|

市場調查報告書

商品編碼

2062148

塑膠擠出機:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Plastic Extrusion Machine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

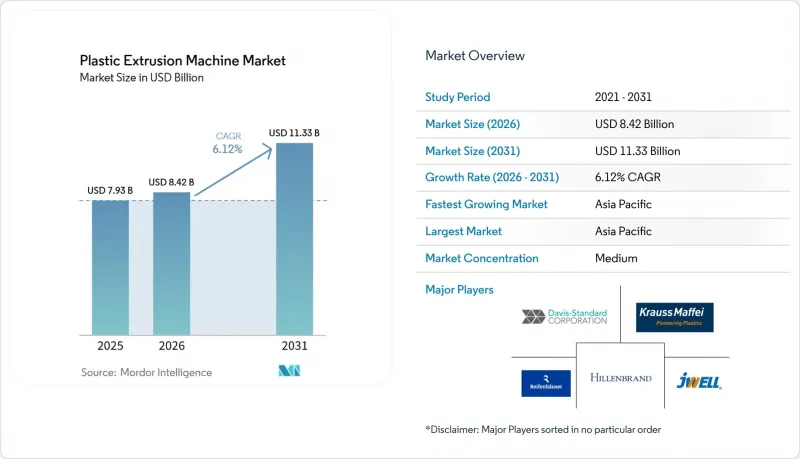

根據 Mordor Intelligence 預測,塑膠擠出機市場規模預計將在 2025 年達到 79.3 億美元,2026 年達到 84.2 億美元,到 2031 年達到 113.3 億美元,2026 年至 2031 年的複合年成長率為 6.12%。

本報告按機器類型(單螺桿擠出機、雙螺桿擠出機等)、工藝類型(吹膜加工擠出機、片材/薄膜擠出機等)、自動化程度(半自動、傳統手動/繼電器、全自動 SCADA/IoT 系統)、終端用戶行業(包裝、建築等)和地區(亞太地區、北美等)進行分類。

全球塑膠擠出機市場趨勢與洞察

自動化和節能機械技術的進步

集中式控制平台,例如 Bausano 的 ORQUESTRA 4.0,可在運作中收集即時資料並規劃維護工作。這種方法可減少意外停機時間,並幫助轉換器即使在歐洲電價上漲的情況下也能保持獲利能力。 2026 年,SML 在其流延薄膜生產線中實施了雙螺桿系統,使單位面積能耗降低了 10-15%,凝膠生成量降低了 20%。這項進展凸顯了對能源效率和品質改進日益成長的關注。 Coperion 的 C-Beyond 生命週期管理套件可監控齒輪箱振動並提供警報以防止關鍵故障。此功能有助於延長設備壽命,並應對熟練技術人員退休帶來的挑戰。德國和美國在早期採用自動化方面處於領先地位,降低整體擁有成本 (TCO) 是推動自動化成為採購決策關鍵因素的重要因素。

對再生和可生物分解聚合物擠出成型的需求日益成長

歐盟包裝和包裝廢棄物法規要求在2030年至2040年間,包裝材料中再生材料的含量必須達到30%至65%,這促使生產線進行大規模改造,以使用雙螺桿限流進料系統處理粉塵狀的片狀材料。科倍隆的STS 35 Mc 11型擠出機憑藉其自清潔、嚙合螺桿和可控熔體溫度,將受污染再生材料的處理能力提高了27%。加州要求所有包裝材料在2032年前必須可回收或可堆肥,這推動了人們對生物基PLA擠出生產線的興趣。製造商們正透過引入耐磨螺桿、更嚴格的停留時間控制和低剪切熔體區來保護再生聚合物的質量,從而重塑整個塑膠擠出機市場的價值提案。

關於使用原生塑膠的環境法規

加拿大禁止使用一次性塑膠製品以及加州SB 54法案迫使零售商和餐廳從使用原生材料轉向使用再生和可堆肥材料。這種合規性提高了對食品級rPET的需求,但價格也比原生材料高出25%。此外,加工商也面臨在緊迫期限內檢驗新配方的挑戰。在歐洲,2030年強制回收將限制不易分層的多層複合材料的使用。由於品牌所有者越來越傾向於選擇提供可追溯再生材料的供應商,無法改造生產線的加工商將面臨失去合約的風險。

