|

市場調查報告書

商品編碼

2062100

五氯酚:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Pentachlorophenol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

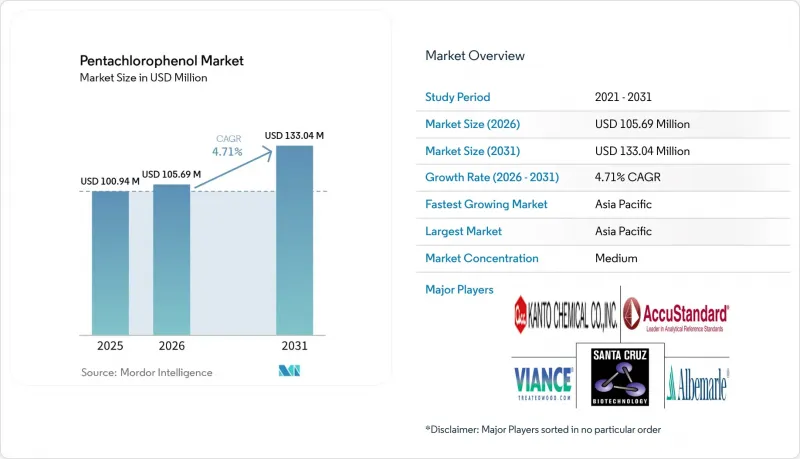

根據 Mordor Intelligence 預測,五氯酚市場規模將從 2025 年的 1.0094 億美元和 2026 年的 1.0569 億美元成長到 2031 年的 1.3304 億美元,2026 年至 2031 年的複合年成長率的 1.3304 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 4.71%。

本報告按等級(工業級和分析級)、應用(木材防腐劑、殺蟲劑和除草劑等)、終端用戶行業(建築、發電等)以及地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲)進行細分。市場預測以美元計價。

全球五氯酚市場趨勢及洞察

新興國家的基礎建設擴張

亞洲數百個涉及公路、鐵路和公共產業的大型企劃,持續推動對深度滲透型防腐劑的需求,這類防腐劑在易受白蟻侵蝕的氣候條件下,性能優於水性化學品。中國「十四五」規劃投資4.2兆美元用於交通走廊和工業園區建設,並在環境法規尚不完善的地區繼續指定使用工業級五氯酚。同樣,印度北部邊境附近耗資34億美元的戰略性鐵路擴建項目,也依賴經過防腐處理的枕木,以抵禦季風環境下的真菌腐爛。在東協地區,長效防腐劑對於滿足潮濕沿海地區預製木結構住宅50年的結構品質保證至關重要,預計到2024年,該市場規模將達到366億美元。由於萘酸銅基防腐劑系統的交付成本大約高出50%,對價格敏感的建築商繼續訂購五氯酚,這支撐了市場對五氯酚的需求,儘管歐洲和美國即將逐步取消相關法規。

在工業殺蟲劑和除草劑中持續使用

工業殺菌劑市場對五氯酚的需求依然強勁,但市場規模仍較小。尤其是在發電廠和煉油廠的高溫冷卻系統中,由於異噻唑啉酮類替代品容易分解,因此對五氯酚的需求得以維持。在南美洲和東南亞部分地區的皮革鞣製廠,當無法採用無鉻加工方法時,也會使用這種化學物質來防止皮革在儲存過程中滋生微生物。儘管自2024年以來全球農業需求大幅下降,但在《斯德哥爾摩公約》以外的地區,含五氯酚的除草劑仍被允許用於控制木本雜草。該領域提供了一筆雖不豐厚但穩定的收入,從而緩解了整體市場的波動。

環保替代品的可用性

自美國環保署 (EPA) 於 2024 年禁止生產以來,銅Azole、鹼性銅季銨鹽、微粉化銅Azole和 DCOI 已佔北美住宅木材需求的 70% 以上。矽酸鹽系統(例如 Russwood 於 2025 年收購的 SiooX)可使木材表面礦化,且不會產生有害廢棄物。這符合 LEED 認證要求,並且在考慮成本追蹤時可降低生命週期成本。隨著中國主要化合物生產商擴大環烷酸銅的生產規模,價格溢價正在下降,向替代品的轉變正在加速。這種向環境的轉變正在侵蝕五氯酚在法規和綠色金融標準一致的地區的市場佔有率。

細分市場分析

工業級產品預計在2025年佔總銷售額的78.15%,凸顯了其在高負載應用中的重要作用,例如電線杆和海洋樁,這些應用需要6至12磅/立方英尺的吸附率。五氯酚市場的主導地位源於這樣一個事實:傳統的加壓鋼瓶和溶劑回收迴路需要100萬至300萬美元的維修費用才能使其適用於水性銅系統。分析級產品預計到2031年將以4.88%的複合年成長率成長,這主要得益於實驗室、監管機構和顧問公司擴大使用EPA 8540方法試劑盒和亞ppm級檢測技術進行現場評估。默克集團和BioSynthe公司的認證參考物質正在支持這項合規需求的激增,預計到2031年將保持穩定成長。

儘管美國環保署(EPA)的逐步淘汰期限臨近,但新興亞洲國家仍在繼續訂購工業級五氯酚用於基礎設施建設,從而緩解了全球銷售量下滑的影響。然而,在印度和中國,萘酸銅與工業級五氯酚的價格差距正在縮小,這給利潤率帶來了壓力。分析級五氯酚恰恰受益於這些監管變化。隨著逐步淘汰的推進,對監測試劑的需求不斷成長,五氯酚在總銷售額中的市佔率也隨之擴大。

區域分析

預計到2025年,亞太地區將佔全球銷售額的39.22%,並將以5.16%的複合年成長率持續成長至2031年。這主要得益於中國4.2兆美元的交通基礎建設以及印度的戰略性鐵路和寬頻計畫。越南、印尼和菲律賓的加工商受益於當地豐富的木材資源和較低的合規成本,鞏固了五氯酚相對於銅Azole類化合物的價格優勢。北美市場正經歷結構性下滑。由於美國環保署(EPA)的生產禁令將於2024年生效,新的供應將停止,僅允許現有庫存使用至2027年2月。加州公共產業委員會計劃在2028年前禁止使用新的五氯酚處理過的電線電線杆,預計將加速市場下滑。

歐洲的情況較為複雜。隨著雜酚油的逐步淘汰,加工商轉向使用環烷酸銅,而五氯酚的過渡則暫時提振了需求。然而,REACH法規對消費品中5ppm的含量限制正在抑制長期成長。在南美、中東和非洲,由於監管執行不力以及對成本的高度敏感性,需求雖然多元化但仍然強勁。然而,更嚴格的綠色金融標準可能會限制處理木材的出口,並可能導致這些地區在2030年後市場萎縮。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 新興國家的基礎建設擴張

- 在工業殺蟲劑和除草劑中持續使用

- 停止使用雜酚油將有助於向替代品過渡。

- 需要深層滲透防腐劑的CLT結構板

- 利用木製桅杆在遍遠地區部署寬頻

- 市場限制因素

- 環保替代品的可用性

- 基於ESG因素,保險公司和投資者對公共產業進行監管

- 危險處理木材的處置成本不斷上漲

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按年級

- 工業級

- 分析級

- 透過使用

- 木材防腐劑

- 殺蟲劑和除草劑

- 皮革保存

- 工業消毒劑

- 其他用途(例如,抗菌劑)

- 按最終用戶行業分類

- 建造

- 發電業務(電線杆和橫樑)

- 農業和林業

- 皮革和紡織品

- 其他終端用戶產業(塗料、紙漿等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- AccuStandard

- Albemarle Corporation

- Biosynth

- Cabot Corporation

- Chem Service Inc.

- KANTO KAGAKU

- Koppers Inc.

- Merck KGaA

- Pure Water Products, LLC

- Santa Cruz Biotechnology Inc.

- Troy Corporation

- Viance

第7章 市場機會與未來展望

According to Mordor Intelligence, the pentachlorophenol market size is projected to expand from USD 100.94 million in 2025 and USD 105.69 million in 2026 to USD 133.04 million by 2031, registering a CAGR of 4.71% between 2026 to 2031.

