|

市場調查報告書

商品編碼

2062144

壓電陶瓷:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Piezoelectric Ceramics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

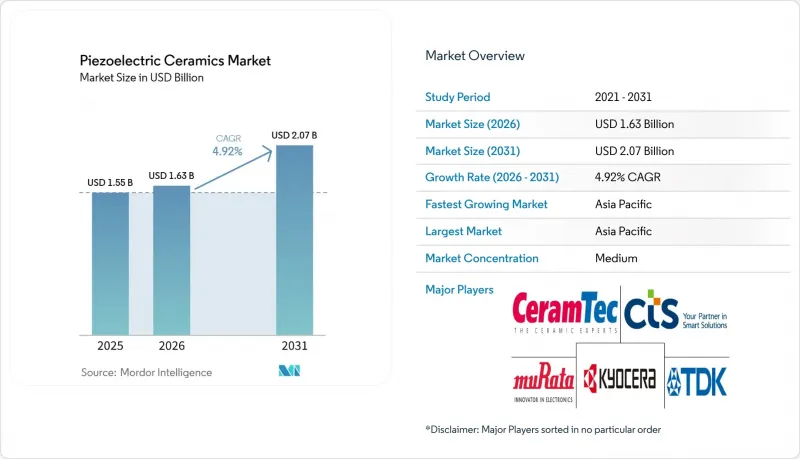

根據 Mordor Intelligence 預測,壓電陶瓷市場規模將從 2025 年的 15.5 億美元和 2026 年的 16.3 億美元成長到 2031 年的 20.7 億美元,2026 年至 2031 年的複合年成長率為 4.92%。

本報告按材料成分(含鉛和無鉛)、應用(感測器、執行器、能源採集和奈米發電機等)、終端用戶產業(家用電子電器、汽車和電動車等)以及地區(亞太地區、北美、歐洲、南美以及中東和非洲)進行細分。市場預測以美元計價。

全球壓電陶瓷市場趨勢與洞察

醫療影像設備和治療設備的應用範圍擴大

隨著醫院尋求攜帶式解決方案,壓電陶瓷正日益取代傳統換能器材料,應用於小型超音波設備。無鉛KNN陶瓷在穿戴式超音波貼片中實現了630 pC/N的d33值,在保持靈敏度的同時,有效解決了毒性問題。採用CMOS生產線製造的pMUT(壓電陶瓷換能器)降低了生產成本,並簡化了照護現場掃描器中的訊號整合。高強度聚焦超音波(HIFU)系統目前採用直徑超過150 mm的CeramTec半球形換能器,滿足腫瘤消融的功率密度需求。美國和歐盟的生物相容性法規正在加速向無鉛BNT-BT複合材料的過渡,這種材料在較低的工作溫度下即可提供與PZT相當的輸出功率。因此,設備製造商在性能和法規合規性方面均受益,從而推動了壓電陶瓷市場的發展。

5G/6G射頻濾波器的微型化需要高介電常數的壓電陶瓷。

毫米波部署需要用於製造高Q值體聲波(BAW)和聲表面波(SAW)濾波器的AlScN和LiNbO3薄膜,這些濾波器需能安裝在尺寸小於1mm²的智慧型手機模組中。 kt²值超過10%的AlScN薄膜能夠提供行動電話製造商在頻寬的頻段分配中所需的更陡峭的滾降特性。 LiNbO3 LLSAW濾波器針對6GHz以下頻寬進行了最佳化,與石英相比,具有更優異的功率處理能力。FUJIFILM2025年獲得專利的鈮摻雜PZT多層薄膜在低於7V的電壓下實現了389 pC/V的d31值,滿足了低電壓移動電子設備的要求。 6G研發中頻段的快速成長確保了持續的需求,並支撐了壓電陶瓷市場的長期發展。

與基於PVDF的壓電聚合物的競爭

聚偏氟乙烯(PVDF)的柔軟性、輕量化以及獲得FDA批准等優勢,正推動其在穿戴式裝置、軟體機器人和植入式感測器等領域廣泛應用,對硬質陶瓷構成挑戰。其d33值僅20–30 pC/N,遠低於壓電陶瓷(PZT),足以滿足低力應用的需求。溶液澆鑄和靜電紡絲等經濟高效的製造方法,正促使消費品牌採用聚合物薄膜。這種向入門級應用領域的轉變,加劇了價格競爭,並對整個壓電陶瓷市場的利潤率構成壓力。