細分市場分析

預計到2031年,雙螺桿擠出機的成長速度將超過整體塑膠擠出機市場,複合年成長率(CAGR)將達到6.21%。儘管到2025年單螺桿擠出機將佔據塑膠擠出機市場53.11%的佔有率,但這種成長趨勢在各個地區都有體現。目前,用於塑膠擠出的實驗性雙螺桿系統的市場規模相對較小,但以驚人的速度擴張。這一趨勢歸因於各地加工商在擴大生產規模之前,使用回收材料和生物基複合材料運作測試批量生產。

模組化螺桿元件使操作人員能夠調節混合、輸送和分流部分,從而在添加量僅為0.1%時提高顏料分散性,並有助於防止吸濕性聚合物的熱劣化。雖然隨著螺桿直徑的增加,資本投資也會增加,但由於處理能力與直徑的平方成正比,因此在大批量生產工廠中,每公斤成本反而會降低。由於維護要求相對簡單,單螺桿機在管材和型材領域仍佔據主導地位。然而,在一些地區,加工商對高回收材料配方進行認證,而這些配方只能由雙螺桿機可靠地加工,因此單螺桿機的市場佔有率正在逐漸下降。

預計到2025年,吹膜加工將佔銷售佔有率的32.24%。然而,擠壓塗布和複合薄膜預計將以6.42%的複合年成長率成長,反映出品牌所有者對單一材料阻隔結構的偏好日益增強。隨著食品品牌從混合複合包裝袋轉向符合即將實施的A級可回收標籤的全PE替代品,塑膠擠出機市場,尤其是9至11層塗層生產線,正在不斷擴張。

能源審計顯示,共擠出製程每平方公尺的能耗低於2.6千瓦時,約為溶劑型複合材料生產能耗的一半。這使得加工商能夠降低能源成本以及與溶劑排放相關的合規成本。在印度和東協地區,管道、管材和型材生產線仍在滿足基礎設施需求,但投資正逐步轉向阻隔膜生產線。這些生產線旨在滿足需要延長產品保存期限的合約要求,例如新鮮肉類和即食食品。

區域分析

到2025年,亞太地區將佔全球整體銷售額的48.22%,預計到2031年將維持6.88%的複合年成長率,這主要得益於中國、印度和東南亞國協產能的擴張。泰國擁有3,200家轉換器和3,460萬噸的石化產品產能,其回收方面仍有提升空間。如果政策制定者設定更嚴格的循環經濟目標,則有望帶來更多成長機會。

在北美,尤其由於加州SB 54法案和加拿大更嚴格的法規,現有設施的維修比新建設施更受重視。然而,機械回收率低意味著需要依賴從歐洲進口經認證的rPET,這持續推動對雙螺桿回收生產線的投資。墨西哥正在吸引近岸外包投資,尤其是在電動車線材和食品接觸膜領域,並根據美墨加協定促進向美國原始設備製造商的跨境供應。

在歐洲,該行業受到最嚴格的監管。 PPWR(聚丙烯薄膜)對再生材料含量和可回收等級的重視,促使加工商採用具備線上品質分析功能的先進的5層至11層共擠出機。德國和義大利在自動化應用方面處於領先地位,而東歐和北歐國家正在試驗化學回收材料的製備,這需要高真空脫揮發性擠出機。南美和中東的成長情況各不相同。儘管外匯波動,巴西仍在繼續投資青貯薄膜生產線,而沙烏地阿拉伯正在提高HDPE(高密度聚乙烯)管道的產能,以滿足供水基礎設施的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 自動化和節能機械技術的進步

- 對可回收和可生物分解聚合物擠出的需求不斷成長

- 政府對循環經濟設備的誘因

- 人工智慧驅動的預測過程控制實現零缺陷生產

- 用於個人化醫療植入的現場微擠出

- 市場限制因素

- 關於使用原生塑膠的環境法規

- 高扭力變速箱供應商短缺導致前置作業時間延長。

- 人口結構變化導致熟練操作人員短缺

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按機器類型

- 單螺桿擠出

- 雙螺桿擠出

- 多螺絲和特殊配置

- 下游輔助設施

- 透過流程

- 膨脹成型

- 片材和薄膜擠出

- 管材和型材擠壓

- 管材擠出

- 擠壓塗布和層壓

- 其他工藝類型

- 按自動化級別

- 半自動(PLC整合)

- 傳統型(手動/繼電器型)

- 全自動(相容於SCADA/IoT)

- 按最終用戶行業分類

- 包裝

- 建築/施工

- 汽車和運輸業

- 電氣和電子設備

- 消費品和家用電器

- 醫療保健

- 農業

- 其他終端用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Bausano SpA, societa unipersonale

- BREYER Maschinenfabrik GmbH

- Coperion GmbH

- Costruzioni Meccaniche Luigi Bandera SpA

- Cowell(Nanjing)Extrusion Machinery Co., Ltd.

