|

市場調查報告書

商品編碼

2062155

化學指示劑油墨:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Chemical Indicator Inks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

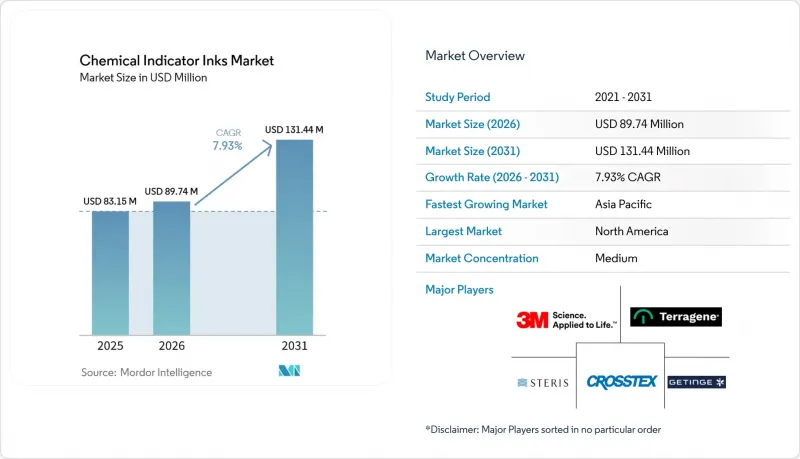

據 Mordor Intelligence 稱,2025 年化學指示劑油墨市場價值為 8,315 萬美元,預計到 2031 年將達到 1.3144 億美元,而 2026 年為 8,974 萬美元,預測期(2026-2031 年)的複合年成長率為 7.93%。

本報告按類型(水性指示劑油墨、其他)、工藝(蒸氣滅菌指示劑、其他)、應用(包裝、標籤、其他)、終端用戶行業(醫院和診所、其他)以及地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲)進行細分。市場預測以美元計價。

全球化學指示劑油墨市場趨勢與洞察

對感染控制規定的認知有所提高

監管機構目前建議使用多參數4型指示劑取代單參數試紙,以應對合規性挑戰。 2025年3月,隨著美國食品藥物管理局(FDA) 批准 ANSI/AAMI ST58:2024 標準,美國醫院將被要求使用可追溯的化學指示劑記錄每個滅菌週期,這些指示劑能夠檢驗時間、溫度和滅菌劑濃度。聯合委員會將於2024年7月和2025年7月更新標準,將這些要求納入認證審核,因此需要對產品進行升級。加拿大 GUI-0074 和歐洲 EN 556-1:2024 標準正在使區域法規與 ISO 11140 標準保持一致,擴大了符合標準的機構數量。這些監管變化正在推動化學指示劑墨水市場的成長,因為高比色系統正成為一項重要的業務投資。

手術量和門診治療量增加

門診手術和機器人輔助手術的成長速度超過了住院手術,這推動了對低溫滅菌器的需求,而低溫滅菌器不能僅僅依賴蒸氣指示劑。直覺外科公司(Intuitive Surgical)報告稱,2025年達文西手術量約為315萬例,較去年同期成長18%,預計2026年將達到兩位數成長。美國醫療保險和醫療補助服務中心(CMS)在2026年新增了573個門診診所代碼,將滅菌工作量分散到眾多小規模的醫療機構,這些機構通常缺乏集中式滅菌部門。每個新增的醫療機構都必須儲備檢驗的指示劑,這確保了供應商的穩定需求,並擴大了化學指示劑墨水的市場潛力。

低收入地區市場意識薄弱

撒哈拉以南非洲的手術部位感染率高達11.8%,遠高於高所得國家的1.9%。由於資金限制,這些地區的許多醫療機構依賴僅監測單一變數的基本型1級試紙,而非使用多參數指示劑。儘管捐助計畫通常會資助滅菌設備,但耗材卻不包含在內,導致技術人員缺乏檢驗滅菌循環所需的工具。此外,相當一部分工作人員缺乏解讀符合國際標準化組織(ISO)標準的指示劑的正式訓練。除非多邊組織的採購指南將化學指示劑的資金納入其中,否則這些指示劑的普及程度預計仍將不平衡。這種不均衡可能會影響這些地區化學指示劑墨水市場的成長潛力。