This report is Segmented by Grade (Industrial Grade and Analytical Grade), Application (Wood Preservatives, Pesticides and Herbicides, and More), End-User Industry (Construction, Power Utilities, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Pentachlorophenol Market Trends and Insights

Expanding Infrastructure in Emerging Economies

Hundreds of road, rail, and utility mega-projects in Asia are unlocking sustained demand for deep-penetration preservatives that outperform water-borne chemistries in termite-prone climates. China's 14th Five-Year Plan channels USD 4.2 trillion into transportation corridors and industrial parks, a pipeline that continues to specify industrial-grade pentachlorophenol where environmental enforcement remains patchy. India's USD 3.4 billion strategic railway build-out near its northern border similarly leans on treated sleepers that resist fungal decay under monsoon exposure. Across ASEAN, prefab timber housing valued at USD 36.6 billion in 2024 relies on long-life preservatives to satisfy 50-year structural warranties in humid coastal markets. Because copper-naphthenate systems cost about 50% more on a delivered basis, price-sensitive contractors continue to order pentachlorophenol, propping up pentachlorophenol market demand even as regulatory sunsets loom in the West.

Continued Use in Industrial Pesticides and Herbicides

Industrial biocides remain a niche but resilient outlet for pentachlorophenol, especially in high-temperature cooling systems at power plants and refineries where isothiazolinone alternatives break down rapidly. Leather tanneries in South America and parts of Southeast Asia also employ the chemical to prevent microbial attack on hides during storage when chromium-free processes are unavailable. Although global agricultural volumes have fallen sharply post-2024, jurisdictions outside the Stockholm Convention still allow pentachlorophenol herbicide formulations for woody weed control. The segment anchors a predictable if modest revenue stream that tempers overall market volatility.

Availability of Eco-Friendly Alternatives

Copper azole, alkaline copper quaternary, micronized copper azole, and DCOI have captured more than 70% of North American residential-lumber demand since the 2024 EPA manufacturing cutoff. Silicate-based systems such as SiooX, acquired by Russwood in 2025, mineralize the wood surface and generate no hazardous waste, aligning with LEED credits and lowering life-cycle costs once tracking fees are considered. As large Chinese formulators scale copper naphthenate, price premiums shrink, accelerating substitution. This eco-pivot slices into the pentachlorophenol market share in regions where regulations and green-finance criteria converge.

Other drivers and restraints analyzed in the detailed report include:

- Creosote Withdrawal Driving Substitution

- Rural Broadband Roll-Outs Using Timber Masts

- Rising Disposal Costs for Hazardous Treated Wood

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial grade generated 78.15% of 2025 revenue, underscoring its role in high-load applications like utility poles and marine pilings that demand 6-12 lb/ft3 retention rates. The pentachlorophenol segment's advantage stems from legacy pressure cylinders and solvent-recovery loops that would require USD 1-3 million in retrofits to handle aqueous copper systems. Analytical grade is rising at a 4.88% CAGR through 2031 as laboratories, regulators, and consultants expand site assessments using EPA Method 8540 kits and sub-ppm detection technologies. Certified reference materials from Merck KGaA and Biosynth support this compliance boom, positioning the sub-segment for steady growth through 2031.

Despite EPA phase-out deadlines, emerging Asia keeps ordering industrial grade for infrastructure corridors, cushioning global volume declines. However, price parity between copper naphthenate and industrial pentachlorophenol is approaching in India and China, pressuring margins. Analytical grade benefits from that very regulatory churn; as phase-outs bite, demand for monitoring reagents intensifies, expanding its pentachlorophenol industry share within total revenue.

Geography Analysis

Asia-Pacific accounted for 39.22% of 2025 revenue and is advancing at a 5.16% CAGR through 2031, underpinned by China's USD 4.2 trillion transport build-out and India's strategic rail and broadband projects. Treaters in Vietnam, Indonesia, and the Philippines benefit from abundant local timber and lower compliance costs, locking in pentachlorophenol's price edge over copper azole. North America is in structural decline; the EPA manufacturing ban, effective 2024, halts new supply, and only stockpiles may be used until February 2027. California's Public Utilities Commission is set to ban new pentachlorophenol poles by 2028, accelerating contraction.

Europe exhibits a mixed profile: creosote withdrawal temporarily lifts demand as treaters switch to pentachlorophenol while upgrading for copper naphthenate, but REACH limits of 5 ppm in consumer articles cap long-term growth. South America and the Middle-East and Africa offer fragmented yet resilient demand thanks to lax enforcement and cost sensitivity; however, rising green-finance criteria may curtail exports of treated wood, narrowing the market in these regions post-2030.