細分市場分析

截至2025年,含鉛系統將佔據壓電陶瓷市場81.11%的佔有率,預計到2031年,這一佔有率將以5.14%的複合年成長率成長。含鉛產品的市場規模成長速度超過整體市場,這主要得益於PZT d33值超過600 pC/N的基準設定。正如FUJIFILM公司7V以下多層致動器專利所示,製造商正在使用鈮等摻雜劑來提高性能。無鉛方案也在同步開發,以降低未來的合規風險,但PZT在醫療影像和聲納等高性能應用領域的優勢仍然無可撼動。

BNT-BT圓盤在40 kHz超音波清洗機中展現出與PZT相當的聲輸出性能,同時抑制了熱量的產生;而KNN軟質材料則適用於水下接收器。居里溫度超過650 度C的鉍層狀鐵電使其能夠在極端溫度下應用,例如油井測井。然而,由於更換材料時需要對形狀、電壓和壽命進行重新認證,其應用速度正在放緩,儘管這支撐了壓電陶瓷市場多年來的成長勢頭。

區域分析

預計到2025年,亞太地區將佔全球銷售額的52.22%,並維持5.78%的複合年成長率直至2031年。中國在粉末和低成本圓盤的大規模生產方面具有優勢,日本專注於多層和薄膜精密元件,而韓國和台灣則將元件整合到智慧型手機和5G模組中。村田製作所投資2.33億美元、將於2026年2月完工的福井研發中心,正透過專注於鈦酸鋇和PZT的技術開發,進一步鞏固其在該地區的領先地位。印度公司,例如Sparkler Ceramics,正在擴大工業感測器的生產,而澳洲礦業公司則推動了對用於惡劣環境的耐環境感測器的需求。

北美市場的需求主要由航太、國防和醫療超音波應用驅動。 《晶片製造獎勵法案》(CHIPS Act)下的製造業獎勵,透過共用半導體生產和無塵室設施,間接惠及壓電陶瓷產業。 TDK在美國為蘋果產品新建的生產線,凸顯了在日益加劇的地緣政治不確定性下,在地採購的吸引力。加拿大和墨西哥透過組裝航太工具和汽車感測器,為區域壓電陶瓷市場做出貢獻。

在歐洲,德國的汽車和工業自動化產業以及英國的航太產業發揮主導作用。 CeramTec公司正在擴大用於聲納應用的大型PZT圓盤的生產,而PI Ceramic公司在2025年4月於BNT和KNN材料方面取得的進展正在加速聯合專案的推進。歐盟嚴格的RoHS法規促使無鉛替代品的普及速度比其他地區更快。此外,巴西的近海能源專案和沙烏地阿拉伯的智慧城市計畫雖然規模較小,但正在全球壓電陶瓷市場創造具有戰略意義的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大醫療影像診斷設備和治療設備的應用範圍。

- 5G/6G射頻濾波器的微型化需要高介電常數的壓電陶瓷。

- 政府對採用PZT介質的國內MLCC產能的支持措施

- 量子換能器的研究與開發推動了對低溫壓電陶瓷的需求。

- 積層製造技術使得在航太領域實現複雜的壓電超結構成為可能。

- 市場限制因素

- 與基於PVDF的壓電聚合物的競爭

- 無鉛KNN系統用Nb2O5和Ta2O5的供應鏈波動性

- 積層製造技術大規模生產壓電陶瓷的缺陷率較高

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按材料組成

- 鉛基(PZT、PMN-PT、PZN-PT)

- 無鉛(BNT-BT、KNN、BaTiO3、ZnO)

- 透過使用

- 感測器(壓力感測器、超音波、MEMS麥克風)

- 執行器(燃油噴射器、微定位器)

- 能量收集器和奈米發電機

- 超音波成像和清洗

- 頻率控制與定時(SAW/BAW共振器)

- 按最終用戶行業分類

- 家用電子產品

- 汽車和電動旅行

- 醫療保健和生命科學

- 工業自動化與機器人技術

- 航太/國防

- 能源公用事業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 北歐國家

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- APC International Ltd.

- Arkema

- CeramTec GmbH

- CTS Corporation

- FUJI CERAMICS CORPORATION

- Johnson Matthey

- KEMET

- Kistler Group

- KYOCERA Corporation

- Morgan Advanced Materials

- Murata Manufacturing Co., Ltd.