細分市場分析

預計到2025年,水性油墨將佔印刷油墨市場佔有率的47.12%。這反映了水性油墨與現代印刷機的兼容性,以及其符合中國「十四五」規劃中揮發性有機化合物(VOC)排放限制的要求。隨著醫院和醫療設備製造商加快調整採購政策以符合其淨零排放目標,水性化學指示劑油墨市場預計將穩定成長。富士膠片的AQUAFUZE混合型水性紫外線(UV)油墨系列和太陽化學的SunCure Advance ECO生物可再生油墨等供應商正致力於在提高性能的同時減少碳足跡。

依產品類型分類,UV固化系統以8.36%的複合年成長率成長,在市場中成長最快。這項成長主要得益於即時固化技術,該技術可降低高達60%的能源成本,並提高處理大量標籤的合約滅菌商的處理能力。該技術的應用正在各個行業不斷擴展,例如,Mimaki推出了符合化學品註冊、評估、授權和限制(REACH)法規的ELH油墨,Star Color則提供了低遷移柔版印刷油墨套裝,這兩款產品均在醫藥包裝領域獲得了廣泛認可。此外,擅長開發結合滅菌認證、低溫運輸時間和溫度響應的雙指示劑化學品的供應商,可以進入高階市場,並推動化學指示劑油墨市場的成長。

預計到2025年,蒸氣指示器將佔製程指示器銷售額的36.98%。這主要歸功於全球醫院對高壓釜的廣泛應用。修訂後的ANSI(美國國家標準協會)/AAMI(醫療設備促進協會)ST58:2024標準強制要求使用4型內部監測器,這將增加更換需求,並鞏固蒸氣指示器的市場佔有率。

預計等離子體和氣化過氧化氫指示劑將以 8.14% 的複合年成長率成長。這一成長主要得益於機器人技術的進步、熱敏植入的應用以及食品藥物管理局於 2024 年將其重新歸類為 A 類,從而簡化了檢驗流程。 Getinge 的「Poladus 150」套裝和 Mesa Labs 的「ExpoSure」試劑盒展示了一個由儀器和耗材組成的生態系統,旨在透過專有墨水留住客戶,從而推動化學指示劑墨水市場領先技術供應商的市場佔有率不斷成長。

區域分析

2025年,北美地區佔總銷售額的37.88%。美國醫院採用ANSI/AAMI ST58:2024(美國國家標準協會/醫療設備促進協會)標準,以及製藥業的巨額資本投資,都支撐了市場需求。此外,隨著美國醫療保險和醫療補助服務中心(CMS)擴大門診手術的報銷範圍,基本客群隨之擴大。無線射頻辨識(RFID)檢測技術正從大學附屬醫院逐步推廣至大型綜合醫療網路(IDN),進一步提升了化學指示劑油墨的市場佔有率。

在歐洲,歐盟醫療設備法規 (EU MDR) 的審核、EN 556:2024 標準的協調統一以及 12% 的碳邊境調節關稅的引入,都對水性塗料和 UV(紫外線)塗料的市場發展起到了推動作用。由於二氧化鈦 (TiO2) 關稅的徵收,顏料成本不斷上漲,加工商正在尋求長期供應合約和後向整合,這正在重塑市場競爭格局。

亞太地區是成長最快的地區,預計到2031年複合年成長率將達到8.32%。印度計劃在2030年新增200萬張醫院床位,以及中國要求將揮發性有機化合物(VOCs)排放量減少30%,這些因素共同推動了市場規模的成長和技術的變革。私募股權對亞洲合約研發生產機構(CDMO)和醫院的投資進一步增加了對檢驗的指示劑的需求,加速了化學指示劑油墨市場的擴張。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 提高對感染控制措施的認知

- 手術和門診手術數量增加

- 藥品和醫療設備生產中更嚴格的驗證標準

- 用於資產追蹤的內建RFID的智慧指示標籤

- 智慧油墨在低溫運輸生技藥品包裝的快速應用。

- 市場限制因素

- 低收入地區市場意識薄弱

- 特殊顯色顏料供應不穩定

- 溶劑型油墨載體的永續性壓力

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 水性指示劑墨水

- 溶劑型指示劑油墨

- UV固化指示油墨

- 混合/雙指示器系統

- 透過流程

- 蒸氣滅菌指示器

- 環氧乙烷(EO)滅菌指示劑

- 乾熱滅菌指示器

- 等離子體/過氧化氫氣氣體殺菌指示劑

- 輻射(伽馬射線/電子束)指示器

- 甲醛滅菌指示劑

- 透過使用

- 包裝(袋子、包裝紙、膠帶)

- 標籤和吊牌

- 試紙袋

- 按最終用戶行業分類

- 醫院和診所

- 製藥和醫療設備製造商

- 診斷實驗室

- 合約滅菌服務供應商

- 研究機構和學術機構

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Andersen Sterilizers

- Anpro

- Crosstex International, Inc.

- Ecolab

- Getinge AB

- GKE

- Inkmaker SRL

- LA-CO Industries

- McKesson Medical-Surgical Inc.

- Mesa Labs, Inc.

- NiGK Corporation

- PMS Healthcare Technologies

- Propper Manufacturing

- Raven Biological Laboratories

- STERIS

- Terragene

第7章 市場機會與未來展望

According to Mordor Intelligence, the chemical indicator inks market size was valued at USD 83.15 million in 2025 and is estimated to grow from USD 89.74 million in 2026 to reach USD 131.44 million by 2031, at a CAGR of 7.93% during the forecast period (2026-2031).

This report is Segmented by Type (Water-Based Indicator Inks and More), Process Type (Steam Sterilization Indicators and More), Application (Packaging, Labels and Tags, and More), End-User Industry (Hospitals and Clinics and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Chemical Indicator Inks Market Trends and Insights

Increased Awareness About Infection-Control Regulations

Regulators now recommend the use of multi-parameter Type 4 indicators instead of single-parameter strips, addressing a compliance gap. In March 2025, the U.S. Food and Drug Administration (FDA) recognition of ANSI/AAMI ST58:2024 requires U.S. hospitals to document each sterilization cycle with a traceable chemical indicator that verifies time, temperature, and sterilant concentration. Updates from the Joint Commission in July 2024 and July 2025 incorporate these requirements into accreditation audits, necessitating product upgrades. Canada's GUI-0074 and Europe's EN 556-1:2024 align regional regulations with ISO 11140, expanding the number of compliant facilities. These regulatory changes drive the growth of the chemical indicator inks market by making advanced chromogenic systems a necessary business investment.

Rising Surgical and Outpatient Procedure Volumes

Ambulatory and robotic-assisted surgeries are growing faster than inpatient procedures, driving the need for low-temperature sterilizers that cannot rely solely on steam indicators. In 2025, Intuitive Surgical reported approximately 3.15 million da Vinci procedures, reflecting an 18% year-over-year increase, with expectations of double-digit growth in 2026. The United States Centers for Medicare and Medicaid Services (CMS) introduced 573 new outpatient codes for 2026, distributing sterilization workloads across numerous smaller centers that often lack centralized sterile-processing departments. Each new site is required to stock validated indicators, ensuring consistent demand for suppliers and increasing the market potential for chemical indicator inks.

Limited Market Awareness in Low-Income Regions

Surgical-site infection rates in sub-Saharan Africa are 11.8%, compared to 1.9% in high-income countries. Many medical facilities in these regions, constrained by financial limitations, rely on basic Class 1 strips that monitor only a single variable instead of using multi-parameter indicators. Donor programs often fund sterilizers but exclude consumables, leaving technicians without the necessary tools to validate sterilization cycles. Additionally, a significant portion of staff lacks formal training in interpreting International Organization for Standardization (ISO)-compliant indicators. Without the inclusion of chemical-indicator funding in procurement guidelines by multilateral agencies, the adoption of these indicators is expected to remain inconsistent. This inconsistency could impact the growth potential of the chemical indicator inks market in these regions.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Validation Norms in Pharma and Med-Device Manufacturing

- RFID-Integrated Smart Indicator Labels for Asset Tracking

- Volatile Supply of Specialty Chromogenic Pigments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, water-based formulations accounted for 47.12% of the type segment, reflecting their compatibility with modern presses and compliance with volatile organic compound (VOC) limits outlined in China's 14th Five-Year Plan. As hospitals and medical device companies increasingly align their purchases with corporate net-zero objectives, the market for water-based chemical indicator inks is expected to grow steadily. Suppliers such as Fujifilm, with its AQUAFUZE hybrid water-based ultraviolet (UV) line, and Sun Chemical, with its bio-renewable SunCure Advance ECO, are improving performance while reducing carbon footprints.

Among the type segments, UV-curable systems are growing at a compound annual growth rate (CAGR) of 8.36%, the fastest in the market. This growth is driven by instant curing technology, which reduces energy costs by up to 60% and increases throughput for contract sterilizers handling high-volume labels. The industry is seeing increased adoption, with companies like Mimaki introducing Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH)-compliant ELH inks and StarColor offering low-migration flexographic (flexo) sets, both gaining traction in pharmaceutical packaging. Additionally, suppliers proficient in developing dual-indicator chemistries, combining sterilization proof with cold-chain time-temperature response, can access premium market segments and support the growth of the chemical indicator inks market.

In 2025, steam indicators accounted for 36.98% of the process-type revenue, primarily driven by the extensive use of hospital autoclaves worldwide. The updated ANSI (American National Standards Institute)/AAMI (Association for the Advancement of Medical Instrumentation) ST58:2024 standard requires Type 4 internal monitors, leading to increased replacement sales and supporting steam's market share.

Plasma and vaporized hydrogen peroxide indicators are projected to grow at a CAGR (Compound Annual Growth Rate) of 8.14%. This growth is attributed to advancements in robotics, the adoption of heat-sensitive implants, and the FDA's (Food and Drug Administration) 2024 Category A reclassification, which simplified validation processes. Getinge's Poladus 150 bundle and Mesa Labs' ExpoSure kits illustrate equipment-consumable ecosystems designed to retain customers through proprietary inks, contributing to the chemical indicator inks market share held by leading technology providers.

Geography Analysis

In 2025, North America accounted for 37.88% of the revenue. The adoption of ANSI/AAMI ST58:2024 (American National Standards Institute/Association for the Advancement of Medical Instrumentation) by hospitals in the United States, along with significant capital expenditures in the pharmaceutical industry, supported demand. Additionally, the Centers for Medicare & Medicaid Services (CMS) expanded reimbursement for outpatient procedures, increasing the customer base. RFID (Radio-Frequency Identification) trials are progressing from university hospitals to major Integrated Delivery Networks (IDNs), enhancing the market presence of chemical indicator inks.

Europe follows, driven by EU MDR (European Union Medical Device Regulation) audits, the harmonization of EN 556:2024, and the implementation of a 12% Carbon Border Adjustment tariff, which supports water-based and UV (ultraviolet) sets. Rising pigment costs due to duties on titanium dioxide (TiO2) are prompting converters to pursue long-term supply agreements or backward integration, reshaping the competitive landscape.

Asia-Pacific is the fastest-growing region, with an 8.32% CAGR (Compound Annual Growth Rate) projected through 2031. India's plan to add 2 million hospital beds by 2030 and China's 30% reduction mandate on volatile organic compounds (VOCs) are driving both volume growth and technology shifts. Private-equity investments in Asian Contract Development and Manufacturing Organizations (CDMOs) and hospitals are further increasing demand for validated indicators, accelerating the market expansion for chemical indicator inks.

- 3M

- Andersen Sterilizers

- Anpro

- Crosstex International, Inc.

- Ecolab

- Getinge AB

- GKE

- Inkmaker SRL

- LA-CO Industries

- McKesson Medical-Surgical Inc.

- Mesa Labs, Inc.

