訓機構

- 自學者

- 透過學習形式

- 自主學習

- 教師主導學習

- 混合式/融合式學習

- 同步虛擬課堂

- 透過配送通路

- 基於網路的平台和門戶

- 行動學習應用

- 學習管理系統(LMS)

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 哥倫比亞

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(瑞典、挪威、丹麥、芬蘭、冰島)

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 東南亞(新加坡、印尼、馬來西亞、泰國、越南、菲律賓)

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、合作、產品發布)

- 市佔率分析

- 公司簡介

- Pearson

- McGraw Hill

- Cengage Learning

- John Wiley & Sons

- Houghton Mifflin Harcourt

- Oxford University Press

- Cambridge University Press

- Scholastic Corporation

- Elsevier(Health Education)

- Springer Nature

- Savvas Learning Company

- Discovery Education

- Hachette Livre(Hodder Education)

- Georg von Holtzbrinck(Macmillan Education)

- SAGE Publishing

- Sanoma Learning

- Santillana

- Nelson(Canada)

- Hodder Education

- Vibal Group

- Diwa Learning Systems

- VitalSource Technologies(distribution/content partnerships)

- Chegg

- IXL Learning

- Coursera

- Udemy

第7章 市場機會與未來展望

According to Mordor Intelligence, the digital education publishing market size was valued at USD 26.30 billion in 2025 and is estimated to grow from USD 28.72 billion in 2026 to reach USD 53.14 billion by 2031, at a CAGR of 13.10% during the forecast period (2026-2031).

This report is Segmented by Content Type (Digital Textbooks, Interactive Courseware, and More), End User (K-12 Educational Institutions, Higher Education Institutions, and More), Learning Format (Self-Paced Learning, Instructor-Led Learning, Blended/Hybrid Learning, and More), and More. The Market Forecasts are Provided in Terms of Value (USD), Based On Availability.

Global Digital Education Publishing Market Trends and Insights

Institutionalized Hybrid Learning Procurement Cycles Lock Multi-Year Revenue Streams

District- and system-level hybrid learning mandates channel spending into three-to-five-year licenses, turning one-off transactions into renewals anchored to LMS integration, content accessibility, and vendor certification trajectories. Where textbook adoption is centralized across 19 U.S. states plus Washington, D.C., formal RFPs elevate LTI 1.3, WCAG 2.2, and Section 508 compliance from nice-to-have attributes to eligibility gates for state-level approvals, stabilizing the digital education publishing market by rewarding compliant vendors during multi-year adoption cycles . Government platforms place greater weight on digital-first content, as illustrated by India's PM e-VIDYA and DIKSHA, which support national-scale distribution; when ministries standardize repositories and content metadata, publishers adapt product roadmaps to align with public workflows and multilingual needs. China's "AI + Education" action plan spans primary through higher education, with a 2030 horizon for full AI course integration, reinforcing demand for digital courseware and localized AI-aligned content that can connect to provincial platforms. In Europe, the Digital Education Action Plan frames interoperability and teacher capacity-building, pushing content providers toward standards participation and accessible-by-design production processes to remain relevant in cross-border programs, which sustains renewal potential across the digital education publishing market. As procurement focuses on durable integrations rather than discrete titles, the digital education publishing market faces higher switching costs, favoring vendors entrenched in district workflows and data systems.

Curriculum-Aligned Digital Assessment Mandates Restructure Content Development Economics

Mandated formative assessment and progress monitoring shift publishers from content shipments to ongoing diagnostic and analytics partners that feed lesson planning and intervention at the classroom scale. The framework effect is clearest where ministries outline explicit digital skills targets, as seen in the EU's policy track to raise computer and information literacy while directing investment into interoperable platforms that can host and share assessment outcomes across schools, thereby reshaping demand in the digital education publishing market . China's "AI + Education" direction produces content localization and AI-supported assessment needs across languages and scripts, with provincial smart platforms serving large installed bases that can use embedded diagnostics to close learning gaps. Human-in-the-loop workflows remain essential even as AI accelerates item creation, as evidenced by peer-reviewed research on AI-assisted test generation that documents scalability alongside the persistent need for expert review to ensure quality and fairness. The net effect is that content, assessment, and analytics converge into continuous services tied to institutional licenses rather than discrete textbook cycles, which reinforces recurring revenue for the digital education publishing market.

