|

市場調查報告書

商品編碼

2062124

音訊串流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Audio Streaming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

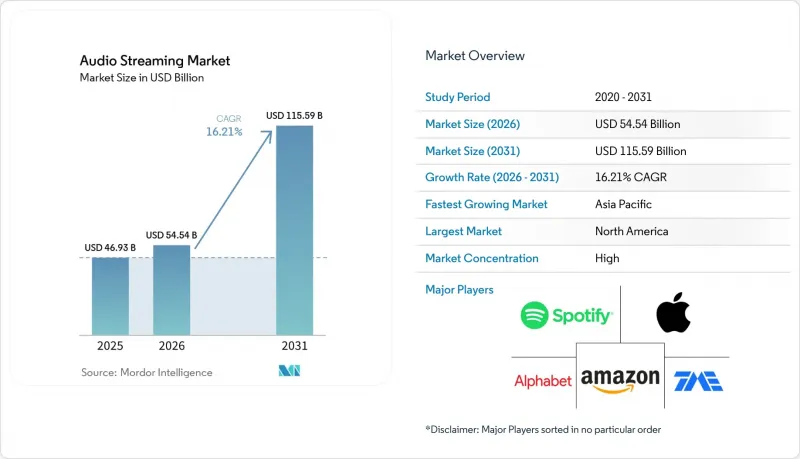

根據 Mordor Intelligence 預測,音訊串流媒體市場規模將從 2025 年的 469.3 億美元成長到 2026 年的 545.4 億美元,然後在 2031 年達到 1,155.9 億美元,2026 年至 2031 年的複合年成長率為 16.21%。

本報告按服務類型(點播、網路線上廣播等)、獲利模式(訂閱、廣告支援等)、平台/裝置(智慧型手機/平板電腦、桌上型電腦/筆記型電腦等)、內容(音樂、播客等)、最終用戶(個人消費者、與汽車製造商 (OEM) 的合作等)以及地區進行細分。市場預測以美元 (USD) 計價。

全球音訊串流媒體市場趨勢及洞察

最佳化新興市場的訂閱定價

在低收入市場調整訂閱價格,既能改善收入結構,又不會完全阻礙新用戶獲取,其影響遠不止於音頻串流媒體市場的銷售策略。 Spotify 於 2025 年 8 月將其在印度的付費方案價格提高了 17% 至 28%,但用戶數量仍持續成長。這表明,最忠實的聽眾對價格的敏感度並不像許多消費者模型所假設的那樣高。在串流媒體已經主導音樂消費市場的地區,這一趨勢更為顯著。根據國際唱片業協會 (IFPI) 的報告,2024 年中東和北非地區的錄製音樂收入年增 22.8%,其中串流媒體收入佔總收入的 99.5%。這意味著定價決策正在直接影響該地區的音樂市場貨幣化(IFPI)。 IFPI 也指出,撒哈拉以南非洲地區將成為 2025 年成長最快的音樂市場,營收將首次突破 1 億美元。這印證了區域定價不僅轉移了現有支出,而且還開啟了新的收入來源這一觀點。在音訊串流媒體市場,只要平台繼續調整其區域收費系統以適應行動寬頻的擴張,且跨境價格差異不會削弱區域定價結構,這種成長要素。

通訊業者(Telco)和OTT服務的商品搭售將促進付費服務的普及。

在通訊業者串流媒體市場,商品搭售正在降低訂閱門檻,它將串流服務整合到月度數據套餐中,而不是將其視為單獨購買項目。根據數位媒體協會 (DMA) 的報告,預計到 2025 年底,亞太地區將有超過 500 家 OTT通訊業者達成合作,這表明商品搭售已成為一種標準經營模式,而非實驗性模式。 Airtel 於 2025 年 2 月在其後付費和家庭 Wi-Fi 套餐中添加了 Apple Music,透過通訊業者管道將平台的覆蓋範圍擴展到大規模、價格最敏感的消費群體之一。 Angami 公佈了與中東和北非 16 個國家的 45 家通訊業者的合作,表明當地營運商也在利用商品搭售來保持其在與大規模全球服務商的競爭中的地位。這一點意義重大,因為透過商品搭售銷售訂閱的用戶往往比透過應用程式註冊訂閱的用戶更謹慎,不易解約率,從而提高了音訊串流媒體市場的客戶維繫,並降低了客戶流失率。

