|

市場調查報告書

商品編碼

2062062

引擎驅動焊接機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Engine Driven Welders - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

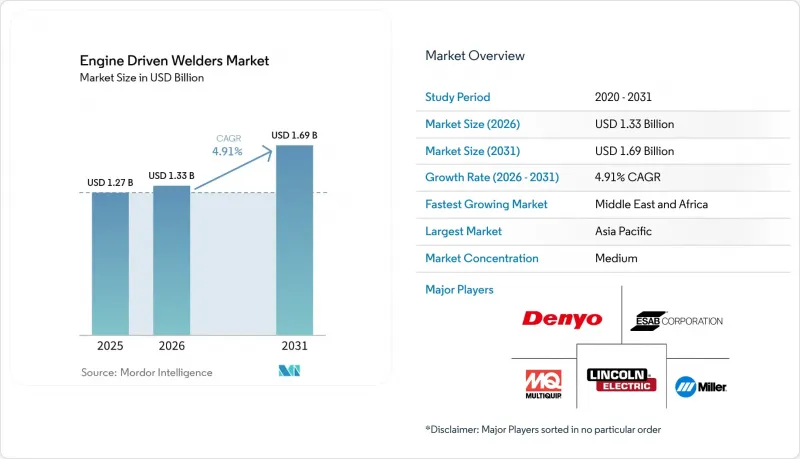

根據 Mordor Intelligence 預測,引擎驅動焊接機的市場規模預計將在 2025 年達到 12.7 億美元,2026 年達到 13.3 億美元,到 2031 年達到 16.9 億美元,2026 年至 2031 年的複合年成長率為 4.91%。

本報告按輸出功率(0-100A、101-300A、其他)、燃料類型(汽油、柴油、其他)、焊接工藝(電弧焊接(SMAW)、MIG焊接(GMAW)、其他)、終端用戶產業(建築基礎設施、其他)以及地區(北美、南美、歐洲、亞太、中東和非洲)進行細分。市場預測以美元(USD)計價。

全球引擎驅動焊接機市場趨勢及洞察

石油和天然氣管道基礎設施擴建

管道建造週期持續推動著對高電流、恆壓引擎驅動平台的持續需求,這些平台能夠在長達數年的專案週期內為自動化環焊提供可重複的電弧穩定性。 INGAA基金會針對北美地區的長期展望指出,到2052年,將新增約14萬英里的天然氣運輸和整合能力,從而為依賴移動式焊接電源的現場作業奠定基準。近期活動報告顯示,正在進行和計劃中的項目總價值達數百億美元,其中包括將二疊紀盆地天然氣輸送至墨西哥灣沿岸的新路線,以及為支持區域需求中心而擴建加拿大運輸能力。如此快速的建造使得對能夠在不斷變化的環境條件下處理預熱、倒角公差和嚴格製程控制的焊接系統的需求持續存在。儘管工程進度易受中游經濟狀況和下游提貨情況的影響,可能導致開工日期變更,但在施工階段對現場焊接電源的結構性需求卻始終存在。透過標準化堅固耐用、高功率、具備自動化就緒工作循環和充足備用電源的型號,設備負責人即使在管道訂單累積訂單的情況下,也能確保運轉率,包括厚壁接頭和長時間焊接作業。

擴大偏遠和農村地區的建設活動

與資料中心園區、可再生能源發電和走廊基礎設施相關的工作持續擴張,越來越多的活動轉移到電網脆弱或早期階段無法覆蓋的地區。在美國,一份2026年的規劃文件顯示,整體開工量將溫和成長,其中私人辦公大樓建設主要由需要高電力容量和漫長施工週期的超大規模資料中心所構成。這使得焊工忙於安裝鋼骨框架、機架和輔助結構。引擎驅動的焊接機為這一趨勢提供了支持,它們為工具、空氣壓縮機和照明設備供電,即使遠離主電源也能保持穩定的電弧。承包商正在透過強調針對服務卡車負載容量最佳化的整合系統來平衡部署,從而減少運輸次數並縮短安裝時間。這在大型分散式站點尤其重要。雖然材料成本、關稅和授權程序有時會延長工期,但由於需要在分散地點建造電力消耗量設施,移動平台在結構焊接和MRO(維護、維修和大修)焊接領域都更受歡迎。將引擎驅動焊接機的性能數據與調度和人員配備聯繫起來的承包商可以深入了解運轉率,並降低遠端工作的燃料成本。

限制在封閉空間內使用的排放氣體法規

某些與焊接相關的金屬被認定為有毒空氣污染物,這限制了在封閉空間內進行無通風引擎運行,從而限制了柴油引擎在密閉室內環境中的使用。在受監管的地區,排放氣體標準強制要求柴油引擎安裝後後處理系統並定期進行再生循環,這增加了維護程序並影響了長時間輪班。為了應對這些限制,業主們正在根據具體情況採用液化石油氣/壓縮天然氣等替代燃料,或實施電池混合動力系統,該系統可在不產生引擎廢氣的情況下提供電弧動力。地下作業和密閉空間的相關法規也促使人們更加關注低排放、小面積的設備。那些制定安全通風和煙塵抽排標準並使設備符合空氣品質要求的企業,在保持合規性的同時,也維持了生產效率。這一趨勢正在增強引擎驅動焊接機市場中複合材料技術的實力。

細分市場分析

到2025年,101-300安培功率範圍的焊接機將佔總銷售量的44.67%,繼續成為分散作業現場管線工人和中小型結構製造的重要工具。這類焊接機兼具便攜性和充足的功率儲備,可透過內建發電機使用通用焊條為輔助工具供電,從而維持現場小規模團隊的生產效率。買家會選擇電弧特性穩定、負載持續率高、電纜管理便捷的型號,以應對在各種表面狀況的鋼材上進行各種不便的焊接作業。大規模部署此類焊機的公司通常會進行AWS結構和管道標準的培訓,以確保設備性能能夠轉化為符合標準的穩定焊接。此輸出範圍的優點在於其柔軟性。在引擎驅動焊接機市場中,它的特點是能夠適應各種應用場景,同時保持適當的車輛負載能力。

預計到2031年,500安培及以上功率的焊接機市場將以每年5.21%的速度成長,這主要得益於重工業和造船廠厚板焊接自動化程度的提高,以及涉及混凝土和鋼材的大型企劃對更高焊接面積的需求。高階焊接機的提案在於其緊湊的佔地面積,使其能夠安裝在卡車和滑橇上,即使在高負荷運轉下也能保持持續輸出,從而使施工團隊能夠將工業級能力應用於大規模現場組裝工作。使用者也十分欣賞其氣動電弧刨削功能以及使用更粗焊絲並實現穩定噴射傳輸的能力,這減少了焊接道次。多種整合焊接、壓縮空氣和輔助電源的型號反映了市場向單底盤解決方案的轉變,這種解決方案簡化了改造,並節省了負載負載容量和卡車貨箱空間。這種平台整合減少了設備雜亂,並加快了引擎驅動焊接機市場中從事各種鋼骨建設專案的施工團隊的部署速度。

預計到2025年,柴油動力系統將佔據全球67.81%的市場佔有率,這主要得益於其耐用性、高負載下的燃油效率以及在偏遠地區(無電網支援)的長期運作能力。管道和重型建築承包商更青睞柴油動力系統,因為其在低轉速下即可輸出強勁扭矩,並且在Tier 1場地具有安全可靠的運行特性,從而降低了加油風險。可維護性也是柴油動力系統的一大優勢,定期維護並符合運作週期要求,能夠確保成熟的零件網路和較長的引擎壽命。在日益嚴格的ESG政策和區域排放法規的背景下,車隊所有者擴大採用雙燃料套件,以便在適當的運行條件下混合液化石油氣(LPG),從而在不影響連續運作能力的前提下實現更清潔的運行。這種混合動力方案,結合怠速管理和基於遠端資訊處理的維護技術,使引擎驅動焊接機市場的所有者能夠在滿足現場法規要求的同時有效控制成本。

液化石油氣/壓縮天然氣替代燃料預計將以每年5.78%的速度成長,在空氣品質法規日益嚴格的室內和都市區應用中發揮越來越重要的作用。使用者採用這些解決方案是為了減少氮氧化物和顆粒物排放,並確保能夠在封閉空間內限制使用柴油引擎的場所使用。汽油仍然用於入門級和輕型應用,在這些應用中,購買價格和輕便性比長期運作的效率更為重要,尤其是在間歇性維修和農業應用中。結合引擎和電池的混合動力配置正在興起,以彌合清潔運作和長期工作之間的差距,而緊湊型電池優先車型已在某些封閉空間和電力受限的環境中得到應用。隨著加氣網路和充電基礎設施的成熟,只要法規和運作週期允許,混合動力和替代系統預計將繼續在引擎驅動的焊接機市場中與柴油機形成互補。

區域分析

預計到2025年,亞太地區將佔全球銷售額的48.21%,這得益於其強大的製造業基礎和大規模的公共工程項目,這些項目不斷擴展走廊、能源資產和工業設施,涵蓋各種氣候和地形。造船、汽車、能源和大型基礎設施等相關製造業支撐著移動式焊接設備在建築和MRO(維護、修理和大修)作業中的常規使用,尤其是在需要臨時供電的地區。該地區的專案配置往往傾向於選擇電弧穩定、輔助電源可靠的設備,即使在高濕度、高溫或高海拔等環境下也能正常運作。隨著用戶擴大採用數位監控和遠端參數控制,具備遠端資訊處理功能的多進程平台在服務車隊中越來越受到關注。雖然由於不同城市和國家的排放法規各不相同,液化石油氣(LPG)和混合動力焊接設備僅在室內和監管嚴格的場所有選擇地部署,但在引擎驅動的焊接設備市場中,柴油焊接設備仍然在戶外項目中佔據主導地位。

在北美,由於結構鋼、能源基礎設施和資料中心營運的擴張,以及待開發區工地對行動電源的需求,市場需求保持穩定。建築公司正在投資整合式焊接設備,以縮短設定時間,並利用較小的工作團隊來提高每個班級的工作量,從而應對人手不足。隨著Tier 4 Final排放標準和區域性有害空氣污染物分類限制了柴油在封閉空間的使用,人們對液化石油氣(LPG)和混合動力設備的興趣日益濃厚,尤其是在住宅附近的室內作業和夜班工作中。對於現場維修和公共產業,在偏遠和對天氣敏感的環境中長時間使用,堅固耐用的柴油設備仍然是首選。隨著租賃公司和車隊營運商擴大採用遠端資訊處理技術,運轉率追蹤正在影響引擎驅動焊接設備市場的車隊更換選擇。

預計中東和非洲地區的成長率將達到7.21%,成為成長最快的地區,這主要得益於各國積極推進大型企劃、擴大能源和石化產能以及推進公共產業網路現代化。惡劣的環境條件和工地間的長途運輸進一步凸顯了設備的耐用性、易於維護性和可靠的本地零件供應網路的重要性。為了降低停機風險,業主通常會選擇擁有完善分銷網路、提供保固和耗材供應的全球品牌。大規模製造工廠和現場團隊受益於高功率多進程焊接機,這些焊接機能夠簡化庫存管理和培訓流程,實現零件的通用化。基礎設施和能源投資的長期性和高資本投入,持續推動引擎驅動焊接機市場對大型作業車輛和維修車輛應用設備的需求。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 石油和天然氣管道基礎設施擴建

- 擴大偏遠和農村地區的建設活動

- 農業機械製造和維修領域的需求增加

- 軍事和國防領域的作戰需求不斷成長。

- 移動焊接和維護服務的成長

- 自然災害後的復原和緊急基礎設施的修復。

- 市場限制因素

- 高油耗和營運成本

- 噪音污染和對企業的干擾

- 頻繁維護和停機的必要性

- 限制在封閉空間內使用的排放法規

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 產業吸引力—五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 產業內部的競爭

- 依使用情況對輸出進行分類

- 具有雙重價值提案,可推動高階市場發展。

第5章 市場規模與成長預測

- 依輸出類型

- 0~100A

- 101~300A

- 301~500A

- 超過500安培

- 按燃料類型

- 汽油

- 柴油引擎

- LPG/CNG

- 替代混合動力系統

- 透過焊接工藝

- 電弧焊接(SMAW)

- MIG焊接(GMAW)

- 氬弧焊(GTAW)

- 高級多進程(脈衝MIG焊接、刨削)

- 按最終用戶行業分類

- 建設基礎設施

- 石油和天然氣管道

- 採礦和採石

- 造船/造船

- 發電和公用事業

- 汽車和一般製造業

- 一般維修/維修

- 其他(農業/農場、租賃公司等)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 秘魯

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東協(印尼、泰國、菲律賓、馬來西亞、越南)

- 其他亞太國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 科威特

- 土耳其

- 埃及

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Lincoln Electric Holdings Inc.

- Miller Electric Mfg LLC(ITW)

- ESAB Corp.

- Denyo Co., Ltd.

- Multiquip Inc.

- Vanair Manufacturing

- Hobart Brothers LLC

- MOSA SpA

- Shindaiwa Ltd.

- Atlas Copco AB

- Doosan Portable Power

- Generac Power Systems

- Kohler Co.(Engines)

- Cummins Inc.(Onan Division)

- Briggs & Stratton(Vanguard)

- Harbor Freight(VULCAN Brand)

- AGG Power Solutions

- Yamaha Motor Co.(Industrial Engines)

- Oerlikon Welding(Air Liquide)

- Westinghouse Outdoor Power

- Kipor Power

- Daihen Corp.

- Riland Industrial Co.

- Rental Fleet Leaders(United Rentals, Sunbelt)

第7章 市場機會與未來展望

According to Mordor Intelligence, the engine driven welders market size is projected to be USD 1.27 billion in 2025, USD 1.33 billion in 2026, and reach USD 1.69 billion by 2031, growing at a CAGR of 4.91% from 2026 to 2031.

This report is Segmented by Power Output (0-100 A, 101 - 300 A, and More), by Fuel Type (Gasoline, Diesel, and More), by Welding Process (Stick Welding (SMAW), MIG Welding (GMAW) and More), by End-User Industry (Construction & Infrastructure, and More), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Engine Driven Welders Market Trends and Insights

Expansion of Oil and Gas Pipeline Infrastructure

The pipeline buildout cycle remains a durable demand engine for high-amperage, constant-voltage engine-driven platforms that can deliver repeatable arc stability for automated girth welding over multi-year project timelines. The INGAA Foundation's long-range outlook for North America highlights around 140,000 miles of new gas transmission and gathering capacity additions through 2052, which sustains a baseline of right-of-way work that depends on mobile welding power at every spread. Recent activity tallies track tens of billions of dollars in active and proposed projects, with examples that include greenfield routes designed to move Permian volumes to Gulf Coast egress and Canadian capacity expansions to support regional demand centers. The construction cadence brings recurring needs for welding systems that handle preheats, bevel tolerances, and strict procedure control in variable environmental conditions. Project timing remains sensitive to midstream economics and downstream offtake conditions, which can shift start dates but rarely eliminate the structural need for on-site welding power in the build phase. Equipment planners who standardize on rugged high-output models with automation-ready duty cycles and auxiliary power headroom protect utilization across thick-wall and long-duration joints in this pipeline backlog context.

Growing Construction Activity in Remote and Rural Areas

Workloads tied to data centre campuses, renewable generation, and corridor infrastructure continue to expand and are shifting more activity into locations where the grid is weak or unavailable during early phases. In the United States, 2026 planning documents point to modest overall start growth, with private office construction dominated by hyperscale data centers that demand high electrical capacity and long construction sequences, which keep welding crews busy across steel frames, racks, and auxiliary structures. Engine-driven welders support this motion because they can power tools, air compressors, and lighting while maintaining stable arcs away from mains power. Contractors balance deployment by emphasizing payload-optimized all-in-one systems on service trucks to cut trips and reduce setup time, which becomes more valuable on large, dispersed sites. Input costs, tariffs, and permitting have extended some timelines, yet the requirement to build out power-hungry facilities in dispersed locations favors mobile platforms for both structural and MRO welding scopes. Contractors that link engine-driven welder performance data to scheduling and labor allocation gain utilization insight and contain fuel overhead on remote work packages.

Emission Regulations Restricting Usage in Enclosed Spaces

Toxic air contaminant designations for several welding-related metals limit unvented engine operation in enclosed spaces, which has narrowed diesel use in tight indoor environments. In regulated jurisdictions, emission standards drive the adoption of aftertreatment and periodic regeneration cycles on diesel engines, adding maintenance steps and affecting scheduling on long shifts. Owners address these constraints with LPG/CNG alternatives in some settings and with battery-hybrid systems that supply arc power without continuous engine exhaust. Site rules in underground work and confined spaces have also accelerated interest in equipment with lower tailpipe emissions and smaller footprints. Organizations that standardize safe ventilation and fume extraction and match equipment to air-quality requirements maintain compliance while preserving productivity. This pattern is reinforcing a mixed-technology toolbox within the engine-driven welders market.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Mobile Welding and Maintenance Services

- Increasing Military and Defense Field Operations Requirements

- High Fuel Consumption and Operational Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 101-300 ampere class captured 44.67% of 2025 revenue and remains the workhorse for pipeline crews and light-to-medium structural fabrication across dispersed job sites. These units balance portability with enough output headroom to run common electrodes and to power auxiliary tools through onboard generators, which keeps small teams productive in the field. Buyers select models with stable arc characteristics, strong duty cycles, and easy cable management to handle out-of-position work on steels with variable surface conditions. Companies that deploy these machines at scale often train on AWS structural and pipeline codes so that equipment capability translates into consistent, code-compliant welds. The appeal of this band is its flexibility, which covers a wide swath of use cases while keeping total truck payload in check for service vehicles in the engine-driven welders market.

Above 500 amperes, units are projected to grow at 5.21% through 2031 as heavy fabrication and shipyards automate thick-plate welding and as megaprojects in concrete and steel require higher deposition rates. The value proposition at the high end is sustained output under demanding duty cycles with a footprint that still allows truck or skid mounting, so teams can bring industrial-grade capability to large field assemblies. Users also value the ability to power air-arc gouging and to run larger wire diameters with stable spray transfer, which reduces pass counts. Several integrated models combine welding, compressed air, and auxiliary power to simplify upfits, reflecting the shift to single-chassis solutions that save payload and bed space. That platform consolidation reduces equipment sprawl and speeds setup for crews tasked with diverse steelwork on a given day in the engine-driven welders market.

Diesel powertrains held 67.81% of global sales in 2025 on the strength of durability, fuel efficiency under load, and the ability to run long hours on remote sites without grid support. Pipeline and heavy construction contractors prefer diesel because of robust torque at low RPM and safe handling characteristics on Tier 1 sites, which lowers hazards during refueling. Serviceability is also a differentiator, with mature parts networks and long engine lifecycles when maintenance is consistent and aligned to duty cycles. As ESG policies and local emission constraints tighten, fleet owners are piloting dual-fuel kits that allow LPG blending on appropriate jobs to achieve cleaner operation without losing continuous-duty power. That hybridized approach, paired with idle management and telematics-driven maintenance, allows owners to control costs while meeting site rules in the engine-driven welders market.

LPG/CNG alternatives are projected to expand at 5.78% per year, lifting their role in regulated indoor and urban applications where air-quality limits are tight. Owners adopt these solutions to reduce nitrogen oxide and particulate output and to gain access to sites that restrict diesel engines in enclosed areas. Gasoline continues to serve entry-level and light-duty use where purchase price and low weight matter more than long-hour efficiency, especially for intermittent repair and farm applications. Hybrid configurations that pair engines with batteries are emerging to bridge the gap between clean operation and long shifts, with compact battery-first models already serving certain confined or power-limited environments. As refueling networks and charging infrastructure mature, hybrid and alternative systems will continue to supplement diesel where rules and duty cycles permit in the engine-driven welders market.

Geography Analysis

Asia-Pacific held 48.21% of 2025 revenue on the back of strong manufacturing bases and large public works programs that continue to expand corridors, energy assets, and industrial facilities across diverse climates and terrains. Fabrication tied to shipbuilding, automotive, energy, and large-scale infrastructure sustains regular use of mobile welders for both construction and MRO tasks in areas where temporary power is necessary. The region's project mix favors equipment that can operate in humid, hot, or high-altitude conditions with stable arcs and reliable auxiliary power. As more owners layer in digital monitoring and remote parameter control, multiprocess platforms with telematics are gaining attention across service fleets. Emission constraints vary by city and country, which is prompting selective uptake of LPG and hybrid units for indoor or restricted sites, while diesel remains dominant on open-air projects in the engine-driven welders market.

North America shows stable demand patterns supported by structural steel, energy infrastructure, and expanding data center activity that relies on mobile power at greenfield sites. Contractors respond to labor shortages by investing in integrated welders that compress setup time and allow smaller crews to cover more tasks per shift. Tier 4 Final rules and local toxic air contaminant classifications limit diesel use in enclosed spaces, which lifts interest in LPG and hybrid options for indoor work or night shifts near residences. Field repair and utility work continue to favor robust diesel units for long-hour use in remote or weather-exposed settings. As telematics gain traction across rental and fleet operators, utilization tracking is influencing fleet renewal choices in the engine-driven welders market.

The Middle East and Africa region is projected to grow fastest at 7.21% as countries advance megaprojects, expand energy and petrochemical capacity, and modernize utility networks. Harsh environmental conditions and long distances between depots raise the value of ruggedness, simple maintenance access, and reliable local parts channels. Owners often standardize on global brands that maintain distributor networks with warranty coverage and consumable pipelines to reduce downtime risk. Large fabrication yards and field teams benefit from high-output multiprocess units that share components across fleets, which simplifies stocking and training. The long project horizons and capital intensity of infrastructure and energy investments continue to underpin equipment needs across heavy-duty and service-truck applications in the engine-driven welders market.

- Lincoln Electric Holdings Inc.

- Miller Electric Mfg LLC (ITW)

- ESAB Corp.

- Denyo Co., Ltd.

- Multiquip Inc.

- Vanair Manufacturing

- Hobart Brothers LLC

- MOSA S.p.A.

- Shindaiwa Ltd.

- Atlas Copco AB

- Doosan Portable Power

- Generac Power Systems

- Kohler Co. (Engines)

- Cummins Inc. (Onan Division)

- Briggs & Stratton (Vanguard)

- Harbor Freight (VULCAN Brand)

- AGG Power Solutions

- Yamaha Motor Co. (Industrial Engines)

- Oerlikon Welding (Air Liquide)

- Westinghouse Outdoor Power

- Kipor Power

- Daihen Corp.

- Riland Industrial Co.

- Rental Fleet Leaders (United Rentals, Sunbelt)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Oil and Gas Pipeline Infrastructure

- 4.2.2 Growing Construction Activity in Remote and Rural Areas

- 4.2.3 Rising Demand from Agricultural Equipment Manufacturing and Repair

- 4.2.4 Increasing Military and Defense Field Operations Requirements

- 4.2.5 Growth in Mobile Welding and Maintenance Services

- 4.2.6 Natural Disaster Recovery and Emergency Infrastructure Repair

- 4.3 Market Restraints

- 4.3.1 High Fuel Consumption and Operational Cost

- 4.3.2 Noise Pollution and Operator Discomfort

- 4.3.3 Frequent Maintenance Requirements and Downtime

- 4.3.4 Emission Regulations Restricting Usage in Enclosed Spaces

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Application-Driven Power Output Segmentation

- 4.9 Dual-Purpose Value Proposition Driving Premium Segment

5 Market Size & Growth Forecasts(Value, In USD)

- 5.1 By Power Output

- 5.1.1 0 - 100 A

- 5.1.2 101 - 300 A

- 5.1.3 301 - 500 A

- 5.1.4 Above 500 A

- 5.2 By Fuel Type

- 5.2.1 Gasoline

- 5.2.2 Diesel

- 5.2.3 LPG / CNG

- 5.2.4 Alternative & Hybrid Systems

- 5.3 By Welding Process

- 5.3.1 Stick Welding (SMAW)

- 5.3.2 MIG Welding (GMAW)

- 5.3.3 TIG Welding (GTAW)

- 5.3.4 Advanced Multi-Process (Pulse-MIG, Gouging)

- 5.4 By End-User Industry

- 5.4.1 Construction & Infrastructure

- 5.4.2 Oil & Gas / Pipeline

- 5.4.3 Mining & Quarrying

- 5.4.4 Shipbuilding & Marine

- 5.4.5 Power Generation & Utilities

- 5.4.6 Automotive and General Manufacturing

- 5.4.7 General Maintenance & Repair

- 5.4.8 Others (Agriculture & Farming, Rental & Leasing Companies, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Peru

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Kuwait

- 5.5.5.5 Turkey

- 5.5.5.6 Egypt

- 5.5.5.7 South Africa

- 5.5.5.8 Nigeria

- 5.5.5.9 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Lincoln Electric Holdings Inc.

- 6.4.2 Miller Electric Mfg LLC (ITW)

- 6.4.3 ESAB Corp.

- 6.4.4 Denyo Co., Ltd.

- 6.4.5 Multiquip Inc.

- 6.4.6 Vanair Manufacturing

- 6.4.7 Hobart Brothers LLC

- 6.4.8 MOSA S.p.A.

- 6.4.9 Shindaiwa Ltd.

- 6.4.10 Atlas Copco AB

- 6.4.11 Doosan Portable Power

- 6.4.12 Generac Power Systems

- 6.4.13 Kohler Co. (Engines)

- 6.4.14 Cummins Inc. (Onan Division)

- 6.4.15 Briggs & Stratton (Vanguard)

- 6.4.16 Harbor Freight (VULCAN Brand)

- 6.4.17 AGG Power Solutions

- 6.4.18 Yamaha Motor Co. (Industrial Engines)

- 6.4.19 Oerlikon Welding (Air Liquide)

- 6.4.20 Westinghouse Outdoor Power

- 6.4.21 Kipor Power

- 6.4.22 Daihen Corp.

- 6.4.23 Riland Industrial Co.

- 6.4.24 Rental Fleet Leaders (United Rentals, Sunbelt)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

焊接設備市場-2026-2032年全球市場預測焊接設備、配件及耗材市場-2026-2032年全球市場預測

焊接設備市場-2026-2032年全球市場預測焊接設備、配件及耗材市場-2026-2032年全球市場預測 2026年全球管道焊接轉子市場報告

2026年全球管道焊接轉子市場報告 等離子焊接機市場:全球產業規模、市場佔有率、趨勢、機會和預測(按類型、分銷管道、應用和地區分類)、競爭格局(2021-2031 年)

等離子焊接機市場:全球產業規模、市場佔有率、趨勢、機會和預測(按類型、分銷管道、應用和地區分類)、競爭格局(2021-2031 年) 牙科實驗室焊接機市場規模、佔有率和成長分析:按類型、技術、應用、最終用途和地區分類-2026-2033年產業預測

牙科實驗室焊接機市場規模、佔有率和成長分析:按類型、技術、應用、最終用途和地區分類-2026-2033年產業預測 焊接機械市場規模、佔有率和成長分析:按產品類型、自動化程度、最終用途和地區分類-2026-2033年產業預測

焊接機械市場規模、佔有率和成長分析:按產品類型、自動化程度、最終用途和地區分類-2026-2033年產業預測 2026-2030年全球焊接設備市場

2026-2030年全球焊接設備市場 焊接設備市場:依自動化程度、焊接技術、應用和地區分類

焊接設備市場:依自動化程度、焊接技術、應用和地區分類 全球焊接市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球焊接市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 焊接設備市場規模、佔有率和趨勢分析報告:按技術、類型、應用、地區和細分市場分類(2026-2033 年)

焊接設備市場規模、佔有率和趨勢分析報告:按技術、類型、應用、地區和細分市場分類(2026-2033 年)