|

市場調查報告書

商品編碼

2062072

鍍鋅鋼:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Galvanized Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

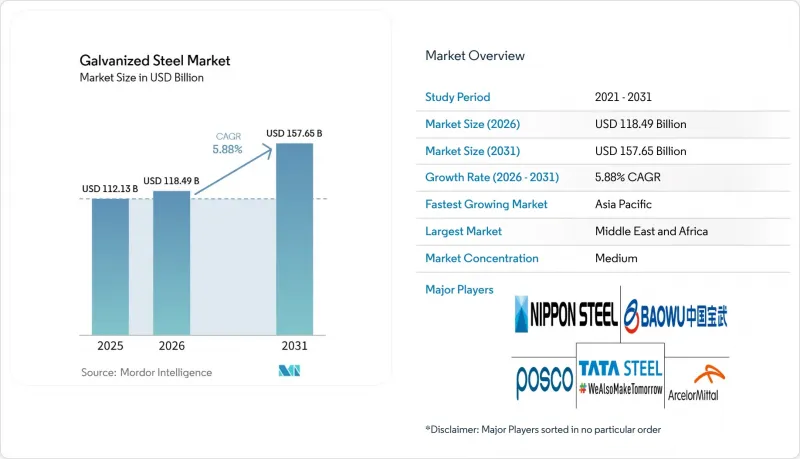

根據 Mordor Intelligence 預測,鍍鋅鋼市場規模將從 2025 年的 1121.3 億美元和 2026 年的 1184.9 億美元成長到 2031 年的 1576.5 億美元,2026 年至 2031 年的複合年成長率為 5.8%。

本報告按類型(例如,熱鍍鋅鋼)、形狀(例如,卷材/板材、管材/管件、線材)、應用(例如,建築、汽車、工業設備/機械)和地區(例如,亞太地區、北美、歐洲、南美、中東和非洲)進行細分。市場預測以價值(美元)表示。

全球鍍鋅鋼市場趨勢及洞察

來自建築和基礎設施行業的需求不斷成長

基於沙烏地阿拉伯「2030願景」和阿拉伯聯合大公國多元化策略的大規模交通走廊和綜合用途開發項目,正在推動鍍鋅鋼材需求的成長。例如,SeAH GSI在沙烏地阿拉伯投資2.4億美元建設工廠,以及EMSTEEL在阿拉伯聯合大公國投資6.25億迪拉姆拓展業務。埃及蘇伊士運河浮橋計畫於2025年使用超過8,000噸熱鍍鋅鋼材,這充分證明了該材料在海洋環境中的適用性。印度的公路和地鐵建設規劃正在提振國內需求,而中國的「一帶一路」計劃則向東南亞和非洲出口鋼捲和鋼板。在中等收入國家,鍍鋅樑和屋頂材料因其高耐久性而備受歡迎,預計2026年各國政府的獎勵策略將確保一系列多年期計畫的順利進行。這些因素共同支撐著鍍鋅鋼市場的持續成長。

汽車耐腐蝕性要求

在北美和歐洲,12 年的耐腐蝕保證已成為行業標準,該保證要求車身本體部件的鍍鋅層厚度達到 60 克/平方米或以上。蒂森克虜伯的「selectrify」電池外殼等創新產品在電動車 (EV) 平台上越來越受歡迎,與鋁製外殼相比,該外殼可降低 40% 的成本和 30% 的二氧化碳排放。Schneider Electric於 2025 年推出了專為工業環境設計的戶外充電器電鍍鋅機殼。預計到 2025 年,泰國的電動車產量將增加 20%,這將推動東南亞供應鏈對電鍍鋅鋼板的需求。高強度鍍鋅鋼材也被用於減輕電池重量,同時又不影響碰撞安全性,這提升了汽車產業鍍鋅鋼材的市場前景。

鋅、鐵和鋼鐵原料價格的波動

2026年第一季,鋅價均價為每噸3,280至3,650美元,較去年同期上漲12%至18%。此次上漲導致鍍鋅企業的利潤率下降200至300個基點。受能源成本上漲和配額限制收緊的影響,2026年3月歐洲熱軋捲板價格達到每噸713.57歐元。由於鋼廠優先生產高利潤的汽車鋼板,管材的前置作業時間延長至35天。一些缺乏避險能力的小規模鍍鋅企業正在退出低利潤率的領域,例如圍欄產品。儘管價格條款在一定程度上緩解了風險,但價格波動仍然是鍍鋅鋼板市場面臨的一大挑戰。