權利金比率通膨增速超過每位用戶平均收入成長率

版權費上漲是音訊串流媒體市場利潤成長最明顯的結構性限制因素之一。版權費率委員會 (CRB) 的 Web VI 決定將每次播放的版權費從 2026 年的 0.0021 美元提高到 0.0028 美元,並預計在 2030 年進一步提高到 0.0032 美元。數位媒體協會 (DMA) 表示,在現有框架下,平台已將其約 70% 的收入支付給版權所有者,這意味著在不提高價格或利潤率的情況下,平台幾乎沒有空間來消化更高的版權費率。這個問題在新興市場更為嚴重,儘管本地定價可以擴大目標客戶群,但往往無法快速提高每位用戶平均收入 (ARPU) 以跟上不斷上漲的版權費率。 2025 年 6 月,IMPALA 也警告稱,擬議的串流改革可能會導致版權收入集中在專注於目錄內容的版權所有者手中,這可能會增加那些依靠長尾內容實現差異化的平台的成本壓力。

細分市場分析

到2025年,點播音樂串流媒體將佔據音訊串流媒體市場78.20%的佔有率,並繼續保持其在該領域的主要收入來源地位。這一主導地位源於其龐大的曲庫、建議系統以及用戶重複收聽的習慣,這些因素共同支撐著大規模用戶群的月度經常性收入。此外,該服務還受益於長期的授權協議、完善的播放清單生態系統和社交共用功能,使得轉換服務。這些功能至關重要,因為音訊串流媒體市場仍然高度依賴可預測且重複的使用場景,而點播音樂仍然是與日常收聽聯繫最緊密的形式。同時,點播音樂不再是用戶參與度成長的唯一驅動力,因為其他音訊內容類別正在創造新的收聽機會和廣告空間。

受廣告需求以及創主導內容託管成本低於授權音樂的驅動,播客託管和分發市場預計到2031年將以19.60%的複合年成長率成長。到2026年,全球播客月度聽眾預計將達到6.19億,同期美國播客廣告市場年增31%。這顯示播客分發在音訊串流媒體市場中日益重要的戰略地位。 Spotify表示,在其有聲書業務發展的第二年,該公司聽眾年增36%,並在14個市場擁有超過50萬種有聲書。這印證了有聲書正在從單純的個人購買轉變為更廣泛的訂閱服務中一種新的互動方式的觀點。線上廣播、ASMR和冥想音訊繼續保持著穩定的聽眾群體,與標準的點播使用相比,它們提供了更長、更沉浸式的聆聽體驗。這意味著,儘管點播音樂仍然是服務模式經濟效益的商業性標桿,但音訊串流媒體產業正在逐步適應更廣泛的聆聽風格。

預計到2025年,音訊串流媒體市場中,訂閱模式將佔據63.10%的市場佔有率,這意味著付費用戶仍是各大平台的主要收入來源。這一模式仍受惠於大規模的付費會員群體,例如Spotify的2.93億付費用戶,以及生態系統的優勢——例如Apple Music等服務能夠與設備使用情況和帳戶ID緊密關聯。此外,由於訂閱收入比廣告收入更具可預測性,即使在成熟市場,各平台仍不斷嘗試定期漲價。這種模式之所以具有韌性,是因為忠實用戶將無廣告收聽、離線存取和豐富的音訊內容庫視為其核心價值提案。在音訊串流媒體市場,付費模式依然佔據中心地位,即便下一階段的成長不僅依賴新增訂閱用戶,也依賴廣告變現模式的改進。

預計到2031年,廣告支援模式將以17.80%的複合年成長率成長,成為音訊串流媒體市場成長最快的獲利管道。 IAB和普華永道的報告顯示,到2025年,數位音訊廣告市場規模將達到84億美元,年增10.2%。這表明,在海量收聽時長的推動下,獲利模式仍在不斷擴張。程序化廣告工具透過改善受眾定位、動態創新和跨裝置衡量,幫助平台更好地利用廣告資源,縮小了用戶使用時間長度與廣告收入之間長期存在的差距。混合型免費增值計畫繼續發揮至關重要的作用,降低了低收入市場的進入門檻,並為用戶逐步過渡到付費計畫提供了途徑。雖然按收費付費模式的市場佔有率仍然相對較小,但它在音頻串流媒體行業中保持著廣泛的定價結構,為那些不想每月訂閱的偶爾用戶提供了選擇。

區域分析

預計到2025年,北美將佔據音訊串流市場39.64%的佔有率,成為貢獻最大的區域市場。美國音樂批發市場預計將在2025年達到115.35億美元,付費串流訂閱用戶將增加至1.065億。這是自2022年以來最高的年度淨增幅,顯示即使在市場環境趨於成熟的情況下,該市場仍保持持續成長。該地區還擁有最強大的程式化音訊廣告基礎,各大平台在付費訂閱之外,進一步加強了免費收聽和播客的獲利能力。在加拿大,高寬頻普及率推動了加值服務的擴張;而在墨西哥,中產階級的壯大以及透過捆綁銷售實現的從免費內容到付費內容的轉變,正在推動市場發展。同時,SiriusXM和YouTube於2026年4月宣布的音訊廣告合作,顯示播客和廣播廣告空間正日益融入大規模的廣告銷售系統。此外,美國的版稅法規比許多其他地區更為重要,因為美國的版稅率的確定會影響整個音訊串流媒體市場的許可和定價趨勢。

亞太地區是音訊串流媒體市場成長最快的地區,預計到2031年複合年成長率將達到17.66%。騰訊音樂公佈2026年第一季營收為79億元人民幣(約11.5億美元),較去年同期成長7.3%。這表明,對本地平台和內容在地化的持續投入將繼續支撐其強勁成長。印度擁有超過8.12億行動寬頻用戶,隨著定價和方案計畫不斷適應收入水平,付費音訊服務仍擁有龐大的潛在客戶群。日本、韓國和澳洲仍然是高階市場,每個市場都有其獨特的內容偏好,因此需要在地化的編輯政策和建議模式。南美洲也持續成長,但各地區的成長速度有所不同。在巴西,網路普及率已達到84.3%,在自由裁量權收入有限的地區,像Claro Musica這樣的通訊業者的分發模式仍然發揮著至關重要的作用。

到2025年,歐洲仍將佔據相當大的市場佔有率,但其成長軌跡將呈現分化態勢,部分成長來自滲透率極高的西歐市場,另一部分則來自該地區內成長更為迅速的新興市場。 2024年,德國人均數位音樂支出年增18.7%,英國有聲書市場規模達2.68億英鎊(約3.41億美元)。這表明,消費者的付費意願正從音樂擴展到所有音訊格式。隱私法規正在重塑歐洲的獲利模式,更嚴格的導向標準迫使廣告支援的音訊平台轉向情境廣告。中東和非洲地區正成為音訊串流媒體市場日益重要的策略成長中心。沙烏地阿拉伯已撥款48億沙烏地里亞爾(約12.8億美元)用於2024年的娛樂產業發展。 Anghami預計2025會計年度營收將達9,930萬美元,年增27%。 Boomplay擁有1.45億首歌曲的龐大曲庫,協助西非成為內容分發中心。監管因素、豐富的本地內容以及對娛樂產業不斷成長的投資,都使得區域性專業機構的重要性持續凸顯,即便全球平台不斷擴張。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 新興市場訂閱費用合理化

- 通訊業者(Telco)和OTT服務的商品搭售正在促進付費服務的使用。

- 智慧音箱的部署數量正在迅速增加。

- 車載串流整合(OEM等級)

- AI語音DJ和生成式播放清單可以延長您的每日收聽時間。

- 基於區塊鏈的版稅支付方式正在吸引獨立唱片公司。

- 市場限制因素

- 用戶忠誠度成長速度超過了每位用戶平均收入 (ARPU) 的成長速度。

- 大型唱片公司的內容授權窗口策略

- 資料隱私法規限制了廣告定向投放

- 演算法發現偏差正在疏遠長尾內容創作者。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按服務類型

- 點播音樂串流

- 線上廣播

- 播客託管和分發

- 有聲書串流媒體

- 其他小眾音頻(ASMR、冥想)

- 透過貨幣化模式

- 基於訂閱

- 廣告收入

- 混合型免費增值模式

- 監聽收費

- 按平台/設備

- 智慧型手機和平板電腦

- 桌上型電腦/筆記型電腦

- 智慧音箱與家庭中心

- 聯網汽車

- 穿戴式裝置和其他物聯網設備

- 按內容類型

- 音樂

- podcast

- 有聲書

- 現場廣播

- 最終用戶

- 個人消費者

- 商業設施(零售、飯店)

- 與汽車製造商的整合

- 媒體和娛樂公司

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Spotify Technology SA

- Apple Inc.(Apple Music)

- Amazon.com Inc.(Amazon Music)

- Alphabet Inc.(YouTube Music)

- Tencent Music Entertainment Group

- Sirius XM Holdings Inc.(Pandora)

- SoundCloud Global Limited & Co. KG

- Deezer SA

- iHeartMedia Inc.

- KKBOX Inc.

- Anghami Plc

- JioSaavn LLC

- Gaana Media Private Ltd.

- Yandex NV(Yandex Music)

- NetEase Cloud Music Inc.

- Napster Group PLC

- TIDAL Music AS

- Qobuz SAS

- Boomplay Music Group

- Claro Musica(America Movil SAB de CV)

第7章 市場機會與未來展望

According to Mordor Intelligence, the audio streaming market size is expected to grow from USD 46.93 billion in 2025 to USD 54.54 billion in 2026 and is forecast to reach USD 115.59 billion by 2031 at 16.21% CAGR over 2026-2031.

This report is Segmented by Service Type (On-Demand, Live Internet Radio, and More), Monetization (Subscription-Based, Advertising-Supported, and More), Platform/Device (Smartphones and Tablets, Desktop/Laptop, and More), Content (Music, Podcasts, and More), End-User (Individual Consumers, Automotive OEM Integrations, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Audio Streaming Market Trends and Insights

Subscription Price Rationalization In Emerging Economies

Subscription price changes in lower-income markets are improving revenue mix without fully stopping user additions, which makes them more than a simple volume tactic in the audio streaming market. Spotify raised Premium pricing in India by 17-28% in August 2025, yet subscriber growth continued, which suggests that the most engaged listener groups were less price sensitive than many consumer models assumed. The same pattern matters even more in regions where streaming already dominates the listening economy. IFPI reported that recorded music revenue in the Middle East and North Africa grew 22.8% year over year in 2024, with streaming accounting for 99.5% of total revenue, which means pricing decisions directly shape category monetization in that region IFPI.ORG.IFPI also stated that Sub-Saharan Africa was the fastest-growing music market in 2025 and crossed USD 100 million in revenue for the first time, which supports the view that localized pricing is opening new revenue pools instead of just shifting existing spending. For the audio streaming market, this driver stays durable as long as platforms keep regional tiers aligned with mobile broadband expansion and keep cross-border arbitrage from weakening local price structures.

Telco-OTT Bundling Pushes Paid Uptake

Telco bundling is reducing the friction of subscription adoption by placing streaming inside monthly connectivity plans instead of treating it as a separate purchase in the audio streaming market. The Digital Media Association reported more than 500 OTT-operator partnerships across Asia-Pacific by the end of 2025, which shows that bundling had become a standard commercial route rather than a trial model. Airtel added Apple Music to its postpaid and home Wi-Fi plans in February 2025, which extended the platform's reach through an operator channel in one of the most price-sensitive large consumer bases. Anghami disclosed partnerships with 45 telecom operators across 16 Middle East and North Africa countries, showing that local specialists are also using bundling to defend their position against larger global services. This matters because bundled users usually face a more deliberate cancellation step than app-based sign-ups, and that tends to improve retention and lower voluntary churn over time in the audio streaming market.