Piracy and Weak DRM Erode Revenue Capture in Emerging Markets

Low-connectivity environments influence delivery choices and can raise exposure to unauthorized redistribution when materials need to be accessible offline for extended periods. In markets where mobile and fixed broadband affordability exceeds benchmark targets, user reliance on cached or sideloaded content increases the risk surface for leakage, complicating ROI on premium titles in the digital education publishing market. Regions with school networks still in early deployment phases often lack persistent identity and license checks, which reduces the effectiveness of cloud-based DRM verification workflows and forces content providers to consider alternative controls suited to intermittent connectivity. When national platforms set open-access defaults for baseline materials, publishers respond by segmenting premium features such as adaptivity and analytics to defend value, which shapes product strategy across the digital education publishing market. This environment sustains a continuous need for packaging models and distribution safeguards aligned with local connectivity profiles and school device policies, which can change the calculus of DRM architectures.

Other drivers and restraints analyzed in the detailed report include:

- LMS-Native Content Bundles Compress Publisher Margins Through Platform Revenue Shares

- Mobile-First Access Expands Addressable Markets in Connectivity-Constrained Geographies

- Uneven Broadband and Device Access Fragments Addressable TAM

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital Textbooks commanded 44.36% of the digital education publishing market share in 2025, reflecting the persistence of state adoption cycles and the embedded role of core curricula in formal procurement. Immersive and simulation-based formats are projected to grow fastest at a 21.87% CAGR through 2031 as institutions and employers seek experiential learning that mimics clinical, engineering, and safety-critical environments, broadening the scope of the digital education publishing market. Europe's investment in national digital platforms and school networks supports multimedia-first pedagogy. It raises the bar for content packaging and accessibility that textbooks alone cannot meet, thereby influencing publishers' portfolio balance between static and interactive assets. The digital education publishing industry is also prioritizing analytics-ready assets that can align with policy objectives such as skill tracking and inclusive access, putting adaptive and assessment-ready content at the center of renewal strategies in formal education. Where national repositories provide baseline materials, publishers focus on premium layers like adaptive feedback, progress dashboards, and secure proctoring to create a moat beyond open content and retain institutional contracts across the digital education publishing market.

Interactive Courseware and Assessment Materials continue to gain adoption as AI-assisted authoring compresses development timelines. At the same time, human validation maintains psychometric quality, as documented in peer-reviewed research on AI-generated test items with expert oversight. Multimedia Content adoption rises where broadband and device availability enable richer formats, with data integration partnerships that connect assessments and curricula to personalize sequencing in classrooms and districts. The digital education publishing market for immersive and simulation content is projected to expand at a 21.87% CAGR through 2031, as institutions procure scenario-based learning that can be measured through embedded tasks and analytics. Reference and supplemental content see more OER competition, which pushes differentiation toward adaptivity, accessibility, and evidence of learning impact that meets public-sector expectations. Together, these shifts move portfolios from static PDFs toward dynamic modules with assessment hooks that align with emerging standards and policy goals across the digital education publishing market.

K-12 and Higher Education Institutions collectively held 37.75% share in 2025, while Corporate and Professional Learners are set to grow at a 19.39% CAGR through 2031 as organizations fund targeted upskilling and verifiable credentials that can be tracked across HR systems. Enterprise demand focuses on skill diagnostics, continuous assessment, and role-based content paths that drive workforce productivity, steering a larger share of the digital education publishing market toward subscription delivery and analytics integrations. University-linked platforms and publishers are forming technology partnerships to bring AI-supported search, content discovery, and verification into institutional workflows, which sustains premium pricing for authenticated usage and citation inside the digital education publishing market. The digital education publishing industry also benefits when institutional buyers require accessible-by-design components that integrate into LMS catalogs in line with data protection rules, which encourages investment in platform reliability and customer support aligned with public expectations. Over time, outcome-linked content and credential networks become competitive moats as employers equate verified competencies with job readiness, which elevates the value of embedded assessment across the digital education publishing market.

Technical and vocational training providers benefit from national goals that expand access to labs, connectivity, and teacher development, thereby increasing the adoption of modular, stackable content aligned with local employment paths in the digital education publishing market. Corporate programs seek content that integrates with internal systems and supports role-based analytics without breaching regional data expectations, aligning with evolving standards agendas across the EU and other regions. Meanwhile, the K-12 and higher education segments continue to prioritize aligned assessments, teacher guidance, and compliance with accessibility mandates, which help stabilize renewals even as budgets fluctuate at the district and campus levels. These patterns point to a durable demand base for analytics-rich content that verifies skill gains and supports compliance across diverse user types inside the digital education publishing market.