- AccuStandard

- Albemarle Corporation

- Biosynth

- Cabot Corporation

- Chem Service Inc.

- KANTO KAGAKU

- Koppers Inc.

- Merck KGaA

- Pure Water Products, LLC

- Santa Cruz Biotechnology Inc.

- Troy Corporation

- Viance

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding infrastructure in emerging economies

- 4.2.2 Continued use in industrial pesticides and herbicides

- 4.2.3 Creosote withdrawal driving substitution

- 4.2.4 CLT structural panels requiring deep-penetration preservatives

- 4.2.5 Rural broadband roll-outs using timber masts

- 4.3 Market Restraints

- 4.3.1 Availability of eco-friendly alternatives

- 4.3.2 ESG-driven insurer and investor restrictions on utilities

- 4.3.3 Rising disposal costs for hazardous treated wood

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Grade

- 5.1.1 Industrial Grade

- 5.1.2 Analytical Grade

- 5.2 By Application

- 5.2.1 Wood Preservatives

- 5.2.2 Pesticides and Herbicides

- 5.2.3 Leather Preservation

- 5.2.4 Industrial Biocides

- 5.2.5 Other Applications (e.g., Antimicrobial Agents)

- 5.3 By End-user Industry

- 5.3.1 Construction

- 5.3.2 Power Utilities (Poles and Cross-arms)

- 5.3.3 Agriculture and Forestry

- 5.3.4 Leather and Textiles

- 5.3.5 Other End-user Industries (Coating, Pulp, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AccuStandard

- 6.4.2 Albemarle Corporation

- 6.4.3 Biosynth

- 6.4.4 Cabot Corporation

- 6.4.5 Chem Service Inc.

- 6.4.6 KANTO KAGAKU

- 6.4.7 Koppers Inc.

- 6.4.8 Merck KGaA

- 6.4.9 Pure Water Products, LLC

- 6.4.10 Santa Cruz Biotechnology Inc.

- 6.4.11 Troy Corporation

- 6.4.12 Viance

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

水處理消毒劑市場:依產品、配方、功能、給藥方法、銷售管道和應用分類-2026-2032年全球市場預測除生物劑市場:依類型、形態、溶解度、原料、應用及通路分類-2026-2032年全球市場預測

水處理消毒劑市場:依產品、配方、功能、給藥方法、銷售管道和應用分類-2026-2032年全球市場預測除生物劑市場:依類型、形態、溶解度、原料、應用及通路分類-2026-2032年全球市場預測 特種殺菌劑市場規模、佔有率、成長、全球產業分析、區域洞察及2026-2034年預測

特種殺菌劑市場規模、佔有率、成長、全球產業分析、區域洞察及2026-2034年預測 溴基殺菌劑市場規模、佔有率和趨勢分析報告:按最終用途、地區和細分市場預測(2026-2033 年)

溴基殺菌劑市場規模、佔有率和趨勢分析報告:按最終用途、地區和細分市場預測(2026-2033 年) 除生物劑市場報告:按產品、應用和地區分類,2026-2034年

除生物劑市場報告:按產品、應用和地區分類,2026-2034年 除生物劑市場:依產品類型、應用和地區分類RO膜專用快速消毒劑市場:按技術、膜材料、運行模式、壓力類型、應用和最終用戶分類,全球預測,2026-2032年2026-2034年全球除生物劑市場規模、佔有率、趨勢和成長分析報告

除生物劑市場:依產品類型、應用和地區分類RO膜專用快速消毒劑市場:按技術、膜材料、運行模式、壓力類型、應用和最終用戶分類,全球預測,2026-2032年2026-2034年全球除生物劑市場規模、佔有率、趨勢和成長分析報告 除生物劑市場分析與預測:按地區和應用分類(至2034年)

除生物劑市場分析與預測:按地區和應用分類(至2034年) 工業水消毒劑市場機會、成長要素、產業趨勢分析及2026年至2035年預測

工業水消毒劑市場機會、成長要素、產業趨勢分析及2026年至2035年預測