Royalty-Rate Inflation Exceeding ARPU Growth

Royalty inflation is one of the clearest structural limits on profit expansion in the audio streaming market. The Copyright Royalty Board's Web VI determination raised the per-performance mechanical rate from USD 0.0021 under Web V to USD 0.0028 in 2026 and set a path to USD 0.0032 by 2030. The Digital Media Association stated that platforms already remit around 70% of revenue to rights holders under existing frameworks, which means there is limited room to absorb higher rates without price action or margin pressure. The problem is sharper in emerging markets, where localized pricing can expand the addressable base but often cannot raise ARPU fast enough to match the speed of royalty increases. IMPALA also warned in June 2025 that streaming reform proposals could steer more royalty flows toward catalog-heavy rights owners, which may deepen cost pressure for platforms that rely on long-tail content to differentiate.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Smart Speaker Install Base Expansion

- OEM-Level In-Car Streaming Integrations

- Content-License Windowing By Major Labels

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-demand music streaming held 78.20% of the audio streaming market share in 2025, which kept it as the core revenue engine for the category. That lead came from catalog depth, recommendation systems, and repeat listening habits that support monthly recurring revenue across large subscriber bases. The service also benefits from long-established licensing relationships, playlist ecosystems, and social sharing features that make switching less effortless than it appears at first glance. Those features matter because the audio streaming market still depends heavily on predictable, repeat use cases, and on-demand music remains the format most closely tied to everyday listening. At the same time, the segment is no longer the only driver of engagement growth because adjacent spoken-audio categories are adding new listening occasions and ad inventory.

Podcast hosting and distribution is projected to grow at a 19.60% CAGR through 2031, helped by advertising demand and the lower marginal cost of hosting creator-led content versus licensed music. Global monthly podcast listenership reached 619 million in 2026, and the United States podcast advertising market expanded 31% year over year in the same period, showing why podcast distribution is gaining strategic weight inside the audio streaming market. Spotify said audiobook listeners rose 36% year over year in the service's second year in that category, with a catalog that exceeded 500,000 titles across 14 markets, which supports the view that audiobooks are becoming an added engagement layer inside broader subscriptions rather than a separate purchase decision. Live internet radio, ASMR, and meditation audio still retain dedicated audiences whose sessions are often longer and more ambient than standard on-demand use. That means the audio streaming industry is gradually supporting more listening modes, even though on-demand music still sets the commercial baseline for service type economics.

Subscription-based monetization held 63.10% share of the audio streaming market size in 2025, which shows that recurring paid access remained the main cash foundation across leading platforms. This structure is still supported by large premium bases, including Spotify's 293 million premium subscribers, and by ecosystem advantages that help services like Apple Music stay closely tied to device usage and account identity. Subscription revenue also remains easier to forecast than advertising income, which is why platforms continue testing periodic price increases even in mature markets. The model has resilience because highly engaged users treat ad-free listening, offline access, and broader content libraries as part of the core value proposition. In the audio streaming market, this keeps paid tiers central even as the next phase of growth is coming from improved ad monetization rather than only new subscriptions.

The advertising-supported model is forecast to grow at a 17.80% CAGR through 2031, making it the fastest-growing monetization path in the audio streaming market. IAB and PwC reported that digital audio advertising grew 10.2% to USD 8.4 billion in 2025, which shows that monetization is still rising against a very large base of listening time. Programmatic tools are helping platforms make that inventory more usable through audience targeting, dynamic creative, and better cross-device measurement, which narrows the long-standing gap between time spent and ad spend capture. Hybrid freemium tiers still matter because they reduce entry barriers in lower-income markets and create a funnel into paid plans over time. Pay-per-listen models remain smaller, but they preserve a place for occasional users who want access without a monthly commitment, which keeps pricing architecture broad in the audio streaming industry.