- Davis-Standard, LLC

- Hillenbrand

- JianTai

- JWELL Extrusion Machinery Co., Ltd.

- Kolsite Group(Rajoo Engineers)

- KraussMaffei

- KUNG HSING PLASTIC MACHINERY CO., LTD.

- Leistritz Extrusionstechnik GmbH

- Nanjing KY Chemical Machinery

- Qingdao Shansu Extrusion Equipment Co.,ltd

- Reifenhauser Group

- SML Maschinengesellschaft mbH

- The Japan Steel Works Ltd.

- Windsor Machines Pvt. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the plastic extrusion machine market size is projected to be USD 7.93 billion in 2025, USD 8.42 billion in 2026, and reach USD 11.33 billion by 2031, growing at a CAGR of 6.12% from 2026 to 2031.

This report is Segmented by Machine Type (Single Screw Extrusion, Twin Screw Extrusion, and More), Process Type (Blown Film Extrusion, Sheet/Film Extrusion, and More), Automation Level (Semi-Automated, Conventional Manual/Relay-based, and Fully-Automated SCADA/IoT-enabled), End-User Industry (Packaging, Building and Construction, and More), and Geography (Asia-Pacific, North America, and More).

Global Plastic Extrusion Machine Market Trends and Insights

Advancements in Automation and Energy-Efficient Machinery

Centralized control platforms, such as Bausano's ORQUESTRA 4.0, collect live operating data and organize maintenance events. This approach reduces unscheduled downtime, helping converters manage margins amid rising power prices in Europe. In 2026, SML introduced a twin-screw system that achieved a 10-15% reduction in specific energy input and a 20% decrease in gels on cast-film lines. This development highlights the growing focus on energy efficiency and quality improvements. Coperion's C-Beyond lifecycle suite monitors gearbox vibrations and provides alerts to prevent catastrophic failures. This feature supports asset-life extensions, addressing challenges posed by the retirement of skilled technicians. Germany and the U.S. are leading early adoption, with the reduced total cost of ownership driving automation as a critical factor in purchase decisions.

Rising Demand for Recycled and Biodegradable Polymer Extrusion

The EU Packaging and Packaging Waste Regulation mandates 30-65% recycled content between 2030 and 2040, prompting a wave of line retrofits that favor twin-screw starve-feeding of dusty flake streams. Coperion's STS 35 Mc 11 boosts throughput by 27% on contaminated regrind because intermeshing screws self-clean and control melt temperature. California's requirement that all packaging be recyclable or compostable by 2032 lifts interest in bio-based PLA extrusion lines. Manufacturers respond with abrasion-resistant screws, tighter residence-time control, and low-shear melting zones that protect recycled polymer integrity, reshaping value propositions across the plastic extrusion machine market.

Environmental Regulations on Virgin-Plastic Use

Canada's prohibition on single-use plastics, along with California's SB 54, is requiring retailers and restaurants to transition from virgin materials to recycled or compostable options. This regulatory compliance has increased demand for food-grade rPET, which is priced 25% higher than its virgin counterpart. Additionally, converters are working within tight deadlines to validate new formulations. In Europe, a 2030 recyclability mandate will restrict multilayer laminates that cannot be easily delaminated. Converters unable to modify their production lines may lose contracts, as brand owners increasingly prefer suppliers that provide traceable recycled content.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Predictive Process Control for Zero-Defect Output

- On-Site Micro-Extrusion for Personalized Medical Implants

- Scarcity of High-Torque Gearbox Suppliers Lengthening Lead Times

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Twin-screw units are projected to grow faster than the broader plastic extrusion machine market, with a 6.21% CAGR through 2031. This growth is observed across various regions, even though single-screw machines accounted for 53.11% of the plastic extrusion machine market share in 2025. The market size for laboratory twin-screw systems in plastic extrusion remains relatively small today, but it is expanding at a notable rate. This trend is driven by converters in different geographies running trial batches of recycled or bio-based formulations before scaling to production.

