|

市場調查報告書

商品編碼

2062071

紡粘不織布:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Spunbond Nonwovens - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

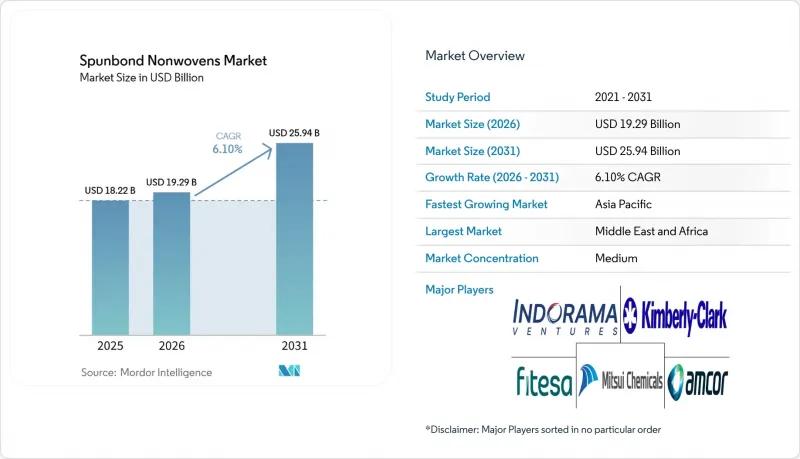

根據 Mordor Intelligence 預測,紡粘不織布市場規模預計在 2025 年達到 182.2 億美元,在 2026 年達到 192.9 億美元,在 2031 年達到 259.4 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 6.10%。

本報告按材料類型(聚丙烯、聚酯、聚乙烯及其他)、功能(一次性/耐用)、應用領域(個人護理、醫療、包裝及其他)和地區(亞太、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元計價。

全球紡粘不織布市場趨勢與洞察

新興經濟體對一次性衛生用品的需求激增

預計到2035年,印度紙尿褲市場規模將從2025年的19.96億美元成長至82.88億美元,主要成長動力來自雙職工家庭的增加、電子商務的普及以及農村地區推廣使用一次性紙尿褲的衛生項目。在印度尼西亞,雅加達的紙尿褲普及率高達70%,而農村地區僅為25%,這造成了兩極分化的需求模式,低紙張重量紡粘面層紙尿褲更受注重成本的消費者青睞。北美正在崛起為出口中心,Avgol公司投資1億美元在北卡羅來納州莫克斯維爾市建設一條多光束生產線,計劃於2025年建成,旨在為快速成長的亞洲市場供應高階衛生用品。寶潔和金佰利等全球性公司已在印度、越南和泰國建立了本地加工設施,縮短了前置作業時間,並能夠快速部署結合紡粘聚丙烯和天然纖維的 SKU,以滿足當地消費者的偏好。

醫療防護工具市場的擴張

醫院採購政策目前要求78%的手術罩衣訂單必須經過獨立認證,高於2024年的62%,這反映了ANSI/AAMI PB70:2022阻隔標準的日益嚴格。杜邦公司於2026年3月推出的Tyvek APX 400連身工作服,標誌著材料正向紡粘層壓材料轉變,這種材料在保持阻隔性的同時,也兼具透氣性,專為潔淨室和製藥環境而設計。增強型SMS罩衣在2025年佔銷售額的65%,但出貨量僅佔38%,凸顯了腫瘤科和移植手術感染控制方案推動的優質化趨勢。 ISO 13485:2016品質管理系統標準的協調統一,使得亞洲加工商能夠根據互認協議向西方醫院供應產品,從而加快跨境貿易和產品註冊流程。

聚丙烯的環境問題

法國、德國和荷蘭的生產者延伸責任制(EPR)機制現已對不可回收的聚丙烯產品徵收生態調節費,費用最高可達產品價格的20%,這導致仍依賴傳統紡粘工藝的加工商成本增加。由於黏合劑和橡膠會阻礙熔體流動,廢舊衛生用品的機械回收仍然困難重重,導致大多數市售聚丙烯產品中再生材料的含量不足5%。弗勞恩霍夫實驗室的溶劑溶解過程可將異種聚合物的摻入量減少80%,並生產出強度足以用於地工織物的紗線,但其高昂的溶劑回收要求阻礙了該工藝的廣泛應用。支持機構強調,ASTM D6400堆肥標準要求在180天內達到90%的分解率。傳統聚丙烯紡粘工藝無法達到這一標準,品牌所有者可能因此面臨「綠色清洗」的指控。