Geography Analysis

North America held 39.64% share of the audio streaming market in 2025, which made it the largest regional contributor. The United States wholesale recorded music market reached USD 11.535 billion in 2025, and paid streaming subscriptions rose to 106.5 million, the strongest net annual intake since 2022, showing that growth continued even in a mature environment. The region also has the deepest programmatic audio advertising base, which gives leading platforms a stronger ability to monetize free listening and podcasts alongside paid subscriptions. Canada supports premium uptake through high broadband penetration, while Mexico is benefiting from middle-class expansion and bundle-led conversion from free to paid listening. In parallel, the SiriusXM and YouTube audio advertising arrangement announced in April 2026 points to a market where podcast and radio inventory is being drawn more tightly into large-scale ad sales infrastructure. Royalty regulation also matters more here than in many other regions because the United States rate decisions can influence broader licensing and pricing behavior across the audio streaming market.

Asia-Pacific is the fastest-growing region in the audio streaming market, with a projected CAGR of 17.66% through 2031. Tencent Music reported revenue of CNY 7.90 billion (USD 1.15 billion), in Q1 2026, up 7.3% year over year, showing that local platform investment and content localization are still supporting strong expansion. India's mobile broadband base exceeded 812 million subscriptions, which leaves a large addressable audience for paid audio as pricing and bundling continue to adapt to income realities. Japan, South Korea, and Australia remain premium markets, but each has distinct content preferences that require localized editorial decisions and recommendation models. South America is growing as well, though unevenly, with Brazil supported by 84.3% internet penetration and operator-led distribution models such as Claro Musica still important where discretionary spending is tighter.

Europe held a significant share in 2025, but its growth profile is split between highly penetrated Western markets and faster-expanding emerging parts of the region. Germany's household digital music spending rose 18.7% year over year in 2024, and the United Kingdom audiobook segment reached GBP 268 million (USD 341 million), which shows that willingness to pay is widening across audio formats rather than staying limited to music. Privacy rules are reshaping monetization in Europe because tighter targeting standards are pushing platforms toward contextual advertising methods for ad-supported audio. Middle East and Africa is becoming a more strategic growth pocket in the audio streaming market, with Saudi Arabia allocating SAR 4.8 billion (USD 1.28 billion), toward entertainment development in 2024, Anghami reporting FY2025 revenue of USD 99.3 million with 27% year-over-year growth, and Boomplay's 145-million-track catalog helping position West Africa as a content origination hub. This combination of regulation, local content depth, and rising entertainment investment means regional specialists still have room to hold meaningful ground even as global platforms expand.

- Spotify Technology S.A.

- Apple Inc. (Apple Music)

- Amazon.com Inc. (Amazon Music)

- Alphabet Inc. (YouTube Music)

- Tencent Music Entertainment Group

- Sirius XM Holdings Inc. (Pandora)

- SoundCloud Global Limited & Co. KG

- Deezer S.A.

- iHeartMedia Inc.

- KKBOX Inc.

- Anghami Plc

- JioSaavn LLC

- Gaana Media Private Ltd.

- Yandex N.V. (Yandex Music)

- NetEase Cloud Music Inc.

- Napster Group PLC

- TIDAL Music AS

- Qobuz SAS

- Boomplay Music Group

- Claro Musica (America Movil S.A.B. de C.V.)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Subscription Price Rationalization in Emerging Economies

- 4.2.2 Telco-OTT Bundling Pushes Paid Uptake

- 4.2.3 Rapid Smart Speaker Install Base Expansion

- 4.2.4 OEM-Level In-Car Streaming Integrations

- 4.2.5 AI Voice DJ and Generative Playlists Extend Daily Listening Time

- 4.2.6 Blockchain-Based Royalty Settlement Attracts Independent Catalogs

- 4.3 Market Restraints

- 4.3.1 Royalty-Rate Inflation Exceeding ARPU Growth

- 4.3.2 Content-License Windowing by Major Labels

- 4.3.3 Data-Privacy Regulations Limiting Ad-Targeting

- 4.3.4 Algorithmic Discovery Bias Marginalizing Long-Tail Creators

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 On-Demand Music Streaming

- 5.1.2 Live Internet Radio

- 5.1.3 Podcast Hosting and Distribution

- 5.1.4 Audiobook Streaming

- 5.1.5 Other Niche Audio (ASMR, Meditation)

