|

市場調查報告書

商品編碼

2062137

元素氟:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Elemental Fluorine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

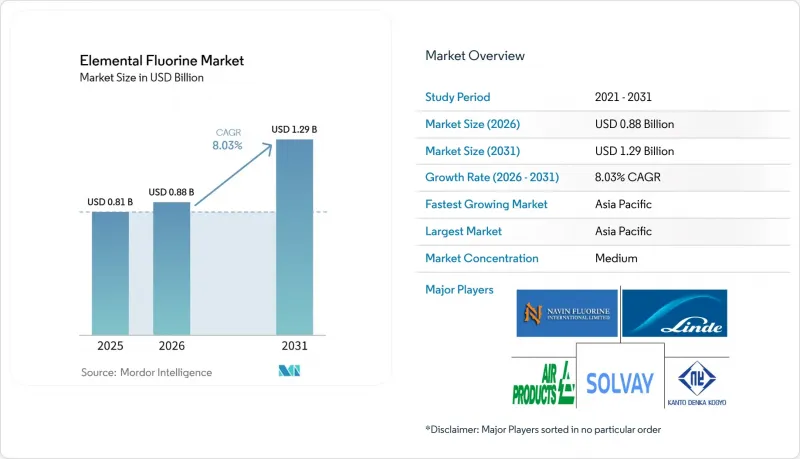

根據 Mordor Intelligence 預測,元素氟的市場規模預計在 2025 年達到 8.1 億美元,2026 年達到 8.8 億美元,到 2031 年達到 12.9 億美元,2026 年至 2031 年的複合年成長率為 8.03%。

本報告按類型(α-氟和BETA-氟)、應用(電子半導體、核能核能、六氟化硫、化學加工及其他)和地區(亞太地區、北美地區、歐洲地區、南美地區以及中東和非洲地區)進行細分。市場預測以美元計價。

全球元素氟市場趨勢及洞察

擴大六氟化鈾(UF6)的轉化和濃縮能力,以生產核燃料。

隨著先進核子反應爐從試驗階段邁向早期商業部署,政府支持的濃縮計畫正在增加氟的消耗量。 Centrus Energy位於俄亥俄州皮克頓的工廠正在擴建,根據2026年簽署的一份多年工程契約,將安裝數千台離心機,預計將成為美國西部唯一一家獲得許可供應高濃縮鈾和低濃縮鈾(LEU)燃料的工廠。由於在UF4轉化為UF6的過程中,每公斤低濃縮鈾(LEU)都需要元素氟,核能發電與氟的需求直接相關。法國和印度類似的產能擴張進一步強化了中期需求前景。提供符合核能標準純度等級氟的供應商正在簽署為期10年的啟動契約,這些合約支持對新型電解槽的投資。

塑膠、液晶顯示器和OLED顯示器的蝕刻和清洗應用領域不斷成長。

到2025年,OLED將佔LG Display銷售額的61%,該公司正投資9.7億美元,計劃在2027年前擴建其面板生產線。先進的顯示技術需要多次乾式蝕刻工藝,其中含氟氣體用於去除聚合物殘留物,而不會損壞底層材料。在5奈米以下的半導體晶圓廠中,由於元素氟的全球暖化潛值(GWP)為零,因此被用於腔室清洗,從而有助於實現範圍1的排放目標。這些趨勢在亞太地區尤為集中,該地區超過80%的新增顯示器和半導體產能正在建設中,使其成為元素氟市場短期內最大的成長要素。

氟電解生產廠需要高額資本投資(Capex)和營運成本(Opex)。

電解槽需要鎳銅合金、雙層管道和連續氣體監測系統等專用材料,大規模設施的安裝成本超過1000萬美元。在歐洲,與亞洲工廠相比,更高的電費進一步推高了變動成本,限制了國內擴張;同時,將半成品送回亞洲進行代工生產的趨勢日益成長。

細分市場分析

預計到2025年,α-氟將佔據元素氟市場70.78%的佔有率。這得益於其在核燃料轉化和半導體腔室清洗領域長期累積的成熟基礎設施。此外,該領域還擁有穩定的基本客群、成熟的鈍化製程以及易於取得的分析標準。