- Physik Instrumente(PI)SE & Co. KG

- PI Ceramic GmbH

- Piezosystem Jena GmbH

- SAMSUNG ELECTRO-MECHANICS

- Sensortech Canada

- Sparkler Ceramics Pvt. Ltd.

- TDK Corporation

- TRS Technologies Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the piezoelectric ceramics market size is projected to expand from USD 1.55 billion in 2025 and USD 1.63 billion in 2026 to USD 2.07 billion by 2031, registering a CAGR of 4.92% between 2026 to 2031.

This report is Segmented by Material Composition (Lead-Based and Lead-Free), Application (Sensors, Actuators, Energy Harvesters and Nanogenerators, and More), End-User Industry (Consumer Electronics, Automotive and E-Mobility, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Piezoelectric Ceramics Market Trends and Insights

Rising Adoption in Medical Imaging and Therapeutic Devices

Piezoelectric ceramics are increasingly replacing older transducer materials in compact ultrasound equipment as hospitals demand portable solutions. Lead-free KNN ceramics have achieved a d33 of 630 pC/N in wearable ultrasound patches, addressing toxicity concerns while maintaining sensitivity. pMUTs manufactured on CMOS lines reduce production costs and simplify signal integration in point-of-care scanners. High-intensity focused ultrasound systems now utilize CeramTec hemispherical discs larger than 150 mm, meeting power-density requirements for tumor ablation. Biocompatibility regulations in the United States and EU are accelerating the transition to lead-free BNT-BT composites, which match PZT power output at lower drive temperatures. As a result, device manufacturers are achieving both performance and compliance benefits, strengthening the piezoelectric ceramics market.

5G/6G RF-Filter Miniaturization Needs High-k Piezoceramics

Millimeter-wave rollouts require AlScN and LiNbO3 thin films for high-Q BAW and SAW filters that fit inside smartphone modules under 1 mm2. AlScN's kt2 exceeding 10% provides a sharper roll-off that handset OEMs need for crowded spectrum allocations. LiNbO3 LLSAW filters are optimized for sub-6 GHz bands, offering superior power handling compared to quartz. FUJIFILM's 2025 patent on niobium-doped PZT multilayers achieves a d31 of 389 pC/V below 7 V, aligning with the requirements of low-voltage mobile electronics. The rapid multiplication of frequency bands in 6G R&D ensures sustained demand, supporting long-term growth in the piezoelectric ceramics market.

Competition from PVDF-Based Piezopolymers

PVDF's flexibility, lightweight properties, and FDA clearance are driving its adoption in wearables, soft robotics, and implantable sensors, challenging rigid ceramics. While its d33 of 20-30 pC/N is significantly lower than PZT, it is sufficient for low-force applications. Cost-effective production methods such as solution casting and electrospinning are encouraging consumer brands to adopt polymer films. This shift toward entry-level applications intensifies price competition, exerting pressure on margins across the piezoelectric ceramics market.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Local MLCC Capacity Using PZT Dielectrics

- Quantum Transducer R&D Drives Cryogenic Piezoceramic Demand

- Supply-Chain Volatility of Nb2O5 and Ta2O5 for Lead-Free KNN Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lead-based systems accounted for 81.11% of the piezoelectric ceramics market share in 2025, with this share projected to grow at a 5.14% CAGR through 2031. The market size for lead-based variants is expanding faster than the overall market due to PZT's benchmark-setting d33 values exceeding 600 pC/N. Manufacturers are enhancing performance through dopants like niobium, as demonstrated by FUJIFILM's sub-7 V multilayer actuator patent. Parallel lead-free programs are being developed to mitigate future compliance risks but have yet to challenge PZT's dominance in high-performance applications such as medical imaging and sonar.

BNT-BT discs have shown equivalent acoustic power to PZT in 40 kHz ultrasonic cleaners with reduced heat generation, while KNN soft grades are targeting underwater receivers. Bismuth-layered ferroelectrics, with Curie points above 650 °C, are enabling extreme-temperature applications like oil-well logging. However, each substitution requires requalification in terms of geometry, voltage, and lifetime, which slows adoption but supports a multi-year growth trajectory within the piezoelectric ceramics market.

Geography Analysis

Asia-Pacific generated 52.22% of global revenue in 2025 and is projected to grow at a 5.78% CAGR through 2031. China dominates in high-volume powder and low-cost disc production, Japan specializes in multilayer and thin-film precision parts, and South Korea and Taiwan integrate components into smartphones and 5G modules. Murata's USD 233 million Fukui R&D facility, completed in February 2026, focuses on barium titanate and PZT advancements, reinforcing the region's leadership. Indian companies like Sparkler Ceramics are scaling industrial sensor production, while Australian miners drive demand for ruggedized sensors in challenging environments.