Modular screw elements allow operators to adjust kneading, conveying, and devolatilizing sections, which improves pigment dispersion at 0.1% loadings and helps prevent thermal degradation in hygroscopic polymers. Capital investment increases with screw diameter, but throughput grows with the square of that diameter, reducing cost per kilogram for high-volume plants. Single-screw machines continue to dominate the pipe and profile sector due to their simpler maintenance requirements. However, their market share is gradually declining in regions where converters are qualifying high-regrind recipes that only twin-screw machines can process consistently.

In 2025, blown film accounted for 32.24% of the revenue share. However, extrusion coating and lamination are anticipated to grow at a CAGR of 6.42%, reflecting the increasing preference among brand owners for mono-material barrier structures. The plastic extrusion machine market, particularly for nine-to-eleven-layer coating lines, is expanding as food brands transition from mixed laminate pouches to all-PE alternatives that align with upcoming grade-A recyclability labels.

Energy audits indicate that co-extrusion consumes less than 2.6 kWh per square meter, which is approximately half the energy usage of solvent-based laminate production. This allows converters to reduce energy expenses and compliance costs related to solvent emissions. While pipe, tubing, and profile lines continue to meet infrastructure demands in India and ASEAN, investments are gradually shifting toward barrier-film lines. These lines are designed to support contracts requiring extended shelf life for products such as fresh meat and ready-to-eat meals.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 48.22% of global revenue and is projected to achieve a CAGR of 6.88% through 2031, supported by capacity expansions in China, India, and ASEAN nations. Thailand, with its 3,200 converters and 34.6 million tonnes of petrochemical capacity, shows room for improvement in recycling. Growth opportunities may arise if policymakers implement stricter circular-economy targets.

In North America, retrofitting facilities is prioritized over constructing new ones, particularly with regulations such as California's SB 54 and Canadian bans becoming more stringent. However, low mechanical-recycling rates have led to a reliance on importing certified rPET from Europe, which continues to drive investments in twin-screw reclamation lines. Mexico is attracting near-shoring investments, particularly in EV wiring and food-contact films, facilitating cross-border supplies to U.S. OEMs under the USMCA agreement.

Europe operates under some of the most stringent regulations in the industry. The PPWR's focus on recycled content and recyclability grades is encouraging converters to adopt advanced five-to-eleven-layer coextruders equipped with online quality analytics. Germany and Italy are leading in automation adoption, while Eastern Europe and the Nordics are testing chemical-recycling feedstock preparation, which requires high-vacuum devolatilization extruders. In South America and the Middle East, growth remains uneven: Brazil is investing in silage-film lines despite currency fluctuations, and Saudi Arabia is increasing its HDPE pipe capacity to address water infrastructure needs.

- Bausano S.p.A, societa unipersonale

- BREYER Maschinenfabrik GmbH

- Coperion GmbH

- Costruzioni Meccaniche Luigi Bandera SpA

- Cowell (Nanjing) Extrusion Machinery Co., Ltd.

- Davis-Standard, LLC

- Hillenbrand

- JianTai

- JWELL Extrusion Machinery Co., Ltd.

- Kolsite Group (Rajoo Engineers)

- KraussMaffei

- KUNG HSING PLASTIC MACHINERY CO., LTD.

- Leistritz Extrusionstechnik GmbH

- Nanjing KY Chemical Machinery

- Qingdao Shansu Extrusion Equipment Co.,ltd

- Reifenhauser Group

- SML Maschinengesellschaft mbH

- The Japan Steel Works Ltd.

- Windsor Machines Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advancements in automation and energy-efficient machinery

- 4.2.2 Rising demand for recycled and biodegradable polymer extrusion

- 4.2.3 Government incentive schemes for circular-economy equipment

- 4.2.4 AI-enabled predictive process control for zero-defect output

- 4.2.5 On-site micro-extrusion for personalised medical implants

- 4.3 Market Restraints

- 4.3.1 Environmental regulations on virgin-plastic use

- 4.3.2 Scarcity of high-torque gearbox suppliers lengthening lead-times

- 4.3.3 Skilled operator shortage amid demographic shift

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Machine Type

- 5.1.1 Single Screw Extrusion

- 5.1.2 Twin Screw Extrusion

- 5.1.3 Multi-screw and Exotic Configurations

- 5.1.4 Ancillary Down-stream Equipment

- 5.2 By Process Type

- 5.2.1 Blown Film Extrusion

- 5.2.2 Sheet / Film Extrusion

- 5.2.3 Tubing and Profile Extrusion

- 5.2.4 Pipe Extrusion

- 5.2.5 Extrusion Coating and Lamination

- 5.2.6 Other Process Types

- 5.3 By Automation Level

- 5.3.1 Semi-Automated (PLC-integrated)

