|

市場調查報告書

商品編碼

2062121

除鏽劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Rust Remover - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

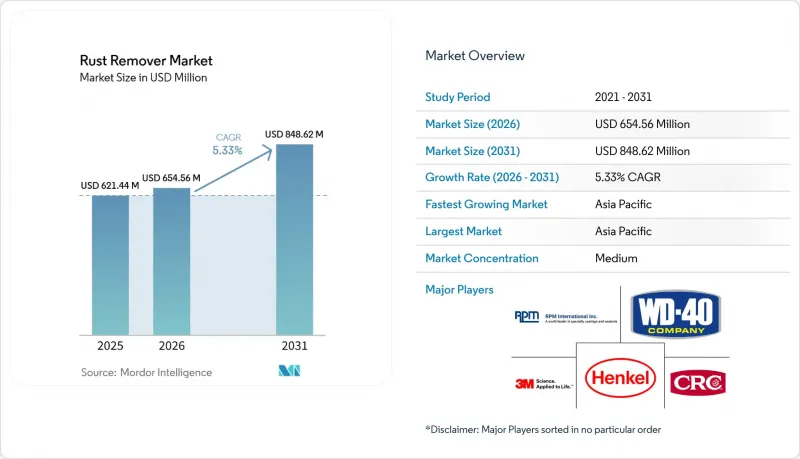

根據 Mordor Intelligence 預測,除鏽劑市場規模將從 2025 年的 6.2144 億美元成長到 2026 年的 6.5456 億美元,到 2031 年達到 8.4862 億美元,2026 年至 2031 年的複合年成長率為 5.33%。

本報告按類型(酸性除鏽劑、中性pH/螯合型除鏽劑、生物基除鏽劑)、劑型(液體、凝膠、噴霧劑、擦拭巾)、終端用戶行業(汽車、建築、工業機械設備等)和地區(亞太地區、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元計價。

全球除鏽劑市場趨勢及洞察

新興國家製造業擴張與基礎建設發展

印度、越南、印尼和墨西哥的工業擴張正在推動預防性表面處理市場的成長。在印度,公路、地鐵和港口工程強制要求對鋼筋和梁進行防腐蝕處理。這使得建築工地對適用於行動噴塗設備的濃縮液的需求持續成長。在越南,電子工廠正在採用聚脲屏障來抵禦鹽霧侵蝕。然而,在定期停機期間,仍需要進行化學除鏽。鑑於該地區嚴重的腐蝕相關損失對經濟的影響,這一點至關重要。在墨西哥,近岸外包的趨勢正在推動工具和模具維護需求的成長。同時,在巴西,對國產農業機械的稅收優惠政策導致維修店大量囤積凝膠產品。這些凝膠的優勢在於它們能夠很好地黏附在大型鑄件上而不會流淌。這些趨勢共同推動了除鏽劑市場的發展,並確保即使在商品價格下跌時期,銷售量能保持成長。

推動對低揮發性有機化合物和生物基化學品的監管。

2025年1月,美國環保署(EPA)推出了新的氣霧劑塗料法規。這些法規限制了除鏽劑的產品加權反應活性,並要求如果揮發性有機化合物(VOC)含量超過特定閾值,則必須進行電子揭露。許多傳統的碳氫化合物載體變得不再實用,因為未列出溶劑成分將自動招致巨額罰款。同時,源自玉米和木薯糖的檸檬酸基體係可以達到類似的除氧化皮效果。這些系統產生的煙霧很少,並且與黃原膠混合後,可形成不滴落的凝膠,適用於垂直表面的單層塗覆。同時,歐盟化學品註冊、評估、授權和限制(REACH)法規以及中國生態環境部的更嚴格規定,正給全球供應商帶來更大的壓力。供應商正日益轉向能夠滿足不同司法管轄區要求的統一配方組合。這種轉變正在重塑競爭格局。如今,可靠的分析報告、對揮發性有機化合物的細緻追蹤以及獲取生物基原料與每公升的價格同樣重要。