儘管BETA-氟的基數較小,但預計到2031年,其複合年成長率將達到8.24%。 BETA-氟在選擇性氟化反應中的獨特反應活性日益受到電池和製藥領域創新者的價值認可。隨著生產規模的擴大,BETA-氟在元素氟市場中的佔有率預計將會增加,但α-氟在整個預測期內仍可能保持其主導地位。

區域分析

亞太地區擁有顯示器、半導體和電動車等產品的供應鏈集中地,預計到2025年將佔全球銷售額的54.45%。中國製造商如東岳集團正將1.919億港幣重新分配,用於建設高純度聚四氟乙烯(PTFE)和四氟丙烯(TP)的試驗生產線,以生產低全球暖化潛值(GWP)冷媒,用於晶片製造廠。隨著韓國OLED產能的擴張和日本對精細氣體領域的投資進一步鞏固了該地區的地位,預計到2031年,亞太地區的複合年成長率將保持8.95%。

在北美,隨著亞利桑那州和德克薩斯州的製造項目符合《晶片和工業產品補貼法案》(CHIPS Act)的津貼資格,以及東南部地區的電池材料項目根據《通貨膨脹控制法案》(Inflation Control Act)逐步建立,該行業的戰略重要性正在恢復。光是Centrus Energy公司的Piketon HALEU專案就能為核燃料混合提供數年的氟原料。由於國內螢石短缺問題依然存在,且無水氟化氫(HF)的大部分原料仍依賴從墨西哥和中國進口,生產商正將HF工廠集中建在墨西哥灣沿岸地區。

歐洲面臨電價飆升和氟氣配額緊張的雙重壓力。儘管大型工業氣體公司傾向於擴大位於德國和愛爾蘭的現有設施,但為了降低營運成本風險,許多冷媒和聚偏氟乙烯(PVDF)的生產擴張正轉移到肯塔基州和江蘇省。無水氟化氫的高昂進口成本使歐洲處於結構性劣勢,儘管有針對低全球暖化潛勢(GWP)化學品的監管獎勵,但元素氟市場的成長速度仍落後於全球平均水平。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大六氟化鈾轉化和濃縮能力,用於核燃料

- 拓展蝕刻和清洗塑膠、液晶顯示器和OLED顯示器的應用。

- 由於法規的實施,高全球暖化潛勢 (GWP) NF3 類車輛將逐步減少,這將促進 F2 類車輛的普及。

- 現場模組化氟發生器可降低物流風險

- 高純度F2作為鋰離子電池電解添加劑的新應用

- 市場限制因素

- 氟電解生產廠的高資本投資和營運成本

- 全球電池用無水氟化氫原料供不應求

- 持證氟化物處理技術人員短缺

- 價值鏈分析

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- α-氟

- BETA-氟

- 透過使用

- 電子和半導體

- 能源與核能

- 六氟化硫

- 化學處理

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Air Liquide

- Air Products and Chemicals, Inc.

- Arkema

- Central Glass Co., Ltd.

- DAIKIN INDUSTRIES, Ltd.

- Deepak Nitrite Limited

- DONGYUE GROUP

- F2 Chemicals Ltd.

- Inhance Technologies

- KANTO DENKA KOGYO CO., LTD.

- Linde PLC

- Messer SE & Co. KGaA

- Navin Fluorine International Limited

- Pelchem SOC Ltd.

- Resonac

- Solvay

- The Chemours Company

第7章 市場機會與未來展望

According to Mordor Intelligence, the elemental fluorine market size is projected to be USD 0.81 billion in 2025, USD 0.88 billion in 2026, and reach USD 1.29 billion by 2031, growing at a CAGR of 8.03% from 2026 to 2031.

This report is Segmented by Type (a-Fluorine and B-Fluorine), Application (Electronics and Semiconductors, Energy and Nuclear, Sulfur Hexafluoride, Chemical Processing, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Elemental Fluorine Market Trends and Insights

Expansion of UF6 Conversion/Enrichment Capacity for Nuclear Fuel

Government-supported enrichment projects are increasing fluorine consumption as advanced reactors transition from pilot phases to early commercial deployment. Centrus Energy's Piketon, Ohio site is expanding with thousands of centrifuges under a multi-year engineering contract awarded in 2026, positioning the facility as the West's only licensed source of high-assay LEU fuel. Each kilogram of LEU requires elemental fluorine during the UF4-to-UF6 conversion process, directly linking nuclear capacity to fluorine demand. Similar capacity expansions in France and India are further strengthening mid-term demand visibility. Suppliers offering nuclear-qualified purity grades are securing decade-long offtake agreements, which support investments in new electrolyzers.