細分市場分析

2025年,聚丙烯在紡粘不織布市場仍佔據55.18%的佔有率,主要得益於其低廉的原料成本和較高的產能。然而,其他材料正在迅速崛起,預計到2031年,PLA和尼龍的複合年成長率將達到7.24%。聚酯纖維憑藉其卓越的拉伸強度,在對耐用性有較高要求的細分市場中佔據主導地位,並且儘管價格溢價高達20%,但在汽車內飾和地工織物領域,其市場佔有率仍在不斷擴大。 NatureWorks公司的「Ingeo 6500D PLA」的碳足跡比聚丙烯低62%,並且隨著加工商積極尋求PPWR(塑膠廢棄物減量)獎勵,PLA正擴大被用作衛生用品的表面層材料。預計到2026年,全球PLA產能將加倍,達到約100萬噸,從而緩解了先前阻礙其普及的供不應求。在聚丙烯 (PP) 領域,北歐化工的 HG485FB 牌號正在拓展單一材料設計的應用範圍,幫助加工商主動滿足可回收性法規要求,而無需進行昂貴的設備升級。尼龍紡粘膠目前仍是一個小眾市場,但隨著 Samsara Eco 等化學回收企業在 2028 年運作,預計市場將迎來成長。

像Kipaz和Mertem Kimya這樣的第二代機械回收商正在開發符合GRS認證的rPET切片的原料來源,使紡粘製造商能夠在不犧牲機械性能的前提下,達到其PPWR再生材料含量目標。這些變化描繪出一幅雙軌發展圖景:PP在短期內將保持其成本優勢,但隨著法規和消費者監督的日益嚴格,生物基和再生替代品將在價值鏈中佔據更高的位置。總體而言,聚合物多樣化將增加加工商的轉換成本,並可能進一步促進樹脂製造商和捲材供應商之間的合資,以確保未來的市場接受度。

區域分析

亞太地區在中國120萬噸產能和印度尿布市場兩位數成長的推動下,預計2025年將佔全球銷售額的39.10%。中國國內的產業結構調整,例如浙江金賽夫預計到2024年將以8.4億美元的銷售額位居全球第八,顯示該行業正從通用型產品轉向利潤更高的醫療和過濾等細分市場。日本市場環境自2025年以來發生了變化。帝人株式會社(Teijin)和旭化成株式會社(Asahi Kasei)合併了其技術紡織品部門,而東麗株式會社(Toray)則關閉了盈利能力較差的聚丙烯(PP)生產線,作為其「達爾文」成本削減計劃的一部分。東南亞仍然處於成長的前沿,隨著印尼和越南遍遠地區的尿布滲透率下降到 30% 以下,區域供應商正在透過最佳化基紙張重量來擴大其產品線,以吸引首次使用尿布的用戶。

北美的發展趨勢受垂直整合和近岸外包的影響。 Avgol位於莫克斯維爾的工廠不僅滿足了國內對衛生用品的需求,還利用美國強大的物流優勢出口到亞洲。美國食品藥物管理局(FDA)對醫用罩衣的規定促使醫院負責人選擇擁有ISO 13485認證的本地供應商或雙方認可的供應商,從而限制了低成本亞洲進口產品在關鍵醫用級產品領域的市場滲透。根據美墨加協定(USMCA),加拿大和墨西哥作為輔助樞紐,使美國品牌能夠免稅採購加工產品,並在卡車運輸三天內送達。

在歐洲,隨著2026年8月《塑膠包裝法規》(PPWR)的實施,監管力道正快速收緊。北歐化工(Borealis)、Fibertex和Suominen等公司正在投資建造符合法規要求的單一材料生產線,德國的原始設備製造商(OEM)也在仔細審查其供應鏈,以確保使用再生塑膠樹脂。基礎設施地工織物的需求正在向北歐國家轉移,海岸防護計畫正在消化先前由俄羅斯客戶採購的大量紡粘土捲材。中東和非洲是成長最快的地區,預計到2031年將以7.04%的複合年成長率成長。這主要得益於「2030願景」鐵路走廊的建設、指定使用紡粘土襯墊的海水淡化廠以及埃及快速發展的衛生用品行業(Gulsan在埃及的年運作4萬噸)。南美洲雖然規模較小,但也正在經歷加速成長。在巴西和阿根廷,雖然農村地區衛生用品的普及率較低,但政府主導的衛生改善宣傳活動正在進行中,Fitesa 12 億美元的銷售額凸顯了該地區的成長潛力。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 新興經濟體對一次性衛生用品的需求激增

- 醫療防護工具市場的擴張

- 與紡織品相比,具有成本和性能優勢

- 在應對氣候變遷的基礎設施中採用紡粘不織布地工織物

- 品牌所有者正在向單一材料PP包裝轉型

- 市場限制因素

- 與聚丙烯相關的環境問題

- 丙烯原料價格波動

- 高密度家具級工具機的寬度限制

- 價值鏈分析

- 監理情勢

- 波特五力模型

第5章 市場規模與成長預測

- 依材料類型

- 聚丙烯(PP)

- 聚酯(PET)

- 聚乙烯(PE)

- 其他材料類型(尼龍、PLA 等)

- 按功能

- 一次性的

- 耐久性

- 透過使用

- 個人護理

- 醫療保健

- 包裝

- 其他用途(汽車、過濾、農業、家具等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Ahlstrom

- Amcor plc

- Asahi Kasei Corporation

- Avgol Industries Ltd

- DuPont de Nemours, Inc.

- Fibertex Nonwovens A/S

- First Quality Nonwovens

- Fitesa SA

- Freudenberg Performance Materials

- Ginni Filaments Ltd.

- Hainan Huachen Nonwovens

- Indorama Ventures Public Company Limited

- Jofo Nonwoven Co., Ltd.

- Johns Manville

- KCWW

- Kolon Industries, Inc.

- Mitsui Chemicals, Inc.

- Mogul Nonwovens

- PFNonwovens(Pegas)

- RadiciGroup

- Shandong Ruxing Nonwovens

- Suominen Corporation

- Toray Industries, Inc.

- Xingshifa Group

第7章 市場機會與未來展望

According to Mordor Intelligence, the spunbond nonwovens market size is projected to be USD 18.22 billion in 2025, USD 19.29 billion in 2026, and reach USD 25.94 billion by 2031, growing at a CAGR of 6.10% from 2026 to 2031.

This report is Segmented by Material Type (Polypropylene, Polyester, Polyethylene, and Other Material Types), Function (Disposable and Durable), Application (Personal Hygiene, Medical, Packaging, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Spunbond Nonwovens Market Trends and Insights

Surging Demand for Hygiene Disposables in Emerging Economies

India's diaper market is projected to grow from USD 1.996 billion in 2025 to USD 8.288 billion by 2035, driven by dual-income families, increased e-commerce access, and sanitation programs that are promoting disposable products in smaller cities. In Indonesia, rural areas lag behind with only 25% diaper penetration compared to 70% in Jakarta, creating a two-tiered demand pattern that favors low-basis-weight spunbond topsheets optimized for cost-sensitive consumers. North America is emerging as an export hub after Avgol installed a USD 100 million multi-beam line in Mocksville, North Carolina, in 2025 to supply premium hygiene materials to fast-growing Asian markets. Global players such as Procter & Gamble and Kimberly-Clark have localized converting operations in India, Vietnam, and Thailand, reducing lead times and enabling rapid SKU rollouts that combine spunbond polypropylene with natural fibers to cater to regional preferences.

Expansion of Medical Protective-Gear Market

Hospital procurement policies now require independent certification for 78% of surgical gown orders, up from 62% in 2024, reflecting stricter ANSI/AAMI PB70:2022 barrier standards. DuPont's Tyvek APX 400 coveralls, launched in March 2026, demonstrate a shift toward breathable yet high-barrier spunbond-based laminates designed for clean-room and pharmaceutical environments. Reinforced SMS gowns accounted for 65% of 2025 revenue despite representing only 38% of shipped units, highlighting a premiumization trend driven by infection-control protocols for oncology and transplant surgeries. Harmonized ISO 13485:2016 quality-system standards have enabled Asian converters to serve Western hospitals under mutual-recognition agreements, accelerating cross-border trade and product registration timelines.

Environmental Concerns over Polypropylene

Extended producer responsibility schemes in France, Germany, and the Netherlands now impose eco-modulation fees of up to 20% of product value on non-recyclable polypropylene items, increasing costs for converters still reliant on conventional spunbond. Mechanical recycling of post-consumer hygiene products remains challenging because adhesives and elastics degrade melt flow, keeping recycled-content inclusion below 5% in most commercial polypropylene grades. Fraunhofer's solvent-based dissolution process reduces foreign-polymer contamination by 80% and produces yarns strong enough for geotextiles, but its capital-intensive solvent recovery requirements hinder widespread adoption. Advocacy groups emphasize that ASTM D6400 compostability standards require 90% degradation within 180 days, a benchmark traditional polypropylene spunbond cannot meet, exposing brand owners to accusations of greenwashing.

Other drivers and restraints analyzed in the detailed report include:

- Cost- and Performance-Advantage over Woven Fabrics

- Brand-Owner Shift to Mono-Material PP Packaging

- Volatility in Propylene Feedstock Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polypropylene retained a 55.18% share of the spunbond nonwovens market size in 2025 on the back of low raw-material costs and high throughput, yet other material types are moving quickly, with PLA, nylon, etc. forecast at a 7.24% CAGR to 2031. Polyester commands the durable niche because of its elevated tensile performance, winning share in automotive interiors and geotextiles, even at a 20% price premium. NatureWorks' Ingeo 6500D PLA, which carries a 62% lower carbon footprint than PP, is being adopted for hygiene topsheets as converters pursue PPWR incentives. With global PLA capacity expected to double to roughly 1 million tons by 2026, availability fears that once dampened adoption are fading. On the polypropylene side, Borealis' HG485FB grade is expanding the mono-material design window, helping converters keep ahead of recyclability mandates without costly equipment upgrades. Nylon spunbond remains niche but could scale once chemical-recycling ventures such as Samsara Eco's plant come on-stream in 2028.

Second-generation mechanical recyclers like Kipas and Meltem Kimya are opening feedstock taps for GRS-certified rPET chips, letting spunbond producers hit PPWR recycled-content targets without surrendering mechanical performance. These shifts frame a two-track outlook: PP holds near-term cost advantage; bio-based and recycled alternatives climb the value chain as regulation and consumer scrutiny tighten. Overall, polymer diversification raises switching costs for converters and could spur more joint ventures between resin makers and roll-goods suppliers to secure forward offtake.

Geography Analysis

Asia-Pacific locked in 39.10% of global revenue in 2025, supported by China's 1.2 million-ton installed capacity and India's double-digit diaper growth. Chinese consolidation, Zhejiang Kingsafe ranked eighth worldwide with USD 840 million sales in 2024, signals an industry pivot from commodity grades to higher-margin medical and filtration niches. Japan's landscape shifted after 2025, when Teijin and Asahi Kasei merged technical-textile units, while Toray closed unprofitable PP lines under its Darwin cost-saving program. Southeast Asia remains the frontier; Indonesia and Vietnam boast rural diaper penetration below 30%, so regional suppliers are adding basis-weight-optimized lines to capture first-time users.

North American dynamics are shaped by vertical integration and nearshoring. Avgol's Mocksville plant addresses domestic hygiene needs but also exports to Asia, leveraging U.S. logistics resilience. FDA surgical-gown regulations steer hospital buyers toward ISO-13485-certified local or mutual-recognition suppliers, limiting penetration by low-cost Asian imports in critical medical grades. Canada and Mexico act as auxiliary hubs under USMCA, giving U.S. brands tariff-free, three-day truck access to converted goods.

