|

市場調查報告書

商品編碼

2062153

羰基鐵粉:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Carbonyl Iron Powder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

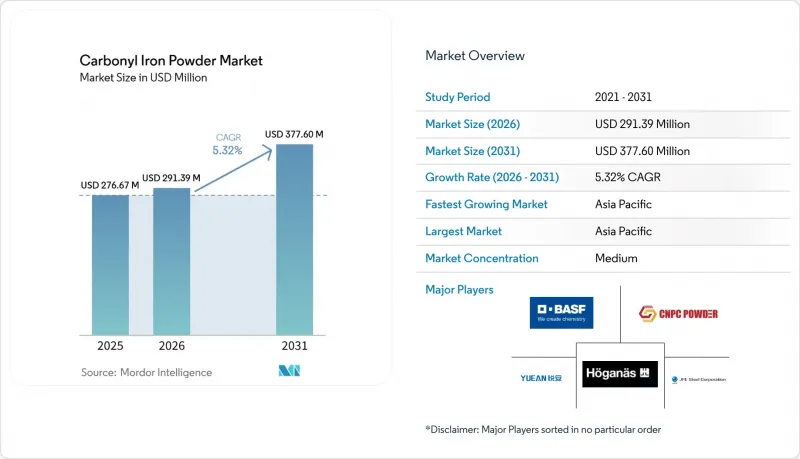

根據 Mordor Intelligence 預測,羰基鐵粉市場規模將從 2025 年的 2.7667 億美元和 2026 年的 2.9139 億美元成長到 2031 年的 3.776 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 5.3%。

本報告按類型(還原羰基鐵粉和噴霧乾燥羰基鐵粉)、純度等級(標準鐵97%或更高,其他)、終端用戶行業(電子、汽車、醫療/製藥,其他)和地區(亞太、北美、歐洲,其他)進行細分。市場預測以美元計價。

全球羰基鐵粉市場趨勢及洞察

擴大粉末冶金技術在輕量化電動車傳動系統零件的應用。

電動車製造商正擴大採用粉末冶金工藝製造的零件,例如齒輪、凸輪和支架。這些零件有助於將傳動系統的質量降低 15% 至 20%,同時保持 500 MPa 以上的疲勞強度。每減輕 1 公斤重量,續航里程就能增加 15 至 20 公里。 Porite 的一項案例研究表明,與機械加工鋼材相比,粉末冶金零件的成本降低了 20% 至 30%。同樣,Sterling Sintered Technologies 的報告顯示,使用羰基鐵粉的軟磁複合材料可將鐵芯損耗降低 20%,馬達尺寸縮小 30%。電動車對輕量化和高效零件日益成長的需求正在推動粉末冶金解決方案的普及。羰基鐵粉因其球形形態和高燒結性,在高性能應用領域備受關注。能夠客製化 1-5 微米範圍內的粒徑,並提供預絕緣等級以最大限度減少渦流損耗的供應商,更有可能提供更高的價格。另一方面,缺乏這些能力的生產商可能會面臨利潤率壓力,因為汽車製造商會利用採購量作為籌碼來談判降低價格。

金屬射出成型技術在小型醫療設備中的廣泛應用

2024年,用於醫療和牙科領域的金屬射出成型(MIM)銷售額預計在5.78億美元至18.8億美元之間,複合年成長率約為9%。羰基鐵粉的優點在於其球形粒徑,可達到60%的體積固態含量,燒結後密度可超過理論密度的95%。為符合美國藥典(USP)及美國材料與試驗協會(ASTM)B883-10標準,其氧含量限制在0.2%以內,有助於降低體液環境中的孔隙率。隨著美國食品藥物管理局(FDA)21 CFR 820文件要求的日益嚴格,未能合規的供應商可能會被排除在高利潤合約之外。金屬射出成型能夠實現0.05毫米或更小的公差以及優於1.6微米的表面光潔度,是製造矯正托架和植入式外殼的關鍵技術。