細分市場分析

預計到2031年,電鍍鋅鋼材的複合年成長率將達到6.21%,高於整體鍍鋅鋼材市場的平均成長率。這一成長主要歸功於汽車製造商對用於外露面板和電池外殼的更薄、更光滑的鍍層的需求。到2025年,熱鍍鋅鋼材將佔據鍍鋅鋼材市場73.26%的佔有率,這得益於其成本效益和適用於建築應用的更厚鍍層。Schneider Electric戶外充電器機殼的需求以及東南亞電動車產量的成長支撐了電鍍鋅鋼板市場的發展。受安賽樂米塔爾「Optigal」產品推出的推動,鋁鋅合金鍍層在太陽能和船舶屋頂材料等高階應用領域越來越受歡迎。合金和電鍍鋅兩大細分市場的共同努力,促進了鍍鋅鋼板產業的多元化發展。

電鍍鋅鋼因其良好的焊接性和塗料附著力而備受青睞,推動了家用電器對DX51D至S220GD等級、鍍鋅層厚度為40-100克/平方米的鍍鋅鋼的需求。家用電器製造商高度重視其成型性和耐腐蝕性的平衡,尤其是在潮濕地區。熱鍍鋅仍然是樑和屋頂材料的標準工藝,鍍層厚度為80-120克/平方米,是一種經濟高效的解決方案。雖然北美和歐洲對鍍鋁鋅的應用日益廣泛,但在印度和東南亞,其應用速度仍然緩慢。因此,鍍鋅鋼市場正經歷高附加價值精密電鍍和大量生產常規電鍍的雙重成長態勢。

區域分析

預計到2025年,亞太地區將佔全球銷售額的55.18%,這主要得益於中國新增99萬噸產能以及計畫於2026年新增的80萬噸產能。中國寶武和河鋼等領先製造商受惠於規模經濟,供應全球約70%的鍍鋅捲材。首鋼新建的鋅鎂鋁生產線正在為沿海基礎設施項目提供支持,該生產線廢鋼利用率超過50%,同時符合歐盟排放標準。由於地鐵和高速公路系統的擴建,印度的鍍鋅鋼板市場在2024年至2025年間有所成長。同時,東南亞地區的消費量也有所增加,越南的需求量達到150萬噸,印尼的500億美元基礎建設計畫也推動了這項成長。區域全面經濟夥伴協定(RCEP)下的關稅減讓進一步促進了區域內貿易。

預計到2031年,中東和非洲地區將以6.19%的複合年成長率實現最高成長速度,主要得益於沙烏地阿拉伯和阿拉伯聯合大公國的大型企劃。例如,SeAH GSI投資2.4億美元的管道廠以及EMSTEEL在阿拉伯聯合大公國年產能20萬噸的擴建項目,都對當地供應起到了支撐作用。 East Pipes Integrated投資7,850萬沙烏地里亞爾建設塗層生產線以及埃及運河大橋項目,都凸顯了造船用鋼需求的成長。儘管南非能源價格飆升,但輸電塔和圍欄的訂單為其提供了穩定性,並有助於該地區市場佔有率的擴大。

在北美,新增產能超過600萬短噸,其中以紐柯公司位於西維吉尼亞的生產線和加州鋼鐵公司計劃於2027年投產的項目最為突出。安賽樂米塔爾公司在阿拉巴馬州投資12億美元興建的電工鋼板廠和美國鋼鐵公司年產100萬噸的Big River 2鍍鋅生產線,體現了在「購買美國貨」政策支持下,製造業回流美國的努力。加拿大漢密爾頓計劃建造一座電弧爐(EAF),目標是在七年內減少60%的二氧化碳排放。這些發展透過多元化供應來源和應對碳邊境調節稅的風險,正在增強該地區的鍍鋅鋼板市場。

預計到2025年底,歐洲將面臨每噸80-85歐元的碳價,進口佔有率也將創下29%的歷史新高。安賽樂米塔爾正積極應對,斥資13億歐元在敦克爾克建設電弧爐(EAF)項目,計劃到2029年生產低碳鋼,並斥資4000萬波幣對其位於克拉科夫的Optigal工廠進行升級改造。儘管配額削減和對超額配額徵收50%的關稅將限制進口,但歐洲鋼鐵工業協會(EUROFER)預測,到2025年,消費量將回升2.4%。這些措施旨在保護本地市場的動態。