Europe is firmly in regulatory overdrive as PPWR applicability arrives in August 2026. Borealis, Fibertex, and Suominen are pouring funds into compliant mono-material lines, and German OEMs are scrutinizing supply chains to guarantee post-consumer resin inclusion. Infrastructural geotextile demand is shifting toward Nordic countries, where coastal-protection projects soak up spunbond rolls that Russian customers would previously have taken. Middle-East and Africa is the fastest-growing region at a 7.04% CAGR through 2031, buoyed by Vision 2030 rail corridors and desalination plants that specify spunbond underlayers, and by Egypt's burgeoning hygiene complex where Gulsan runs 40,000 tons per year of installed capacity. South America is smaller but accelerating: Brazil and Argentina combine low rural hygiene penetration with state-backed sanitation drives, and Fitesa's USD 1.2 billion sales underline the region's scaling potential.

- Ahlstrom

- Amcor plc

- Asahi Kasei Corporation

- Avgol Industries Ltd

- DuPont de Nemours, Inc.

- Fibertex Nonwovens A/S

- First Quality Nonwovens

- Fitesa S.A.

- Freudenberg Performance Materials

- Ginni Filaments Ltd.

- Hainan Huachen Nonwovens

- Indorama Ventures Public Company Limited

- Jofo Nonwoven Co., Ltd.

- Johns Manville

- KCWW

- Kolon Industries, Inc.

- Mitsui Chemicals, Inc.

- Mogul Nonwovens

- PFNonwovens (Pegas)

- RadiciGroup

- Shandong Ruxing Nonwovens

- Suominen Corporation

- Toray Industries, Inc.

- Xingshifa Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Hygiene Disposables in Emerging Economies

- 4.2.2 Expansion of Medical Protective-gear Market

- 4.2.3 Cost- and Performance-advantage over Woven Fabrics

- 4.2.4 Adoption of Spunbond Geotextiles in Climate-Resilient Infrastructure

- 4.2.5 Brand-owner Shift to Mono-material PP Packaging

- 4.3 Market Restraints

- 4.3.1 Environmental Concerns over Polypropylene

- 4.3.2 Volatility in Propylene Feedstock Pricing

- 4.3.3 Machine-width Limits for High-loft Furniture Grades

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Polypropylene (PP)

- 5.1.2 Polyester (PET)

- 5.1.3 Polyethylene (PE)

- 5.1.4 Other Material Types (Nylon, PLA, etc.)

- 5.2 By Function

- 5.2.1 Disposable

- 5.2.2 Durable

- 5.3 By Application

- 5.3.1 Personal Hygiene

- 5.3.2 Medical

- 5.3.3 Packaging

- 5.3.4 Other Applications (Automotive, Filtration, Agriculture, Furniture, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Ahlstrom

- 6.4.2 Amcor plc

- 6.4.3 Asahi Kasei Corporation

- 6.4.4 Avgol Industries Ltd

- 6.4.5 DuPont de Nemours, Inc.

- 6.4.6 Fibertex Nonwovens A/S

- 6.4.7 First Quality Nonwovens

- 6.4.8 Fitesa S.A.

- 6.4.9 Freudenberg Performance Materials

- 6.4.10 Ginni Filaments Ltd.

- 6.4.11 Hainan Huachen Nonwovens

- 6.4.12 Indorama Ventures Public Company Limited

- 6.4.13 Jofo Nonwoven Co., Ltd.

- 6.4.14 Johns Manville

- 6.4.15 KCWW

- 6.4.16 Kolon Industries, Inc.

- 6.4.17 Mitsui Chemicals, Inc.

- 6.4.18 Mogul Nonwovens

- 6.4.19 PFNonwovens (Pegas)

- 6.4.20 RadiciGroup

- 6.4.21 Shandong Ruxing Nonwovens

- 6.4.22 Suominen Corporation

- 6.4.23 Toray Industries, Inc.

- 6.4.24 Xingshifa Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment