|

市場調查報告書

商品編碼

2062092

美國焊接耗材:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)United States Welding Consumables - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

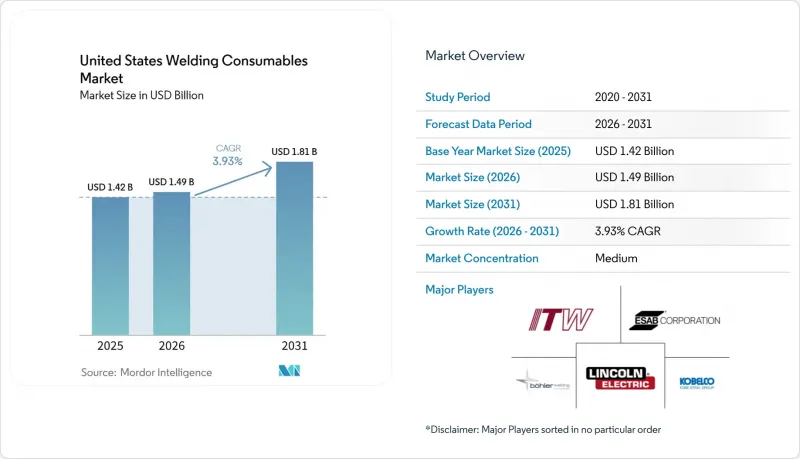

根據 Mordor Intelligence 預測,美國焊接耗材市場將從 2025 年的 14.2 億美元成長到 2026 年的 14.9 億美元,到 2031 年將達到 18.1 億美元,2026 年至 2031 年的複合年成長率為 3.93%。

本報告按產品類型(棒狀焊條、藥芯焊絲等)、焊接工藝(電弧焊接(SMAW、GMAW、GTAW、FCAW)、電阻焊接等)、終端用戶行業(建築和基礎設施、汽車和交通運輸、能源等)以及地區(東北部、中西部、南部、西部)進行細分。市場預測以貨幣形式呈現。

美國焊接耗材市場趨勢與洞察

基礎設施投資和現代化法案的實施

聯邦基礎設施支出為橋樑和高速公路上的重型鋼結構工程提供了支撐,從而確保了對符合橋樑和結構標準的結構焊接耗材的穩定需求。 《基礎設施投資與就業法案》繼續透過聯邦公路管理局提供多年預算撥款,使得預測州級橋樑工程及相關鋼結構需求成為可能。儘管建築材料價格上漲限制了目前的實體供應,但資金籌措前景依然強勁,足以支撐到2026年的工作量。這對於低氫塗層焊條、實心焊絲和藥芯焊絲尤其重要,因為它們是橋樑和大型土木鋼結構項目必不可少的材料。隨著工期壓力促使承包商採用自動化焊接材料,以確保焊接的重複性和輪胎邊緣品質的一致性,美國焊接材料市場將從中受益。各州交通運輸計劃與聯邦撥款相結合,使鋼樑製造和現場組裝的訂單積壓保持穩定,從而在整個預測期內支撐了對焊接材料的需求。

將重工業和金屬加工業帶回我國

製造商正在擴大其國內半導體、電池和先進設備的產能,這增強了對不銹鋼、鎳和鋁等各種特殊熔填材料的中期需求。在美國焊接耗材市場,隨著原始設備製造商(OEM)將高價值工藝本地化,晶圓廠和電池工廠對可追溯且符合無塵室要求的耗材的需求日益成長。在汽車供應鏈中,南部和西南部的新工廠正在調整焊絲、製程控制和設備選型,使其適用於自動化,從而減少返工並幫助彌合大型專案中的技能差距。美國焊接耗材市場也受益於更廣泛的供應商品質框架,該框架鼓勵對已記錄的程序進行雙重認證和認可,這使得優質焊絲在法規環境下的作用更加重要。隨著越來越多的資本項目從宣佈到安裝,焊接耗材的採購週期變得更加可預測,這使得擁有本地庫存和技術支援的供應商更具優勢。

焊工老化與後備人才有限

焊工的平均年齡高於普通勞動力的平均年齡,這加劇了勞動力短缺,並增加了雇主的培訓負擔。許多製造商正透過採用自動化、機器人單元和標準化流程來應對這項挑戰,以降低技能差異,這也促使焊材的選擇轉向那些能夠穩定引弧和保證輪胎邊緣形狀可重複的產品。因此,美國焊接耗材市場對用於自動化製程的高精度、性能可靠的焊絲和焊劑的需求日益成長。訓練方法也正在變化,更加重視機器人電弧焊接和電阻焊接的認證,從而在更短的時間內提升操作人員的能力。在預測期內,這些人口結構變化將在某些應用領域推動製程替代,同時在其他繼續使用電弧焊接的應用領域中,也將支撐對高品質焊材的需求。

細分市場分析

在美國焊接耗材市場,焊條仍將保持最大佔有率,到2025年將佔銷售額的37.12%,而藥芯焊絲預計將以5.76%的複合年成長率成長至2031年。焊條在現場維修、結構工程和維護工作中仍然佔據主導地位,其便攜性、安裝速度和對錶面條件的適應性優於連續焊絲製程的生產效率優勢。在美國焊接耗材市場,低氫和纖維素基焊條仍廣泛應用於能源相關和土木工程管道連接、偏遠地區施工和維修工作。同時,藥芯焊絲因其在立焊和仰焊位置的高焊接速度而市場佔有率不斷成長,使其適用於橋樑建設、高層建築和模組化船舶建造等對每英尺人事費用要求極高的應用領域。由於結構鋼標準的更新和品管系統的完善,市場對焊條和藥芯焊絲等認證焊接材料的需求依然強勁,從而支撐了工廠和現場應用領域均衡的產品組合。

藥芯焊絲非常適合注重重複性和產量的大型項目,以及機器人單元的自動化應用,這推動了其在2031年之前保持主導的成長趨勢。實心焊絲因其穩定的電弧特性和與標準GMAW系統的兼容性,仍然是汽車、重型機械和通用機械加工領域可靠的中端市場選擇。埋弧焊(SAW)焊劑和焊絲在壓力容器、管線工廠和大型結構件領域保持著穩固的市場地位,因為其穩定的機械性能和可控的熱輸入使得在焊劑和製程控制方面的資本投資物有所值。 TIG焊條和硬焊合金用於航太、製藥管道和食品級不銹鋼加工等高純度或薄壁應用;這些產品價格昂貴,且對文件要求嚴格。預計美國焊接耗材產業將繼續根據實際應用最佳化產品選擇,這將維持現場作業對電弧電銲條的需求,並支援用於結構和模組化建築的藥芯焊絲產品實現高於平均水平的成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 基礎設施投資和現代化法案的實施

- 國內重工業和金屬加工業的回歸

- 天然氣管道網路的擴建與現代化

- 陽光地帶各州的商業建築熱潮

- 恢復造船和軍艦建造

- 石油和天然氣行業的維護和修理活動

- 市場限制因素

- 焊工老化與後備人才有限

- 鋼絲和焊劑原料價格的波動

- 汽車產業向替代黏合方法的過渡

- 建築業和製造業對商業週期的經濟敏感性

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 產業吸引力—五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 私募股權對銷售網路的重組

- 食品加工產業對不銹鋼耗材的需求不斷成長。

第5章 市場規模與成長預測

- 依產品類型

- 棒狀電極

- 單線

- 藥芯焊絲

- SAW焊劑和焊絲

- TIG焊條和硬焊合金

- 透過焊接工藝

- 弧

- SMAW(棒材)

- GMAW/MIG

- GTAW/TIG

- FCAW

- 電阻焊接

- 雷射和混合焊接

- 弧

- 產業最終用途

- 建築和基礎設施

- 汽車和運輸業

- 能源(石油、天然氣、電力)

- 造船/海洋

- 重型機械和工業設備

- 其他

- 按地區

- 東北

- 中西部

- 南部

- 西

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Lincoln Electric Holdings Inc.

- ESAB Corporation

- Illinois Tool Works Inc.(Hobart Brothers)

- voestalpine Bohler Welding USA

- Kobe Steel Ltd.(Kobelco Welding of America)

- Air Liquide Welding

- Sandvik Materials Technology(Exaton)

- Messer Group

- Wire Wizard Welding Products

- Harris Products Group

- Washington Alloy Co.

- Weldcote Metals

- Eutectic Castolin

- Select-Arc Inc.

- Alcotec Wire Corp.

- Arcon Welding Equipment

- Blue Demon Welding Products

- Fronius USA LLC

- Praxair(Linde)Filler Metals

- McKay(Lincoln Electric)

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states welding consumables market size is expected to grow from USD 1.42 billion in 2025 to USD 1.49 billion in 2026 and is forecast to reach USD 1.81 billion by 2031 at 3.93% CAGR over 2026-2031.

This report is Segmented by Product Type (Stick Electrodes, Flux-Cored Wires, and More), by Welding Process (Arc (SMAW, GMAW, GTAW, FCAW), Resistance Welding, and More), by End-Use Industry (Construction & Infrastructure, Automotive & Transportation, Energy, and More), and by Geography (Northeast, Midwest, South, and West). The Market Forecasts are Provided in Terms of Value (USD Billion).

United States Welding Consumables Market Trends and Insights

Infrastructure Investment and Modernization Act Implementation

Federal infrastructure spending has raised the floor for steel-intensive work in bridges and highways, supporting steady demand for structural welding consumables that meet bridge and structural codes. The Infrastructure Investment and Jobs Act continues to funnel multi-year allocations through the Federal Highway Administration, which provides visibility into state-level bridge programs and related steel fabrication needs. While inflation in construction inputs has tempered the immediate physical delivery, the funding horizon remains robust, supporting workloads through 2026. This is particularly pertinent for low-hydrogen stick electrodes, solid wires, and flux-cored wires, all essential for bridges and heavy civil steel projects. The United States welding consumables market benefits when schedule pressure pushes contractors toward automation-ready consumables that support repeatability and consistent bead quality. State transportation plans layered on federal allocations keep backlogs steady for steel girder fabrication and field assembly, which supports consumables offtake throughout the forecast window.

Onshoring of Heavy Manufacturing and Metal Fabrication

Manufacturers are increasing domestic capacity in semiconductors, batteries, and advanced equipment, which reinforces medium-term demand for specialized filler metals across stainless, nickel, and aluminum grades. The United States welding consumables market is seeing more specifications that call for traceability and cleanroom-compatible consumables in fabs and battery facilities as OEMs localize high-value steps. In automotive supply chains, new facilities in the South and Southwest are aligning equipment selection with automation-friendly wires and process controls that reduce rework and help bridge skill gaps on large projects. The United States welding consumables market is also benefiting from broader supplier quality frameworks that encourage dual certification and documented procedure qualification, which deepens the role of premium grades in regulated environments. As more capital projects move from announcement to installation, purchasing cycles for welding consumables become more predictable and favor suppliers with local inventories and technical support.

Aging Welder Workforce with Limited Replacement Pipeline

The median age of welders is higher than the broader workforce, which tightens the available labor pool and raises training burdens for employers. Many fabricators respond by adopting automation, robotic cells, and standardized procedures that reduce skill variability, which shifts consumables selection toward products that support consistent arc starts and repeatable bead geometry. The United States welding consumables market is thus seeing stronger interest in wires and fluxes with tight tolerances and documented performance for automated processes. Training pathways are also evolving, with more emphasis on certifications that align with robotic arc welding and resistance welding to broaden operator capabilities in shorter timeframes. Over the forecast period, this demographic pressure encourages process substitution in some applications while supporting premium-grade consumables in others that remain arc-based.

Other drivers and restraints analyzed in the detailed report include:

- Natural Gas Pipeline Network Expansion and Replacement

- Commercial Construction Boom in Sunbelt States

- Raw Material Price Volatility for Steel Wire and Flux

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Stick electrodes held the largest share at 37.12% of 2025 revenue within the United States welding consumables market, while flux-cored wires are projected to grow fastest at a 5.76% CAGR through 2031. Stick remains entrenched in field repairs, structural projects, and maintenance tasks where portability, setup speed, and tolerance to surface conditions outweigh the productivity gains of continuous-wire processes. The United States welding consumables market continues to rely on low-hydrogen and cellulosic stick grades for pipeline tie-ins, remote construction, and repair work across energy and civil sites. In parallel, flux-cored wires are gaining share because they deliver high deposition rates in vertical and overhead positions, suiting bridge erection, high-rise construction, and modular shipbuilding, where labor cost per linear foot matters. Code updates and quality frameworks in structural steel maintain the need for certified consumables in both stick and flux-cored formats, which supports a balanced product mix across shop and field uses.

Flux-cored wires are aligned with automation on large projects and in robotic cells that prioritize repeatability and throughput, which fuels their leading growth profile through 2031. Solid wires remain a steady mid-market option for automotive, heavy equipment, and general fabrication due to their stable arc characteristics and compatibility with standard GMAW systems. SAW flux and wire hold a durable niche in pressure vessels, line pipe mills, and heavy structural sections because consistent mechanical properties and controlled heat input justify capital investment in flux handling and process controls. TIG rods and brazing alloys serve high-purity or thin-wall applications in aerospace, pharmaceutical piping, and food-grade stainless work, which carry premium pricing and strict documentation needs. The United States welding consumables industry is expected to see continued optimization of product selection by job context, which sustains stick volumes in field work and supports above-market growth for flux-cored products in structural and modular builds.

List of Companies Covered in this Report:

- Lincoln Electric Holdings Inc.

- ESAB Corporation

- Illinois Tool Works Inc. (Hobart Brothers)

- voestalpine Bohler Welding USA

- Kobe Steel Ltd. (Kobelco Welding of America)

- Air Liquide Welding

- Sandvik Materials Technology (Exaton)

- Messer Group

- Wire Wizard Welding Products

- Harris Products Group

- Washington Alloy Co.

- Weldcote Metals

- Eutectic Castolin

- Select-Arc Inc.

- Alcotec Wire Corp.

- Arcon Welding Equipment

- Blue Demon Welding Products

- Fronius USA LLC

- Praxair (Linde) Filler Metals

- McKay (Lincoln Electric)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure Investment and Modernization Act Implementation

- 4.2.2 Onshoring of Heavy Manufacturing and Metal Fabrication

- 4.2.3 Natural Gas Pipeline Network Expansion and Replacement

- 4.2.4 Commercial Construction Boom in Sunbelt States

- 4.2.5 Shipbuilding and Naval Vessel Construction Uptick

- 4.2.6 Maintenance and Repair Activities in Oil and Gas Sector

- 4.3 Market Restraints

- 4.3.1 Aging Welder Workforce with Limited Replacement Pipeline

- 4.3.2 Raw Material Price Volatility for Steel Wire and Flux

- 4.3.3 Shift Toward Alternative Joining Methods in Automotive

- 4.3.4 Economic Sensitivity to Construction and Manufacturing Cycles

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Distributor Network Consolidation Through Private Equity Activity

- 4.9 Growing Demand for Stainless Steel Consumables in Food Processing

5 Market Size & Growth Forecasts (Values, In USD Billion)

- 5.1 By Product Type

- 5.1.1 Stick Electrodes

- 5.1.2 Solid Wires

- 5.1.3 Flux-Cored Wires

- 5.1.4 SAW Flux & Wire

- 5.1.5 TIG Rods & Brazing Alloys

- 5.2 By Welding Process

- 5.2.1 Arc

- 5.2.1.1 SMAW (Stick)

- 5.2.1.2 GMAW / MIG

- 5.2.1.3 GTAW / TIG

- 5.2.1.4 FCAW

- 5.2.2 Resistance Welding

- 5.2.3 Laser & Hybrid Welding

- 5.2.1 Arc

- 5.3 By End-Use Industry

- 5.3.1 Construction & Infrastructure

- 5.3.2 Automotive & Transportation

- 5.3.3 Energy (Oil, Gas & Power)

- 5.3.4 Shipbuilding & Offshore

- 5.3.5 Heavy Equipment & Industrial Machinery

- 5.3.6 Others

- 5.4 By Region

- 5.4.1 Northeast

- 5.4.2 Midwest

- 5.4.3 South

- 5.4.4 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Lincoln Electric Holdings Inc.

- 6.4.2 ESAB Corporation

- 6.4.3 Illinois Tool Works Inc. (Hobart Brothers)

- 6.4.4 voestalpine Bohler Welding USA

- 6.4.5 Kobe Steel Ltd. (Kobelco Welding of America)

- 6.4.6 Air Liquide Welding

- 6.4.7 Sandvik Materials Technology (Exaton)

- 6.4.8 Messer Group

- 6.4.9 Wire Wizard Welding Products

- 6.4.10 Harris Products Group

- 6.4.11 Washington Alloy Co.

- 6.4.12 Weldcote Metals

- 6.4.13 Eutectic Castolin

- 6.4.14 Select-Arc Inc.

- 6.4.15 Alcotec Wire Corp.

- 6.4.16 Arcon Welding Equipment

- 6.4.17 Blue Demon Welding Products

- 6.4.18 Fronius USA LLC

- 6.4.19 Praxair (Linde) Filler Metals

- 6.4.20 McKay (Lincoln Electric)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

焊接耗材市場:按產品類型、焊接工藝、材料類型、應用和最終用戶產業分類-全球預測,2026-2032年

焊接耗材市場:按產品類型、焊接工藝、材料類型、應用和最終用戶產業分類-全球預測,2026-2032年 焊接耗材市場報告:按產品類型、焊接技術、終端用戶產業和地區分類(2026-2034 年)

焊接耗材市場報告:按產品類型、焊接技術、終端用戶產業和地區分類(2026-2034 年) 焊接耗材市場:依焊接耗材、焊接技術、應用及地區分類電弧焊接市場:2026-2032年全球市場預測(依焊接流程、自動化程度、冷卻方式、焊槍類型、電流類型、最終用戶和應用分類)

焊接耗材市場:依焊接耗材、焊接技術、應用及地區分類電弧焊接市場:2026-2032年全球市場預測(依焊接流程、自動化程度、冷卻方式、焊槍類型、電流類型、最終用戶和應用分類) 2026年全球汽車數位焊接設備市場報告2026年全球焊接耗材市場報告2026年全球耐磨件市場報告

2026年全球汽車數位焊接設備市場報告2026年全球焊接耗材市場報告2026年全球耐磨件市場報告 焊接材料市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034)新能源汽車焊接合金市場:按合金類型、焊接工藝、母材類型、形狀、應用和最終用戶分類,全球預測(2026-2032年)日本焊接耗材市場規模、佔有率、趨勢及預測(依產品類型、焊接技術、終端用戶產業及地區分類,2026-2034年)

焊接材料市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034)新能源汽車焊接合金市場:按合金類型、焊接工藝、母材類型、形狀、應用和最終用戶分類,全球預測(2026-2032年)日本焊接耗材市場規模、佔有率、趨勢及預測(依產品類型、焊接技術、終端用戶產業及地區分類,2026-2034年)