Growth in Plastics, LCD and OLED Display Etching/Cleaning Uses

OLED penetration accounted for 61% of LG Display's revenue in 2025, with the company investing USD 970 million to expand panel production lines through 2027. Advanced display technologies require multiple dry-etch processes, where fluorinated gases remove polymeric residues without damaging underlying layers. Semiconductor fabs operating below the 5 nm node are adopting elemental fluorine for chamber cleaning due to its zero-GWP properties, which help meet Scope 1 emissions targets. These trends are particularly concentrated in the Asia-Pacific region, where over 80% of new display and semiconductor capacity is under construction, representing the largest near-term growth driver for the elemental fluorine market.

High Capex/Opex for Fluorine Electrolysis Production Plants

Electrolyzer cells require specialized materials such as nickel-copper alloys, double-walled piping, and continuous gas monitoring systems, driving installed costs above USD 10 million for large facilities. In Europe, high electricity tariffs further increase variable costs compared to Asian plants, limiting domestic expansion and encouraging the tolling of semi-finished intermediates back to Asia.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Phase-Down of High-GWP NF3 Favoring F2 Adoption

- On-Site Modular Fluorine Generators Reducing Logistics Risk

- Limited Global Supply of Battery-Grade Anhydrous HF Feedstock

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

a-Fluorine accounted for 70.78% of the elemental fluorine market share in 2025, supported by long-established infrastructure used for nuclear fuel conversion and semiconductor chamber cleaning. This segment benefits from a stable customer base, proven passivation protocols, and readily available analytical standards.

B-Fluorine is projected to grow at a CAGR of 8.24% through 2031, albeit from a smaller base. Its unique reactivity for selective fluorination is increasingly valued by battery and pharmaceutical innovators. As production scales up, B-Fluorine's contribution to the elemental fluorine market size is expected to increase, though a-Fluorine is likely to retain its dominance through the forecast period.

Geography Analysis

Asia-Pacific controlled 54.45% of global revenue in 2025 thanks to the clustering of display, semiconductor, and EV supply chains. Chinese producers such as Dongyue are redirecting HK$191.9 million into high-purity PTFE for chip fabs and pilot tetrafluoropropylene lines that enable low-GWP refrigerants South Korean OLED expansions and Japanese fine-gas investments further strengthen the region's position, keeping Asia-Pacific on an 8.95% CAGR trajectory through 2031.

North America is regaining strategic weight as the CHIPS Act subsidizes fabs in Arizona and Texas, while the Inflation Reduction Act anchors battery-material projects in the Southeast. Centrus Energy's Piketon HALEU project alone creates a multiyear fluorine feed for nuclear fuel blending. Domestic fluorspar scarcity persists, so most anhydrous HF feedstock still ships from Mexico and China, nudging producers toward co-located HF plants on the Gulf Coast.

Europe faces the twin pressures of elevated electricity pricing and stringent F-gas quotas. Industrial-gas majors prefer brownfield expansions in Germany and Ireland, but many refrigerant and PVDF expansions are moving to Kentucky or Jiangsu to cap opex exposure. High anhydrous HF import costs place Europe at a structural disadvantage, keeping its Elemental fluorine market growth below the global mean despite regulatory incentives for low-GWP chemistries.

- Air Liquide

- Air Products and Chemicals, Inc.

- Arkema

- Central Glass Co., Ltd.

- DAIKIN INDUSTRIES, Ltd.

- Deepak Nitrite Limited

- DONGYUE GROUP

- F2 Chemicals Ltd.

- Inhance Technologies

- KANTO DENKA KOGYO CO., LTD.

- Linde PLC

- Messer SE & Co. KGaA

- Navin Fluorine International Limited

- Pelchem SOC Ltd.