- 5.3.2 Conventional (Manual / Relay-based)

- 5.3.3 Fully-Automated (SCADA / IoT-enabled)

- 5.4 By End-user Industry

- 5.4.1 Packaging

- 5.4.2 Building and Construction

- 5.4.3 Automotive and Transportation

- 5.4.4 Electrical and Electronics

- 5.4.5 Consumer Goods and Appliances

- 5.4.6 Medical and Healthcare

- 5.4.7 Agriculture

- 5.4.8 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Bausano S.p.A, societa unipersonale

- 6.4.2 BREYER Maschinenfabrik GmbH

- 6.4.3 Coperion GmbH

- 6.4.4 Costruzioni Meccaniche Luigi Bandera SpA

- 6.4.5 Cowell (Nanjing) Extrusion Machinery Co., Ltd.

- 6.4.6 Davis-Standard, LLC

- 6.4.7 Hillenbrand

- 6.4.8 JianTai

- 6.4.9 JWELL Extrusion Machinery Co., Ltd.

- 6.4.10 Kolsite Group (Rajoo Engineers)

- 6.4.11 KraussMaffei

- 6.4.12 KUNG HSING PLASTIC MACHINERY CO., LTD.

- 6.4.13 Leistritz Extrusionstechnik GmbH

- 6.4.14 Nanjing KY Chemical Machinery

- 6.4.15 Qingdao Shansu Extrusion Equipment Co.,ltd

- 6.4.16 Reifenhauser Group

- 6.4.17 SML Maschinengesellschaft mbH

- 6.4.18 The Japan Steel Works Ltd.

- 6.4.19 Windsor Machines Pvt. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

塑膠擠出成型機市場:按機器類型、聚合物類型、自動化程度、應用和最終用途產業分類-2026-2032年全球市場預測

塑膠擠出成型機市場:按機器類型、聚合物類型、自動化程度、應用和最終用途產業分類-2026-2032年全球市場預測 塑膠擠出成型機市場報告:按機器類型、工藝類型、材料、解決方案、應用和地區分類(2026-2034 年)

塑膠擠出成型機市場報告:按機器類型、工藝類型、材料、解決方案、應用和地區分類(2026-2034 年) 橡膠押出機市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,並預測2026-2034年擠出成型機市場:按類型、材料、製程和應用分類-2026-2032年全球市場預測橡膠雙螺桿擠出機市場:按機器類型、材料類型、螺桿配置、應用和最終用戶產業分類-2026-2032年全球預測輕金屬擠壓機市場:依擠壓機類型、壓力等級、最終用途產業分類,全球預測(2026-2032)金屬擠壓機市場:按產品類型、材料類型、產能和應用分類,全球預測(2026-2032)擠出機市場:依機器類型、產品類型、產能、應用和終端用戶產業分類,全球預測,2026-2032年直接擠出機市場:材料類型、壓機類型、壓力能力和最終用途產業分類,全球預測,2026-2032年直接鋁擠壓機市場:按產品類型、壓力機類型、壓力機產能和最終用途產業分類,全球預測,2026-2032年

橡膠押出機市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,並預測2026-2034年擠出成型機市場:按類型、材料、製程和應用分類-2026-2032年全球市場預測橡膠雙螺桿擠出機市場:按機器類型、材料類型、螺桿配置、應用和最終用戶產業分類-2026-2032年全球預測輕金屬擠壓機市場:依擠壓機類型、壓力等級、最終用途產業分類,全球預測(2026-2032)金屬擠壓機市場:按產品類型、材料類型、產能和應用分類,全球預測(2026-2032)擠出機市場:依機器類型、產品類型、產能、應用和終端用戶產業分類,全球預測,2026-2032年直接擠出機市場:材料類型、壓機類型、壓力能力和最終用途產業分類,全球預測,2026-2032年直接鋁擠壓機市場:按產品類型、壓力機類型、壓力機產能和最終用途產業分類,全球預測,2026-2032年