機械和塗層替代方案

粉末塗裝製程不排放揮發性有機化合物 (VOC),幾乎不產生廢棄物,因此正擴大應用於電動車電池機殼。這一轉變促使汽車製造商摒棄傳統的除鏽和重新噴漆的順序工藝。阿克蘇諾貝爾公司對製造商的調查顯示,相當多的電動車製造商現在指定使用粉末塗裝,其採用率略高於整個汽車行業的平均水平。 PlasmaTreat 公司的「AntiCorr」是一種等離子增強轉化塗層,它完全避免了傳統的化學浴,直接形成一層薄薄的矽氧烷層。隨著鍍鋅鋼和鋁材的廣泛應用,曾經是除鏽市場核心的裸金屬表面庫存正在減少,市場基準銷售量也正在萎縮。

細分市場分析

2025年,酸性除鏽劑的銷售額佔比達到52.12%,但傳統方法仍是常規維護手冊的基礎,適用於去除厚鏽。另一方面,由於環境法規的日益嚴格,合規成本不斷上升,促使買家轉向獲得美國農業部(USDA)生物基認證的檸檬酸基除鏽系統。預計2026年至2031年間,生物基除鏽解決方案的複合年成長率將達5.81%。航太維修基地由於擔心氫脆問題,正在逐步擴大其在除鏽劑市場的佔有率。儘管中性pH螯合劑仍處於小眾市場,但在文化遺產保護和電子組裝領域,由於對金屬表面精度要求較高,其反應速度較慢的缺點被彌補,因此獲得了高利潤的合約。

在預測期內,除鏽劑中螯合劑的市場規模預計將穩定成長,儘管基數小規模。雖然酸性產品在重型設備維修領域仍佔據主導地位,但隨著額外個人防護設備、排煙設施和危險廢棄物處理成本在投標比較中逐漸顯現,總競標成本 (TCO) 的差距正在縮小。供應商目前提供混合套裝,將酸性預清洗與螯合劑精處理相結合,以平衡性能和法規遵從性,從而加速行業從完全依賴強酸的方法向其他方法的轉變。

區域分析

預計到2025年,亞太地區將佔全球銷售額的45.12%,並在2026年至2031年間以6.11%的複合年成長率成長。在中國,採用焊接和電塗裝塗裝之間在線噴塗磷化處理的汽車生產線每天都會消耗大量的化學品。即使少量轉向使用生物酸,也會導致化學品用量增加。在印度,Bharatmala高速公路走廊的承包商正在指定防銹處理方案,以符合印度公路運輸部部的指導方針,因為該高速公路的每個路段都使用大量的鋼筋。在越南,腐蝕造成的損失是一個重大的經濟負擔,海事領域對中性pH凝膠的需求日益成長。這些凝膠可以減少船體維護期間的潛水作業時間。同時,東協提供的優惠性外國直接投資激勵措施正在吸引零件供應商。這些供應商正在採用低揮發性有機化合物(VOC)液體,為出口歐洲做準備,並促進跨區域配方協調。

在北美,美國環保署(EPA)強制推行的電子報告製度正推動檸檬酸、葡萄糖酸和其他弱酸的市佔率成長。在墨西哥灣,海上設施拆除競標中需要考慮全生命週期排放,這導致螯合劑的需求增加,即使其每公升價格更高。此外,美國日益盛行的DIY文化也透過社群媒體上發布的防鏽技巧影片,推動了週末零售的成長。

儘管歐洲市場已趨於成熟,但仍高度重視循環經濟指標。 《塗料技術與研究期刊》的一項研究表明,專案支出中有相當一部分與健康、安全和環境 (HSE) 相關。這一趨勢促使業主轉向更耐用、維護成本更低的塗料,從而減少維護次數。能夠同時提供防鏽和防閃光保護的供應商正在獲得競爭優勢,而能夠減少一次支架搭建週期在歐盟競標中是一項顯著優勢。

南美洲、中東和非洲的市場佔有率雖小,但成長迅速。在巴西,大豆收割者面臨腐蝕性化肥粉塵帶來的挑戰。同時,在沙烏地阿拉伯,海水淡化廠需要在高鹽度環境中處理不銹鋼管路。儘管政治風險和外匯波動使得預測變得困難,但本地混合廠的出現提供了解決方案。這些工廠降低了進口關稅和前置作業時間,為反應敏捷的企業帶來了額外的優勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 新興國家的製造業擴張與基礎建設維修

- 透過法規促進低揮發性有機化合物和生物基化學品的發展

- 對已退役的海上油氣平台維修

- 綠氫電解槽組件的預購需求

- 在智慧工廠中引入基於機器人/雷射的線上除鏽技術

- 市場限制因素

- 機械和塗層替代方案

- 磷酸和檸檬酸鹽供應的地緣政治波動

- 微刷和乾冰清洗技術的興起

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 酸性除鏽劑

- 中性pH值/螯合除鏽劑

- 生物基除鏽劑

- 按形式

- 液體

- 凝膠

- 噴

- 擦拭巾

- 按最終用戶行業分類

- 車

- 建造

- 海上

- 工業機械和設備

- 家庭/消費者

- 航太

- 石油和天然氣

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Advanced Protective Technologies, LLC.

- AkzoNobel NV

- BASF

- Capella Solutions Group

- Chempace

- CRC Industries

- Fuchs Petrolub SE

- GUNK

- Henkel AG & Co. KGaA

- JENOLITE

- Kao Corporation

- Permatex

- Rodda Paint, Co.

- RPM International Inc

- Star brite Inc.

- Turtle Wax Inc.

- WD-40

- Zep Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the rust remover market size is expected to increase from USD 621.44 million in 2025 to USD 654.56 million in 2026 and reach USD 848.62 million by 2031, growing at a CAGR of 5.33% over 2026-2031.

This report is Segmented by Type (Acid-Based Rust Removers, Neutral PH/Chelate-Based Rust Removers, and Bio-Based Rust Removers), Form (Liquid, Gel, Spray, and Wipes), End-User Industry (Automotive, Construction, Industrial Machinery and Equipment, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Rust Remover Market Trends and Insights

Expansion of Manufacturing and Infrastructure Rehabilitation in Emerging Economies

Industrial expansions in India, Vietnam, Indonesia, and Mexico are broadening the market for preventive surface treatments. In India, highway, metro, and port projects mandate corrosion protection for steel rebar and girders. This creates a consistent demand for liquid concentrates compatible with mobile spray rigs at job sites. Vietnam's electronics hubs deploy polyurea barriers to combat salt-laden humidity. However, they still require chemical rust removal during scheduled shutdowns. This is crucial, considering the region faces significant corrosion-related losses impacting its economy. In Mexico, the trend of near-shoring boosts the demand for tooling and mold maintenance. Meanwhile, in Brazil, tax incentives for domestically produced farming equipment ensure repair shops are well-stocked with gel products. These gels are particularly advantageous as they adhere to large castings without runoff. Together, these trends are strengthening the rust removers market, ensuring volume growth even amidst softening commodity prices.

Regulatory Push Toward Low-VOC and Bio-Based Chemistries

In January 2025, the United States Environmental Protection Agency introduced a new aerosol-coatings rule. This rule limits the product-weighted reactivity for rust converters and requires any volatile organic compound present above a certain threshold to be disclosed electronically. If a solvent is not listed, it automatically incurs a significant penalty, making many traditional hydrocarbon carriers impractical. On the other hand, citric-acid systems, derived from corn or cassava sugar, can achieve similar mill-scale removal. These systems produce minimal fumes and, when combined with xanthan gum, create drip-resistant gels suitable for a single vertical coat application. Meanwhile, tightening regulations under the European Union's Registration, Evaluation, Authorization, and Restriction of Chemicals and China's Ministry of Ecology and Environment standards further push global suppliers. They are increasingly moving towards unified formula portfolios that can meet the demands of various jurisdictions. This shift is reshaping the competitive landscape: now, having robust analytical reporting, meticulous volatile organic compound tracking, and access to biobased feedstocks are just as vital as pricing per liter.

Mechanical and Coating-Based Substitutes

Electric-vehicle battery enclosures are increasingly opting for powder coatings, which offer a zero-volatile organic compound application and generate nearly zero waste. This shift is enticing original equipment manufacturers to move away from traditional methods of sequential rust removal and repainting. A survey by AkzoNobel, encompassing manufacturers, revealed that a significant portion of electric vehicle producers now specify powder coatings, slightly outpacing the adoption rate seen in the broader automotive sector. Plasmatreat's AntiCorr, a plasma-enhanced conversion coating, directly applies thin siloxane layers, completely sidestepping traditional chemical baths. With the growing adoption of galvanized steel and aluminum, the once-dominant inventory of bare ferrous surfaces central to the rust removers market has diminished, eroding the market's baseline volume.

Other drivers and restraints analyzed in the detailed report include:

- Refurbishment of Decommissioned Offshore Oil and Gas Platforms

- Pre-Treatment Demand for Green-Hydrogen Electrolyzer Components

- Geopolitical Volatility in Phosphoric and Citric Acid Supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acid-Based Rust Removers maintained a 52.12% slice of 2025 revenue, while traditional methods anchor legacy maintenance manuals and facilitate heavy-scale removal, rising compliance costs tied to environmental regulations are steering buyers towards citric systems, proudly boasting a certification as fully biobased by the United States Department of Agriculture. Bio-based solutions are projected to expand at 5.81% CAGR between 2026 and 2031. Aerospace maintenance depots, wary of hydrogen embrittlement, are progressively boosting their share of the rust removers market. While still a niche, neutral-pH chelates are securing high-margin contracts in heritage preservation and electronics assembly, where the need for bare-metal precision compensates for their slower kinetics.

Over the forecast period, the market for chelate formulations in rust removers is projected to grow steadily, albeit from a modest base. While acid products continue to dominate heavy machinery refurbishment, the visible costs of additional personal protective equipment, fume extraction, and hazardous waste management are becoming evident in bid comparisons, tightening total cost of ownership gaps. Suppliers are now offering hybrid kits, combining acid pre-wash with chelate polish, to balance performance with regulatory comfort, easing the industry's shift away from a strong-acid-only approach.

Geography Analysis

Asia-Pacific accounted for 45.12% of 2025 revenue and is on track for a 6.11% CAGR between 2026 and 2031. Chinese automotive production lines, which employ inline spray phosphates between welding and e-coating, drain significant volumes daily. Even a small shift towards bio-acids leads to an increase in volume. In India, contractors on the Bharatmala highway corridors, which use large amounts of reinforcing bar per stretch, specify rust treatments to align with the Ministry of Road Transport guidelines. Vietnam, dealing with substantial corrosion losses as a share of its economy, witnesses growing demand in its maritime sector for neutral-pH gels. These gels reduce diver time during hull maintenance. Meanwhile, foreign direct investment incentives from the Association of Southeast Asian Nations attract component suppliers. By adopting low-volatile organic compound liquids, these suppliers position themselves for European exports, advancing cross-regional formulation harmonization.

In North America, the Environmental Protection Agency's electronic-reporting mandate shifts market shares towards citric, gluconic, and other benign acids. Offshore decommissioning bids in the Gulf of Mexico now account for total lifecycle emissions, driving up chelate demands, even at a higher per-liter cost. Furthermore, a strong do-it-yourself culture in the United States sees social-media rust-hack videos translating into active weekend retail sales.

Europe, despite its maturity, remains focused on circular-economy metrics. A study from the Journal of Coatings Technology and Research pointed out that health, safety, and environmental access expenses dominate project spending. This trend nudges asset owners towards durable, low-maintenance coatings that reduce intervention frequency. Suppliers who offer rust removal alongside flash-inhibition gain a competitive edge, saving an extra scaffold cycle a significant advantage in European Union bidding.

While South America and the Middle-East and Africa command smaller market shares, they exhibit areas of rapid growth. In Brazil, soy harvesters face challenges with corrosive fertilizer dust. Meanwhile, in Saudi Arabia, desalination plants manage high-salinity stainless piping. Although political risks and currency fluctuations complicate forecasting, the emergence of localized blending plants offers a solution. These plants reduce import duties and lead times, granting nimble players incremental advantages.

- 3M

- Advanced Protective Technologies, LLC.

- AkzoNobel NV

- BASF

- Capella Solutions Group

- Chempace

- CRC Industries

- Fuchs Petrolub SE

- GUNK

- Henkel AG & Co. KGaA

- JENOLITE

- Kao Corporation

- Permatex

- Rodda Paint, Co.

- RPM International Inc

- Star brite Inc.

- Turtle Wax Inc.

- WD-40

- Zep Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of manufacturing and infrastructure rehab in emerging economies

- 4.2.2 Regulatory push toward low-VOC and bio-based chemistries

- 4.2.3 Refurbishment of decommissioned offshore oil and gas platforms

- 4.2.4 Pre-treatment demand for green-hydrogen electrolyzer components

- 4.2.5 Robotic/laser in-line rust-removal adoption in smart factories

- 4.3 Market Restraints

- 4.3.1 Mechanical and coating-based substitutes

- 4.3.2 Geopolitical volatility in phosphoric/citric acid supply

- 4.3.3 Rise of micro-abrasive and dry-ice cleaning technologies

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Acid-Based Rust Removers

- 5.1.2 Neutral pH/Chelate-Based Rust Removers

- 5.1.3 Bio-Based Rust Removers

- 5.2 By Form

- 5.2.1 Liquid

- 5.2.2 Gel

- 5.2.3 Spray

- 5.2.4 Wipes

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Construction

- 5.3.3 Marine

- 5.3.4 Industrial Machinery and Equipment

- 5.3.5 Household/Consumer

- 5.3.6 Aerospace

- 5.3.7 Oil and Gas

- 5.3.8 Others

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Advanced Protective Technologies, LLC.

- 6.4.3 AkzoNobel NV

- 6.4.4 BASF

- 6.4.5 Capella Solutions Group

- 6.4.6 Chempace

- 6.4.7 CRC Industries

- 6.4.8 Fuchs Petrolub SE

- 6.4.9 GUNK

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 JENOLITE

- 6.4.12 Kao Corporation

- 6.4.13 Permatex

- 6.4.14 Rodda Paint, Co.

- 6.4.15 RPM International Inc

- 6.4.16 Star brite Inc.

- 6.4.17 Turtle Wax Inc.

- 6.4.18 WD-40

- 6.4.19 Zep Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

全球工業清潔劑市場規模、佔有率、趨勢及成長分析報告(2026-2034年)

全球工業清潔劑市場規模、佔有率、趨勢及成長分析報告(2026-2034年) 工業清洗市場:2026-2032年全球市場預測(依產品、操作、應用、最終用戶產業及銷售管道分類)清潔劑與脫脂劑售後市場:依產品類型、劑型、應用、終端用戶產業、通路分類,全球預測(2026-2032年)生物清潔劑市場:依產品類型、劑型、應用、最終用戶和銷售管道分類-2026-2032年全球預測

工業清洗市場:2026-2032年全球市場預測(依產品、操作、應用、最終用戶產業及銷售管道分類)清潔劑與脫脂劑售後市場:依產品類型、劑型、應用、終端用戶產業、通路分類,全球預測(2026-2032年)生物清潔劑市場:依產品類型、劑型、應用、最終用戶和銷售管道分類-2026-2032年全球預測 工業脫脂劑市場報告:按類型、等級、應用和地區分類(2026-2034年)

工業脫脂劑市場報告:按類型、等級、應用和地區分類(2026-2034年) 全球無塑膠清潔劑市場:市場規模、佔有率和趨勢分析(按形態、成分、最終用途和地區分類),細分市場預測(2026-2033 年)全球水性脫脂劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球煉油廠清洗化學品市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球無塑膠清潔劑市場:市場規模、佔有率和趨勢分析(按形態、成分、最終用途和地區分類),細分市場預測(2026-2033 年)全球水性脫脂劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球煉油廠清洗化學品市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球工業洗碗機市場報告2026年全球工業脫脂劑市場報告

2026年全球工業洗碗機市場報告2026年全球工業脫脂劑市場報告