|

市場調查報告書

商品編碼

2062099

無菸煤:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Anthracite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

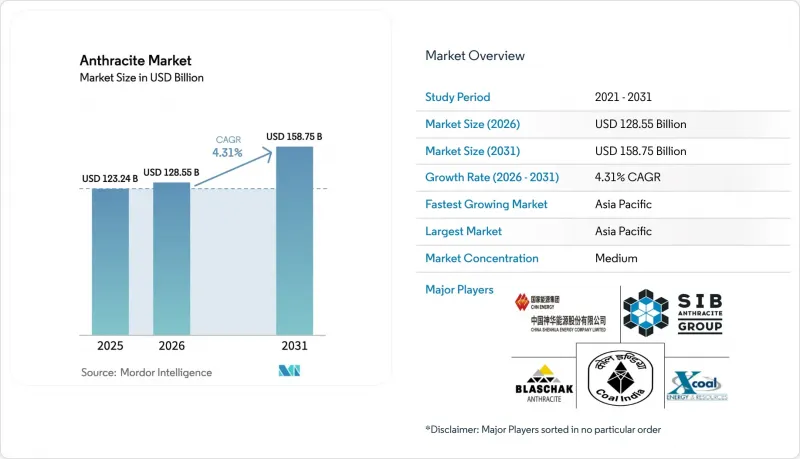

據 Mordor Intelligence 稱,2025 年無菸煤市場價值為 1232.4 億美元,預計到 2031 年將達到 1587.5 億美元,而 2026 年為 1285.5 億美元,預測期(2026-2031 年)的複合成長率為 4.31%。

本報告按等級(標準級、超高高等級(UHG) 和煅燒/電煅燒級)、應用(冶金、水和污水過濾等)、終端用戶行業(鋼鐵冶金、化工和石化、水處理企業等)以及地區(亞太地區、北美地區等)進行細分。市場預測以美元 (USD) 為單位。

全球無菸煤市場趨勢與洞察

綠色煉鋼製程強制使用超低灰碳添加劑。

鋼鐵生產商向氫氣直接還原鐵(DRI)和電弧爐過渡時,需要添加灰分低於8%、硫含量低於0.4%的碳添加劑,以最大限度地減少爐渣產生並維持熔池的化學成分。賓州近期的收購顯然瞄準了這些超高品質的礦床,以滿足美國和歐洲對電弧爐(EAF)日益成長的需求。隨著中國計劃在2030年將電弧爐市場佔有率提高到20%,全球對低揮發性原料的競爭日趨激烈,即使中等品質的熱力無菸煤正被天然氣直接還原鐵和生物碳取代,其價格仍居高不下。

地方政府向雙介質(無菸煤+沙)過濾系統過渡

北美和歐洲的公共產業正在對傳統砂過濾維修,透過加裝粗粒無菸煤蓋層,延長運作高達50%,並降低反沖洗成本。沙加緬度市2025年的合約修訂案以及水研究基金會(WRF)50萬美元的PFAS計畫都表明,這種需求具有長週期性和規範主導。營運成本的降低能夠保護採購預算免受價格波動衝擊,並為無菸煤市場的一部分提供強力的支援。

石油焦和生物炭的價格折扣

2024年至2026年間,美國墨西哥灣沿岸高硫石油焦的交易價格低至每噸60美元,侵蝕了無菸煤在水泥窯和工業鍋爐中的市場佔有率。瑞典一座電弧爐(EAF)正在進行的中試規模生物炭試驗可望實現淨零排放,並可能隨著供應鏈的成熟而加速轉型。生產商正透過延長合約期限並強調無菸煤的低灰分和低揮發性來應對這一挑戰,在無菸煤市場,品質而非價格才是決定其應用的關鍵因素。

細分市場分析

2025年,標準級無菸煤的市佔率維持在47.12%,主要得益於傳統水處理、住宅暖氣和中型煉鋼的需求。然而,由於水泥窯和鍋爐應用中石油焦的價格競爭,該細分市場的利潤率有所下降。相較之下,煅燒級和電煅燒級無菸煤預計到2031年將以5.12%的複合年成長率成長,預計將獲得鋰離子電池、鈉離子電池和燃料電池負極材料的訂單,尤其專注於固定碳含量達到95%或以上的產品。中國電池製造商與賓夕法尼亞州和西伯利亞的生產商簽署的早期供應協議表明,需求將穩步成長,這將推動預測期內煅燒級無菸煤市場的整體規模擴大。

高等級(UHG)無菸煤,其固定碳含量為92%或以上,揮發分含量為5%或以下,是價值最高的無菸煤,其價格比標準品位無菸煤高出20%至40%。 Menar公司於2025年收購了Spring Lake煤礦,為全球供應增加了72萬噸出口級超高品位無菸煤。由於其嚴格的品質標準,超高品位無菸煤是鐵合金還原和電弧爐(EAF)噴吹的關鍵原料,並且與低品位煤炭相比,它對運費衝擊和監管成本的抵禦能力更強,從而保護了其利基市場。

區域分析

亞太地區主導無菸煤市場,預計2025年將佔全球需求的53.24%。受中國煤化工業務擴張以及印度2028-2029會計年度10億噸產量目標的推動,預計到2031年,該地區無菸煤市場將維持4.47%的複合年成長率。中國神華集團斥資350億美元收購13家子公司,進行重組,旨在確保物流和電力資產,進而最佳化從礦場到港口的供應,同時將蘊藏量提高25%。東南亞國協,特別是印尼和越南,正持續擴大燃煤發電和水泥熟料產能,因為進口無菸煤的熱值更高、雜質含量更低,比國產褐煤更具優勢。

北美無菸煤市場依賴賓州的煤田,該煤田擁有超過百年的開採歷史。 2024年, Delta Dunia收購了Atlantic Carbon Group,將其旗下四座超優質煤礦整合到價值1.224億美元的集團旗下。自2014年以來,對歐洲和亞洲的無菸煤出口一直保持兩位數的成長,這主要得益於其揮發分含量高、硫含量低等差異化優勢。隨著可再生能源和價格更低的天然氣蠶食發電產能,美國國內對火力發電的需求正在下降,但過濾材料和特殊碳等細分市場的需求支撐著基本的加工需求。

在歐洲,儘管火力發電需求萎縮,但特種煤市場卻蓬勃發展。歐盟的碳邊境調節機制(CBAM)鼓勵進口商轉向使用經認證的低排放煤,這為能夠證明其礦場效率的美國和南非供應商創造了市場機會。東歐的區域供熱和北歐的水處理設施仍在進行現貨採購,但長期交易量取決於煤炭淘汰政策的進展。在以巴西為首的南美洲,由於外匯和運費的變化,市場波動不定。在俄羅斯煤炭供應面臨地緣政治障礙後,澳洲煤炭的佔有率在2025年至2026年間飆升至30%。南非是非洲的中心,隨著梅納爾煤礦的擴建,該地區已成為出口導向超高品質煤炭的重要樞紐。同時,南非國家運輸集團(Transnet)的改革向第三方開放了鐵路運輸配額,預計將降低離岸價(FOB)並增加無菸煤市場的供應。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 綠色鋼鐵生產過程中強制使用超低灰碳添加劑。

- 地方政府向兩相(無菸煤+沙)過濾系統過渡

- 鋰離子電池負極材料中電煅燒無菸煤的生長

- 由於耐火材料維修,對高密度碳磚的需求增加。

- 自主長壁採礦提升了成本競爭力

- 市場限制因素

- 石油焦和生物炭價格折扣

- 海運費率波動和紅海繞行溢價

- 歐盟即將對煤炭衍生的碳排放徵收碳邊境調節稅。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按年級

- 標準級

- 超高等級 (UHG)

- 燒結等級和電燒結等級

- 透過使用

- 冶金(鋼鐵、鐵合金、耐火材料)

- 供水和廢水過濾

- 火力發電和熱電聯產

- 化工原料及碳產品

- 其他應用(陶瓷、燃料電池等)

- 按最終用戶行業分類

- 鋼鐵冶金

- 化工/石油化工

- 水處理設施

- 能源與電力

- 其他終端使用者產業(建築材料、碳產品等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Atlantic Carbon Group

- Blaschak Anthracite

- BUMA International Group

- Carbones Holding GmbH

- CHINA SHENHUA

- Coal India Limited

- Feishang Anthracite Resources Limited

- Guess & Co

- JINERGY

- Lehigh Anthracite

- Reading Anthracite Company

- Sadovaya Group

- Sibanthracite Group

- Xcoal Energy & Resources

- Yanzhou Coal Mining Company Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the anthracite market size was valued at USD 123.24 billion in 2025 and is estimated to grow from USD 128.55 billion in 2026 to reach USD 158.75 billion by 2031, at a CAGR of 4.31% during the forecast period (2026-2031).

This report is Segmented by Grade (Standard Grade, Ultra-High Grade (UHG), and Calcined and Electrically-Calcined Grade), Application (Metallurgy, Water and Waste-Water Filtration, and More), End-User Industry (Steel and Metallurgy, Chemicals and Petrochemicals, Water Treatment Utilities, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Anthracite Market Trends and Insights

Mandates for Ultra-Low-Ash Carbon Additives in Green-Steel Processes

Steelmakers moving toward hydrogen DRI and electric arc furnaces need carbon additives with less than 8% ash and below 0.4% sulfur to minimize slag volumes and maintain bath chemistry. Recent acquisitions in Pennsylvania explicitly target these ultra-high-grade deposits to supply U.S. and European EAF expansions. China's plan to raise EAF share to 20% by 2030 intensifies global competition for low-volatile feedstocks, sustaining premium pricing even as mid-grade thermal anthracite faces substitution from natural-gas DRI and bio-carbon.

Municipal Shift to Dual-Media (Anthracite + Sand) Filtration Beds

North American and European utilities are retrofitting conventional sand filters with a coarse anthracite cap that extends run length up to 50% and cuts backwash costs. Sacramento's 2025 contract amendment and the Water Research Foundation's USD 500,000 PFAS project underscore the long-cycle, specification-driven nature of this demand. The operational savings shield procurement budgets from price shocks, anchoring a resilient slice of the anthracite market.

Petroleum-Coke and Bio-Carbon Price Discounting

High-sulfur U.S. Gulf Coast petcoke has traded as low as USD 60 per tonne in 2024-2026, slicing into anthracite's share of cement kilns and industrial boilers. Pilot-scale bio-carbon trials in Swedish EAFs promise net-zero emissions and could accelerate displacement if supply chains mature. Producers counter by lengthening contract tenors and highlighting anthracite's low ash and volatile-matter specs, where quality, not price, governs adoption.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Electrically-Calcined Anthracite in Li-Ion Anodes

- High-Density Carbon-Brick Demand from Refractory Retrofits

- Seaborne Freight-Rate Volatility and Red-Sea Rerouting Premiums

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Standard grade retained 47.12% share of the anthracite market in 2025, buoyed by traditional water-treatment, residential heating, and mid-tier metallurgy demand. The sub-segment's margin, however, narrowed as petcoke undercut it in cement kilns and boilers. By contrast, calcined and electrically-calcined grades are forecast to rise at a 5.12% CAGR through 2031, capturing lithium-ion, sodium-ion, and fuel-cell anode orders that value fixed-carbon levels above 95%. Early-stage supply agreements between Chinese cell makers and Pennsylvanian and Siberian producers point to steady uptake that will lift the overall anthracite market size allocated to calcined grades during the forecast window.

Ultra-High Grade (UHG) anthracite, defined by ≥92% fixed carbon and ≤5% volatiles, sits at the apex of the value ladder and trades at premiums of 20-40% over Standard Grade. Menar's Springlake Colliery purchase in 2025 added 720,000 tons per year of export-quality UHG material to global supply. Tight spec ranges make UHG indispensable in ferroalloy reduction and EAF injection, safeguarding a niche that absorbs freight shocks and regulatory costs better than lower-grade peers.

Geography Analysis

Asia-Pacific dominated the anthracite market with 53.24% of 2025 demand and will post a 4.47% CAGR through 2031, propelled by China's coal-to-chemicals rollouts and India's 1 billion-tonne production target for FY 2028-29. China Shenhua's restructuring, adding 13 subsidiaries for USD 35 billion, secures logistics and power assets that streamline supply from mine to port while expanding reserves by 25%. ASEAN states, notably Indonesia and Vietnam, continue to sanction coal-fired power and clinker capacity where imported anthracite's high calorific value and low impurity profile confer advantages over domestic lignite.

North America's anthracite market leans on Pennsylvania's century-old basin, where Delta Dunia's 2024 purchase of Atlantic Carbon Group united four ultra-premium mines under a USD 122.4 million umbrella. Exports to Europe and Asia have expanded at double-digit rates since 2014, reflecting points of differentiation in volatile-matter content and low sulfur. Domestic thermal demand wanes as renewables and cheap gas capture utility capacity, but the filter-media and specialty-carbon niches sustain baseline throughput.

Europe witnesses contracting thermal demand yet retains a vibrant specialty segment. The EU's Carbon Border Adjustment Mechanism nudges importers toward certified-low-emission cargoes, opening space for U.S. and South African suppliers able to document mine-site efficiencies. Eastern European district heating and Nordic water-treatment plants continue spot purchases, but long-run volumes hinge on the pace of coal phase-out policies. South America, led by Brazil, oscillates with currency swings and freight costs; Australian cargoes surged to 30% share in 2025-2026 after Russian supply faced geopolitical barriers. Africa's epicenter is South Africa, where Menar's expansion gives the region an export-oriented, ultra-high-grade anchor, even as Transnet reforms open third-party rail slots that could lower FOB costs and grow volumes into the anthracite market.

- Atlantic Carbon Group

- Blaschak Anthracite

- BUMA International Group

- Carbones Holding GmbH

- CHINA SHENHUA

- Coal India Limited

- Feishang Anthracite Resources Limited

- Guess & Co

- JINERGY

- Lehigh Anthracite

- Reading Anthracite Company

- Sadovaya Group

- Sibanthracite Group

- Xcoal Energy & Resources

- Yanzhou Coal Mining Company Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandates for ultra-low-ash carbon additives in green-steel processes

- 4.2.2 Municipal shift to dual-media (anthracite + sand) filtration beds

- 4.2.3 Growth of electrically-calcined anthracite in Li-ion anodes

- 4.2.4 High-density carbon-brick demand from refractory retrofits

- 4.2.5 Autonomous long-wall mining boosting cost-competitiveness

- 4.3 Market Restraints

- 4.3.1 Petroleum-coke and bio-carbon price discounting

- 4.3.2 Seaborne freight-rate volatility and Red-Sea rerouting premiums

- 4.3.3 Impending EU Carbon-Border Adjustment on embedded coal carbon

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Grade

- 5.1.1 Standard Grade

- 5.1.2 Ultra-High Grade (UHG)

- 5.1.3 Calcined and Electrically-Calcined Grade

- 5.2 By Application

- 5.2.1 Metallurgy (Steel, Ferro-alloys, Refractories)

- 5.2.2 Water and Waste-Water Filtration

- 5.2.3 Thermal Power Generation and CHP

- 5.2.4 Chemical Feedstock and Carbon Products

- 5.2.5 Other Applications (Ceramics, Fuel Cells, etc.)

- 5.3 By End-user Industry

- 5.3.1 Steel and Metallurgy

- 5.3.2 Chemicals and Petrochemicals

- 5.3.3 Water Treatment Utilities

- 5.3.4 Energy and Power

- 5.3.5 Other End-user Industries (Construction Materials, Carbon Products, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Atlantic Carbon Group

- 6.4.2 Blaschak Anthracite

- 6.4.3 BUMA International Group

- 6.4.4 Carbones Holding GmbH

- 6.4.5 CHINA SHENHUA

- 6.4.6 Coal India Limited

- 6.4.7 Feishang Anthracite Resources Limited

- 6.4.8 Guess & Co

- 6.4.9 JINERGY

- 6.4.10 Lehigh Anthracite

- 6.4.11 Reading Anthracite Company

- 6.4.12 Sadovaya Group

- 6.4.13 Sibanthracite Group

- 6.4.14 Xcoal Energy & Resources

- 6.4.15 Yanzhou Coal Mining Company Limited

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Surging Clean-fuel Demand across Emerging APAC Economies

煅燒無菸煤市場規模、佔有率、趨勢和預測:按技術、應用、終端用戶產業和地區分類,2026-2034年

煅燒無菸煤市場規模、佔有率、趨勢和預測:按技術、應用、終端用戶產業和地區分類,2026-2034年 煅燒無菸煤市場:依等級、製造流程、形態、碳含量及應用分類-2026-2032年全球市場預測無菸煤市場:2026-2032年全球市場預測(依最終用途產業、形狀、開採類型及通路分類)

煅燒無菸煤市場:依等級、製造流程、形態、碳含量及應用分類-2026-2032年全球市場預測無菸煤市場:2026-2032年全球市場預測(依最終用途產業、形狀、開採類型及通路分類) 無菸煤市場機會、成長要素、產業趨勢分析及2026-2035年預測

無菸煤市場機會、成長要素、產業趨勢分析及2026-2035年預測 2026年全球煅燒無菸煤市場報告2026年全球無菸煤市場報告

2026年全球煅燒無菸煤市場報告2026年全球無菸煤市場報告 鍛燒無菸煤市場規模、佔有率和成長分析(按類型、形態、應用、最終用途產業和地區分類)—產業預測(2026-2033 年)

鍛燒無菸煤市場規模、佔有率和成長分析(按類型、形態、應用、最終用途產業和地區分類)—產業預測(2026-2033 年) 無菸煤:全球市場佔有率和排名、總銷售量和需求預測(2025-2031年)

無菸煤:全球市場佔有率和排名、總銷售量和需求預測(2025-2031年) 全球優質無菸煤市場

全球優質無菸煤市場 全球煅燒無菸煤市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)

全球煅燒無菸煤市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)