- 5.2 By Monetization Model

- 5.2.1 Subscription-Based

- 5.2.2 Advertising-Supported

- 5.2.3 Hybrid Freemium

- 5.2.4 Pay-Per-Listen

- 5.3 By Platform/Device

- 5.3.1 Smartphones and Tablets

- 5.3.2 Desktop/Laptop

- 5.3.3 Smart Speakers and Home Hubs

- 5.3.4 Connected Cars

- 5.3.5 Wearables and Other IoT

- 5.4 By Content Type

- 5.4.1 Music

- 5.4.2 Podcasts

- 5.4.3 Audiobooks

- 5.4.4 Live Radio Streams

- 5.5 By End-User

- 5.5.1 Individual Consumers

- 5.5.2 Commercial Venues (Retail, Hospitality)

- 5.5.3 Automotive OEM Integrations

- 5.5.4 Media and Entertainment Enterprises

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Spotify Technology S.A.

- 6.4.2 Apple Inc. (Apple Music)

- 6.4.3 Amazon.com Inc. (Amazon Music)

- 6.4.4 Alphabet Inc. (YouTube Music)

- 6.4.5 Tencent Music Entertainment Group

- 6.4.6 Sirius XM Holdings Inc. (Pandora)

- 6.4.7 SoundCloud Global Limited & Co. KG

- 6.4.8 Deezer S.A.

- 6.4.9 iHeartMedia Inc.

- 6.4.10 KKBOX Inc.

- 6.4.11 Anghami Plc

- 6.4.12 JioSaavn LLC

- 6.4.13 Gaana Media Private Ltd.

- 6.4.14 Yandex N.V. (Yandex Music)

- 6.4.15 NetEase Cloud Music Inc.

- 6.4.16 Napster Group PLC

- 6.4.17 TIDAL Music AS

- 6.4.18 Qobuz SAS

- 6.4.19 Boomplay Music Group

- 6.4.20 Claro Musica (America Movil S.A.B. de C.V.)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

音訊串流媒體市場規模、佔有率和成長分析:按串流內容格式、獲利模式、裝置存取平台、最終用戶群和地區分類-2026-2033年產業預測

音訊串流媒體市場規模、佔有率和成長分析:按串流內容格式、獲利模式、裝置存取平台、最終用戶群和地區分類-2026-2033年產業預測 音訊會議服務市場:按服務類型、最終用戶和地區分類

音訊會議服務市場:按服務類型、最終用戶和地區分類 2026年全球語音會議服務市場報告2026年全球電話會議服務市場報告

2026年全球語音會議服務市場報告2026年全球電話會議服務市場報告 全球音訊串流媒體市場規模、佔有率、趨勢和成長分析報告(2026-2034)Frost Radar:《歐洲統一通訊即服務 (UCaaS) 與雲端連線呼叫服務,2025 年》

全球音訊串流媒體市場規模、佔有率、趨勢和成長分析報告(2026-2034)Frost Radar:《歐洲統一通訊即服務 (UCaaS) 與雲端連線呼叫服務,2025 年》 音訊會議服務市場規模、佔有率和成長分析(按部署類型、產品類型、公司規模、行業垂直領域和地區分類)—產業預測(2026-2033 年)全球音訊會議設備市場,2024-2031年

音訊會議服務市場規模、佔有率和成長分析(按部署類型、產品類型、公司規模、行業垂直領域和地區分類)—產業預測(2026-2033 年)全球音訊會議設備市場,2024-2031年 音訊會議市場

音訊會議市場 音訊串流媒體市場規模、佔有率、趨勢分析報告:按格式、設備、平台、服務、地區、細分預測,2025-2030 年

音訊串流媒體市場規模、佔有率、趨勢分析報告:按格式、設備、平台、服務、地區、細分預測,2025-2030 年