南美市場規模仍然小規模,其中巴西扮演主導角色。在巴西,蓋爾道公司正在升級其家用電器用鋼板生產線。阿根廷的經濟不穩定限制了進口,買家正轉向國內製造商。許多生產商依賴批量鍍鋅廠來生產建築屋頂材料和農業機械。長期成長取決於經濟穩定和基礎設施投資,但在當前情況下,市場仍然分散。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 來自建築和基礎設施行業的需求不斷成長

- 汽車耐腐蝕性要求

- 可再生能源相關結構(太陽能板安裝結構、風力渦輪機塔架)

- 輕型模組在異地和模組化住宅中的普及。

- 人工智慧驅動的預測性維護塗層品管系統

- 市場限制因素

- 鋅、鐵和鋼鐵原料價格的波動

- 替代金屬塗層(Al-Zn、Zn-Mg-Al)

- 對高排放鋼鐵廠徵收碳邊境調節關稅

- 價值鏈分析

- 監理情勢

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 熱鍍鋅鋼

- 電鍍鋅鋼

- 鍍鋁鋅鋼板/鋁鋅合金塗佈鋼板

- 按形式

- 捲材和片材

- 管道和管材

- 線材和桿

- 透過使用

- 建造

- 車

- 工業設備和機械

- 家用電器和暖通空調

- 能源公用事業

- 農業、圍欄和其他

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- AHMSA

- ArcelorMittal

- China Baowu Steel Group Corp., Ltd.

- Cleveland-Cliffs Inc.

- Gerdau S/A

- Hoa Sen Group

- Hyundai Steel

- JFE Steel Corp.

- Jindal Steel & Power

- JSW Steel Ltd.

- Liberty Steel Group

- NIPPON STEEL CORPORATION

- Nucor Corporation

- POSCO

- Salzgitter Flachstahl GmbH

- Severstal

- Shougang Group

- Tata Steel

- Thyssenkrupp AG

- United States Steel Corporation

- voestalpine Stahl GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the galvanized steel market size is projected to expand from USD 112.13 billion in 2025 and USD 118.49 billion in 2026 to USD 157.65 billion by 2031, registering a CAGR of 5.88% between 2026 to 2031.

This report is Segmented by Type (Hot-Dip Galvanized Steel, and More), Form (Coils and Sheets, Pipes and Tubes, Wires and Rods), Application (Construction, Automotive, Industrial Equipment and Machinery, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Galvanized Steel Market Trends and Insights

Growing Demand from Construction and Infrastructure

Large-scale transport corridors and mixed-use developments under Saudi Arabia's Vision 2030 and the UAE's diversification strategies are driving increased demand for coated steel, as evidenced by SeAH GSI's USD 240 million Saudi plant and EMSTEEL's AED 625 million UAE expansion. Egypt's Suez Canal floating bridge utilized over 8,000 tons of hot-dip galvanized sections in 2025, showcasing the material's suitability for marine environments. India's highway and metro development programs are boosting domestic demand, while China's Belt and Road Initiative is exporting coils and sheets to Southeast Asia and Africa. Middle-income economies continue to prefer galvanized beams and roofing for their durability, and government stimulus budgets in 2026 are expected to secure multi-year project pipelines. These factors collectively support sustained growth in the galvanized steel market.

Automotive Corrosion-Resistance Requirements

Twelve-year corrosion warranties, now standard in North America and Europe, mandate zinc coating weights of 60 g/m2 or higher on body-in-white components. Innovations like Thyssenkrupp's selectrify battery housing, which offers a 40% cost and 30% CO2 reduction compared to aluminum, are gaining popularity in electric vehicle (EV) platforms. Schneider Electric introduced electro-galvanized enclosures for outdoor chargers in 2025, designed for industrial environments. Thailand's EV production increased by 20% in 2025, driving demand for electro-galvanized sheets in Southeast Asian supply chains. High-strength galvanized grades are also being utilized to offset battery weight without compromising crash safety, reinforcing the market outlook for galvanized steel in the automotive sector.

Zinc and Steel Raw-Material Price Volatility

In the first quarter of 2026, zinc prices averaged USD 3,280-3,650 per ton, representing a 12%-18% increase compared to the previous year. This rise reduced galvanizer margins by 200-300 basis points. European hot-rolled coil prices reached EUR 713.57 per ton in March 2026, driven by energy cost inflation and stricter quota regulations. Lead times for tubing extended to 35 days as mills prioritized higher-margin automotive sheets. Smaller galvanizers without hedging capabilities are exiting low-margin segments such as fencing products. While price clauses provide some risk mitigation, volatility continues to challenge the galvanized steel market.

Other drivers and restraints analyzed in the detailed report include:

- Renewable-Energy Structures (Solar Frames, Wind Towers)

- Uptake of Lightweight Modules in Modular Housing

- Carbon-Border-Adjustment Tariffs on High-Emission Mills

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electro-galvanized steel grades are anticipated to grow at a 6.21% CAGR through 2031, exceeding the average growth rate of the galvanized steel market. This growth is attributed to automakers' demand for thinner and smoother coatings for exposed panels and battery housings. In 2025, hot-dip galvanized steel captured 73.26% of the galvanized steel market share due to its cost-effectiveness and thicker coatings, which are well-suited for construction applications. The market for electro-galvanized sheets is supported by Schneider Electric's outdoor charger enclosures and the increasing production of electric vehicles (EVs) in Southeast Asia. Aluminum-zinc alloy coatings are gaining traction in premium applications such as solar and marine roofing, driven by ArcelorMittal's Optigal product launch. Together, the alloy and electro-galvanized segments are contributing to a more diversified galvanized steel industry.

Electro-galvanized steel is preferred for its weldability and paint adhesion, which drive its demand in appliances requiring DX51D to S220GD grades with 40-100 g/m2 zinc coatings. Appliance manufacturers value its balance of formability and corrosion resistance, particularly in humid regions. Hot-dip galvanizing remains the standard for beams and roofing, where 80-120 g/m2 coatings provide cost-effective solutions. While Galvalume adoption is increasing in North America and Europe, it remains slower in India and Southeast Asia. Consequently, the galvanized steel market is experiencing simultaneous growth in high-value precision coatings and high-volume traditional coatings.

Geography Analysis

Asia-Pacific accounted for 55.18% of 2025 revenue, driven by China's 990-kiloton capacity addition and an additional 800 kilotons planned for 2026. Major producers like China Baowu and HBIS supply approximately 70% of global coated coil, benefiting from economies of scale. Shougang's new Zn-Mg-Al line supports coastal infrastructure projects while utilizing over 50% scrap, aligning with EU emission standards. India's metro and highway expansions boosted the local galvanized steel market in 2024-2025, while Southeast Asia saw increased consumption due to Vietnam's 1.5 million-ton demand and Indonesia's USD 50 billion infrastructure plan. RCEP tariff reductions further enhance intra-regional trade.

The Middle-East and Africa are expected to grow at the fastest rate of 6.19% CAGR through 2031, driven by megaprojects in Saudi Arabia and the UAE. Investments such as SeAH GSI's USD 240 million pipe mill and EMSTEEL's 200,000-tpy UAE expansion support localized supply. East Pipes Integrated's SAR 78.5 million investment in coating lines and Egypt's canal bridge project highlight marine-grade demand. Despite energy inflation in South Africa, tower and fencing orders provide stability, contributing to the region's growing market share.

North America is adding over 6 million short tons of new capacity, led by Nucor's West Virginia lines and California Steel's 2027 startup. ArcelorMittal's USD 1.2 billion electrical-steel plant in Alabama and U.S. Steel's 1 million-ton Big River 2 galvanizing line reflect reshoring efforts supported by Buy America policies. Canada's EAF proposals in Hamilton aim to reduce CO2 emissions by 60% within seven years. These developments diversify supply and address carbon-border risks, strengthening the region's galvanized steel market.

Europe faces EUR 80-85 per-tonne carbon prices and a record 29% import share in late 2025. ArcelorMittal is responding with a EUR 1.3 billion Dunkirk EAF producing low-CO2 steel by 2029 and a PLN 40 million Optigal upgrade in Krakow. Quota reductions and 50% over-quota duties limit import access, while EUROFER forecasts a 2.4% consumption recovery in 2025. These measures aim to protect local market dynamics.

South America remains a smaller market, led by Brazil, where Gerdau is upgrading lines for appliance sheets. Economic volatility in Argentina limits imports, pushing buyers toward domestic mills. Many producers rely on batch galvanizers to serve construction roofing and farm machinery. Long-term growth depends on economic stabilization and infrastructure investments, but current conditions keep the market fragmented.

- AHMSA

- ArcelorMittal

- China Baowu Steel Group Corp., Ltd.

- Cleveland-Cliffs Inc.

- Gerdau S/A

- Hoa Sen Group

- Hyundai Steel

- JFE Steel Corp.

- Jindal Steel & Power

- JSW Steel Ltd.

- Liberty Steel Group

- NIPPON STEEL CORPORATION

- Nucor Corporation

- POSCO

- Salzgitter Flachstahl GmbH

- Severstal

- Shougang Group

- Tata Steel

- Thyssenkrupp AG

- United States Steel Corporation

- voestalpine Stahl GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand from construction and infrastructure

- 4.2.2 Automotive corrosion-resistance requirements

- 4.2.3 Renewable-energy structures (solar frames, wind towers)

- 4.2.4 Uptake of lightweight modules in off-site and modular housing

- 4.2.5 AI-driven predictive-maintenance coating-quality systems

- 4.3 Market Restraints

- 4.3.1 Zinc and steel raw-material price volatility

- 4.3.2 Alternative metallic coatings (Al-Zn, Zn-Mg-Al)

- 4.3.3 Carbon-border-adjustment tariffs on high-emission mills

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Hot-Dip Galvanized Steel

- 5.1.2 Electro-Galvanized Steel

- 5.1.3 Galvalume/Al-Zn Alloy-Coated Steel

- 5.2 By Form

- 5.2.1 Coils and Sheets

- 5.2.2 Pipes and Tubes

- 5.2.3 Wires and Rods

- 5.3 By Application

- 5.3.1 Construction

- 5.3.2 Automotive

- 5.3.3 Industrial Equipment and Machinery

- 5.3.4 Home Appliances and HVAC

- 5.3.5 Energy and Utilities

- 5.3.6 Agriculture, Fencing and Others

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AHMSA

- 6.4.2 ArcelorMittal

- 6.4.3 China Baowu Steel Group Corp., Ltd.

- 6.4.4 Cleveland-Cliffs Inc.

- 6.4.5 Gerdau S/A

- 6.4.6 Hoa Sen Group

- 6.4.7 Hyundai Steel

- 6.4.8 JFE Steel Corp.

- 6.4.9 Jindal Steel & Power

- 6.4.10 JSW Steel Ltd.

- 6.4.11 Liberty Steel Group

- 6.4.12 NIPPON STEEL CORPORATION

- 6.4.13 Nucor Corporation

- 6.4.14 POSCO

- 6.4.15 Salzgitter Flachstahl GmbH

- 6.4.16 Severstal

- 6.4.17 Shougang Group

- 6.4.18 Tata Steel

- 6.4.19 Thyssenkrupp AG

- 6.4.20 United States Steel Corporation

- 6.4.21 voestalpine Stahl GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Galvanized Steel in EV Charging Stations and Battery Enclosures

- 7.3 Closed-Loop Recycling and "Green-Galv" Premiums

全球熱鍍鋅鋼市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球熱鍍鋅鋼市場規模、佔有率、趨勢和成長分析報告(2026-2034) 鍍鋅鋼板市場:2026-2032年全球市場預測(依塗層類型、產品形式、厚度、鋼材類型、厚度、最終用戶和銷售管道)鍍鋅鋼市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測鍍鋅鋼市場:2026-2032年全球市場預測(依產品類型、形狀、塗層類型、厚度、最終用途產業及分銷通路分類)抗靜電彩色鋼板市場:按應用、最終用途產業、塗層類型、厚度、顏色和分銷管道分類,全球預測(2026-2032年)

鍍鋅鋼板市場:2026-2032年全球市場預測(依塗層類型、產品形式、厚度、鋼材類型、厚度、最終用戶和銷售管道)鍍鋅鋼市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測鍍鋅鋼市場:2026-2032年全球市場預測(依產品類型、形狀、塗層類型、厚度、最終用途產業及分銷通路分類)抗靜電彩色鋼板市場:按應用、最終用途產業、塗層類型、厚度、顏色和分銷管道分類,全球預測(2026-2032年) 2026年全球熱鍍鋅鋼材市場報告2026年全球高壓鍍鋅管市場報告

2026年全球熱鍍鋅鋼材市場報告2026年全球高壓鍍鋅管市場報告 鍍鋅鋼板市場-全球產業規模、佔有率、趨勢、機會與預測:按應用、銷售管道、地區和競爭格局分類,2021-2031年Galfan鋼材市場依塗層厚度、產品類型、通路和最終用途產業分類-全球預測(2026-2032年)全球熱鍍鋅帶鋼市場(按塗層重量、鋼材類型、形狀、應用和最終用途行業分類)預測(2026-2032年)

鍍鋅鋼板市場-全球產業規模、佔有率、趨勢、機會與預測:按應用、銷售管道、地區和競爭格局分類,2021-2031年Galfan鋼材市場依塗層厚度、產品類型、通路和最終用途產業分類-全球預測(2026-2032年)全球熱鍍鋅帶鋼市場(按塗層重量、鋼材類型、形狀、應用和最終用途行業分類)預測(2026-2032年)