North America's demand is driven by aerospace, defense, and medical ultrasound applications. The CHIPS Act's fabrication incentives have indirectly benefited piezoelectric ceramics by sharing cleanroom facilities with semiconductor production. TDK's new U.S. production line for Apple products underscores the appeal of local sourcing amid geopolitical uncertainties. Canada and Mexico contribute through aerospace tooling and automotive sensor assembly, supporting the regional piezoelectric ceramics market.

Europe is led by Germany's automotive and industrial automation sectors and the United Kingdom's aerospace industry. CeramTec is scaling up production of large-format PZT discs for sonar applications, while PI Ceramic's April 2025 advancements in BNT and KNN materials have spurred collaborative projects. Strict EU RoHS regulations are accelerating the adoption of lead-free alternatives faster than in other regions. Additionally, Brazil's offshore energy projects and Saudi Arabia's smart-city initiatives contribute smaller but strategically significant volumes to the global piezoelectric ceramics market.

- APC International Ltd.

- Arkema

- CeramTec GmbH

- CTS Corporation

- FUJI CERAMICS CORPORATION

- Johnson Matthey

- KEMET

- Kistler Group

- KYOCERA Corporation

- Morgan Advanced Materials

- Murata Manufacturing Co., Ltd.

- Physik Instrumente (PI) SE & Co. KG

- PI Ceramic GmbH

- Piezosystem Jena GmbH

- SAMSUNG ELECTRO-MECHANICS

- Sensortech Canada

- Sparkler Ceramics Pvt. Ltd.

- TDK Corporation

- TRS Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising adoption in medical imaging and therapeutic devices

- 4.2.2 5G/6G RF-filter miniaturisation needs high-k piezoceramics

- 4.2.3 Government incentives for local MLCC capacity using PZT dielectrics

- 4.2.4 Quantum transducer R&D drives cryogenic piezoceramic demand

- 4.2.5 Additive manufacturing enables complex aerospace piezo meta-structures

- 4.3 Market Restraints

- 4.3.1 Competition from PVDF-based piezopolymers

- 4.3.2 Supply-chain volatility of Nb2O5 and Ta2O5 for lead-free KNN systems

- 4.3.3 High scrap rates in additive-manufactured piezoceramics scale-up

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Composition

- 5.1.1 Lead-based (PZT, PMN-PT, PZN-PT)

- 5.1.2 Lead-free (BNT-BT, KNN, BaTiO3, ZnO)

- 5.2 By Application

- 5.2.1 Sensors (pressure, ultrasonic, MEMS mics)

- 5.2.2 Actuators (fuel injectors, micro-positioners)

- 5.2.3 Energy Harvesters and Nanogenerators

- 5.2.4 Ultrasonic Imaging and Cleaning

- 5.2.5 Frequency Control and Timing (SAW/BAW resonators)

- 5.3 By End-user Industry

- 5.3.1 Consumer Electronics

- 5.3.2 Automotive and E-Mobility

- 5.3.3 Healthcare and Life-Sciences

- 5.3.4 Industrial Automation and Robotics

- 5.3.5 Aerospace and Defense

- 5.3.6 Energy and Utilities

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 Australia

- 5.4.1.5 NORDIC Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 APC International Ltd.

- 6.4.2 Arkema

- 6.4.3 CeramTec GmbH

- 6.4.4 CTS Corporation

- 6.4.5 FUJI CERAMICS CORPORATION

- 6.4.6 Johnson Matthey

- 6.4.7 KEMET

- 6.4.8 Kistler Group

- 6.4.9 KYOCERA Corporation

- 6.4.10 Morgan Advanced Materials

- 6.4.11 Murata Manufacturing Co., Ltd.

- 6.4.12 Physik Instrumente (PI) SE & Co. KG

- 6.4.13 PI Ceramic GmbH

- 6.4.14 Piezosystem Jena GmbH

- 6.4.15 SAMSUNG ELECTRO-MECHANICS

- 6.4.16 Sensortech Canada

- 6.4.17 Sparkler Ceramics Pvt. Ltd.

- 6.4.18 TDK Corporation

- 6.4.19 TRS Technologies Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment