|

市場調查報告書

商品編碼

2062067

再生橡膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Reclaimed Rubber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

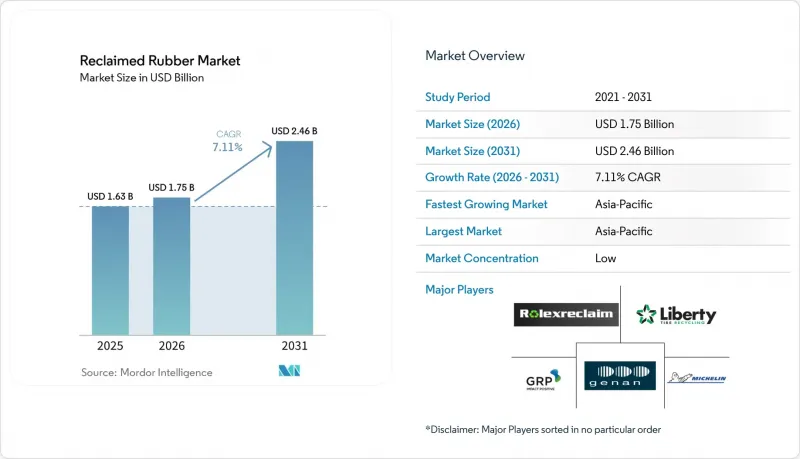

根據 Mordor Intelligence 預測,再生橡膠市場規模將從 2025 年的 16.3 億美元和 2026 年的 17.5 億美元成長到 2031 年的 24.6 億美元,2026 年至 2031 年的複合年成長率為 7.11%。

本報告按產品類型(整胎翻新(WTR)、丁基翻新等)、工藝(機械工藝和化學/硫化工序)、應用(汽車和飛機輪胎、橡膠墊和地板材料等)、最終用戶行業(汽車和運輸、建築等)和地區(亞太地區、北美、歐洲、南美等)進行分類。

全球再生橡膠市場趨勢及洞察

一種經濟高效且永續的天然橡膠替代品。

2024年至2025年間,再生橡膠展現出顯著的成本優勢,其價格比原生天然橡膠和合成彈性體低30%至50%。天然橡膠價格徘徊在每噸1800美元至2100美元之間,而整胎再生橡膠的價格則更為親民,僅每噸800美元至1200美元。這種結構性的價格差異源自於再生橡膠避免了農業風險溢價和石油化學原料價格波動的影響。汽車產業的二級供應商已開始在地墊、擋泥板和避震器等產品中加入20%至40%的再生橡膠,並嚴格遵守ISO 9001品質標準。值得一提的是,豐田合成株式會社於2025年12月為豐田RAV4推出了含有20%再生材料的密封條,彰顯了該材料的卓越性能。在建設產業,REGUPOL公司因每年處理價值1.15億英鎊的廢橡膠而備受關注。與使用全新EPDM橡膠相比,他們的努力使符合ASTM D5603衝擊標準的地板材料材料成本降低了40%。此外,隨著歐盟排放交易體系涵蓋廢棄物焚燒,再生材料在碳定價機制中變得越來越受歡迎。這主要是由於其環境效益;每減少一噸送往掩埋的輪胎,就能減少約2.5噸二氧化碳當量排放。

全球廢舊輪胎法規正加速推動回收利用義務。

2024年至2025年間,具有約束力的立法將企業的自願性努力轉變為強制性義務。廢棄物運輸條例》呼籲成員國將專注於材料回收而非能源回收。愛爾蘭的「生產者延伸責任制」(EPR)計畫於2025年1月生效,該計畫強制要求輪胎製造商承擔回收成本,並在2027年之前實現90%的回收目標。在中國,經認證的回收商可獲得70%的增值稅退稅,並被要求在非關鍵輪胎配方中使用再生材料。這些法規的推進促成了諸如宜昌橫大里年產10萬噸的工廠等設施的建立,該工廠於2024年12月投產。加州的SB 876法案規定,州政府資助的道路瀝青必須含有至少5%的蛤殼橡膠,這增加了對機械再生橡膠的需求。獲得 ISO 14001 和 ISCC PLUS 認證的加工商可以獲得優先供應商地位,而未達到標準的加工商可能會被排除在貿易之外。

原料品質的差異會影響化合物的均勻性。

廢舊輪胎由於聚合物配比、鋼絲帶束層以及道路污染物含量不一,抵達後需接受嚴格的檢驗。高達15%的進貨材料因金屬和化學殘留物過高而被降級或完全拒收。為了因應這種差異,下游複合材料生產商不得不依賴額外的穩定劑,這又使成本增加了5%至8%,從而削弱了回收的經濟效益。遵循福特FL™ BN 108-01標準的汽車原廠製造商(OEM)要求輪胎的抗張強度超過10兆帕,伸長率超過300%。該規定將再生材料的比例限制在30%或以下,除非製造商能夠確保高純度的原料。 2022年,中國的輪胎回收率僅52.73%,低於全球平均。這一差距凸顯了非正規回收網路帶來的挑戰,這些網路增加了品質風險。投資近紅外線分選技術有可能緩解這種不均勻性,但成本很高,每條生產線需要高達 50 萬美元的資本投資。

細分市場分析

2025年,整胎翻新件(WTR)佔再生橡膠市場的47.12%。預計到2031年,該市場將以7.69%的複合年成長率穩定成長。這一成長得益於機械破碎製程相對較低的資本投入,年處理能力達1萬噸,投資額僅200萬至500萬美元。整胎翻新件的多種聚合物混合物可用於避震器、擋泥板和地墊等應用。這些應用有助於二級供應商在滿足原始設備製造商(OEM)成本降低要求的同時,維持符合ISO 9001標準。

對再生丁基橡膠和三元乙丙橡膠(EPDM)的需求正在增加。這是由於碳排放要求的強制執行,導致屋頂板材和汽車密封條不再完全使用原生材料。再生EPDM的價格比再生水處理橡膠(WTR)高出15-20%,它採用硫化工序來滿足單層屋頂材料的臭氧老化要求。 High-Tech Reclaim和Swani Rubber等公司向工業混煉商供應這些特殊等級的再生EPDM。隨著微波和機械化學製程的不斷改進,再生EPDM與原生聚合物的性能差距正在縮小,從而擴大了其潛在的終端市場。

到2025年,機械研磨將佔據72.11%的市場佔有率,這主要得益於其混合材料加工能力以及0.8-1.2千瓦時/公斤的能耗。 2025年12月,作為其分階段成長策略的一部分,Liberty Tire投資140萬美元擴建其位於北卡羅來納州的工廠,使其年產能增加3.3千噸。

受高階輪胎製造商對高純度原料需求的推動,化學脫硫領域預計將以7.77%的複合年成長率成長。該領域微波脫硫設備的能耗為1.2-1.8千瓦時/公斤,同時可維持高達90%的拉伸強度。位於河南省相城三山的年產5萬噸工廠體現了中國致力於推動再生技術的決心。目前,該領域設備的投資回收期已縮短至三年以內,用於高階應用的再生橡膠比機械級橡膠的價格溢價10-15%。

區域分析

預計到2025年,亞太地區將佔全球銷售額的46.22%,並在2031年之前維持7.88%的複合年成長率。 2024年,中國翻新輪胎加工量達到900萬噸,年增20%,這得益於新推出的針對認證加工商的70%增值稅退稅政策。湖北和山東等省份在2024年至2025年間,每年新增加工量超過15萬噸。同時,印度的斯瓦尼橡膠公司和泰國的綠橡膠能源公司正在擴大其特殊產品和熱解線,以滿足汽車產業中心的需求。

北美地區仍佔有重要地位。聯邦政府已撥款12億美元基礎設施資金用於垃圾焚化發電項目,影響了原物料價格。同時,加州SB 876等州級法規也支撐著蛤殼橡膠瀝青市場。 2023年,美國3億條廢舊輪胎中,有2.4億條得到處理,其中7500萬條轉化為碎橡膠,9600萬條用於能源生產。作為美墨加協定(USMCA)汽車供應鏈的一部分,加拿大和墨西哥為該地區的需求貢獻了15%至18%。

歐洲的貢獻主要體現在強制性回收計畫和生產者延伸責任制(EPR)框架。 Genan公司年破碎量達40萬噸,業務遍及丹麥、葡萄牙和德國,致力於提升纖維組分的價值。米其林在瑞典的熱解舉措已成為歐洲輪胎製造廠整合閉合迴路再生炭黑供應的典範。歐盟政策的目標是到2030年將再生原料的平均含量提高到23%以上,這意味著高規格再生橡膠的需求將持續成長。

在南美洲,巴西正在強制製造商召回產品,而阿根廷於2025年10月推出了首個含有10%輪胎粉末的橡膠改質路面。中東和非洲也具有成長潛力。沙烏地阿拉伯和南非都在考慮實施掩埋禁令以及綠色政府採購法規。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 一種經濟高效且永續的天然橡膠替代品。

- 全球廢棄輪胎法規正在加速強制回收進程。

- 高階輪胎系列OEM再生材質含量目標(2026年及以後)

- 快速脫硫技術的規模化應用可顯著降低能耗。

- 可再生燃料的協同加工激增,帶動了對廢棄輪胎原料的需求。

- 市場限制因素

- 由於原料品質的變化,導致化合物一致性受到影響。

- 消費品中氣味和揮發性有機化合物的監管限值

- 在高性能應用領域與生物基彈性體競爭

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 整胎翻新(WTR)

- 回收丁基橡膠

- 回收的乙丙橡膠(EPDM)

- 其他產品類型(再生天然橡膠、再生乳膠等)

- 透過流程

- 機械過程

- 化學/硫化工序

- 透過使用

- 汽車和飛機輪胎

- 橡膠墊和地板材料

- 模製工業產品

- 橡膠化合物和母粒

- 其他用途(鞋類等)

- 按最終用戶行業分類

- 汽車和運輸業

- 建築/施工

- 消費品

- 工業製造

- 其他終端用戶產業(能源、公共產業等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Balaji Rubber Industries(P)Ltd.

- ELGI Rubber

- Entech Inc.

- GENAN HOLDING A/S

- Green Rubber Global Ltd

- GRP LTD.

- High Tech Reclaim Pvt. Ltd.

- HUXAR

- Michelin

- Mitsubishi Chemical Group Corporation

- Liberty Tire Recycling

- Pirelli & CSpA

- Rolex Reclaim Pvt. Ltd.

- Star Polymer Inc

- Sun Exims Pvt. Ltd.

- Swani Rubber Industry

第7章 市場機會與未來展望

According to Mordor Intelligence, the reclaimed rubber market size is projected to expand from USD 1.63 billion in 2025 and USD 1.75 billion in 2026 to USD 2.46 billion by 2031, registering a CAGR of 7.11% between 2026 to 2031.

This report is Segmented by Product Type (Whole Tyre Reclaim (WTR), Butyl Reclaim, and More), Process (Mechanical Process and Chemical/Devulcanization Process), Application (Automotive and Aircraft Tires, Rubber Mats and Flooring, and More), End-User Industry (Automotive and Transportation, Building and Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, and More).

Global Reclaimed Rubber Market Trends and Insights

Cost-Effective Sustainable Substitute for Virgin Rubber

In 2024-2025, reclaimed rubber showcased a significant cost advantage, being priced 30-50% lower than both virgin natural and synthetic elastomers. While natural rubber prices hovered between USD 1,800-2,100 per ton, whole tire reclaim was available at a more modest USD 800-1,200. This structural price gap arises because reclaimed rubber sidesteps both agricultural risk premiums and the volatility associated with petrochemical feedstocks. Tier-2 automotive suppliers have begun integrating 20-40% reclaimed content into products like floor mats, mud flaps, and dampers, all while adhering to ISO 9001 quality standards. In a notable move, Toyoda Gosei introduced weather-stripping featuring 20% recycled content for the Toyota RAV4 in December 2025, underscoring the material's validated performance. Over in the construction sector, REGUPOL is making waves by processing 115 million pounds of scrap rubber each year. Their efforts have led to a 40% reduction in material costs for flooring that meets ASTM D5603 impact standards, compared to using virgin EPDM. Additionally, with the EU Emissions Trading System expanding to cover waste incineration, carbon-pricing schemes are increasingly favoring reclaimed materials. This is largely due to the environmental benefit: diverting just 1 ton of tires from landfills can prevent the release of approximately 2.5 tons of CO2-equivalent emissions.

Global Waste-Tire Regulations Accelerating Recycling Mandates

In 2024-2025, binding legislation converted voluntary corporate initiatives into enforceable mandates. The EU Waste Shipment Regulation 2024/1157 requires member states to focus on material recycling instead of energy recovery. Ireland's Extended Producer Responsibility (EPR) program, implemented in January 2025, obligates tire producers to fund collections and achieve a 90% recovery target by 2027. In China, certified recyclers receive a 70% VAT rebate and must use recycled content in non-critical tire compounds. This regulatory push has driven the establishment of facilities such as Yichang Hengdali's 100 kiloton per annum plant, which began operations in December 2024. California's SB 876 law requires a 5% crumb-rubber minimum in state-funded road asphalt, increasing demand for mechanical reclaim. Processors with ISO 14001 and ISCC PLUS certifications gain preferred-supplier status, while non-compliant operators face potential exclusion.

Variability in Feedstock Quality Disrupting Compound Consistency

End-of-life tires, laden with mixed polymer ratios, steel belts, and road contaminants, face scrutiny upon arrival. Up to 15% of this incoming material gets downgraded or outright rejected due to excessive metal or chemical residues. To counteract this variability, downstream compounders resort to extra stabilizers, which inflate costs by an additional 5-8% and erode the economic advantage of reclamation. Automotive OEMs, adhering to Ford's FLTM BN 108-01 standard, mandate a tensile strength exceeding 10 MPa and an elongation surpassing 300%. This stipulation restricts reclaim loadings to below 30% unless manufacturers can guarantee high-purity streams. In 2022, China's tire-recovery rate stood at 52.73%, lagging behind the global average. This shortfall underscores the challenges posed by informal collection networks, which amplify quality risks. While investments in near-infrared sorting promise to mitigate this heterogeneity, they come at a steep price, demanding up to USD 0.5 million in capital per line.

Other drivers and restraints analyzed in the detailed report include:

- OEM Recycled-Content Targets for Premium Tire Lines

- Rapid Devulcanization Technology Scale-Up Slashing Energy Use

- Odor and VOC Compliance Limits for Consumer-Facing Goods

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Whole Tire Reclaim (WTR) accounted for 47.12% of the reclaimed rubber market. Projections indicate steady growth, with an expected CAGR of 7.69% through 2031. This growth is supported by the mechanical grinding process, which requires a relatively low capital investment of USD 2-5 million for a capacity of 10 kilotons per year. WTR's diverse polymer blend is utilized in vibration dampers, mud flaps, and floor mats. These applications help Tier-2 suppliers achieve cost reductions required by OEMs while maintaining compliance with ISO 9001 standards.

The demand for butyl and EPDM reclaims is increasing, driven by their use in roofing membranes and automotive weather-seals, which are shifting away from virgin-only material specifications due to carbon-reduction mandates. EPDM reclaim, priced 15-20% higher than WTR, uses devulcanization processes to meet the ozone-aging requirements necessary for single-ply roofing. High-Tech Reclaim and Swani Rubber supply these specialty grades to industrial compounders. As microwave and mechanochemical methods continue to improve, they are narrowing the performance gap with virgin polymers, which is expanding the range of potential end markets.

In 2025, mechanical grinding accounted for 72.11% of the market share due to its capability to process mixed feedstock and its energy requirement of 0.8-1.2 kWh/kg. In December 2025, Liberty Tire expanded its North Carolina facility with a USD 1.4 million investment, increasing capacity by 3.3 kilotons per year as part of its incremental growth strategy.

The chemical devulcanization segment is projected to grow at a CAGR of 7.77%, supported by the demand from OEMs for higher-purity feedstock used in premium tires. Microwave units in this segment consume 1.2-1.8 kWh/kg of energy while retaining up to 90% of tensile strength. Xiangcheng Sanshan's 50 kilotons per year plant in Henan reflects China's focus on advancing reclaim technology. Equipment in this segment now offers payback periods of less than three years, and reclaimed rubber used in premium applications achieves a 10-15% price premium compared to mechanical grades.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 46.22% of global revenue, projections indicate a growth rate of 7.88% CAGR extending to 2031. In 2024, China's recycled-tire volume reached 9 million tons, marking a 20% year-on-year increase, supported by a newly introduced 70% VAT rebate for certified processors. Provinces such as Hubei and Shandong expanded their capacities by over 150 kilotons annually during 2024-2025. Meanwhile, India's Swani Rubber and Thailand's Green Rubber Energy are increasing specialty and pyrolysis lines to address demand in automotive corridors.

North America maintains a significant position. Federal infrastructure funding of USD 1.2 billion is allocated to waste-to-energy projects, influencing feedstock pricing. At the same time, state regulations, such as California's SB 876, support the market for crumb-rubber asphalt. In 2023, the U.S. processed 240 million out of 300 million scrap tires, converting 75 million to ground rubber and utilizing 96 million for energy. Canada and Mexico, both part of the USMCA automotive chain, contribute an additional 15-18% to the regional demand.

Europe's contributions are shaped by mandatory take-back and Extended Producer Responsibility (EPR) frameworks. Genan, with a grinding capacity of 400 kilotons per year, operates across Denmark, Portugal, and Germany, and is advancing textile-fraction valorization. Michelin's pyrolysis initiative in Sweden serves as a model for a closed-loop recovered carbon black supply, integrated into European tire manufacturing plants. EU policies aim to increase the average recycled raw material content beyond 23% by 2030, indicating a rise in demand for high-spec reclaim.

In South America, Brazil enforces manufacturer take-back, while Argentina introduced its first rubber-modified highway section, incorporating 10% tire powder, in October 2025. The Middle East and Africa, present potential for growth. Both Saudi Arabia and South Africa are considering the implementation of landfill bans and green public procurement regulations.

- Balaji Rubber Industries (P) Ltd.

- ELGI Rubber

- Entech Inc.

- GENAN HOLDING A/S

- Green Rubber Global Ltd

- GRP LTD.

- High Tech Reclaim Pvt. Ltd.

- HUXAR

- Michelin

- Mitsubishi Chemical Group Corporation

- Liberty Tire Recycling

- Pirelli & CSpA

- Rolex Reclaim Pvt. Ltd.

- Star Polymer Inc

- Sun Exims Pvt. Ltd.

- Swani Rubber Industry

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost-effective sustainable substitute for virgin rubber

- 4.2.2 Global waste-tire regulations accelerating recycling mandates

- 4.2.3 OEM recycled-content targets for premium tire lines (post-2026)

- 4.2.4 Rapid devulcanization technology scale-up slashing energy use

- 4.2.5 Surge in Renewable-Fuel Co-Processing Driving End-of-Life Tyre Feedstock Demand

- 4.3 Market Restraints

- 4.3.1 Variability in feedstock quality disrupting compound consistency

- 4.3.2 Odour and VOC compliance limits for consumer-facing goods

- 4.3.3 Competition from bio-based elastomers in high-performance uses

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Whole Tire Reclaim (WTR)

- 5.1.2 Butyl Reclaim

- 5.1.3 Ethylene Propylene Diene Monomer (EPDM) Reclaim

- 5.1.4 Other Product Types (Natural Rubber Reclaim, Latex Reclaim, etc.)

- 5.2 By Process

- 5.2.1 Mechanical Process

- 5.2.2 Chemical/Devulcanisation Process

- 5.3 By Application

- 5.3.1 Automotive and Aircraft Tires

- 5.3.2 Rubber Mats and Flooring

- 5.3.3 Molded Industrial Goods

- 5.3.4 Rubber Compounds and Masterbatch

- 5.3.5 Other Applications (Footwear, etc.)

- 5.4 By End-user Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Building and Construction

- 5.4.3 Consumer Goods

- 5.4.4 Industrial Manufacturing

- 5.4.5 Other End-user Industries (Energy and Utilities, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Balaji Rubber Industries (P) Ltd.

- 6.4.2 ELGI Rubber

- 6.4.3 Entech Inc.

- 6.4.4 GENAN HOLDING A/S

- 6.4.5 Green Rubber Global Ltd

- 6.4.6 GRP LTD.

- 6.4.7 High Tech Reclaim Pvt. Ltd.

- 6.4.8 HUXAR

- 6.4.9 Michelin

- 6.4.10 Mitsubishi Chemical Group Corporation

- 6.4.11 Liberty Tire Recycling

- 6.4.12 Pirelli & CSpA

- 6.4.13 Rolex Reclaim Pvt. Ltd.

- 6.4.14 Star Polymer Inc

- 6.4.15 Sun Exims Pvt. Ltd.

- 6.4.16 Swani Rubber Industry

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

再生橡膠市場:依原料、類型、製造流程、形態、應用和最終用途產業分類-2026-2032年全球預測

再生橡膠市場:依原料、類型、製造流程、形態、應用和最終用途產業分類-2026-2032年全球預測 全球再生橡膠市場規模、佔有率、趨勢和成長分析報告(2026-2034)再生乳膠橡膠市場按產品類型、原料、製造技術、應用和銷售管道分類-2026-2032年全球預測

全球再生橡膠市場規模、佔有率、趨勢和成長分析報告(2026-2034)再生乳膠橡膠市場按產品類型、原料、製造技術、應用和銷售管道分類-2026-2032年全球預測 再生橡膠市場規模、佔有率及成長分析(按產品、應用及地區分類)-2026-2033年產業預測

再生橡膠市場規模、佔有率及成長分析(按產品、應用及地區分類)-2026-2033年產業預測 再生橡膠市場規模、佔有率、趨勢分析報告:按產品、最終用途、地區、細分市場預測,2025-2030 年

再生橡膠市場規模、佔有率、趨勢分析報告:按產品、最終用途、地區、細分市場預測,2025-2030 年 全球天然再生橡膠市場規模研究,按產品(全輪胎再生橡膠、丁基再生橡膠、三元乙丙再生橡膠等)、最終用途和區域預測 2022-2032

全球天然再生橡膠市場規模研究,按產品(全輪胎再生橡膠、丁基再生橡膠、三元乙丙再生橡膠等)、最終用途和區域預測 2022-2032 再生橡膠市場、規模、佔有率、趨勢、行業分析報告(按產品、應用、最終用戶和地區)- 市場預測,2025-2034 年硫化再生橡膠市場、規模、佔有率、趨勢、行業分析報告(按類型、形式、應用和地區)- 市場預測,2025-2034 年

再生橡膠市場、規模、佔有率、趨勢、行業分析報告(按產品、應用、最終用戶和地區)- 市場預測,2025-2034 年硫化再生橡膠市場、規模、佔有率、趨勢、行業分析報告(按類型、形式、應用和地區)- 市場預測,2025-2034 年 全球再生橡膠市場,2024-2028

全球再生橡膠市場,2024-2028