Geography Analysis

North America secured 31.74% share in 2025, supported by well-funded K-12 districts and campus programs that favor inclusive-access licenses tied to LMS provisioning and analytics. Centralized textbook adoption across 19 states of the United States and Washington, D.C. underscores the importance of LTI 1.3, WCAG 2.2, and Section 508 compliance, which guide product design and bidding eligibility across the digital education publishing market. Institutions also maintain a preference for browser-based access that aligns with accessibility tooling and identity management, which sustains web-first portfolios. At the same time, mobile apps fill specific use cases and underserved contexts. The region's shift toward diagnostic and analytics-infused curricula strengthens recurring revenue models for vendors that can evidence learning impact and policy alignment across the digital education publishing market. Over time, these features add to switching costs and favor vendors with proven integrations and compatibility with district data flows that span instruction and assessment.

Asia-Pacific is the fastest-growing region with a projected 15.99% CAGR to 2031, supported by large-scale public investments in connectivity, devices, and smart education platforms. India's recent budgetary allocations continue to support digital resources and infrastructure for schools, thereby increasing platform usage and teacher adoption in government systems aligned with national initiatives like PM e-VIDYA and DIKSHA, which boost discovery and distribution at scale across the digital education publishing market. China's "AI + Education" action plan sets expectations for AI course coverage through 2030 and leverages provincial platforms that support massive enrollments, accelerating the development of localized content and assessment features in the digital education publishing market. ASEAN markets show wide variation in internet access and speeds, which pushes publishers to tailor SKUs to bandwidth realities while preparing for growth as national programs advance digital-economy ambitions. As national clouds and data-residency rules evolve, vendors adopt region-specific hosting and privacy practices that enable public procurement and long-term institution partnerships in the digital education publishing market.

Europe posts steady gains as EU-level programs set direction for interoperable solutions and skills outcomes while member states manage procurement and co-funding. The Digital Education Action Plan 2021-2027 prioritizes teacher capacity, platform interoperability, and measurable progress in student digital skills, thereby shaping vendor priorities in accessibility, standards, and analytics across the digital education publishing market. Germany's Digitalpakt 2.0 allocates funding from 2026 through 2030 for WLAN, devices, and training, which will expand capacity for rich media and hybrid instruction at scale once local match funding is arranged. EU data protection expectations guide hosting and analytics models that support institutional use without compromising privacy, which further aligns content packaging and assessment design with public-sector requirements in the digital education publishing market. Select markets in the Middle East and Africa and in Latin America continue to expand connectivity and school networks under national digital masterplans, which will progressively widen the addressable user base for digital-first content delivery at school and in the workplace.

- Pearson

- McGraw Hill

- Cengage Learning

- John Wiley & Sons

- Houghton Mifflin Harcourt

- Oxford University Press

- Cambridge University Press

- Scholastic Corporation

- Elsevier (Health Education)

- Springer Nature

- Savvas Learning Company

- Discovery Education

- Hachette Livre (Hodder Education)

- Georg von Holtzbrinck (Macmillan Education)

- SAGE Publishing

- Sanoma Learning

- Santillana

- Nelson (Canada)

- Hodder Education

- Vibal Group

- Diwa Learning Systems

- VitalSource Technologies (distribution/content partnerships)

- Chegg

- IXL Learning

- Coursera

- Udemy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Institutionalized hybrid learning procurement cycles

- 4.2.2 Curriculum-aligned digital assessment mandates

- 4.2.3 LMS-native content bundles scaling adoption

- 4.2.4 Mobile-first access expands consumption

- 4.2.5 Interoperability certifications increasingly drive purchasing

- 4.2.6 GenAI item banks speed test-prep

- 4.3 Market Restraints

- 4.3.1 Piracy and weak DRM leakage

- 4.3.2 Uneven broadband and device access

- 4.3.3 LMS revenue share compresses margins

- 4.3.4 Accessibility retrofits inflate production costs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Educator Enablement & Implementation Services

- 4.8 Content Authoring & Lifecycle Economics (item banks, metadata, updates)

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Competitive Rivalry

- 4.9.2 Threat of New Entrants

- 4.9.3 Bargaining Power of Suppliers

- 4.9.4 Bargaining Power of Buyers

- 4.9.5 Threat of Substitutes

5 Market Size & Growth Forecasts

- 5.1 By Content Type

- 5.1.1 Digital Textbooks

- 5.1.2 Interactive Courseware

- 5.1.3 Assessment & Test-Prep Materials

- 5.1.4 Reference & Supplemental Materials

- 5.1.5 Multimedia Content

- 5.1.6 Immersive & Simulation-Based Content

- 5.2 By End User

- 5.2.1 K-12 Educational Institutions

- 5.2.2 Higher Education Institutions

- 5.2.3 Corporate & Professional Learners

- 5.2.4 Technical & Vocational Training Providers

- 5.2.5 Independent Learners

- 5.3 By Learning Format

- 5.3.1 Self-Paced Learning

- 5.3.2 Instructor-Led Learning

- 5.3.3 Blended / Hybrid Learning

- 5.3.4 Synchronous Virtual Classrooms

- 5.4 By Delivery Channel

- 5.4.1 Web-Based Platforms & Portals

- 5.4.2 Mobile Learning Applications

- 5.4.3 Learning Management Systems (LMS)

- 5.4.4 Others

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Colombia

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Benelux (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 Nordics (Sweden, Norway, Denmark, Finland, and Iceland)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, Product Launches)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Pearson

- 6.4.2 McGraw Hill

- 6.4.3 Cengage Learning

- 6.4.4 John Wiley & Sons

- 6.4.5 Houghton Mifflin Harcourt

- 6.4.6 Oxford University Press

- 6.4.7 Cambridge University Press

- 6.4.8 Scholastic Corporation

- 6.4.9 Elsevier (Health Education)

- 6.4.10 Springer Nature

- 6.4.11 Savvas Learning Company

- 6.4.12 Discovery Education

- 6.4.13 Hachette Livre (Hodder Education)

- 6.4.14 Georg von Holtzbrinck (Macmillan Education)

- 6.4.15 SAGE Publishing

- 6.4.16 Sanoma Learning

- 6.4.17 Santillana

- 6.4.18 Nelson (Canada)

- 6.4.19 Hodder Education

- 6.4.20 Vibal Group

- 6.4.21 Diwa Learning Systems

- 6.4.22 VitalSource Technologies (distribution/content partnerships)

- 6.4.23 Chegg

- 6.4.24 IXL Learning

- 6.4.25 Coursera

- 6.4.26 Udemy

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

數位教育市場預測至2034年—全球解決方案類型、學習方式、部署方式、設備類型、收入模式、應用、最終用戶和地區分析2034年幼兒教育平台市場預測-全球分析(按組件、學習形式、設備類型、應用、最終用戶和地區分類)

數位教育市場預測至2034年—全球解決方案類型、學習方式、部署方式、設備類型、收入模式、應用、最終用戶和地區分析2034年幼兒教育平台市場預測-全球分析(按組件、學習形式、設備類型、應用、最終用戶和地區分類) 2026-2030年全球教育產業數位電子看板市場

2026-2030年全球教育產業數位電子看板市場 翻轉教室市場報告:按產品、最終用戶和地區分類(2026-2034 年)

翻轉教室市場報告:按產品、最終用戶和地區分類(2026-2034 年) 數位教育市場:2026-2032年全球市場預測(按交付方式、內容類型、學習風格、支援的設備、訂閱模式、應用程式和最終用戶分類)

數位教育市場:2026-2032年全球市場預測(按交付方式、內容類型、學習風格、支援的設備、訂閱模式、應用程式和最終用戶分類) 2026年全球數位教育市場報告數位教育出版市場:依格式、主題、定價模式、設備、交付方式及最終用戶分類-2026年至2032年全球預測

2026年全球數位教育市場報告數位教育出版市場:依格式、主題、定價模式、設備、交付方式及最終用戶分類-2026年至2032年全球預測 數位教育市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、設備、部署類型、最終用戶和解決方案分類

數位教育市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、設備、部署類型、最終用戶和解決方案分類 全球數位教育市場規模、佔有率、趨勢和成長分析報告(2026-2034)日本數位學習平台市場規模、佔有率、趨勢及預測(按平台類型、最終用戶和地區分類,2026-2034年)

全球數位教育市場規模、佔有率、趨勢和成長分析報告(2026-2034)日本數位學習平台市場規模、佔有率、趨勢及預測(按平台類型、最終用戶和地區分類,2026-2034年)