職場吸入奈米顆粒的法律責任

儘管一項系統性回顧未能發現氧化鐵與疾病之間存在明確的關聯,但監管機構仍將職場氧化鐵的暴露限值設定為10毫克/立方公尺。他們現在強制要求在2027年7月前進行即時粉塵和健康監測。加強合規措施,包括安裝高效能空氣濾清器(HEPA過濾器)、季度審核和健康追蹤,導致每條生產線每年額外增加5萬至15萬美元的成本。成本的增加導致保險公司將保費提高了15%至25%。雖然大型綜合製造商能夠應對這些成本,但小型加工商正面臨可能導致退出市場的財務壓力。這一趨勢正逐步推動羰基鐵粉市場走向整合。

細分市場分析

至2025年,低品級產品、醫藥添加劑和金屬射出成型醫療器材零件(氧含量≤0.2%,粒徑1-10微米)將佔低品級羰基鐵粉市場67.11%的佔有率。生產需要壓力超過20兆帕的運作釜,循環時間超過120小時,鐵純度超過99.5%。這些特性確保了足夠的原料強度和超過理論標準95%的緻密度,滿足醫療保健和營養保健品應用的需求,且價格相對穩定。

在8 MPa反應器中經過60小時霧化製備的羰基鐵粉預計將以5.88%的複合年成長率成長。這一成長主要歸功於其更窄的D50粒徑分佈(3-8微米),從而降低了軟磁複合材料(尤其是工作頻率為50-100 kHz的逆變器線圈)中的渦流損耗。亞太地區汽車計畫中800V電動汽車平台和碳化矽逆變器的日益普及推動了這個細分市場的成長。提供預絕緣霧化級產品的供應商在高頻電感器市場佔據了重要地位,在該市場中,鐵芯損耗降低1%可轉化為充電時間縮短0.5%。此外,能夠同時進行高壓霧化和中壓霧化的雙線生產商能夠更好地滿足羰基鐵粉市場的多樣化需求,同時保持利潤率。

區域分析

預計到2025年,亞太地區將佔全球銷售額的42.27%,到2031年複合年成長率將達到6.31%。這項成長主要得益於中國市場的強勁表現,中國佔全球產能的45%以上,2023年需求量超過8,000噸。 2025年第一季,中國生產商宣布投產一條新的12,000噸生產線,以滿足東南亞和北美客戶的需求。印度進口成本高出20-30%,預計2025年進口量將達到1200-1500噸,這表明需要建立區域分銷中心。

在北美,航太、國防和製藥業是需求的主要驅動力,而ASTM和USP可追溯性至關重要。美國羰基公司位於阿拉巴馬州的工廠在國內供應中發揮關鍵作用。此外,Höganass公司的生物炭替代舉措預計到2026年將二氧化碳排放強度降低15%,符合原始設備製造商(OEM)的範圍3目標。在歐洲,BASF位於路德維希港的工廠在2023年將產能提高了800噸,並開始對亞微米級產品採用更嚴格的分類標準。然而,2024/1785號指令的實施增加了合規成本,導致規模較小的加工商考慮業務整合或搬遷。

南美和中東/非洲地區仍然嚴重依賴進口,面臨8-12週前置作業時間的挑戰。建立擁有500-1000噸庫存的保稅倉庫和技術服務中心,預計將帶來10-15%的價格溢價。鑑於跨國買家正根據歐盟和美國標準對供應商進行審核,這種做法尤其重要。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電磁干擾屏蔽應用的需求不斷成長

- 粉末冶金技術的擴展及其在汽車零件中的應用

- 金屬射出成型上的應用

- 擴大製藥用鐵補充劑的生產

- 新興的3D列印電磁波吸收結構

- 市場限制因素

- 羰基鐵原料生產成本高且供應不穩定。

- 吸入奈米顆粒帶來的健康與環境風險

- 廉價的噴霧乾燥鐵粉作為替代品的威脅。

- 價值鏈分析

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- 還原羰基鐵粉

- 噴霧乾燥羰基鐵粉

- 按純度等級

- 標準(鐵含量97%或以上)

- 高純度(鐵含量99%或以上)

- 超高純度(鐵含量99.9%或更高)

- 按最終用戶行業分類

- 電子與電機工程

- 車

- 醫療和製藥

- 航太/國防

- 工業機械

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Americal Carbonyl

- BASF

- CNPC Powder

- CRS Holdings, LLC.

- Hoganas AB

- JFE Steel Corporation

- Jiangsu Tianyi Ultra-fine Metal Powder

- Jiangxi Yuean Advanced Materials Co Ltd

- KPT

- Micrometals Inc.

- MUBY Chemicals

- Nanorh

- Rio Tinto

- Shanghai Knowhow Powder-Tech Co.,Ltd

- Sintez-CIP Ltd

- Stanford Advanced Materials

第7章 市場機會與未來展望

According to Mordor Intelligence, the carbonyl iron powder market size is projected to expand from USD 276.67 million in 2025 and USD 291.39 million in 2026 to USD 377.60 million by 2031, registering a CAGR of 5.32% between 2026 to 2031.

This report is Segmented by Type (Reduced Carbonyl Iron Powder and Atomized Carbonyl Iron Powder), Purity Grade (Standard More Than or Equal To 97% Fe, and More), End-User Industry (Electronics and Electricals, Automotive, Healthcare and Pharmaceuticals, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Carbonyl Iron Powder Market Trends and Insights

Surge in Powder-Metallurgy Use for Lightweight Electric Vehicle Drivetrain Parts

Electric-vehicle manufacturers are increasingly adopting powder-metallurgy components such as gears, cams, and brackets. These components help reduce drivetrain mass by 15% to 20% while maintaining fatigue strength above 500 MPa. This reduction contributes to an additional range of 15 to 20 km for every kilogram saved. A case study from Porite indicated a 20% to 30% cost reduction compared to machined steel. Similarly, Sterling Sintered Technologies reported that soft magnetic composites made with carbonyl iron powder reduced core losses by 20% and decreased motor sizes by 30%. The growing demand for lightweight and efficient components in electric vehicles is driving the adoption of powder-metallurgy solutions. Carbonyl iron powder is gaining attention in high-performance applications due to its spherical morphology and high sinterability. Suppliers capable of customizing particle sizes within the 1 to 5 micron range and providing pre-insulated grades to minimize eddy-current losses are positioned to achieve higher pricing. On the other hand, producers without these capabilities may face pressure on margins as automakers leverage their purchasing volumes to negotiate lower prices.

Uptake of Metal-Injection Molding for Miniaturized Medical Devices

In 2024, the revenue from medical and dental metal-injection molding (MIM) ranged between USD 578 million and USD 1.88 billion, with a growth rate of nearly 9% CAGR. The preference for carbonyl iron powder is driven by its spherical particles, which enable a 60 vol% solids loading and achieve densities exceeding 95% of theoretical post-sintering. To meet USP and ASTM B883-10 standards, oxygen content is limited to 0.2%, which helps reduce porosity in body-fluid environments. Suppliers that fail to comply may face exclusion from high-margin contracts, as FDA 21 CFR 820 documentation requirements become stricter. Metal-injection molding, capable of achieving tolerances below 0.05 mm and surface finishes finer than 1.6 µm, is essential for manufacturing orthodontic brackets and implantable housings.

Occupational Nanoparticle Inhalation Liabilities

Regulators, despite a systematic review finding no consistent disease link, have capped workplace iron-oxide exposure at 10 mg m-3. They now require real-time dust monitoring and medical surveillance by July 2027. Compliance upgrades, such as HEPA filtration, quarterly audits, and health tracking, increase costs by USD 50,000 to 150,000 annually per line. This rise in costs has prompted insurers to adjust premiums by 15% to 25%. While large integrated producers are managing these costs, smaller converters are experiencing financial pressure, which could lead to their exit from the market. This development is gradually driving the carbonyl iron powder market toward increased consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Iron-Fortified Micro-Encapsulated Nutraceuticals

- Localized Radar-Absorbing Composites for Autonomous-Vehicle Sensors

- Substitution Threat from Cheaper Water-Atomized Iron Powders

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, reduced grades, pharmaceutical supplements and metal-injection-molding medical parts, requiring oxygen levels of <0.2% and particle sizes between 1-10 µm, accounted for 67.11% of the carbonyl iron powder market under the reduced grades segment. Production depends on reactors operating at ≥ 20 MPa for cycles exceeding 120 hours, achieving iron purity levels above 99.5%. These characteristics ensure adequate green strength and densification surpassing 95% of theoretical standards, meeting the needs of healthcare and nutraceutical applications with relatively stable price sensitivity.

Atomized carbonyl iron powder, produced in 8 MPa reactors over a span of 60 hours, is projected to grow at a 5.88% CAGR. This growth is driven by its tighter D50 distributions of 3-8 µm, which help reduce eddy-current losses in soft magnetic composites, particularly for 50-100 kHz inverter coils. The segment is supported by the increasing adoption of 800-V EV platforms and silicon-carbide inverters in Asia-Pacific's vehicle programs. Suppliers offering pre-insulated atomized grades are gaining traction in high-frequency inductors, where a 1% reduction in core loss results in a 0.5% decrease in charging time. Additionally, dual-line producers capable of both high-pressure reduced and mid-pressure atomized outputs are positioned to maintain margins while addressing the varied demands of the carbonyl iron powder market.

Geography Analysis

In 2025, Asia-Pacific represented 42.27% of the revenue, with a projected 6.31% CAGR through 2031. This growth is supported by China's significant role, holding over 45% of global capacity and a demand exceeding 8,000 tons in 2023. In the first quarter of 2025, Chinese producers announced 12,000 tons of new production lines to cater to customers in Southeast Asia and North America. India, dealing with a 20%-30% premium on landed costs, imported between 1,200 and 1,500 tons in 2025, indicating the need for regional distribution hubs.

In North America, the aerospace, defense, and pharmaceutical sectors drive demand, with a focus on ASTM and USP traceability. American Carbonyl's plant in Alabama plays a key role in the domestic supply. Additionally, Hoganas' biochar substitution initiative is expected to reduce CO2 intensity by 15% by 2026, aligning with OEM Scope 3 targets. In Europe, BASF's site in Ludwigshafen increased capacity by 800 tons in 2023 and is now applying stricter classifications for sub-µm grades. However, Directive 2024/1785 is raising compliance costs, prompting smaller converters to consider consolidation or relocation.

South America and the Middle East & Africa remain fully dependent on imports, facing challenges with lead times of 8 to 12 weeks. Establishing bonded regional warehouses with 500 to 1,000 tons of stock and technical-service centers could enable price premiums of 10% to 15%. This approach is particularly relevant as multinational buyers implement supplier audits aligned with EU and U.S. standards.

- Americal Carbonyl

- BASF

- CNPC Powder

- CRS Holdings, LLC.

- Hoganas AB

- JFE Steel Corporation

- Jiangsu Tianyi Ultra-fine Metal Powder

- Jiangxi Yuean Advanced Materials Co Ltd

- KPT

- Micrometals Inc.

- MUBY Chemicals

- Nanorh

- Rio Tinto

- Shanghai Knowhow Powder-Tech Co.,Ltd

- Sintez-CIP Ltd

- Stanford Advanced Materials

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand in EMI-Shielding Applications

- 4.2.2 Increasing Use in Powder Metallurgy and Automotive Components

- 4.2.3 Adoption in Metal Injection-Molding (MIM) for Complex Parts

- 4.2.4 Expansion of Pharmaceutical Iron-Supplement Production

- 4.2.5 Emerging 3-D-Printed EM-Absorber Structures

- 4.3 Market Restraints

- 4.3.1 High Production Cost and Volatile Iron-Carbonyl Feedstock Supply

- 4.3.2 Health and Environmental Risks from Nano-Particle Inhalation

- 4.3.3 Substitution Threat from Cheaper Atomized Iron Powders

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Reduced Carbonyl Iron Powder

- 5.1.2 Atomized Carbonyl Iron Powder

- 5.2 By Purity Grade

- 5.2.1 Standard (more than or equal to 97% Fe)

- 5.2.2 High-Purity (more than or equal to 99% Fe)

- 5.2.3 Ultra-High-Purity (more than or equal to 99.9% Fe)

- 5.3 By End-user Industry

- 5.3.1 Electronics and Electricals

- 5.3.2 Automotive

- 5.3.3 Healthcare and Pharmaceuticals

- 5.3.4 Aerospace and Defense

- 5.3.5 Industrial Machinery

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Americal Carbonyl

- 6.4.2 BASF

- 6.4.3 CNPC Powder

- 6.4.4 CRS Holdings, LLC.

- 6.4.5 Hoganas AB

- 6.4.6 JFE Steel Corporation

- 6.4.7 Jiangsu Tianyi Ultra-fine Metal Powder

- 6.4.8 Jiangxi Yuean Advanced Materials Co Ltd

- 6.4.9 KPT

- 6.4.10 Micrometals Inc.

- 6.4.11 MUBY Chemicals

- 6.4.12 Nanorh

- 6.4.13 Rio Tinto

- 6.4.14 Shanghai Knowhow Powder-Tech Co.,Ltd

- 6.4.15 Sintez-CIP Ltd

- 6.4.16 Stanford Advanced Materials

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

羰基鐵市場 - 全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、地區和競爭格局,2021-2031年

羰基鐵市場 - 全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、地區和競爭格局,2021-2031年 鐵粉市場預測至2034年—按類型、等級、應用、最終用戶和地區分類的全球分析

鐵粉市場預測至2034年—按類型、等級、應用、最終用戶和地區分類的全球分析 食品級鐵粉市場:按類型、粒徑、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測

食品級鐵粉市場:按類型、粒徑、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測 全球羰基鐵粉市場規模、佔有率、趨勢和成長分析報告(2026-2034年)3D列印用鐵粉市場:按類型、列印技術、粉末形態、終端用戶產業和粒徑範圍分類 - 全球預測(2026-2032年)用於 3D 列印的鐵基金屬粉末市場:按類型、製造技術、形狀、最終用途行業和配銷通路分類 - 全球預測 2026-2032 年鋼粉市場按製造技術、合金成分、粉末形態和應用分類-全球預測(2026-2032 年)全球鐵粉市場:市場規模、佔有率、成長率、產業分析、按類型、應用和地區劃分的考量及未來預測(2026-2034)

全球羰基鐵粉市場規模、佔有率、趨勢和成長分析報告(2026-2034年)3D列印用鐵粉市場:按類型、列印技術、粉末形態、終端用戶產業和粒徑範圍分類 - 全球預測(2026-2032年)用於 3D 列印的鐵基金屬粉末市場:按類型、製造技術、形狀、最終用途行業和配銷通路分類 - 全球預測 2026-2032 年鋼粉市場按製造技術、合金成分、粉末形態和應用分類-全球預測(2026-2032 年)全球鐵粉市場:市場規模、佔有率、成長率、產業分析、按類型、應用和地區劃分的考量及未來預測(2026-2034) 鐵粉市場規模、佔有率和趨勢分析報告:按類型、最終用途、地區和細分市場預測(2025-2033 年)

鐵粉市場規模、佔有率和趨勢分析報告:按類型、最終用途、地區和細分市場預測(2025-2033 年) 羰基氟化物:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

羰基氟化物:全球市場佔有率和排名、總收入和需求預測(2025-2031年)