- NiGK Corporation

- PMS Healthcare Technologies

- Propper Manufacturing

- Raven Biological Laboratories

- STERIS

- Terragene

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased awareness about infection-control regulations

- 4.2.2 Rising surgical and outpatient procedure volumes

- 4.2.3 Stricter validation norms in pharma and med-device manufacturing

- 4.2.4 RFID-integrated smart indicator labels for asset tracking

- 4.2.5 Rapid adoption of on-pack smart inks for cold-chain biologics

- 4.3 Market Restraints

- 4.3.1 Limited market awareness in low-income regions

- 4.3.2 Volatile supply of specialty chromogenic pigments

- 4.3.3 Sustainability pressure on solvent-based ink carriers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Water-Based Indicator Inks

- 5.1.2 Solvent-Based Indicator Inks

- 5.1.3 UV-Curable Indicator Inks

- 5.1.4 Hybrid / Dual-Indicator Systems

- 5.2 By Process Type

- 5.2.1 Steam Sterilization Indicators

- 5.2.2 Ethylene Oxide (EO) Sterilization Indicators

- 5.2.3 Dry-Heat Sterilization Indicators

- 5.2.4 Plasma / H2O2 Gas Sterilization Indicators

- 5.2.5 Radiation (Gamma / E-Beam) Indicators

- 5.2.6 Formaldehyde Sterilization Indicators

- 5.3 By Application

- 5.3.1 Packaging (Bags, Wraps, Tapes)

- 5.3.2 Labels and Tags

- 5.3.3 Test Strips and Pouches

- 5.4 By End-user Industry

- 5.4.1 Hospitals and Clinics

- 5.4.2 Pharmaceutical and Medical-Device Firms

- 5.4.3 Diagnostic Laboratories

- 5.4.4 Contract Sterilization Service Providers

- 5.4.5 Research Institutes and Academia

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Andersen Sterilizers

- 6.4.3 Anpro

- 6.4.4 Crosstex International, Inc.

- 6.4.5 Ecolab

- 6.4.6 Getinge AB

- 6.4.7 GKE

- 6.4.8 Inkmaker SRL

- 6.4.9 LA-CO Industries

- 6.4.10 McKesson Medical-Surgical Inc.

- 6.4.11 Mesa Labs, Inc.

- 6.4.12 NiGK Corporation

- 6.4.13 PMS Healthcare Technologies

- 6.4.14 Propper Manufacturing

- 6.4.15 Raven Biological Laboratories

- 6.4.16 STERIS

- 6.4.17 Terragene

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

UV膠印油墨市場規模、佔有率和成長分析:按類型、應用、承印物、最終用途、通路和地區分類-2026-2033年產業預測

UV膠印油墨市場規模、佔有率和成長分析:按類型、應用、承印物、最終用途、通路和地區分類-2026-2033年產業預測 印刷油墨催化劑市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年

印刷油墨催化劑市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年 油墨市場報告:按技術、油墨類型、應用和地區分類(2026-2034 年)

油墨市場報告:按技術、油墨類型、應用和地區分類(2026-2034 年) 化學指示劑油墨市場:按類型、應用、終端用戶產業和地區分類

化學指示劑油墨市場:按類型、應用、終端用戶產業和地區分類 2026年全球溶劑型裝飾墨水市場報告

2026年全球溶劑型裝飾墨水市場報告 化學指示劑油墨市場:2026-2032年全球市場預測(按技術、形態、分銷管道、應用和最終用途行業分類)裝飾油墨市場:依油墨類型、技術、應用、終端用戶產業和銷售管道-全球預測,2026-2032年功能性油墨市場:依功能化學、印刷技術、固化機制、配方及應用分類,全球預測(2026-2032)高生物基含量UV油墨市場:按類型、技術、基材、應用、終端用戶產業和分銷管道分類,全球預測(2026-2032年)

化學指示劑油墨市場:2026-2032年全球市場預測(按技術、形態、分銷管道、應用和最終用途行業分類)裝飾油墨市場:依油墨類型、技術、應用、終端用戶產業和銷售管道-全球預測,2026-2032年功能性油墨市場:依功能化學、印刷技術、固化機制、配方及應用分類,全球預測(2026-2032)高生物基含量UV油墨市場:按類型、技術、基材、應用、終端用戶產業和分銷管道分類,全球預測(2026-2032年) 全球食用墨水及相關配件市場規模、佔有率、趨勢及成長分析報告(2026-2034年)

全球食用墨水及相關配件市場規模、佔有率、趨勢及成長分析報告(2026-2034年)