|

市場調查報告書

商品編碼

2062125

特殊鋼:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Special Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

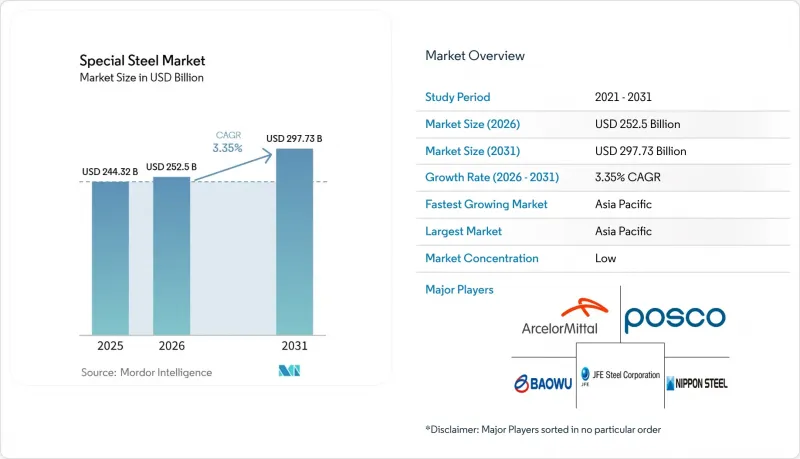

根據 Mordor Intelligence 預測,特種鋼市場規模將從 2025 年的 2,443.2 億美元成長到 2026 年的 2,525 億美元,到 2031 年將達到 2,977.3 億美元,2026 年至 2031 年的複合年成長率為 3.35%。

本報告按產品類型(不銹鋼、工具鋼、合金鋼等)、形狀(板材、棒材、捲材等)、應用領域(汽車零件、航太結構/引擎、機械/工具等)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以美元計價。

全球特種鋼市場趨勢與洞察

在脫碳背景下向電弧爐(EAF)和直接氫還原(H2-DRI)過渡。

與高爐相比,電弧爐 (EAF) 和氫直接還原鐵 (H2-DRI) 專案可將現場二氧化碳排放減少高達 70%。 SSAB 預計到 2026 年,其位於奧克瑟勒鬆的工廠將實現無石化燃料生產;H2 Green Steel 的目標是到 2030 年在瑞典生產 500 萬噸綠色鋼鐵。儘管資本密集度仍然很高,每噸年產能需要 1200 至 1500 美元,但隨著歐盟碳價超過每噸 90 歐元,投資回收期正在縮短。北美地區的改造項目,例如 Algoma Steel 投資 7 億加元的項目,符合汽車製造商的低碳採購要求。正如蒂森克虜伯在杜伊斯堡的改造計畫延長所顯示的那樣,如果氫氣供應和再生能源無法跟上計畫進度,實施風險依然存在。

可再生能源相關設施的擴建

離岸風電、電解槽和氫氣管道專案正在推動特種鋼不同等級最終用途的多元化。美國已撥款420億美元用於離岸風電基礎建設,目標是到2030年實現30吉瓦的裝置容量,相當於每年需要150萬至200萬噸鋼材。歐盟的「REPowerEU」計畫目標是到2050年實現300吉瓦的離岸風力發電,需要1500萬至2000萬噸鋼材用於單樁和塔筒。到2026年,電解槽的裝置容量可能達到8吉瓦,每吉瓦大約需要4000噸特殊不銹鋼。 API 5L X70/X80標準管道在氫氣輸送基礎設施中佔據主導地位,歐洲氫能骨幹網計畫預計到2040年將建成8.1萬公里的基礎設施。

能源密集型製程和碳定價

高爐煉鋼每噸粗鋼消耗18至22吉焦耳的能源,而碳定價機制推高營運成本的速度超過了鋼鐵廠向客戶轉嫁成本的速度。歐盟的排放權價格已超過90歐元(103美元),這將使整合成本每噸增加約18至20歐元(20至23美元),同時,到2026年,碳排放交易體系(CBAM)將關閉低成本進口管道。中國不斷擴大的碳市場以及對印度邊境調節政策的擔憂,正迫使國內生產商儘管初期成本較高,但仍投資興建電弧爐(EAF)。

細分市場分析

不銹鋼預計到2025年將佔據35.22%的市場佔有率,這凸顯了其在電解槽堆和海上結構防腐蝕方面的關鍵作用。印尼鎳鐵產量激增以及印度產能擴張將推動不鏽鋼市場到2031年維持3.67%的複合年成長率。工具鋼的需求趨於平穩,而積層製造在2023年工具生產中11%的佔有率將對傳統供應管道構成壓力。

合金鋼在傳動系統和重型機械部件中仍然發揮著重要作用,但向電動車的轉型正促使人們傾向於使用更輕的金屬。軸承鋼的創新,例如NSK的高速電動汽車車橋單元,正使電熱熔碴重熔的化學成分成為汽車供應鏈的主流。核能項目,例如俄羅斯國家原子能公司(Rosatom)的BR-1200鋼,正在推動奧氏體合金進入高溫應用領域。

區域分析

預計到2025年,亞太地區將佔43.35%的市場佔有率,這主要歸功於中國的規模優勢、印度的經濟獎勵策略以及印尼鎳礦產業的整合。中國寶武鋼鐵2024年粗鋼產量為1.3185億噸,並計劃透過氫能冶金在2050年實現碳中和。印度的目標是到2030-2031年實現3億噸的產能,並透過與生產連結獎勵計畫來降低對特種鋼進口的依賴。儘管東協地區的鋼鐵廠正在擴張,但由於土地徵用和資金籌措的延誤,這一擴張速度有所放緩。

在北美,他們正利用豐富的廢鋼資源和生產回流的有利條件。紐柯公司投資31億美元的鋼板廠和安賽樂米塔爾公司投資10億美元的卡爾弗特工廠維修項目都與目的地設備製造商(OEM)的輕量化計劃相契合。如果日本製鐵和美國鋼鐵公司的合作最終達成,預計將建立一個跨太平洋的特種鋼平台,而蓋爾道公司目前62%的息稅折舊攤銷前利潤(EBITDA)都集中在美國市場。

歐洲面臨最高的脫碳成本。 SSAB計劃在2026年前實現石化燃料鋼鐵供應,而Autokump的鉻鐵業務整合則降低了鉻價波動帶來的風險。由於碳排放交易體系(ETS)價格上漲對其熔爐獲利能力構成壓力,蒂森克虜伯正在尋求合作夥伴。英國塔爾伯特港的改造計畫則表明,在裁員的大背景下,政府仍給予了大力支持。

南美洲的命運取決於巴西的貿易保護措施和永續採礦業的進步。定於2026年進行的反傾銷仲裁可望穩定國內價格。阿根廷的緊縮措施抑制了需求,但區域出口路線正在創造局部機會。

在中東和非洲地區,沙烏地阿拉伯的建築需求和南非在鉻鐵供應方面的主導地位相互交織。能源成本威脅冶煉廠的生產,但「2030願景」大型企劃支撐著對長條類產品的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 在脫碳背景下向電爐(EAF)和氫直接還原鐵(DRI)過渡。

- 擴大可再生能源相關設施(離岸風電、電解槽、氫氣管道)

- 數位化合金設計平台正在縮短合金牌號開發週期。

- 新興國家的基礎設施獎勵策略

- 由於電解槽和管道的建設,對綠色、耐氫鋼材的需求激增。

- 市場限制因素

- 加強高能耗製程和碳定價體系

- 採用輕金屬進行競爭性製造

- 關鍵礦產(鎳和鉻)供應鏈的波動性

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 不銹鋼

- 工具鋼

- 合金鋼

- 軸承鋼

- 碳鋼(特級)

- 按形式

- 板材

- 酒吧

- 桿

- 線圈

- 其他(鍛造產品、線材、鋼坯)

- 透過使用

- 汽車零件

- 航太結構和引擎

- 石油和天然氣設備

- 機器/工具

- 建築和基礎設施

- 能源與電力(渦輪機、核能、可再生能源)

- 其他用途(鐵路、醫療設備、國防)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Aperam SA

- ArcelorMittal

- China BaoWu Steel Group Corporation Limited

- CRS Holdings, LLC.

- Daido Steel Co., Ltd.

- Gerdau S/A

- JFE Steel Corporation

- JSW

- Nippon Steel Corporation

- Nucor Corporation

- Outokumpu

- POSCO

- Sandvik AB

- SSAB

- Tata Steel

- Thyssenkrupp Steel Europe

- United States Steel Corporation

- Vardhman Special Steels Limited

- Voestalpine Stahl GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the special steel market size is expected to grow from USD 244.32 billion in 2025 to USD 252.5 billion in 2026 and is forecast to reach USD 297.73 billion by 2031 at 3.35% CAGR over 2026-2031.

This report is Segmented by Product Type (Stainless Steel, Tool Steel, Alloy Steel, and More), Form (Sheets and Plates, Bars, Rods, Coils, and Others), Application (Automotive Components, Aerospace Structures and Engines, Machinery and Tools, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Special Steel Market Trends and Insights

Decarbonization Driven Switch To EAF And H2-DRI Routes

EAF and H2-DRI projects trim as much as 70% of site-level CO2 emissions compared with blast furnaces. SSAB expects fossil-free output from Oxelosund by 2026, while H2 Green Steel targets 5 million tons of green steel in Sweden by 2030. Capital intensity remains high at USD 1,200-1,500 per tonne of annual capacity, yet European Union (EU) carbon prices above EUR 90 per ton are accelerating payback periods. North American conversions, such as Algoma Steel's CAD 700 million program, align with automaker low-carbon sourcing mandates. Execution risk persists when hydrogen supply and renewable power lag project timelines, evidenced by Thyssenkrupp's delayed Duisburg transition.

Expansion Of Renewable-Energy Hardware

Offshore-wind, electrolyzer, and hydrogen-pipeline projects are widening end-use diversity for special steel market grades. The United States earmarked USD 42 billion for offshore-wind infrastructure, aiming for 30 GW by 2030, equating to 1.5-2.0 million tons of plate demand per year. EU's REPowerEU targets 300 GW of offshore wind by 2050, pulling 15-20 million tons of monopile and tower steel. Electrolyzer installations could reach 8 GW in 2026, with each gigawatt consuming around 4,000 tons of specialty stainless. API 5L X70/X80 pipe grades dominate hydrogen-transmission frameworks, and the European Hydrogen Backbone foresees 81,000 km of infrastructure by 2040.

Energy-Intensive Processes and Carbon Pricing

Blast-furnace steelmaking consumes 18-22 gigajoules per tonne of crude steel, and carbon-pricing mechanisms are escalating operating costs faster than mills can pass through to customers. European Union (EU) allowance prices over EUR 90 (USD 103) add around EUR 18-20 (USD 20-23) per tonne to integrated costs, while CBAM removes the low-cost import avenue by 2026. China's expanding carbon market and India's fear of border adjustments are pushing domestic producers toward EAF (Electric Arc Furnace) investment despite higher initial costs.

Other drivers and restraints analyzed in the detailed report include:

- Digitally Enabled Alloy-Design Platforms Shortening Grade-Development Cycles

- Infrastructure Stimulus In Emerging Economies

- Competition From Additive-Manufactured Lightweight Metals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Stainless steel's 35.22% share in 2025 underscores its corrosion-critical role in electrolyzer stacks and offshore structures. Indonesia's nickel-pig-iron surge and India's capacity expansion underpin a 3.67% CAGR to 2031. Tool steel demand is flattening as the additive share in tooling production hit 11% in 2023, pressuring traditional supplies.

Alloy steel maintains relevance for drivetrain and heavy-equipment parts, but electric-vehicle shifts favor lighter metals. Bearing steel innovation, such as NSK's high-speed EV axle unit, is pushing electroslag-remelted chemistries into mainstream auto supply. Nuclear programs, exemplified by Rosatom's BR-1200 grade, pull austenitic alloys into high-temperature service.

Geography Analysis

Asia-Pacific's 43.35% 2025 share stems from Chinese scale, Indian stimulus, and Indonesian nickel integration. China Baowu produced 131.85 million tons of crude steel in 2024 and pursues carbon-neutrality by 2050 through hydrogen metallurgy. India targets 300 million tons of capacity by 2030-31, supported by production-linked incentives that lower specialty-grade import reliance. ASEAN mills expand, though land and financing delays temper realization.

North America leverages scrap abundance and reshoring tailwinds. Nucor's USD 3.1 billion sheet mill and ArcelorMittal's USD 1 billion Calvert upgrade align with OEM (original equipment manufacturer) light-weighting programs. A pending Nippon Steel-US Steel tie-up would create a trans-Pacific specialty platform, while Gerdau's EBITDA now skews 62% to its U.S. network.

Europe faces the steepest decarbonization costs. SSAB will deliver fossil-free steel by 2026, and Outokumpu's ferrochrome integration buffers chromium volatility. Thyssenkrupp seeks partners as ETS prices pressure blast-furnace economics, and the UK's Port Talbot conversion demonstrates political support framed by job cuts.

South America hinges on Brazilian trade defenses and sustainable mining improvements. Anti-dumping rulings due 2026 may stabilize domestic pricing. Argentina's austerity curbs demand, though regional export channels open pockets of opportunity.

Middle East and Africa combine Saudi construction demand with South African ferrochrome supply dominance. Energy costs threaten smelter output, yet Vision 2030 megaprojects anchor long-product demand.

- Aperam S.A.

- ArcelorMittal

- China BaoWu Steel Group Corporation Limited

- CRS Holdings, LLC.

- Daido Steel Co., Ltd.

- Gerdau S/A

- JFE Steel Corporation

- JSW

- Nippon Steel Corporation

- Nucor Corporation

- Outokumpu

- POSCO

- Sandvik AB

- SSAB

- Tata Steel

- Thyssenkrupp Steel Europe

- United States Steel Corporation

- Vardhman Special Steels Limited

- Voestalpine Stahl GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Decarbonisation-driven switch to EAF and H2-DRI routes

- 4.2.2 Expansion of renewable-energy hardware (off-shore wind, electrolyser frames, and hydrogen pipelines)

- 4.2.3 Digitally enabled alloy-design platforms shortening grade-development cycles

- 4.2.4 Infrastructure stimulus in emerging economies

- 4.2.5 Surge in green-hydrogen-ready steels for electrolyser and pipeline build-out

- 4.3 Market Restraints

- 4.3.1 Energy-intensive processes and tightening carbon-pricing regimes

- 4.3.2 Competition from additive-manufactured light-weight metals

- 4.3.3 Supply-chain volatility in critical minerals (nickel and chromium)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Stainless Steel

- 5.1.2 Tool Steel

- 5.1.3 Alloy Steel

- 5.1.4 Bearing Steel

- 5.1.5 Carbon Steel (Special Grades)

- 5.2 By Form

- 5.2.1 Sheets and Plates

- 5.2.2 Bars

- 5.2.3 Rods

- 5.2.4 Coils

- 5.2.5 Others (Forgings, Wires, and Billets)

- 5.3 By Application

- 5.3.1 Automotive Components

- 5.3.2 Aerospace Structures and Engines

- 5.3.3 Oil and Gas Equipment

- 5.3.4 Machinery and Tools

- 5.3.5 Construction and Infrastructure

- 5.3.6 Energy and Power (Turbines, Nuclear, and Renewables)

- 5.3.7 Other Applications (Railways, Medical Devices, and Defense)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Aperam S.A.

- 6.4.2 ArcelorMittal

- 6.4.3 China BaoWu Steel Group Corporation Limited

- 6.4.4 CRS Holdings, LLC.

- 6.4.5 Daido Steel Co., Ltd.

- 6.4.6 Gerdau S/A

- 6.4.7 JFE Steel Corporation

- 6.4.8 JSW

- 6.4.9 Nippon Steel Corporation

- 6.4.10 Nucor Corporation

- 6.4.11 Outokumpu

- 6.4.12 POSCO

- 6.4.13 Sandvik AB

- 6.4.14 SSAB

- 6.4.15 Tata Steel

- 6.4.16 Thyssenkrupp Steel Europe

- 6.4.17 United States Steel Corporation

- 6.4.18 Vardhman Special Steels Limited

- 6.4.19 Voestalpine Stahl GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

特種鋼市場:按類型、產品形式、應用和分銷管道分類-2026-2032年全球市場預測

特種鋼市場:按類型、產品形式、應用和分銷管道分類-2026-2032年全球市場預測 全球特種鋼市場:機會與策略展望(至2035年)SBQ 運輸用鋼材市場按產品類型、形式、應用和最終用途分類,全球預測(2026-2032 年)SBQ鋼材市場依產品類型、製造流程、材質等級、應用及通路分類-2026年至2032年全球預測能源SBQ鋼材市場:按產品類型、產品形式、應用、鋼材等級和製造流程分類的全球預測,2026-2032年

全球特種鋼市場:機會與策略展望(至2035年)SBQ 運輸用鋼材市場按產品類型、形式、應用和最終用途分類,全球預測(2026-2032 年)SBQ鋼材市場依產品類型、製造流程、材質等級、應用及通路分類-2026年至2032年全球預測能源SBQ鋼材市場:按產品類型、產品形式、應用、鋼材等級和製造流程分類的全球預測,2026-2032年 特殊鋼:2025-2031年全球市佔率排名、總銷售額與需求預測

特殊鋼:2025-2031年全球市佔率排名、總銷售額與需求預測 美洲特種棒材優質鋼市場規模及預測(2021 - 2031 年)、區域佔有率、趨勢及成長機會分析報告範圍:按類型、應用和最終用途

美洲特種棒材優質鋼市場規模及預測(2021 - 2031 年)、區域佔有率、趨勢及成長機會分析報告範圍:按類型、應用和最終用途 特殊鋼筋 (SBQ) 的全球市場:市場佔有率及排行榜·整體銷售額及需求預測 (2025-2031年)

特殊鋼筋 (SBQ) 的全球市場:市場佔有率及排行榜·整體銷售額及需求預測 (2025-2031年) SBQ(特殊鋼棒)全球市場、績效及預測(2019-2030年)

SBQ(特殊鋼棒)全球市場、績效及預測(2019-2030年) 2022-2032 年全球特殊鋼市場規模研究(按產品、應用和區域預測)

2022-2032 年全球特殊鋼市場規模研究(按產品、應用和區域預測)