|

市場調查報告書

商品編碼

2062069

電磁干擾(EMI)屏蔽:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)Electromagnetic Interference (EMI) Shielding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

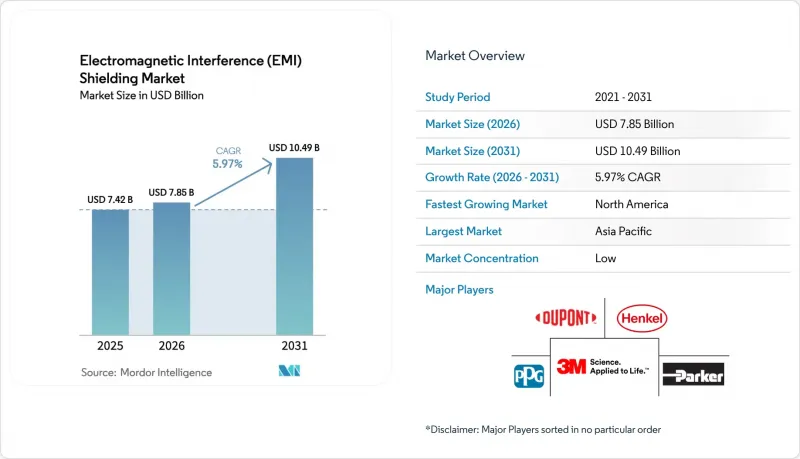

據 Mordor Intelligence 稱,2025 年電磁干擾 (EMI) 屏蔽市場價值為 74.2 億美元,預計到 2031 年將達到 104.9 億美元,而 2026 年為 78.5 億美元,預測期(2026-2031 年)的複合年成長率為 5.97%。

本報告材料類型(金屬屏蔽、其他)、屏蔽方法(三防膠、墊片屏蔽、其他)、應用領域(消費性電子產品和穿戴式裝置、其他)、形態(片材和泡棉、其他)以及地區(亞太地區、北美地區、歐洲地區、其他地區)進行細分。市場預測以美元計價。

全球電磁干擾 (EMI) 屏蔽市場趨勢及洞察

家用電器和穿戴式裝置的廣泛應用

隨著智慧型手機、智慧型手錶和耳機體積的不斷縮小,工程師現在要求屏蔽層厚度小於10微米,同時在2.4-6GHz頻段維持60dB或更高的衰減效能。基於MXene的織物單層衰減性能可達42dB,三層堆疊結構可達69dB,並且能夠承受超過500次的彎曲,使其成為穿戴式裝置曲面應用的理想選擇。折疊式智慧型手機的鉸鏈能夠承受超過20萬次的彎曲。銀奈米線油墨即使在50%的應變下也能保持31,000 S/cm的導電性,從而防止射頻洩漏通道的形成。隨著透明、可拉伸和可水洗薄膜技術的日益成熟,擁有捲對輥塗線的供應商有望超越傳統的金屬罐供應商。

快速部署5G/毫米波基礎設施

26 GHz 和 39 GHz 毫米波基地台需要基板級屏蔽,其屏蔽等級至少為 80 dB,因為低損耗聚四氟乙烯 (PTFE) 和液晶聚合物基板會放大輻射。隨著美國聯邦通訊委員會 (FCC) 第 15 部分和歐洲電訊標準協會 (ETSI) EN 301 489 標準在 2024 年變得更加嚴格,原始設備製造商 (OEM) 目前正在採購整合導熱孔和電磁干擾 (EMI) 墊片的模製組件,以簡化其製造流程。預計到 2028 年,北美的小型基地台數量將超過一百萬個,而華盛頓特區附近的資料中心營運商在發生圖形處理器 (GPU) 記憶體故障事件後,已經開始對機架進行改造,加裝 60-80 dB 的屏蔽面板。

先進屏蔽材料和製程高成本

奈米材料薄膜的成本可能超過每公斤200美元,是鍍鎳碳纖維價格的十倍。真空濺鍍設備造價超過50萬美元,運作週期為30-60分鐘;而超音波鍍膜設備的初始投資較低,約5萬美元,但會增加油墨配方的複雜性。獲得認證會使研發預算增加15-20%,因此,沒有內部電磁相容性(EMC)檢查室的中小型企業將面臨產品上市延遲的問題。

細分市場分析

預計到2025年,導電塗料和油漆將佔銷售額的32.70%。這要歸功於它們與噴塗、刷塗和浸塗等工藝的兼容性,無需大量資本投資或設備改造即可無縫整合到現有生產線中。在需要高可靠性的應用中,例如需要80 dB或更高衰減的航空電子設備艙,金屬屏蔽仍然佔據主導地位。

預計到2031年,導電聚合物和複合材料的複合年成長率將達到6.12%,這引起了尋求海洋和戶外通訊設備機殼耐腐蝕性能的設計人員的關注。聚苯胺/鎳鐵氧體複合材料透過吸收主導機制,在K波段實現了78.07 dB的屏蔽效果,其綠色指數超過1.0。這表明,與歐盟REACH法規禁止使用的六價鉻表面處理相比,該複合材料具有環境優勢。混合TPU複合材料目前的電導率為312 S/cm,這使得提供多材料組合的供應商能夠在日益萎縮的供應商名單中實現交叉銷售。

預計到2025年,基於墊片的屏蔽層將佔據53.15%的市場佔有率,在預測期(2026-2031年)內將以6.23%的複合年成長率成長。這主要得益於汽車原始設備製造商(OEM)指定使用導電彈性體和泡棉覆蓋的墊片,這些墊片在10萬次車門開關循環後仍能保持低於1Ω的接觸電阻,並能承受高達125 度C的引擎室溫度。雖然基板級屏蔽層正在贏得智慧型手機和物聯網模組的需求,但隨著模組供應商轉向在基板製造過程中整合模塑屏蔽層,該細分市場的利潤率正面臨壓力。

三防膠適用於成本要求較高的消費性應用、機上盒和智慧音箱。噴塗的銀或鎳漆可提供 30–50 dB 的衰減,符合 FCC Part 15 B 類標準,無需模具投入。電纜屏蔽和機殼/通風屏蔽則面向基礎設施市場。資料中心營運商在安裝液冷 AI 機架時,需要帶有蜂巢網格的射頻屏蔽通風面板,該面板可在 1–6 GHz 頻段提供 60–80 dB 的衰減,同時保持 200 CFM 以上的風量,以防止過熱降頻。

區域分析

預計到2025年,亞太地區將佔全球銷售額的41.40%。這主要得益於中國電子製造地的發展,其中深圳和東莞的叢集組裝了全球超過60%的智慧型手機和穿戴式裝置;此外,印度不斷擴大的電動車電池產能也推動了對電池管理系統(BMS)屏蔽層的需求。日本高性能鐵氧體磁芯(用於2-6 GHz模組)的市場規模約為9億美元。韓國在5G領域的領先地位以及三星的投資正在推動晶片屏蔽層的需求,而新加坡和雅加達的資料中心對通風面板的需求也在激增。

預計到2031年,北美將以6.55%的複合年成長率實現最快成長,這得益於超大規模資料中心的擴張和5G基礎設施的投資。到2025年,光是北維吉尼亞就佔該地區EMI屏蔽通風面板消耗量的30%以上,因為業者開始在同一設施內部署GPU叢集和邊緣節點。

預計到2025年,歐洲將佔據相當大的市場佔有率,這主要得益於德國的汽車和工業基礎,以及歐盟REACH法規加速了從六價鉻酸鹽塗層向導電聚合物的轉變。法國的航太和國防領域對防雷電纜屏蔽層和符合MIL-STD-461G標準的防護機殼有著迫切的需求,而英國則透過5G部署和智慧電網投資,為通訊和工業自動化領域提供支援。南美、中東和非洲仍是新興市場,巴西的航太叢集和阿拉伯聯合大公國的智慧城市計畫提供了獨特的機遇,但與成熟市場相比,當地製造業的限制和對進口的高度依賴限制了其成長。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 家用電器和穿戴式裝置的快速普及。

- 快速部署5G/毫米波基礎設施

- 加強汽車、醫療和航空航太領域的全球電磁相容性法規

- 特定產業的衛星星系正在推動對飛行中屏蔽的需求。

- 先進封裝中晶片和系統級封裝元件的隔間級屏蔽

- 市場限制因素

- 先進屏蔽材料和製程高成本

- 超小型和折疊式設備的外形規格限制

- 銅價波動增加了大規模生產項目中物料清單 (BOM) 的風險。

- 價值鏈分析

- 監理情勢

- 波特五力模型

第5章 市場規模與成長預測

- 依材料類型

- 導電塗料和油漆

- 金屬護盾

- 導電聚合物和複合材料

- EMI/EMC濾波器

- 膠帶和覆膜

- 碳基泡沫和奈米材料薄膜

- 屏蔽方法

- 三防膠

- 墊片護罩

- 基板級屏蔽

- 電纜屏蔽

- 機殼和通風罩

- 透過使用

- 家用電子電器和穿戴式裝置

- 汽車和電動車

- 通訊和5G/6G基礎設施

- 航太、國防、電動垂直起降飛行器

- 醫療保健和醫療設備

- 工業設備及自動化

- 可再生能源和智慧電網

- 資料中心和雲端基礎設施

- 按形狀

- 薄膜和塗層

- 墊片和O形圈

- 表格和表格

- 織品/軟紡織品

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太國家

- 中東和非洲

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Changzhou National Radio-Products Factory

- DuPont

- ETS-Lindgren

- Henkel AG & Co. KGaA

- Holland Shielding Systems BV

- Kitagawa Industries Co., Ltd.

- Leader Tech Inc.

- MG Chemicals

- Mobix Labs

- Nolato AB

- Parker Hannifin Corp

- PPG Industries Inc.

- RTP Company

- Schaffner Holding AG

- Sekisui Chemical Co., Ltd.

- Shin-Etsu Polymer Co., Ltd.

- Sidus Space

- TDK Corporation

- Tech-Etch Inc.

- WL Gore & Associates Inc.

- YShield GmbH & Co. KG

第7章 市場機會與未來展望

According to Mordor Intelligence, the electromagnetic interference shielding market size was valued at USD 7.42 billion in 2025 and is estimated to grow from USD 7.85 billion in 2026 to reach USD 10.49 billion by 2031, at a CAGR of 5.97% during the forecast period (2026-2031).

This report is Segmented by Material Type (Metal Shielding, and More), Shielding Method (Conformal Coating, Gasket Shielding, and More), Application (Consumer Electronics and Wearables, and More), Form Factor (Sheets and Foams and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Electromagnetic Interference (EMI) Shielding Market Trends and Insights

Surging Adoption of Consumer Electronics and Wearables

Smartphones, smartwatches, and earbuds are shrinking, so engineers now specify shielding layers thinner than 10 μm that still deliver over 60 dB attenuation from 2.4-6 GHz. MXene-based fabrics achieve 42 dB in a single layer and 69 dB in triple stacks while enduring more than 500 bends, making them ideal for curved wearable surfaces. Foldable-phone hinges flex over 200,000 times; silver-nanowire inks keep 31,000 S/cm conductivity even under 50% strain, preventing RF leakage paths. As transparent, stretchable, and washable films mature, suppliers with roll-to-roll coating lines will outpace traditional metal-can vendors.

Rapid 5G/mm-Wave Infrastructure Rollout

Millimeter-wave base stations at 26 GHz and 39 GHz need board-level shields rated above 80 dB because low-loss polytetrafluoroethylene (PTFE) and liquid-crystal-polymer substrates amplify radiated emissions. Federal Communications Commission (FCC) Part 15 and European Telecommunications Standards Institute (ETSI) EN 301 489 tightened in 2024, so OEMs (Original Equipment Manufacturers) now buy molded assemblies that combine thermal vias and EMI gaskets, cutting production steps. North American small-cell counts are on track to top 1 million by 2028, and data-center operators near Washington D.C. already retrofit racks with 60-80 dB panels after graphics processing unit (GPU) memory-error incidents.

High Cost of Advanced Shielding Materials and Processes

Nanomaterial films can exceed USD 200 per kg, ten times the price of nickel-coated carbon fibers. Vacuum sputtering tools cost above USD 500,000 and run 30-60 minute cycles, while ultrasonic coaters have lower capital needs, at roughly USD 50,000, but add ink-formulation complexity. Certification adds 15-20% to development budgets, so small firms without in-house Electromagnetic Compatibility (EMC) labs face delayed launches.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Global EMC Regulations in Auto, Medical and Aero Sectors

- Chiplet and SiP Compartment-Level Shielding in Advanced Packaging

- Copper-Price Volatility Elevating BOM Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conductive coatings and paints controlled 32.70% of revenue in 2025, sustained by their compatibility with spray, brush, and dip-coating processes that integrate seamlessly into existing production lines without capital-intensive tooling changes. Metal shielding still dominates high-robustness roles such as avionics bays that need more than 80 dB attenuation.

Conductive polymers and composites will grow at 6.12% CAGR to 2031, attract designers seeking corrosion immunity in marine and outdoor telecom enclosures; polyaniline/nickel-ferrite composites achieved 78.07 dB shielding effectiveness in K-band with absorption-dominant mechanisms and Green Index above 1.0, signaling environmental advantages over hexavalent-chromate surface treatments banned under EU REACH. Hybrid TPU composites now post 312 S/cm conductivity, so suppliers offering multi-material portfolios can cross-sell within shrinking vendor lists.

Gasket Shielding held 53.15% method share in 2025 and will grow at 6.23% CAGR during the forecast period (2026-2031), propelled by automotive OEMs specifying conductive-elastomer and fabric-over-foam gaskets that maintain less than 1 Ω contact resistance across 100,000 door-open cycles and withstand underhood temperatures reaching 125°C. Board-Level Shielding captures smartphone and IoT-module demand, yet this segment faces margin pressure as module vendors shift to molded shielding integrated during substrate fabrication.

Conformal Coating serves cost-sensitive consumer applications, set-top boxes, and smart speakers, where spray-applied silver or nickel paints deliver 30-50 dB attenuation sufficient for FCC Part 15 Class B compliance without tooling investment. Cable Shielding and Enclosure and Vent Shielding address infrastructure markets: data-center operators installing liquid-cooled AI racks require RF-shielded ventilation panels with honeycomb mesh that attenuates 60-80 dB at 1-6 GHz while sustaining airflow above 200 CFM to prevent thermal throttling.

Geography Analysis

Asia-Pacific commanded 41.40% of revenue in 2025, anchored by China's electronics-manufacturing base, where Shenzhen and Dongguan clusters assemble over 60% of global smartphones and wearables, and India's expanding EV cell-production capacity, which is attracting battery-management-system shielding demand. Japan logged about USD 900 million on advanced ferrite cores for 2-6 GHz modules. South Korea's 5G leadership and Samsung investments uplift chiplet shielding, while Singapore and Jakarta data centers spike vent-panel demand.

North America, forecast to grow fastest at 6.55% CAGR through 2031, benefits from hyperscale data-center expansion and 5G infrastructure investment; Northern Virginia alone accounted for over 30% of regional EMI-shielding ventilation-panel consumption in 2025 as operators co-locate GPU clusters and edge nodes within the same facilities.

Europe held a significant share in 2025, driven by Germany's automotive and industrial base and stringent EU REACH regulations that accelerate the substitution of hexavalent-chromate coatings with conductive polymers. France's aerospace and defense sectors demand lightning-strike-certified cable shields and MIL-STD-461G enclosures, while the United Kingdom's 5G rollout and smart-grid investments support telecom and industrial-automation segments. South America and Middle East and Africa remain emerging markets, with Brazil's aerospace clusters and UAE's smart-city projects providing niche opportunities, yet limited local manufacturing and reliance on imports constrain growth relative to established regions.

- 3M

- Changzhou National Radio-Products Factory

- DuPont

- ETS-Lindgren

- Henkel AG & Co. KGaA

- Holland Shielding Systems BV

- Kitagawa Industries Co., Ltd.

- Leader Tech Inc.

- MG Chemicals

- Mobix Labs

- Nolato AB

- Parker Hannifin Corp

- PPG Industries Inc.

- RTP Company

- Schaffner Holding AG

- Sekisui Chemical Co., Ltd.

- Shin-Etsu Polymer Co., Ltd.

- Sidus Space

- TDK Corporation

- Tech-Etch Inc.

- W. L. Gore & Associates Inc.

- YShield GmbH & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging adoption of consumer electronics and wearables

- 4.2.2 Rapid 5G/mm-Wave infrastructure rollout

- 4.2.3 Stricter global EMC regulations in auto, medical and aero sectors

- 4.2.4 Vertical-specific satellite constellations driving on-board shielding demand

- 4.2.5 Chiplet and SiP compartment-level shielding in advanced packaging

- 4.3 Market Restraints

- 4.3.1 High cost of advanced shielding materials and processes

- 4.3.2 Form-factor constraints in ultra-compact and foldable devices

- 4.3.3 Copper-price volatility elevating BOM risk in large-volume programs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Conductive Coatings and Paints

- 5.1.2 Metal Shielding

- 5.1.3 Conductive Polymers and Composites

- 5.1.4 EMI/EMC Filters

- 5.1.5 Tapes and Laminates

- 5.1.6 Carbon-based Foams and Nanomaterial Films

- 5.2 By Shielding Method

- 5.2.1 Conformal Coating

- 5.2.2 Gasket Shielding

- 5.2.3 Board-Level Shielding

- 5.2.4 Cable Shielding

- 5.2.5 Enclosure and Vent Shielding

- 5.3 By Application

- 5.3.1 Consumer Electronics and Wearables

- 5.3.2 Automotive and Electric Vehicles

- 5.3.3 Telecommunications and 5G/6G Infrastructure

- 5.3.4 Aerospace, Defense and eVTOL

- 5.3.5 Healthcare and Medical Devices

- 5.3.6 Industrial Equipment and Automation

- 5.3.7 Renewable Energy and Smart Grid

- 5.3.8 Data Centers and Cloud Infrastructure

- 5.4 By Form Factor

- 5.4.1 Films and Coatings

- 5.4.2 Gaskets and O-Rings

- 5.4.3 Sheets and Foams

- 5.4.4 Fabric/Flexible Textiles

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Asia-Pacific

- 5.5.5.1 China

- 5.5.5.2 India

- 5.5.5.3 Japan

- 5.5.5.4 South Korea

- 5.5.5.5 Rest of Asia-Pacific

- 5.5.6 Middle-East and Africa

- 5.5.6.1 South Africa

- 5.5.6.2 United Arab Emirates

- 5.5.6.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Changzhou National Radio-Products Factory

- 6.4.3 DuPont

- 6.4.4 ETS-Lindgren

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 Holland Shielding Systems BV

- 6.4.7 Kitagawa Industries Co., Ltd.

- 6.4.8 Leader Tech Inc.

- 6.4.9 MG Chemicals

- 6.4.10 Mobix Labs

- 6.4.11 Nolato AB

- 6.4.12 Parker Hannifin Corp

- 6.4.13 PPG Industries Inc.

- 6.4.14 RTP Company

- 6.4.15 Schaffner Holding AG

- 6.4.16 Sekisui Chemical Co., Ltd.

- 6.4.17 Shin-Etsu Polymer Co., Ltd.

- 6.4.18 Sidus Space

- 6.4.19 TDK Corporation

- 6.4.20 Tech-Etch Inc.

- 6.4.21 W. L. Gore & Associates Inc.

- 6.4.22 YShield GmbH & Co. KG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

電磁干擾屏蔽市場規模、佔有率、趨勢和預測:按材料、屏蔽方法、終端用戶產業和地區分類,2026-2034年

電磁干擾屏蔽市場規模、佔有率、趨勢和預測:按材料、屏蔽方法、終端用戶產業和地區分類,2026-2034年 全球電磁干擾屏蔽市場:依材料、方法、頻率和類型分類-預測(至2032年)

全球電磁干擾屏蔽市場:依材料、方法、頻率和類型分類-預測(至2032年) 電磁干擾屏蔽市場:依材料、屏蔽方法、屏蔽技術、應用及通路分類-2026-2032年全球市場預測EMI濾波器測試儀市場:按濾波器類型、測試參數、技術、額定功率、頻率範圍、最終用戶產業和通路分類,全球預測,2026-2032年

電磁干擾屏蔽市場:依材料、屏蔽方法、屏蔽技術、應用及通路分類-2026-2032年全球市場預測EMI濾波器測試儀市場:按濾波器類型、測試參數、技術、額定功率、頻率範圍、最終用戶產業和通路分類,全球預測,2026-2032年 5G電磁干擾(EMI)材料市場規模、佔有率和成長分析:按材料類型、應用領域、產業部門、最終用戶和地區分類-2026-2033年產業預測EMI基板級屏蔽市場(按安裝類型、材料類型、屏蔽配置、頻率範圍和最終用途行業分類)-全球預測,2026-2032年擠壓式電磁屏蔽墊片市場(依材料類型、最終用途產業、應用、安裝類型、導電等級和產品形式分類),全球預測,2026-2032年積體電路基板級屏蔽市場:依材料、厚度、最終用戶、應用和分銷管道分類,全球預測(2026-2032年)

5G電磁干擾(EMI)材料市場規模、佔有率和成長分析:按材料類型、應用領域、產業部門、最終用戶和地區分類-2026-2033年產業預測EMI基板級屏蔽市場(按安裝類型、材料類型、屏蔽配置、頻率範圍和最終用途行業分類)-全球預測,2026-2032年擠壓式電磁屏蔽墊片市場(依材料類型、最終用途產業、應用、安裝類型、導電等級和產品形式分類),全球預測,2026-2032年積體電路基板級屏蔽市場:依材料、厚度、最終用戶、應用和分銷管道分類,全球預測(2026-2032年) 防靜電紡織品市場分析及預測(至2035年):類型、產品、服務、技術、應用、材料類型、製程、最終用戶、功能、安裝類型電磁屏蔽市場分析及預測(至2035年):類型、產品、服務、技術、應用、材質類型、組件、最終用戶、安裝類型、設備

防靜電紡織品市場分析及預測(至2035年):類型、產品、服務、技術、應用、材料類型、製程、最終用戶、功能、安裝類型電磁屏蔽市場分析及預測(至2035年):類型、產品、服務、技術、應用、材質類型、組件、最終用戶、安裝類型、設備