|

市場調查報告書

商品編碼

2062087

金屬替代品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Metal Replacement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

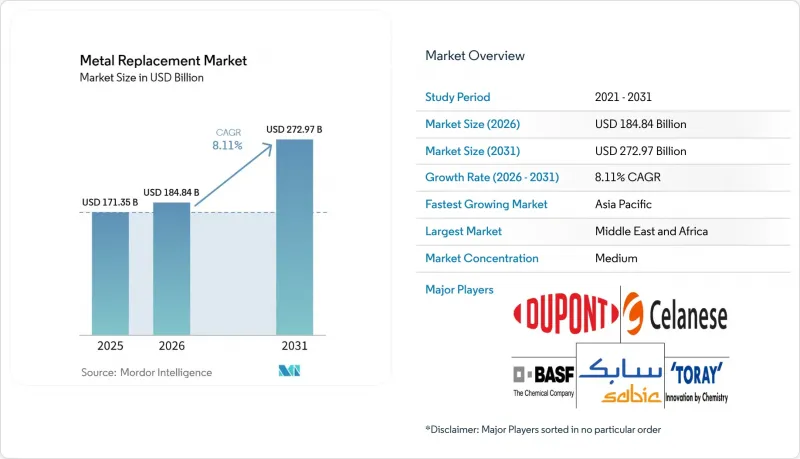

根據 Mordor Intelligence 預測,金屬替代品市場規模預計將在 2025 年達到 1,713.5 億美元,2026 年達到 1,848.4 億美元,到 2031 年達到 2729.7 億美元,2026 年至 2031 年的複合年成長率為 8.11%。

本報告材料類型(工程塑膠和複合材料)、終端用戶產業(汽車、航太與國防、工業設備與機械、建築基礎設施、醫療保健與醫療設備等)以及地區(亞太地區、北美、歐洲、南美以及中東和非洲)進行細分。市場預測以美元計價。

全球金屬替代品市場趨勢及洞察

汽車和航太領域都在不斷擴大輕量化趨勢。

電池式電動車需要將底盤重量減輕200-300公斤,以抵消鋰離子電池的重量。因此,各大汽車製造商正在用玻璃纖維增強聚丙烯護板和碳纖維增強熱塑性電池外殼取代車身底部鋼材,從而在滿足碰撞安全標準的同時提高能源效率。空中巴士已認證其完全可回收的熱塑性機身面板將於2025年投入使用。與熱固性樹脂相比,這些面板在製造過程中可減少40%的能源消耗,並允許進行局部維修,在25年的使用壽命內,預計將航空公司的維護成本降低15-20%。到2024年,全球風力發電機裝置容量將增加117吉瓦,其中複合材料葉片佔轉子品質的90%以上,這將使離岸風力發電對基礎鋼材的需求減少高達40%。經桑迪亞國家實驗室批准的一種碳-玻璃複合材料混合設計,使其抗張強度提高了44.7%,從而可以在不相應增加質量的情況下將轉子直徑從150米增加到180米。 Akelite 於 2025 年開發的熱塑性樹脂刀片原型重量減輕了 7.3%,一旦標準制定完成,即可完全回收。

工程塑膠和複合材料的應用日益廣泛

由於阿科瑪公司將Lilsan PA11的產量提高了20%,以滿足電動車冷卻管路的需求,預計到2025年,這種生物基聚醯胺11將佔據汽車引擎室市場12%的佔有率。聚亞苯硫醚因其耐酸性,目前佔工業泵殼市場8%的佔有率。這消除了以往每例停機成本高達5萬至10萬美元的情況。儘管PEEK植入比聚碳酸酯貴15%,但它已將脊椎融合手術的再次手術率降低了30%,從而為每位患者節省了8000至12000美元的費用。碳纖維增強 PEEK 螺絲在屍體檢查中顯示出比鈦螺絲高 25% 的拔出強度,並於 2025 年獲得了美國 FDA 的三項新核准。 PLASTRON LFT 是 Polyplastics 公司於 2025 年推出的纖維素纖維混合物,可在維持全球 OEM 廠商所需衝擊強度的同時,將產品的碳足跡減少 30%。

高性能聚合物和複合材料高成本

截至2025年,PEEK的價格為每公斤60至80美元,是鋁壓鑄合金價格的8至12倍,這限制了其在消費性電子產品等對成本敏感的應用領域的使用。由於聚丙烯腈原料價格上漲12%,航太級碳纖維預浸料的價格已達到每公斤150美元,這延緩了複合材料在飛機二次零件的應用。聚亞苯硫醚的混煉需要價值800萬至1200萬美元的雙螺桿擠出機,而且全球只有不到20家專業製造商能夠提供這種材料。亞麻和麻纖維複合複合材料可以降低30%至40%的增強材料成本,但其8%的吸濕性會導致尺寸偏差,使其不適用於門模組等精密應用。再生碳纖維的價格為每公斤15至25美元,其抗張強度降低了20%至30%,因此其用途僅限於筆記型電腦機殼等非結構性產品。

細分市場分析

預計到2025年,工程塑膠將佔預計銷售額的62.50%。這主要歸功於聚醯胺在底盤零件領域的主導地位以及聚碳酸酯在電子設備機殼中的高強度應用。隨著亞洲碳纖維產量的增加,複合材料與聚碳酸酯的成本差異將縮小至每公斤20-25美元,預計到2031年,複合材料的複合年成長率將達到9.10%。由於聚碳酸酯易水解,5G天線製造商正在轉向聚亞苯硫醚。 ABS仍然是機殼的一種經濟實惠的選擇,價格為每公斤3美元,但其80°C的軟化點限制了其在非熱應用領域的應用。 PEEK、PEI和PPS等高性能材料在醫療和航太應用領域繼續鞏固其市場地位。

玻璃纖維增強塑膠的價格為每公斤1.50至2美元,廣泛用於汽車底盤護板和渦輪機殼體。儘管碳纖維的成本較高,為每公斤25至40美元,但碳纖維增強系統在航空航太車身面板和高階電動車車身結構中仍然至關重要。天然纖維複合材料主要用於歐洲的門板,其低碳排放備受重視。航太株式會社正在法國擴大碳纖維的生產規模,而海克塞爾公司的快速固化預浸料可將高壓釜週期縮短至兩小時,從而幫助熱固性樹脂保持其與熱塑性樹脂的競爭力。

區域分析

預計到2025年,亞太地區將佔全球銷售額的47.30%,這主要得益於中國600萬至800萬噸的工程塑膠產能以及日本在碳纖維前驅生產領域的主導地位。三井化學在中國擁有用於電動車電池托盤的長纖維聚丙烯工廠,而日本的東麗株式會社、帝人株式會社和三菱化學株式會社正在加強其在航太級原料領域的專業化生產。隨著製造商減少對中國的依賴,印度正在吸引新的聚合物投資,而韓國正在測試和營運碳纖維回收生產線,以滿足中國在2028年強制實施的8%再生纖維使用要求。東協正在擴大其市場佔有率,這得益於區域全面經濟夥伴關係協定(RCEP)下的關稅優惠以及比中國沿海地區低30%至40%的人事費用。

在北美,航太複合材料、底特律的輕量化舉措以及風力發電廠都受益於美國《通貨膨脹削減法案》提供的30%製造業稅額扣抵。BASF已將其路德維希港工廠的聚異丁烯產量提高了60%,以滿足電動車電池密封件的需求。同時,加拿大豐富的水力資源吸引了一家年產3,000噸的聚丙烯腈(PAN)纖維工廠落戶,該廠的碳排放量比中國一家燃煤工廠低40%。墨西哥則受益於美國《海事合作協定》(MCA)的國內採購規則,該規則促進了複合樹脂的近岸生產。

歐洲面臨高昂的能源成本挑戰,但受益於2030年嚴格的二氧化碳排放目標,並在以聚合物取代平均每輛乘用車100公斤鋼材方面取得了進展。 Syensqo和Arkema HAICoPAS聯合體已獲得歐洲航空安全局(EASA)對PEKK/碳纖維機身面板的批准。這將層壓時間從8小時縮短至45分鐘,並實現了閉合迴路維修流程。回收是英國的優先事項,Hexcel和Lavoisier將航太廢料轉化為碳纖維再生纖維,其成本比原生材料低40%。斯堪的納維亞製造商正在使用亞麻纖維面板,其碳纖維含量約為玻璃纖維的一半。在沙烏地阿美和Cienco投資300億美元建設垂直一體化複合材料園區的推動下,中東和非洲預計將實現9.07%的最高複合年成長率。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 汽車和航太領域都在不斷擴大輕量化趨勢。

- 工程塑膠和複合材料的應用日益廣泛

- 電動汽車零件製造的快速擴張

- 推廣用於減輕運輸設備重量的法規

- 透過人工智慧驅動的拓撲最佳化實現先進的聚合物組件設計。

- 市場限制因素

- 先進聚合物和複合材料高成本

- 在高應力和高溫應用的性能極限

- 多材料組件的回收及報廢階段所面臨的挑戰。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依材料類型

- 工程塑膠

- 聚醯胺(PA)

- 聚碳酸酯(PC)

- 丙烯腈丁二烯苯乙烯(ABS)

- 聚對苯二甲酸乙二醇酯(PET)

- 聚亞苯硫醚(PPS)

- 高性能聚合物(PEEK、PEI 等)

- 複合材料

- 玻璃纖維增強塑膠(GFRP)

- 碳纖維增強塑膠(CFRP)

- 天然纖維複合材料

- 工程塑膠

- 按最終用戶行業分類

- 車

- 航太/國防

- 工業設備和機械

- 建設基礎設施

- 醫療保健和醫療設備

- 消費品/電子設備

- 能源與公共產業

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Arkema

- Asahi Kasei Corporation

- BASF

- Celanese Corporation

- Covestro AG

- DSM

- DuPont

- Ensinger

- Evonik Industries AG

- Hexcel Corporation

- Jushi Group

- LANXESS

- LG Chem

- Mitsubishi Chemical Group

- Owens Corning Corporation

- RTP Company

- SABIC

- SGL Carbon SE

- Solvay

- Sumitomo Chemical Co., Ltd.

- Teijin Aramid

- TORAY INDUSTRIES INC.

- Victrex plc

第7章 市場機會與未來展望

According to Mordor Intelligence, the metal replacement market size is projected to be USD 171.35 billion in 2025, USD 184.84 billion in 2026, and reach USD 272.97 billion by 2031, growing at a CAGR of 8.11% from 2026 to 2031.

This report is Segmented by Material Type (Engineering Plastics and Composites), End-User Industry (Automotive, Aerospace and Defense, Industrial Equipment and Machinery, Construction and Infrastructure, Healthcare and Medical Devices, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Metal Replacement Market Trends and Insights

Growth in Automotive and Aerospace Lightweighting Trends

Battery-electric vehicles need to reduce 200-300 kg of chassis weight to offset the mass of lithium-ion batteries, leading automakers to replace underbody steel with glass-fiber polypropylene shields and carbon-fiber-reinforced thermoplastic battery enclosures that meet crash-worthiness standards while improving energy efficiency. Airbus validated a fully recyclable thermoplastic fuselage panel in 2025, which reduces manufacturing energy consumption by 40% compared to thermosets and allows for localized repairs, potentially lowering airline maintenance costs by 15-20% over a 25-year lifespan. Global wind-turbine capacity additions reached 117 GW in 2024, with composite blades now accounting for over 90% of rotor mass and reducing offshore foundation steel requirements by up to 40%. Hybrid carbon-glass designs approved by Sandia National Laboratories demonstrated a 44.7% increase in tensile strength, enabling rotor diameters to expand from 150 m to 180 m without proportional mass increases. Thermoplastic blades prototyped by Akelite in 2025 achieved an additional 7.3% weight reduction and full recyclability once standards are established.

Increasing Adoption of Engineering Plastics and Composites

Bio-based polyamide 11 captured 12% of the automotive under-hood market in 2025 after Arkema increased Rilsan PA11 production by 20% to meet EV cooling-line demand. Polyphenylene sulfide now holds 8% of the industrial pump housing market due to its acid resistance, which eliminates downtime previously costing operators USD 50,000-100,000 per incident. PEEK implants, despite being priced at a 15% premium over polycarbonate, have reduced spinal-fusion revision rates by 30%, saving USD 8,000-12,000 per patient. Carbon-fiber-reinforced PEEK screws demonstrated 25% greater pull-out strength than titanium in cadaveric tests, earning three new U.S. FDA clearances in 2025. Polyplastics' cellulose-fiber-blended PLASTRON LFT, launched in 2025, reduced the product carbon footprint by 30% while maintaining the impact strength required by global OEMs.

High Cost of Advanced Polymers and Composites

PEEK was priced at USD 60-80 per kg in 2025, eight to twelve times the cost of aluminum die-cast alloys, limiting its use in cost-sensitive applications such as appliances. Aerospace-grade carbon-fiber prepreg reached USD 150 per kg after a 12% increase in polyacrylonitrile feedstock prices, delaying composite adoption in secondary aircraft parts. Polyphenylene sulfide compounding requires USD 8-12 million twin-screw extruders, restricting supply to fewer than 20 global specialists. Flax and hemp composites reduce reinforcement costs by 30-40%, but their 8% moisture absorption causes dimensional drift, excluding them from precision applications like door modules. Recycled carbon fiber, priced at USD 15-25 per kg, has 20-30% lower tensile strength, limiting its use to non-structural products such as laptop shells.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Electric-Vehicle Component Manufacturing

- Regulatory Push for Transportation Lightweighting

- Performance Limits in High-Stress/High-Temperature Uses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Engineering plastics accounted for 62.50% of the projected 2025 revenue, driven by the dominance of polyamide in under-hood components and the strength of polycarbonate in electronics housings. Composites are anticipated to grow at a 9.10% CAGR through 2031, as Asian carbon-fiber production reduces the cost gap to USD 20-25 per kg. The susceptibility of polycarbonate to hydrolysis is encouraging 5G antenna manufacturers to shift toward polyphenylene sulfide. ABS remains a cost-effective option for appliance shells at USD 3 per kg, but its 80 °C softening point limits its use to non-thermal applications. High-performance materials like PEEK, PEI, and PPS continue to reinforce their niche roles in medical and aerospace applications.

Glass-fiber-reinforced plastics, priced at USD 1.50-2.00 per kg, are widely used in automotive underbody shields and turbine housings. Carbon-fiber-reinforced systems remain essential for aerospace skins and premium EV body structures, despite their higher fiber cost of USD 25-40 per kg. Natural-fiber composites are primarily utilized in European door panels, valued for their lower embedded carbon. Toray has expanded French carbon-fiber production, while Hexcel's rapid-cure prepreg reduces autoclave cycles to two hours, helping thermosets maintain competitiveness against thermoplastics.

Geography Analysis

Asia-Pacific is expected to contribute 47.30% of 2025 revenue, driven by China's 6-8 Mt engineering plastics capacity and Japan's leadership in carbon-fiber precursor production. China hosts Mitsui Chemicals' long-glass-fiber polypropylene plant for EV battery trays, while Japan's Toray, Teijin, and Mitsubishi Chemical strengthen their aerospace-grade feedstock specialization. India is attracting new polymer investments as manufacturers diversify from China, and South Korea is piloting carbon-fiber recycling lines to meet China's 2028 mandate for 8% recycled fiber. ASEAN nations are gaining market share due to tariff concessions under RCEP and labor costs 30-40% lower than coastal China.

In North America, aerospace composites, Detroit's lightweighting initiatives, and wind-energy installations are supported by the U.S. Inflation Reduction Act's 30% manufacturing tax credit. BASF has increased polyisobutylene output by 60% at Ludwigshafen to meet EV battery-seal demand, while Canada's hydropower resources have attracted a 3,000-ton PAN-fiber plant with a 40% lower carbon footprint compared to coal-powered Chinese facilities. Mexico benefits from USMCA content rules favoring near-shoring of compounded resins.

Europe faces challenges from high energy costs but benefits from stringent 2030 CO2 targets, driving steel-to-polymer substitutions averaging 100 kg per passenger car. The Syensqo and Arkema HAICoPAS consortium secured EASA approval for a PEKK/carbon-fiber fuselage panel, reducing lay-up time from 8 hours to 45 minutes and enabling closed-loop repair pathways. The UK emphasizes recycling, with Hexcel and Lavoisier converting aerospace scrap into Carbonium reclaimed fabric at 40% lower cost than virgin materials. Nordic builders are adopting flax-fiber panels with half the embodied carbon of glass fiber. The Middle-East and Africa are forecast to achieve the highest CAGR of 9.07%, supported by Saudi Aramco and Syensqo's USD 30 billion investment in a vertically integrated compositing park.

- Arkema

- Asahi Kasei Corporation

- BASF

- Celanese Corporation

- Covestro AG

- DSM

- DuPont

- Ensinger

- Evonik Industries AG

- Hexcel Corporation

- Jushi Group

- LANXESS

- LG Chem

- Mitsubishi Chemical Group

- Owens Corning Corporation

- RTP Company

- SABIC

- SGL Carbon SE

- Solvay

- Sumitomo Chemical Co., Ltd.

- Teijin Aramid

- TORAY INDUSTRIES INC.

- Victrex plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in automotive and aerospace lightweighting trends

- 4.2.2 Increasing adoption of engineering plastics and composites

- 4.2.3 Rapid expansion of electric-vehicle component manufacturing

- 4.2.4 Regulatory push for transportation lightweighting

- 4.2.5 AI-driven topology optimisation enhancing polymer part design

- 4.3 Market Restraints

- 4.3.1 High cost of advanced polymers and composites

- 4.3.2 Performance limits in high-stress/high-temperature uses

- 4.3.3 Recycling and end-of-life challenges for multi-material parts

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Engineering Plastics

- 5.1.1.1 Polyamide (PA)

- 5.1.1.2 Polycarbonate (PC)

- 5.1.1.3 Acrylonitrile-Butadiene-Styrene (ABS)

- 5.1.1.4 Polyethylene Terephthalate (PET)

- 5.1.1.5 Polyphenylene Sulfide (PPS)

- 5.1.1.6 High-Performance Polymers (PEEK, PEI, etc.)

- 5.1.2 Composites

- 5.1.2.1 Glass Fibre-Reinforced Plastics (GFRP)

- 5.1.2.2 Carbon Fibre-Reinforced Plastics (CFRP)

- 5.1.2.3 Natural-Fibre Composites

- 5.1.1 Engineering Plastics

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace and Defense

- 5.2.3 Industrial Equipment and Machinery

- 5.2.4 Construction and Infrastructure

- 5.2.5 Healthcare and Medical Devices

- 5.2.6 Consumer Goods and Electronics

- 5.2.7 Energy and Utilities

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Arkema

- 6.4.2 Asahi Kasei Corporation

- 6.4.3 BASF

- 6.4.4 Celanese Corporation

- 6.4.5 Covestro AG

- 6.4.6 DSM

- 6.4.7 DuPont

- 6.4.8 Ensinger

- 6.4.9 Evonik Industries AG

- 6.4.10 Hexcel Corporation

- 6.4.11 Jushi Group

- 6.4.12 LANXESS

- 6.4.13 LG Chem

- 6.4.14 Mitsubishi Chemical Group

- 6.4.15 Owens Corning Corporation

- 6.4.16 RTP Company

- 6.4.17 SABIC

- 6.4.18 SGL Carbon SE

- 6.4.19 Solvay

- 6.4.20 Sumitomo Chemical Co., Ltd.

- 6.4.21 Teijin Aramid

- 6.4.22 TORAY INDUSTRIES INC.

- 6.4.23 Victrex plc

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Growth potential in electric-vehicle manufacturing