- Resonac

- Solvay

- The Chemours Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of UF6 conversion/enrichment capacity for nuclear fuel

- 4.2.2 Growth in plastics, LCD and OLED display etching/cleaning uses

- 4.2.3 Regulatory phase-down of high-GWP NF3 favouring F2 adoption

- 4.2.4 On-site modular fluorine generators reducing logistics risk

- 4.2.5 Emerging use of high-purity F2 as lithium-ion battery electrolyte additive

- 4.3 Market Restraints

- 4.3.1 High capex/opex for fluorine electrolysis production plants

- 4.3.2 Limited global supply of battery-grade anhydrous HF feedstock

- 4.3.3 Shortage of certified fluorine-handling technicians

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 a- Fluorine

- 5.1.2 B- Fluorine

- 5.2 By Application

- 5.2.1 Electronics and Semiconductors

- 5.2.2 Energy and Nuclear

- 5.2.3 Sulfur Hexafluoride

- 5.2.4 Chemical Processing

- 5.2.5 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Air Liquide

- 6.4.2 Air Products and Chemicals, Inc.

- 6.4.3 Arkema

- 6.4.4 Central Glass Co., Ltd.

- 6.4.5 DAIKIN INDUSTRIES, Ltd.

- 6.4.6 Deepak Nitrite Limited

- 6.4.7 DONGYUE GROUP

- 6.4.8 F2 Chemicals Ltd.

- 6.4.9 Inhance Technologies

- 6.4.10 KANTO DENKA KOGYO CO., LTD.

- 6.4.11 Linde PLC

- 6.4.12 Messer SE & Co. KGaA

- 6.4.13 Navin Fluorine International Limited

- 6.4.14 Pelchem SOC Ltd.

- 6.4.15 Resonac

- 6.4.16 Solvay

- 6.4.17 The Chemours Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

氟化鋰市場-全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、地區和競爭格局分類,2021-2031年

氟化鋰市場-全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、地區和競爭格局分類,2021-2031年 氟化鎂市場:2026-2032年全球市場預測(依產品類型、等級、形態、最終用戶、銷售管道及應用分類)

氟化鎂市場:2026-2032年全球市場預測(依產品類型、等級、形態、最終用戶、銷售管道及應用分類) 氟化鈣晶體 - 全球市佔率及排名、2026年至2032年總銷售及需求預測五氟硫基化合物市場按產品類型、純度等級、製造技術、應用、終端用戶產業和銷售管道分類-2026-2032年全球預測氟化浸沒冷卻液市場按類型、純度等級、應用、終端用戶產業和分銷管道分類 - 全球預測(2026-2032 年)紫外光級氟化鈣晶體市場按形態、純度、應用、終端用戶產業和銷售管道,全球預測(2026-2032年)高性能含氟液體市場按產品類型、純度、形態、應用、終端用戶產業和分銷管道分類,全球預測(2026-2032年)

氟化鈣晶體 - 全球市佔率及排名、2026年至2032年總銷售及需求預測五氟硫基化合物市場按產品類型、純度等級、製造技術、應用、終端用戶產業和銷售管道分類-2026-2032年全球預測氟化浸沒冷卻液市場按類型、純度等級、應用、終端用戶產業和分銷管道分類 - 全球預測(2026-2032 年)紫外光級氟化鈣晶體市場按形態、純度、應用、終端用戶產業和銷售管道,全球預測(2026-2032年)高性能含氟液體市場按產品類型、純度、形態、應用、終端用戶產業和分銷管道分類,全球預測(2026-2032年) 無機氟化物市場規模、佔有率及成長分析(按形態、類型、最終用途、應用和地區分類)-2026-2033年產業預測

無機氟化物市場規模、佔有率及成長分析(按形態、類型、最終用途、應用和地區分類)-2026-2033年產業預測 元素氟市場規模、佔有率和成長分析(按形態、應用、最終用途產業和地區分類)-2026年至2033年產業預測

元素氟市場規模、佔有率和成長分析(按形態、應用、最終用途產業和地區分類)-2026年至2033年產業預測 氟化鋁市場規模、佔有率和成長分析(按類型、等級、應用和地區分類):產業預測(2026-2033 年)

氟化鋁市場規模、佔有率和成長分析(按類型、等級、應用和地區分類):產業預測(2026-2033 年)